- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Cloud Workload Protection Platform Market Size, Share | CAGR 19.6%

Global Cloud Workload Protection Platform Market Size, Share, Analysis By Component (Solutions, Services), By Deployment Environment (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type (Runtime Protection, CSPM, CIEM, Container & Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size (Large Enterprises, SMBs), By End-User (BFSI, Government, Healthcare, IT & Telecommunications, Retail, Manufacturing) Industry Trends, Market Dynamics & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 5.24 Billion | USD 26.20 Billion | 19.6% | North America, 44.5% |

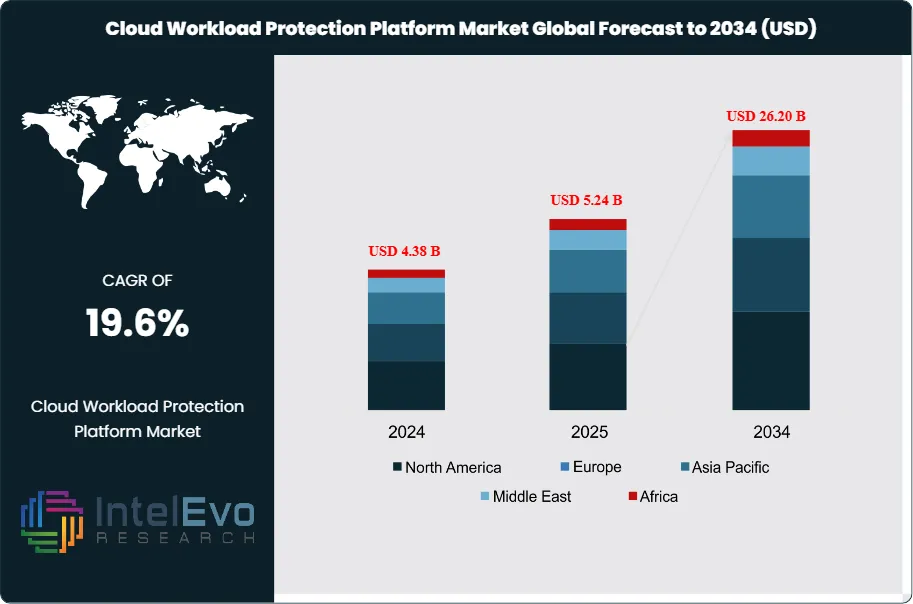

The Cloud Workload Protection Platform Market was valued at approximately USD 4.38 Billion in 2024 and reached USD 5.24 Billion in 2025. The market is projected to grow to USD 26.20 Billion by 2034, expanding at a CAGR of 19.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.96 Billion over the analysis period, a trajectory anchored by three converging forces: container and Kubernetes production adoption crossing 78% of Fortune 1000 enterprises in Q2 2025, CISA binding operational directive BOD-25-01 requiring federal civilian agencies to deploy workload-level runtime protection across cloud infrastructure, and the consolidation of fragmented point tools (CSPM, CIEM, CNAPP, container security) into unified cloud workload protection platforms that enterprise buyers prefer over three-to-five-vendor stacks.

Get More Information about this report -

Request Free Sample ReportDemand-side dynamics accelerated following Google's March 2025 announced acquisition of Wiz for USD 32 Billion, which signaled to enterprise CISOs that hyperscaler-integrated cloud security is a board-level technology bet rather than a point-tool procurement. The transaction valued Wiz at approximately 40x forward revenue, an economic signal that triggered accelerated budget approvals for CWPP platforms at Fortune 500 enterprises previously delaying cloud security modernization. DORA enforcement across EU financial institutions from January 2025 required continuous monitoring of cloud workload integrity at 1,800+ regulated entities, effectively expanding the addressable European market for cloud workload protection platforms by EUR 580 Million annually. The SEC's Cybersecurity Disclosure Rule extended to cloud infrastructure breaches during 2024-2025 enforcement actions, including two Item 1.05 Form 8-K disclosures in Q3 2025 that explicitly cited inadequate workload runtime visibility as a contributing factor.

Technology inflection points in the cloud workload protection platform market reshaped procurement economics during 2024-2025. eBPF-based agent architectures reached production maturity at all major vendors during Q1 2025, reducing workload performance overhead from 8-12% (typical for kernel-module agents) to under 2% across Linux container runtimes, a capability threshold that removed the primary buyer objection at performance-sensitive workloads including high-frequency trading and real-time inference. AI-driven behavioral anomaly detection on cloud workloads, embedded within platforms from Palo Alto Networks Prisma Cloud, CrowdStrike Falcon Cloud Security, and Microsoft Defender for Cloud, reduced false-positive rates on container runtime alerts from an industry-typical 28-34% to 6-8% by Q4 2025. This growth pattern mirrors the EDR market's 2017-2020 trajectory when behavioral detection and cloud-delivered architectures drove concentrated compound growth before market consolidation through the early 2020s.

While headline growth figures suggest broad vendor participation, revenue concentration among the top five vendors tightened from 52% in 2022 to 64% in 2025, a consolidation driven by the engineering depth required to span multi-cloud workload coverage (AWS, Azure, GCP, Oracle, IBM) and the capital intensity of ML-based detection model training. Preliminary Q1 2025 procurement data suggests enterprises renewing annual cloud security contracts averaged 2.8 vendors in 2025 against 4.2 vendors in 2023, a consolidation that favors unified CNAPP-class vendors and penalizes point-tool specialists. Regional investment hotspots include Israel's cybersecurity cluster (which generated USD 1.6 Billion in CWPP-adjacent Series B through D funding during 2025), the Santa Clara-Palo Alto corridor anchoring Palo Alto Networks, Zscaler, and Sysdig operations, and Bangalore's emerging cloud security engineering base where CrowdStrike, Wiz, and Trend Micro expanded headcount by a combined 3,400 during 2024-2025. The cloud workload protection platform market sits at the intersection of cloud-native application adoption, regulatory compliance enforcement, and platform consolidation economics, a combination that supports the forecast growth path through 2034.

, By Deployment Environment (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type (Runtime Protection, CSPM, CIEM, Container & Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size (Large Enterprises, SMBs), By End-User (BFSI, Government, Healthcare, IT & Telecommunications, Retail, Manufacturing) Industry Trends, Market Dynamics & Forecast 2026-2034")

Key Takeaways

- Market Growth: The cloud workload protection platform market expanded from USD 5.24 Billion in 2025 toward a projected USD 26.20 Billion by 2034, registering a 19.6% CAGR driven by Kubernetes production adoption at 78% of Fortune 1000 enterprises, DORA regulatory obligations, and the Google-Wiz USD 32 Billion acquisition signaling hyperscaler commitment to the category.

- Segment Dominance: Runtime protection captured 41.8% of 2025 revenue because kernel-level behavioral monitoring provides the only defense against zero-day container escape exploits, with eBPF agent maturation during Q1 2025 reducing performance overhead to under 2% and removing the primary historical buyer objection at performance-sensitive workloads.

- Segment Dominance: Public cloud deployments represented 68.4% of 2025 environment-based revenue because AWS, Azure, and GCP workloads dominate enterprise net-new cloud adoption and the hyperscaler shared-responsibility model explicitly places workload security outside native cloud provider coverage, creating structural demand for third-party CWPP platforms.

- Driver: CISA binding operational directive BOD-25-01 effective March 2025 required federal civilian executive branch agencies to deploy workload-level runtime protection across cloud infrastructure, routing USD 840 Million of federal cybersecurity budget toward CWPP procurement through FY26 and concentrating demand at FedRAMP High authorized platforms.

- Restraint: Multi-cloud integration complexity and cloud-native application skills shortages compressed deployment velocity, with enterprises averaging 14.8 months from CWPP procurement to full production rollout across 80% of workloads, a timeline that constrains recognized revenue growth at vendors despite strong booking trajectories.

- Opportunity: Kubernetes and container-specific workload protection represents a USD 7.8 Billion addressable opportunity through 2030, unlocked by the 340% increase in production Kubernetes clusters between 2022 and 2025 and NIST SP 800-190 Revision 1 updates formalizing container security baseline requirements for federal workloads.

- Trend: CNAPP consolidation eliminating standalone CSPM, CIEM, and container security point tools reached 62% of Fortune 500 cloud security renewals in 2025, with adoption concentrated at 71% in North American enterprises against 38% in Asia Pacific, a diffusion gap driving vendor M&A activity totaling USD 38 Billion during 2024-2025.

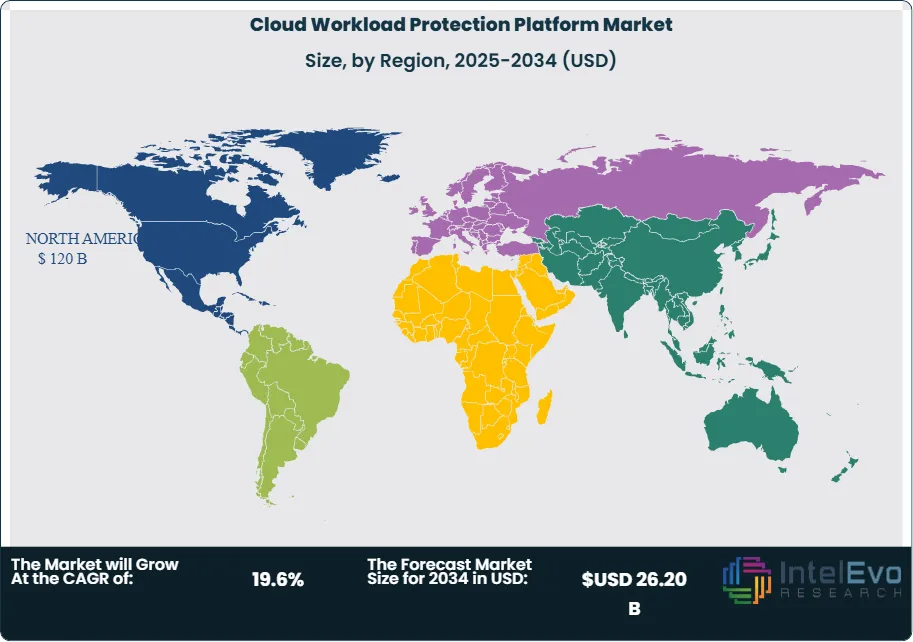

- Regional Analysis: North America led with 44.5% market share worth USD 2.33 Billion in 2025, supported by federal CISA directives, Silicon Valley-based hyperscaler ecosystem density, and the concentration of FedRAMP High authorized CWPP vendors serving the USD 120 Billion US federal cybersecurity budget allocation.

Competitive Landscape Overview

The cloud workload protection platform market is moderately consolidated. The top four vendors controlled 53.2% of 2025 revenue, a concentration that rose 8 percentage points since 2022 as unified CNAPP platforms displaced multi-vendor point-tool stacks. Competition runs on three axes: breadth of cloud and workload coverage (VMs, containers, serverless, Kubernetes, databases), depth of runtime behavioral detection at low performance overhead, and integration with DevSecOps pipelines through IaC scanning and pre-deployment policy enforcement. Four vertical integration deals valued at a combined USD 38 Billion closed or were announced during 2024-2025 including Google's USD 32 Billion offer for Wiz, Palo Alto Networks' USD 1.6 Billion acquisition of Dig Security, and CrowdStrike's USD 2.1 Billion acquisition of Flow Security, all consolidating the category around platform breadth rather than point-tool excellence.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Regional Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Palo Alto Networks | USA | Leader | Prisma Cloud | Global | Acquired Dig Security for USD 1.6B in Oct 2024 to extend data security posture management within Prisma Cloud |

| CrowdStrike Holdings | USA | Leader | Falcon Cloud Security | North America, Europe | Acquired Flow Security for USD 2.1B in Mar 2025 adding DSPM and data-centric CWPP capabilities |

| Wiz Inc. (Google Cloud) | USA/Israel | Leader | Wiz Cloud Security Platform | Global | Google announced USD 32B acquisition in Mar 2025, expected to close H2 2026 pending regulatory review |

| Microsoft Corporation | USA | Leader | Defender for Cloud | Global | Launched Defender for Cloud P3 tier in Jun 2025 with AI Copilot for Security integration across workloads |

| Trend Micro | Japan/USA | Challenger | Trend Vision One Cloud | Asia Pacific, Europe | Released Vision One Zero Trust Secure Access for cloud workloads in Feb 2025 with native AWS Outposts support |

| Check Point Software | Israel | Challenger | CloudGuard CNAPP | Europe, MEA | Acquired Perimeter 81 integration completed Q1 2025 extending SASE and CWPP unified offering |

| Sysdig Inc. | USA | Challenger | Sysdig Secure | North America | Raised USD 195M Series G at USD 2.6B valuation Sep 2025, funding Kubernetes runtime protection R&D |

| Aqua Security | Israel | Niche Player | Aqua Platform | North America, Europe | Launched Aqua AI Guard for generative AI workload protection in Nov 2025 targeting LLMOps security |

By Component.

Solutions (software and platform subscriptions) captured 72.6% of cloud workload protection platform market revenue in 2025 at USD 3.80 Billion because the category is fundamentally software-delivered and consumption is measured in protected-workload or protected-agent pricing models. Within solutions, CNAPP-class unified platforms represented 58% of component revenue, a share that rose from 34% in 2022 as enterprises consolidated point tools. Standalone CSPM tools declined 14% year-over-year in 2025 as customers migrated to unified CNAPP offerings at annual renewal. Services represented 27.4% of revenue at USD 1.44 Billion, concentrated at deployment, integration, and managed detection services. Managed CWPP services grew fastest at 24.8% annually as enterprises faced the 340,000-role cybersecurity hiring gap and outsourced 24/7 SOC-adjacent workload monitoring to providers including CrowdStrike Falcon Complete, Trend Micro Managed XDR, and Sysdig Sysdig Secure MDR. Professional services for multi-cloud migration and DevSecOps integration grew at 18.2%, reflecting enterprise investment in CWPP rollout rather than pure shelf-ware spend.

By Deployment Environment.

Public cloud deployments represented 68.4% of 2025 environment-based revenue at USD 3.58 Billion because AWS, Azure, and GCP workloads dominate enterprise net-new cloud adoption and the hyperscaler shared-responsibility model explicitly places workload security outside native cloud provider coverage. AWS-hosted workloads accounted for approximately 41% of public cloud CWPP protected seats, Azure 32%, GCP 18%, with Oracle Cloud, IBM Cloud, and Alibaba Cloud comprising the remaining 9%. Private cloud deployments held 21.8% share at USD 1.14 Billion, concentrated at regulated industries (BFSI, healthcare, federal) where data residency and control frameworks favor VMware vSphere, OpenStack, and IBM Cloud Pak-based workloads. Hybrid cloud deployments captured 9.8% share, growing fastest at 27.4% annually as enterprises standardized single-pane-of-glass workload protection across public and private environments.

By Protection Type.

Runtime protection led the cloud workload protection platform market with 41.8% share worth USD 2.19 Billion in 2025 because kernel-level behavioral monitoring provides the only defense against zero-day container escape exploits and eBPF agent maturation during Q1 2025 reduced performance overhead to under 2%. Configuration and compliance management (CSPM-class capabilities) captured 24.6% share, a mature sub-segment growing at 12.4% as CSPM functionality increasingly bundles into broader CNAPP platforms rather than selling standalone. Identity and entitlements (CIEM-class capabilities) represented 14.8% share, accelerating at 26.3% annually as enterprises addressed the cloud permissions sprawl where the average AWS account in 2025 exhibited 4,200 over-provisioned IAM entitlements. Container and Kubernetes security held 13.4% share, and vulnerability management specifically for cloud workloads captured 5.4%. The runtime plus CIEM combination dominates procurement at security-mature enterprises as these two capabilities specifically address cloud-native threat vectors that traditional endpoint tools cannot detect.

By Organization Size.

Large enterprises (500+ employees) captured 68.2% of cloud workload protection platform market revenue in 2025 at USD 3.57 Billion because complex multi-cloud footprints, regulatory exposure, and dedicated cloud security engineering teams make enterprise buyers the primary CWPP consumer. Within large enterprises, Fortune 2000 accounts represented 42% of enterprise segment revenue, reflecting concentration at the largest cloud spenders. SMBs (under 500 employees) represented 31.8% of revenue at USD 1.67 Billion, the fastest-growing segment at 27.8% annually as cloud-native startups increasingly ran Kubernetes and serverless workloads from day one that required workload-specific protection. The SMB segment is dominated by self-service cloud-delivered platforms with flat-rate pricing, whereas enterprise procurement favors negotiated multi-cloud ELAs with dedicated customer success resources. Vendor go-to-market strategies diverge accordingly: Wiz and Lacework compete aggressively at mid-market with product-led growth, while Palo Alto Networks and CrowdStrike concentrate field sales effort at Fortune 2000 accounts.

Regional Analysis

North America.

Backed by federal CISA directives, Silicon Valley-based hyperscaler ecosystem density, and the concentration of FedRAMP High authorized CWPP vendors serving the USD 120 Billion US federal cybersecurity budget allocation, North America's cloud workload protection platform market captured 44.5% of 2025 revenue at USD 2.33 Billion. The Santa Clara-Palo Alto corridor anchors Palo Alto Networks, Zscaler, and Sysdig operations, generating an estimated USD 680 Million in 2025 revenue. Austin's cybersecurity cluster hosts CrowdStrike's headquarters and supporting R&D, and the DC-Maryland-Virginia federal technology corridor concentrates federal CWPP procurement through GSA Schedule 70 and the DISA Cloud Computing Program Office. Canada's Communications Security Establishment expanded cloud workload protection procurement under CAD 310 Million in 2024-2025 allocations, with Toronto-based Shopify, OpenText, and Telus among the largest private sector CWPP adopters. Mexico's emerging CWPP market was constrained by cloud security skills shortages, with cross-border managed services from US-based MSSPs representing an estimated 61% of Mexican enterprise CWPP consumption in 2025.

Europe.

Regulatory enforcement under the Digital Operational Resilience Act (DORA Regulation 2022/2554) in force from January 2025, combined with the EU AI Act's computational infrastructure protection provisions, reshaped procurement patterns across the European cloud workload protection platform market, which held 26.8% share worth USD 1.40 Billion in 2025. DORA required continuous monitoring of cloud workload integrity at 1,800+ EU financial institutions, generating an estimated EUR 580 Million in incremental CWPP demand annually. Germany's BSI C5 cloud compliance framework and the Bundesamt fur Sicherheit in der Informationstechnik updated guidance in Q2 2025 explicitly requiring workload-level runtime protection at operators of critical infrastructure. Frankfurt, Munich, and Berlin concentrated enterprise CWPP procurement at SAP, Deutsche Bank, and Siemens respectively. The UK's National Cyber Security Centre Cloud Security Guidance 2025 edition formalized workload protection expectations, and the Financial Conduct Authority CP24/22 extended operational resilience obligations to cloud workload security posture. France's ANSSI SecNumCloud qualification for sovereign cloud workloads expanded to eight additional providers during 2025, creating compliance-driven demand for qualifying CWPP platforms. The Netherlands and Ireland concentrated multinational CWPP procurement through EMEA headquarters of AWS, Google, and Meta.

Asia Pacific.

Manufacturing capacity for cloud infrastructure and Kubernetes platform engineering across Hyderabad, Bangalore, and Hangzhou, combined with Japan's METI cybersecurity resilience funding, propelled Asia Pacific's cloud workload protection platform market to 19.4% global share, valued at USD 1.02 Billion in 2025. India accounted for the fastest-growing country-level market globally at 29.8% annual growth, driven by CERT-In cybersecurity reporting obligations, the Digital Personal Data Protection Act of 2023 enforcement beginning in 2025, and Bangalore's emerging cloud security engineering base where CrowdStrike, Wiz, and Trend Micro expanded headcount by a combined 3,400 during 2024-2025. China's Cybersecurity Law and the 2024 Data Security Law enforcement by the Cyberspace Administration of China drove domestic CWPP adoption at state-owned enterprises, though Western vendor access remained constrained by the Measures for Network Data Security Management effective September 2024. Japan's cybersecurity market benefited from the 2024 Active Cyber Defense legislation, and the METI cloud security funding program allocated JPY 18 Billion toward enterprise CWPP rollouts. Singapore's Cyber Security Agency anchored an ASEAN-wide CWPP procurement framework, with the IMDA accrediting 22 CWPP vendors for government cloud workloads by Q3 2025.

Latin America.

Currency volatility across Argentina and cloud skills shortages constrained direct enterprise CWPP procurement, yet Latin America's cloud workload protection platform market still reached USD 267 Million (5.1% global share) in 2025, driven primarily by Brazilian BFSI sector demand and expanding managed security service provider adoption. Brazil's LGPD enforcement by the Autoridade Nacional de Protecao de Dados and the Banco Central's Resolucao 4893 cybersecurity framework for financial institutions created binding compliance drivers for CWPP adoption at Itau Unibanco, Bradesco, Banco do Brasil, and Santander Brasil. Sao Paulo's Faria Lima financial corridor concentrated an estimated 58% of regional CWPP procurement. Mexico's recent COFEPRIS data protection harmonization with Brazil's LGPD framework extended regional data residency requirements that drove CWPP adoption at Mexican financial institutions and public sector cloud migrations. Chile's Ley Marco de Ciberseguridad effective 2025 established the first binding cloud workload protection framework in the Southern Cone. Argentina's pure-play CWPP market faced 31% peso depreciation constraints, pushing enterprises toward Brazilian and Uruguayan regional managed CWPP consumption.

Middle East & Africa.

Saudi Arabia's National Cybersecurity Authority mandates and the UAE's Cybersecurity Council cloud strategy opened a new demand corridor, pushing the MEA cloud workload protection platform market to USD 220 Million (4.2% share) in 2025. Saudi Arabia's NCA Essential Cybersecurity Controls (ECC-2:2024 update) explicitly required cloud workload runtime protection at critical national infrastructure operators including Saudi Aramco, SABIC, and STC Group. The UAE's 2024 cybersecurity strategy and the Dubai Electronic Security Center framework accredited 14 CWPP vendors for government cloud workloads by Q3 2025, and G42 Cloud's Abu Dhabi operations became the largest regional CWPP deployment reference. Israel remains the region's technology origin hub with Tel Aviv hosting Wiz, Check Point, Aqua Security, and Orca Security R&D operations, generating an estimated USD 110 Million in domestic Israeli market revenue but far larger global revenue attribution through Israeli-founded vendors. Qatar's National Cyber Security Agency and Oman's Information Technology Authority released 2025 cloud security guidelines driving public sector CWPP procurement. South Africa's POPIA enforcement by the Information Regulator drove demand at Johannesburg's banking sector. The region's shortage of cloud security engineers remains a structural constraint, with fewer than 4,800 certified cloud security practitioners across the entire MEA geography as of 2025.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Solutions (Software and Platform Subscriptions)

- Services (Deployment, Managed Detection, Professional Services)

By Deployment Environment

- Public Cloud

- Private Cloud

- Hybrid Cloud

By Protection Type

- Runtime Protection

- Configuration and Compliance Management (CSPM)

- Identity and Entitlements Management (CIEM)

- Container and Kubernetes Security

- Cloud Workload Vulnerability Management

By Organization Size

- Large Enterprises (500+ Employees)

- Small and Medium-Sized Businesses (SMBs)

By End-User

- Banking, Financial Services, and Insurance (BFSI)

- Government and Defense

- Healthcare and Life Sciences

- IT and Telecommunications

- Retail and E-Commerce

- Manufacturing and Industrial

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.24 B |

| Forecast Revenue (2034) | USD 26.20 B |

| CAGR (2025-2034) | 19.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Solutions (Software and Platform Subscriptions), Services (Deployment, Managed Detection, Professional Services)), By Deployment Environment, (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type, (Runtime Protection, Configuration and Compliance Management (CSPM), Identity and Entitlements Management (CIEM), Container and Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size, (Large Enterprises (500+ Employees), Small and Medium-Sized Businesses (SMBs)), By End-User, (Banking, Financial Services, and Insurance (BFSI), Government and Defense, Healthcare and Life Sciences, IT and Telecommunications, Retail and E-Commerce, Manufacturing and Industrial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PALO ALTO NETWORKS, INC., CROWDSTRIKE HOLDINGS, INC., WIZ INC. (GOOGLE CLOUD), MICROSOFT CORPORATION, TREND MICRO INCORPORATED, CHECK POINT SOFTWARE TECHNOLOGIES LTD., SYSDIG INC., AQUA SECURITY SOFTWARE LTD., ORCA SECURITY LTD., LACEWORK, INC., QUALYS, INC., TENABLE HOLDINGS, INC., FORTINET, INC., RAPID7, INC., SENTINELONE, INC., CISCO SYSTEMS, INC., SOPHOS LTD., VMWARE (BROADCOM), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Environment (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type (Runtime Protection, CSPM, CIEM, Container & Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size (Large Enterprises, SMBs), By End-User (BFSI, Government, Healthcare, IT & Telecommunications, Retail, Manufacturing) Industry Trends, Market Dynamics & Forecast 2026-2034")

, By Deployment Environment (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type (Runtime Protection, CSPM, CIEM, Container & Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size (Large Enterprises, SMBs), By End-User (BFSI, Government, Healthcare, IT & Telecommunications, Retail, Manufacturing) Industry Trends, Market Dynamics & Forecast 2026-2034")

, By Deployment Environment (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type (Runtime Protection, CSPM, CIEM, Container & Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size (Large Enterprises, SMBs), By End-User (BFSI, Government, Healthcare, IT & Telecommunications, Retail, Manufacturing) Industry Trends, Market Dynamics & Forecast 2026-2034")

Frequently Asked Questions

How big is the Cloud Workload Protection Platform Market?

The Global Cloud Workload Protection Platform Market was valued at USD 4.38 Billion in 2024 and is projected to reach USD 26.20 Billion by 2034, growing at a CAGR of 19.6% from 2026 to 2034. Growth is driven by increasing adoption of multi-cloud and hybrid cloud environments, rising cloud security threats, expanding DevSecOps practices, Zero Trust security implementation, regulatory compliance requirements, and growing demand for AI-powered workload protection, runtime security, and vulnerability management solutions across global enterprises.

Who are the major players in the Cloud Workload Protection Platform Market?

PALO ALTO NETWORKS, INC., CROWDSTRIKE HOLDINGS, INC., WIZ INC. (GOOGLE CLOUD), MICROSOFT CORPORATION, TREND MICRO INCORPORATED, CHECK POINT SOFTWARE TECHNOLOGIES LTD., SYSDIG INC., AQUA SECURITY SOFTWARE LTD., ORCA SECURITY LTD., LACEWORK, INC., QUALYS, INC., TENABLE HOLDINGS, INC., FORTINET, INC., RAPID7, INC., SENTINELONE, INC., CISCO SYSTEMS, INC., SOPHOS LTD., VMWARE (BROADCOM), OTHERS

Which segments covered the Cloud Workload Protection Platform Market?

By Component, (Solutions (Software and Platform Subscriptions), Services (Deployment, Managed Detection, Professional Services)), By Deployment Environment, (Public Cloud, Private Cloud, Hybrid Cloud), By Protection Type, (Runtime Protection, Configuration and Compliance Management (CSPM), Identity and Entitlements Management (CIEM), Container and Kubernetes Security, Cloud Workload Vulnerability Management), By Organization Size, (Large Enterprises (500+ Employees), Small and Medium-Sized Businesses (SMBs)), By End-User, (Banking, Financial Services, and Insurance (BFSI), Government and Defense, Healthcare and Life Sciences, IT and Telecommunications, Retail and E-Commerce, Manufacturing and Industrial)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cloud Workload Protection Platform Market

Published Date : 09 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date