- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Companion Diagnostic Market Size, Share & Forecast | CAGR 10.5%

Global Companion Diagnostic Market Size, Share Analysis By Tech (PCR, NGS, IHC, ISH, FISH, dPCR, Gene Expression, DNA Seq, Microarray), By Indication (Oncology, Cardiovascular, Neurology, Infection, Autoimmune, Rare Genetic), By Product (Assays, Kits, Instruments, Software, Panels, Consumables), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 8.70 Billion | USD 21.40 Billion | 10.5% | North America, 42.0% |

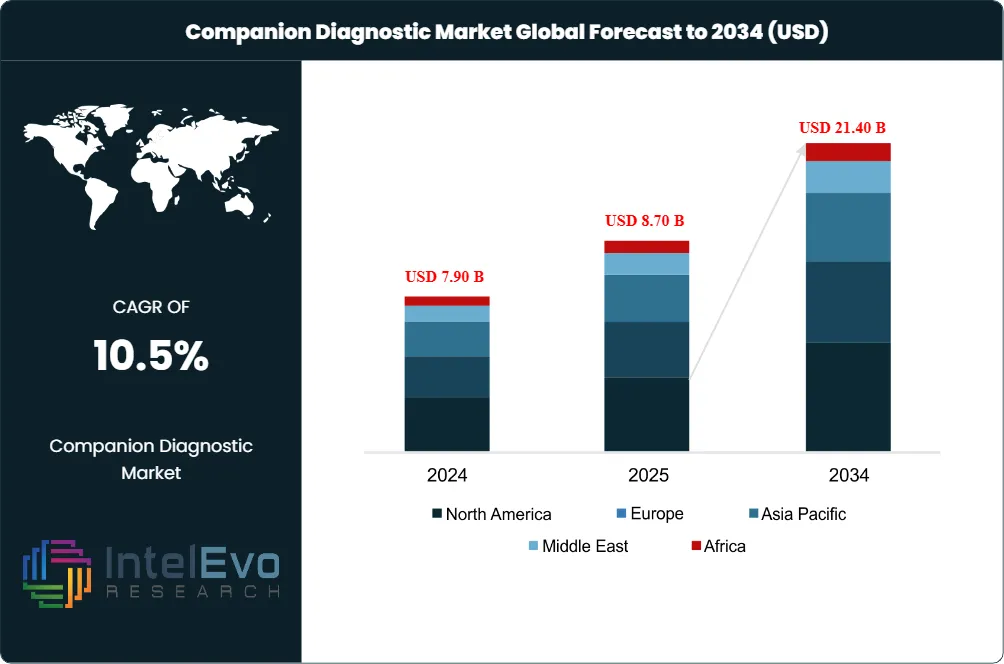

The Companion Diagnostic Market was valued at USD 7.90 Billion in 2024 and USD 8.70 Billion in 2025. The market is projected to reach USD 21.40 Billion by 2034, expanding at a CAGR of 10.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 12.70 Billion over the analysis period. The Companion Diagnostic Market is expanding because targeted therapies now require a paired biomarker test for safe and effective prescribing, and because the FDA had approved more than 78 drug-CDx combinations by early 2025 across oncology, hematology, and rare disease.

Get More Information about this report -

Request Free Sample ReportDemand-side momentum is anchored to the precision-medicine pipeline. Approximately 65% of FDA and EMA drug approvals between 2015 and 2019 included at least one biomarker consideration, and personalized medicines accounted for 25% of all FDA new drug approvals in 2019. The US National Cancer Institute reports nearly 1.9 million new cancer diagnoses annually in the United States, driving sustained volume in CDx testing for non-small-cell lung cancer, breast cancer, colorectal cancer, and melanoma. UnitedHealthcare's policy to reimburse FDA-approved CDx paired with the corresponding drug has stabilized payer adoption across the US commercial book.

Regulatory clarity is reinforcing market expansion. The FDA's tissue-agnostic drug framework has driven nine new molecular entity approvals through 2025 with paired CDx requirements. The EU In Vitro Diagnostic Regulation 2017/746 now classifies CDx as Class C devices requiring notified body assessment plus EMA consultation when linked to centrally authorized medicines. Japan's Pharmaceuticals and Medical Devices Agency issued a partial revision of its Drug-Agnostic Companion Diagnostics guidance on September 5, 2025, then accepted in January 2026 a Japanese Society of Medical Oncology proposal for drug-agnostic mismatch-repair CDx. These frameworks force pharmaceutical companies to co-develop a CDx alongside any biomarker-stratified therapy.

Technology shifts inside the Companion Diagnostic Market are restructuring vendor positioning. Polymerase chain reaction held the largest 2025 share at 28.0%, driven by therascreen, cobas, and Oncomine PCR kits in oncology and infectious disease. NGS is the fastest-growing technology, projected to expand at a 14.3% CAGR through 2030 as broad-panel sequencing assays such as FoundationOne CDx and TSO Comprehensive consolidate multiple single-gene tests into one workflow. Liquid biopsy adoption is accelerating, with Guardant360 CDx, FoundationOne Liquid CDx, and Reveal expanding non-invasive testing across breast, lung, and colorectal indications.

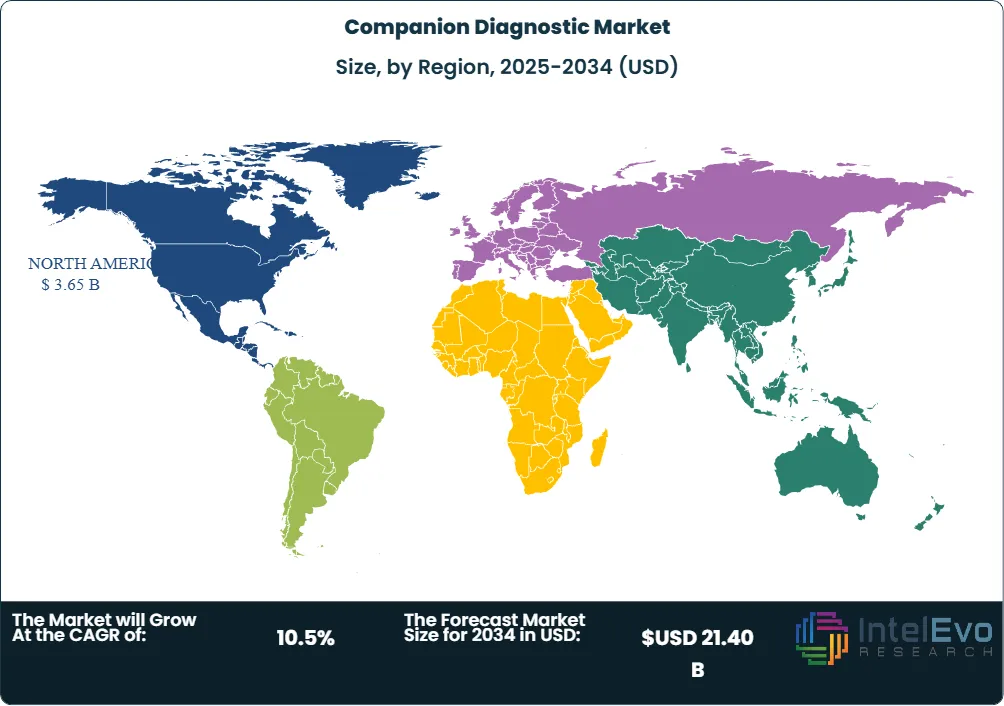

Regional concentration is high. North America held 42.0% of revenue in 2025 at approximately USD 3.65 Billion, supported by US NIH research obligations exceeding USD 47 Billion in fiscal year 2025 and the largest installed base of FDA-approved CDx assays globally. Europe held 25.3%, anchored by IVDR-compliant launches across Germany, France, and the United Kingdom. Asia Pacific is the fastest-growing region at a CAGR of 12.3% through 2034, driven by China NMPA, Japan PMDA, and Korea MFDS synchronized drug-CDx submissions. The Companion Diagnostic Market by 2034 will be defined by vendors that combine NGS depth with liquid-biopsy reach and pharma co-development scale.

Market Definition & Scope

The Companion Diagnostic Market is defined as the global market for in vitro diagnostic devices that provide information essential for the safe and effective use of a corresponding therapeutic drug or biological product. The market encompasses assays, kits, reagents, instruments, software, and laboratory services that detect biomarkers including gene mutations, gene fusions, gene expression, protein expression, and microsatellite instability across tissue and blood samples to determine patient eligibility for targeted therapy.

This analysis includes FDA-approved, CE-marked, and PMDA-approved CDx assays across PCR, NGS, immunohistochemistry, in situ hybridization, and flow cytometry technologies. The scope explicitly excludes complementary diagnostics, prognostic-only tests without therapy linkage, general clinical chemistry assays, infectious disease screening unrelated to therapy selection, and at-home consumer genetic tests. The Companion Diagnostic Market sits within the parent in vitro diagnostics market valued at approximately USD 110 Billion in 2025, representing roughly 7.9% of total IVD revenue.

, By Indication (Oncology, Cardiovascular, Neurology, Infection, Autoimmune, Rare Genetic), By Product (Assays, Kits, Instruments, Software, Panels, Consumables), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Companion Diagnostic Market grew from USD 8.70 Billion in 2025 to a projected USD 21.40 Billion by 2034 at a CAGR of 10.5%, an absolute dollar opportunity of USD 12.70 Billion.

- Segment Dominance (Technology): Polymerase chain reaction held the largest share at 28.0% of revenue in 2025, anchored by therascreen, cobas EGFR, and Oncomine PCR kits across oncology indications.

- Segment Dominance (Indication): Non-small-cell lung cancer captured 22.5% of revenue in 2025, reflecting the depth of EGFR, ALK, ROS1, KRAS G12C, RET, and HER2 biomarker testing required for targeted-therapy selection.

- Driver: By early 2025 the FDA had approved more than 78 drug-CDx combinations, with biomarker-stratified therapies driving roughly 25% of FDA new drug approvals in 2019 and rising through 2025.

- Restraint: The mean delay between drug approval and corresponding CDx approval reached 707 days for tissue-agnostic indications, slowing patient access and complicating reimbursement timing.

- Opportunity: NGS-based CDx is projected to expand at a 14.3% CAGR through 2030, opening an addressable opportunity of approximately USD 6.40 Billion as broad-panel tumor profiling consolidates single-gene tests.

- Trend: Liquid-biopsy CDx adoption accelerated through 2025-2026 on FDA approvals of Guardant360 CDx for ESR1 in breast cancer and Foundation Medicine F1 Liquid CDx label expansions, opening non-invasive testing across multiple solid tumors.

- Regional: North America led the Companion Diagnostic Market at 42.0% share or roughly USD 3.65 Billion in 2025, while Asia Pacific is projected to grow fastest at a 12.3% CAGR through 2034.

Key Insights Summary

- By early 2025 the FDA had approved more than 78 drug-CDx combinations, with paired biomarker tests now extending beyond antibody-based drugs to kinase inhibitors, antibody-drug conjugates, and small-molecule targeted therapies, per peer-reviewed analysis published in Frontiers in Oncology in September 2025.

- On September 29, 2025, the FDA approved Guardant360 CDx as a companion diagnostic for Eli Lilly's imlunestrant (Inluriyo) in ESR1-mutated advanced breast cancer, the sixth FDA-approved indication for the Guardant360 CDx assay.

- On November 19-20, 2025, the FDA approved Thermo Fisher Scientific's Oncomine Dx Target Test as a companion diagnostic for Bayer's sevabertinib in HER2 TKD-mutated non-small-cell lung cancer following a 71% objective response rate in the phase 1/2 SOHO-01 trial.

- QIAGEN reported companion diagnostic revenue growth exceeding 20% CER in both Q2 2025 and Q3 2025 driven by NGS, QIAcuityDx digital PCR, and QIAstat-Dx pharmaceutical partnerships, with new CDx programs announced for Incyte CALR mutations and Foresight Diagnostics CLARITY ctDNA in lymphoma.

- On January 19, 2026, Guardant Health and Merck signed a multi-year strategic CDx collaboration covering trial enrollment assays, novel drug-CDx co-development, and global commercialization of liquid-biopsy CDx using the Guardant Infinity Smart platform across the United States, EU, UK, and Asia Pacific.

- Japan PMDA issued a partial revision of its Drug-Agnostic Companion Diagnostics Guidance on September 5, 2025, then accepted a January 13, 2026 Japanese Society of Medical Oncology proposal to use mismatch-repair CDx in a drug-agnostic manner, expanding tissue-agnostic CDx pathways outside the United States.

- Tissue samples held 62.7% of CDx revenue in 2025 while liquid-biopsy blood samples grew fastest, reflecting the structural shift toward minimally invasive testing as Guardant360 CDx, FoundationOne Liquid CDx, and AmoyDx panels expanded label coverage.

Competitive Landscape Overview

The Companion Diagnostic Market is moderately consolidated. The top four vendors, F. Hoffmann-La Roche through Roche Diagnostics and Foundation Medicine, Thermo Fisher Scientific, QIAGEN N.V., and Agilent Technologies through Dako, collectively held approximately 57% of global revenue in 2025 based on aggregated company disclosures. Competition is structured around three vectors: depth of pharmaceutical co-development partnerships, breadth of FDA-approved drug-CDx labels, and platform interoperability spanning IHC, PCR, and NGS technologies. Roche led with roughly 20% share, supported by more than 40 co-developed companion tests and the Foundation Medicine F1CDx pancancer assay.

Competitive evolution accelerated through 2025-2026. Guardant Health entered multi-year strategic CDx collaborations with Merck on January 19, 2026 and with Nuvalent in late April 2026, embedding the Guardant Infinity platform into pharma trial-enrollment workflows. Thermo Fisher secured FDA approval of Oncomine Dx Target Test as a CDx for sevabertinib in November 2025, deepening its NSCLC CDx coverage. QIAGEN expanded its NGS-based CDx pipeline through partnerships with Incyte and Foresight Diagnostics in mid-2025, while Agilent received European IVDR certification for PD-L1 IHC 22C3 pharmDx in April 2025, an entrant defense against Roche's Ventana PD-L1 SP263. The Companion Diagnostic Market is shifting toward liquid-biopsy and pancancer NGS assays where Guardant Health, Foundation Medicine, and Illumina compete head-to-head.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (Trailing 18 Months) |

|---|---|---|---|---|---|

| F. Hoffmann-La Roche | Switzerland | Leader | VENTANA PD-L1; PATHWAY HER2 (4B5); cobas EGFR; Foundation Medicine F1CDx | Global oncology | January 2025 FDA label expansion of PATHWAY HER2 (4B5) for HER2-ultralow metastatic breast cancer |

| Thermo Fisher Scientific | USA | Leader | Oncomine Dx Target Test; Oncomine Dx Express; Ion Torrent Genexus Dx | Global, all regions | November 2025 FDA approval of Oncomine Dx Target as CDx for sevabertinib in NSCLC |

| QIAGEN N.V. | Netherlands | Leader | therascreen KRAS RGQ PCR; QIAcuityDx; QIAstat-Dx; NGS panels | Europe, North America | Q3 2025 companion diagnostic revenue rose over 20% CER on expanding pharma collaborations |

| Agilent Technologies | USA | Leader | PD-L1 IHC 22C3 pharmDx; Dako HercepTest; Resolution Biosciences ctDx | Global oncology pathology | April 2025 European IVDR certification of PD-L1 IHC 22C3 pharmDx assay |

| Illumina | USA | Challenger | TruSight Oncology Comprehensive (TSO 500); MiSeqDx | North America, Europe | August 2024 FDA approval of TSO Comprehensive as pancancer CDx for NTRK and RET fusions |

| Guardant Health | USA | Challenger | Guardant360 CDx; Guardant Infinity Smart platform; Reveal | North America, Asia Pacific | January 2026 multi-year CDx collaboration with Merck plus Guardant360 CDx FDA approval for imlunestrant |

| Foundation Medicine (Roche) | USA | Challenger | FoundationOne CDx; FoundationOne Liquid CDx | Global oncology | FY2025 expansion of F1CDx pancancer CDx labels across multiple targeted therapies |

| Myriad Genetics | USA | Niche Player | BRACAnalysis CDx; myChoice CDx | North America, Europe | FY2025 ongoing BRACAnalysis CDx label expansion for PARP inhibitor combinations |

| Abbott Laboratories | USA | Niche Player | RealTime IDH1; Vysis ALK; mPCR-based CDx assays | North America, Europe | FY2025 expansion of m2000 RealTime System for molecular CDx workflows |

| bioMerieux | France | Niche Player | FilmArray CDx; THxID-BRAF Kit | Europe, Latin America | Q1 2026 partnership-led expansion of multiplex CDx pipeline in oncology |

Segmentation Analysis

The Companion Diagnostic Market is segmented across four primary dimensions that procurement leads and pharmaceutical co-development teams use during partner selection: by technology, by indication, by product type, and by end-user. Each dimension carries distinct economics around assay validation timeline, regulatory pathway, reimbursement, and co-development cost structure.

By Technology

Polymerase chain reaction held the largest share at 28.0% of revenue in 2025, equivalent to approximately USD 2.44 Billion. PCR-based CDx assays such as the QIAGEN therascreen KRAS RGQ Kit, Roche cobas EGFR Mutation Test, and Thermo Fisher Oncomine Dx Target Test deliver high sensitivity, fast turnaround, and low capital cost per result, making them the default for single-biomarker pharma co-development. Immunohistochemistry held 25.0% of revenue at approximately USD 2.18 Billion, anchored by Roche Ventana PD-L1, Agilent PD-L1 IHC 22C3 pharmDx, and Dako HercepTest assays.

NGS held 22.0% of revenue in 2025 at approximately USD 1.91 Billion and is the fastest-growing technology at a CAGR of 14.3% through 2030. NGS adoption is driven by FoundationOne CDx, Illumina TruSight Oncology Comprehensive, and Guardant Infinity, which enable broad genomic profiling of more than 300 to 500 genes in a single workflow. In situ hybridization held 12.0% and other technologies including flow cytometry and mass spectrometry held 13.0%. Procurement leads conducting CDx ROI calculation increasingly favor NGS where annual test volume exceeds 1,500 specimens, because consumable cost amortization tilts in favor of multiplex profiling over a three-year horizon.

By Indication

Non-small-cell lung cancer captured 22.5% of revenue in 2025, reflecting the depth of EGFR, ALK, ROS1, KRAS G12C, RET, MET, NTRK, and HER2 biomarker testing required for targeted therapy selection. Breast cancer held 19.0% with HER2 IHC, ER, PR, and ESR1 mutation testing, accelerated by the September 2025 Guardant360 CDx approval for ESR1. Colorectal cancer held 14.5% on KRAS, NRAS, BRAF, and microsatellite instability testing, while melanoma held 7.5% and is projected to grow fastest at a 13.6% CAGR through 2030 on BRAF V600E and PD-L1 testing.

By Product Type

Assays, kits, and reagents accounted for 59.1% of revenue in 2025, equivalent to approximately USD 5.14 Billion, because these consumables generate recurring revenue tied directly to test volumes and pharmaceutical drug uptake. Software and services held 28.5% of revenue at approximately USD 2.48 Billion, growing on AI-driven biomarker analytics, digital pathology integration, and laboratory developed test compliance support. Instruments and systems held 12.4% of revenue at approximately USD 1.08 Billion, reflecting the long replacement cycle for capital equipment such as Roche cobas analyzers, Thermo Fisher Genexus Dx, and Illumina NextSeq Dx.

By End-User

Pharmaceutical and biopharmaceutical companies represented 46.3% of end-user demand in 2025 at approximately USD 4.03 Billion, driven by trial enrollment assays and regulatory co-development obligations. Hospitals and physician laboratories accounted for 38.6% at approximately USD 3.36 Billion, reflecting the routine deployment of FDA-approved CDx in tertiary cancer centers including Memorial Sloan Kettering, MD Anderson, and Mayo Clinic. Reference laboratories such as Labcorp and Quest Diagnostics held 10.0%, while contract research organizations held 5.1% but are projected to grow fastest at 13.2% CAGR through 2030 as biotechs outsource biomarker validation. Procurement checklists across all end-user types converge on five evaluation criteria: drug-CDx label specificity, FDA premarket approval status, IVDR compliance for European deployment, sample-type flexibility across tissue and liquid biopsy, and pharma-partnership track record for trial enrollment.

Regional Analysis

The Companion Diagnostic Market spans five regions with distinct regulatory pathways, reimbursement frameworks, and pharma co-development concentrations. Regional revenue shares in 2025 were North America at 42.0%, Europe at 25.3%, Asia Pacific at 23.0%, Latin America at 5.2%, and Middle East and Africa at 4.5%.

North America

North America led the Companion Diagnostic Market at 42.0% share or approximately USD 3.65 Billion in 2025, anchored by the United States, Canada, and Mexico. The US installed base alone is estimated at USD 3.40 Billion and is supported by NIH research obligations exceeding USD 47 Billion in fiscal year 2025 and the largest set of FDA-approved drug-CDx combinations globally at more than 78 by early 2025. UnitedHealthcare reimbursement coverage of FDA-approved CDx paired with the corresponding drug stabilized payer adoption. Roche, Thermo Fisher, and Guardant Health dominate domestic revenue, and Guardant Health entered a multi-year CDx collaboration with Merck on January 19, 2026.

Europe

Europe held 25.3% of the Companion Diagnostic Market in 2025, equivalent to approximately USD 2.20 Billion, with Germany, France, the United Kingdom, Italy, and Switzerland as the largest country markets. The EU In Vitro Diagnostic Regulation 2017/746 reclassified CDx as Class C devices requiring notified body assessment and EMA consultation, accelerating compliance investment through 2025-2026. Agilent received European IVDR certification for PD-L1 IHC 22C3 pharmDx in April 2025, and Roche reported 12% sales growth in companion diagnostics across European pathology labs in H1 2025.

Asia Pacific

Asia Pacific captured 23.0% of revenue in 2025 at approximately USD 2.00 Billion and is projected to expand at the fastest regional CAGR of 12.3% through 2034. China, Japan, South Korea, and India lead demand. The Japan PMDA partial revision of Drug-Agnostic CDx Guidance on September 5, 2025, followed by the January 2026 acceptance of mismatch-repair drug-agnostic CDx, opens tissue-agnostic CDx pathways. China NMPA mandates synchronized drug-CDx submissions, and domestic vendors AmoyDx and Burning Rock Biotech are gaining share through partnerships with AstraZeneca and Roche.

Latin America

Latin America accounted for 5.2% of the Companion Diagnostic Market in 2025, approximately USD 0.45 Billion, with Brazil, Mexico, and Argentina as the largest country markets. Brazil's ANVISA and Mexico's Cofepris are aligning CDx review pathways with FDA standards to reduce time-to-launch for global pharma sponsors. Roche, Agilent, and bioMerieux dominate regional supply through distributor networks, while reimbursement variability remains the primary procurement friction.

Middle East and Africa

Middle East and Africa held 4.5% of the Companion Diagnostic Market in 2025, equivalent to approximately USD 0.40 Billion. Saudi Arabia, the UAE, South Africa, and Egypt lead demand, supported by Saudi Vision 2030 healthcare investments and UAE Centennial 2071 precision-medicine programs. The Saudi Food and Drug Authority and UAE Department of Health have aligned IVD-quality standards with FDA and CE-marking frameworks. King Faisal Specialist Hospital and Cleveland Clinic Abu Dhabi expanded NGS-based CDx workflows through 2025.

Country Analysis

Country-level dynamics within the Companion Diagnostic Market vary sharply on regulatory pathway, reimbursement, and pharma co-development concentration. The four most relevant national markets in 2025 are the United States, Germany, China, and Japan, which together account for approximately 67% of global revenue.

United States

The United States Companion Diagnostic Market was valued at approximately USD 3.40 Billion in 2025 and is projected to grow at a country-specific CAGR of 11.5% through 2034. Federal demand drivers include NIH research obligations exceeding USD 47 Billion in fiscal year 2025 and the FDA's tissue-agnostic drug framework that has produced nine new molecular entity approvals through 2025. The FDA approved more than 78 drug-CDx combinations by early 2025, and major 2025 approvals included Guardant360 CDx for imlunestrant in ESR1-mutated breast cancer (September 2025) and Oncomine Dx Target Test for sevabertinib in NSCLC (November 2025). Roche, Thermo Fisher, Guardant Health, and Foundation Medicine together hold an estimated 60% to 65% of US revenue.

Germany

Germany's Companion Diagnostic Market was valued at approximately USD 0.65 Billion in 2025 and is projected to grow at a country-specific CAGR of 9.2% through 2034. The Bundesinstitut fur Arzneimittel und Medizinprodukte enforces EU IVDR compliance, and German university hospitals in Heidelberg, Munich, and Berlin anchor the largest CDx volume in Europe. Domestic vendors include Roche Diagnostics Germany, QIAGEN, and Sysmex Inostics. The German Federal Joint Committee reimbursement framework for biomarker testing in non-small-cell lung cancer accelerated CDx adoption since 2024.

China

China's Companion Diagnostic Market reached an estimated USD 0.95 Billion in 2025 and is forecast to grow at a country-specific CAGR of 13.8% through 2034, the fastest among major economies. China NMPA mandates synchronized drug-CDx submissions, and the 14th Five-Year Plan for Bioeconomy prioritizes precision oncology infrastructure. Domestic vendors AmoyDx, Burning Rock Biotech, and Genecast Biotechnology are gaining share through partnerships with AstraZeneca, Roche, and Bristol-Myers Squibb. AmoyDx and AstraZeneca finalized an ovarian cancer CDx alliance in 2025, while imported CDx from Roche, Thermo Fisher, and Illumina still dominate NGS-based assays in tier-1 hospitals.

Japan

Japan's Companion Diagnostic Market was valued at approximately USD 0.55 Billion in 2025 and is projected to grow at a country-specific CAGR of 8.9% through 2034. The PMDA issued a partial revision of Drug-Agnostic Companion Diagnostics Guidance on September 5, 2025, then accepted on January 13, 2026 a Japanese Society of Medical Oncology proposal to deploy mismatch-repair CDx drug-agnostically. Sysmex Corporation, Konica Minolta, and Riken Genesis anchor domestic CDx supply, while Guardant Health Japan secured MHLW approval of Guardant360 CDx in 2024.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Technology

- Polymerase Chain Reaction (PCR)

- Next-Generation Sequencing (NGS)

- Immunohistochemistry (IHC)

- In Situ Hybridization (ISH)

- Fluorescence In Situ Hybridization (FISH)

- Digital PCR

- Gene Expression Profiling

- DNA Sequencing

- Microarray Technology

- Others

By Indication

- Oncology

- Cardiovascular Diseases

- Neurological Disorders

- Infectious Diseases

- Autoimmune Diseases

- Respiratory Diseases

- Rare Genetic Disorders

- Metabolic Disorders

- Hematological Disorders

- Others

By Product Type

- Assays, Kits, and Reagents

- Instruments

- Software and Bioinformatics Solutions

- Companion Diagnostic Test Panels

- Sequencing Consumables

- Quality Control Materials

- Sample Preparation Kits

- Others

By End-User

- Hospitals

- Diagnostic Laboratories

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutes

- Contract Research Organizations (CROs)

- Reference Laboratories

- Cancer Research Centers

- Specialty Clinics

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.70 B |

| Forecast Revenue (2034) | USD 21.40 B |

| CAGR (2025-2034) | 10.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Immunohistochemistry (IHC), In Situ Hybridization (ISH), Fluorescence In Situ Hybridization (FISH), Digital PCR, Gene Expression Profiling, DNA Sequencing, Microarray Technology, Others), By Indication, (Oncology, Cardiovascular Diseases, Neurological Disorders, Infectious Diseases, Autoimmune Diseases, Respiratory Diseases, Rare Genetic Disorders, Metabolic Disorders, Hematological Disorders, Others), By Product Type, (Assays, Kits, and Reagents, Instruments, Software and Bioinformatics Solutions, Companion Diagnostic Test Panels, Sequencing Consumables, Quality Control Materials, Sample Preparation Kits, Others), By End-User, (Hospitals, Diagnostic Laboratories, Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Contract Research Organizations (CROs), Reference Laboratories, Cancer Research Centers, Specialty Clinics, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | F. HOFFMANN-LA ROCHE, THERMO FISHER SCIENTIFIC, QIAGEN N.V., AGILENT TECHNOLOGIES, ILLUMINA, INC., GUARDANT HEALTH, FOUNDATION MEDICINE, MYRIAD GENETICS, ABBOTT LABORATORIES, BIOMERIEUX, ABNOVA CORPORATION, BIOGENEX LABORATORIES, DAKO (AGILENT), VENTANA MEDICAL SYSTEMS (ROCHE), LEICA BIOSYSTEMS (DANAHER), SYSMEX CORPORATION, BECTON, DICKINSON AND COMPANY, NEOGENOMICS LABORATORIES, NATERA, INC., PERSONALIS, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Indication (Oncology, Cardiovascular, Neurology, Infection, Autoimmune, Rare Genetic), By Product (Assays, Kits, Instruments, Software, Panels, Consumables), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Indication (Oncology, Cardiovascular, Neurology, Infection, Autoimmune, Rare Genetic), By Product (Assays, Kits, Instruments, Software, Panels, Consumables), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Indication (Oncology, Cardiovascular, Neurology, Infection, Autoimmune, Rare Genetic), By Product (Assays, Kits, Instruments, Software, Panels, Consumables), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Companion Diagnostic Market?

The Global Companion Diagnostic Market was valued at USD 7.90 Billion in 2024 and USD 8.70 Billion in 2025, and is projected to reach USD 21.40 Billion by 2034, growing at a CAGR of 10.5% from 2026 to 2034. Market growth is driven by precision medicine, biomarker-based testing, targeted therapies, and molecular diagnostics.

Who are the major players in the Companion Diagnostic Market?

F. HOFFMANN-LA ROCHE, THERMO FISHER SCIENTIFIC, QIAGEN N.V., AGILENT TECHNOLOGIES, ILLUMINA, INC., GUARDANT HEALTH, FOUNDATION MEDICINE, MYRIAD GENETICS, ABBOTT LABORATORIES, BIOMERIEUX, ABNOVA CORPORATION, BIOGENEX LABORATORIES, DAKO (AGILENT), VENTANA MEDICAL SYSTEMS (ROCHE), LEICA BIOSYSTEMS (DANAHER), SYSMEX CORPORATION, BECTON, DICKINSON AND COMPANY, NEOGENOMICS LABORATORIES, NATERA, INC., PERSONALIS, INC., Others

Which segments covered the Companion Diagnostic Market?

By Technology, (Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Immunohistochemistry (IHC), In Situ Hybridization (ISH), Fluorescence In Situ Hybridization (FISH), Digital PCR, Gene Expression Profiling, DNA Sequencing, Microarray Technology, Others), By Indication, (Oncology, Cardiovascular Diseases, Neurological Disorders, Infectious Diseases, Autoimmune Diseases, Respiratory Diseases, Rare Genetic Disorders, Metabolic Disorders, Hematological Disorders, Others), By Product Type, (Assays, Kits, and Reagents, Instruments, Software and Bioinformatics Solutions, Companion Diagnostic Test Panels, Sequencing Consumables, Quality Control Materials, Sample Preparation Kits, Others), By End-User, (Hospitals, Diagnostic Laboratories, Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Contract Research Organizations (CROs), Reference Laboratories, Cancer Research Centers, Specialty Clinics, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date