- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Compliance Workflow Automation Market Size, Share | CAGR 12.9%

Global Compliance Workflow Automation Market Size, Share, Growth Analysis By Offering (Software/SaaS Platforms, Professional Services, Managed Compliance Services, Consulting & Advisory), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Regulatory Change Management, Audit Management, AML/KYC, ESG Compliance, Data Privacy Compliance, Vendor Risk Management), By End-User Vertical, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

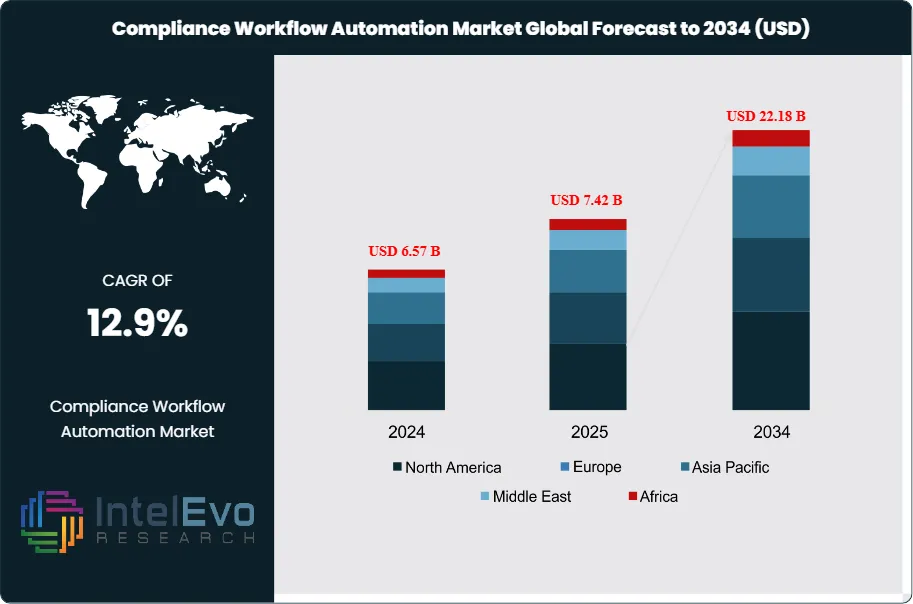

| USD 7.42 Billion | USD 22.18 Billion | 12.9% | North America, 41.6% |

The Compliance Workflow Automation Market was valued at approximately USD 6.57 Billion in 2024 and reached USD 7.42 Billion in 2025. The market is projected to grow to USD 22.18 Billion by 2034, expanding at a CAGR of 12.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 14.76 Billion over the analysis period, reflecting enterprise-wide urgency to replace manual, spreadsheet-dependent compliance processes with integrated software platforms capable of orchestrating regulatory obligations, audit workflows, policy management, and risk controls at scale.

Get More Information about this report -

Request Free Sample ReportCompliance workflow automation encompasses software and services that systematize the end-to-end lifecycle of regulatory compliance activities — from regulatory change monitoring and obligation mapping, through control design and testing, to audit evidence collection, deficiency remediation, and board-level reporting. The market sits at the intersection of governance, risk, and compliance (GRC) software and intelligent process automation, with leading platforms now embedding machine learning, natural language processing, and generative AI to reduce manual compliance task loads by 35–55% versus conventional rule-based workflow tools. The SEC's finalized climate-related disclosure rules, the EU's Digital Operational Resilience Act (DORA) effective January 2025, updated Basel III.1 capital reporting requirements, and expanding state-level US data privacy laws are each generating direct budget authorization for compliance workflow automation at financial institutions, public companies, and regulated infrastructure operators.

Demand is anchored in the banking, financial services, and insurance (BFSI) vertical, which accounted for 34.2% of global compliance workflow automation revenue in 2025 at USD 2.54 Billion. Anti-money laundering automation, KYC workflow orchestration, and SOX control management are the primary BFSI buying triggers. Healthcare and life sciences represents the second-largest vertical at 18.6%, driven by HIPAA audit workflow requirements, FDA 21 CFR Part 11 electronic records compliance, and expanding state-level Surprise Billing Act reporting. The EU AI Act — fully effective in August 2026 — is already generating AI governance and documentation workflow automation demand among technology companies and financial institutions subject to high-risk AI system obligations, adding an estimated USD 820 Million in incremental compliance automation expenditure through 2028.

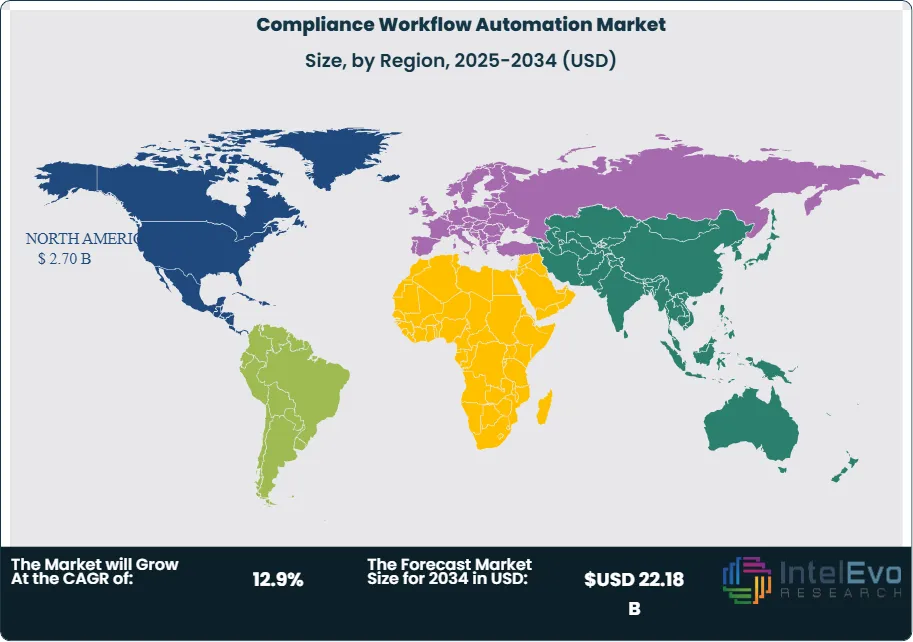

Cloud-based deployment is the dominant delivery model, representing 68.4% of 2025 market revenue at USD 5.07 Billion, driven by SaaS economics, continuous regulatory update feeds built into cloud GRC platforms, and the need for geographically distributed compliance teams to access unified workflow environments. North America leads global compliance workflow automation demand with a 41.6% share at USD 3.09 Billion in 2025, supported by the densest concentration of regulatory mandates per enterprise and the highest compliance technology investment ratios globally. Europe follows at 29.3%, with DORA, GDPR enforcement escalation, and EU Corporate Sustainability Reporting Directive (CSRD) mandates activating budget across financial services, manufacturing, and energy sectors. Asia Pacific is the fastest-growing region at 14.8% CAGR through 2034, with Monetary Authority of Singapore TRM guidelines, Japan's FISC security standards, and India's Digital Personal Data Protection Act driving platform adoption.

Artificial intelligence is the single most consequential technology shift in the compliance workflow automation market. Generative AI capabilities are being embedded into regulatory change management engines to automatically parse regulatory text, identify affected controls, and draft remediation workflows without human intervention — a function that previously consumed 12–18 analyst hours per regulatory update. ServiceNow's Policy Compliance Copilot, IBM OpenPages with Watson, and MetricStream's AI-native architecture each demonstrate the market's trajectory toward autonomous compliance orchestration. AI penetration in enterprise compliance workflow automation reached 41.3% of active deployments in 2025, and industry assessment projects this threshold exceeding 80% by 2030 as generative AI model performance in regulatory language interpretation achieves acceptable accuracy benchmarks certified under NIST AI Risk Management Framework guidelines.

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Regulatory Change Management, Audit Management, AML/KYC, ESG Compliance, Data Privacy Compliance, Vendor Risk Management), By End-User Vertical, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global compliance workflow automation market was valued at USD 7.42 Billion in 2025 and is projected to reach USD 22.18 Billion by 2034, advancing at a CAGR of 12.9% over the 2026–2034 forecast period.

- Segment Dominance: By offering, software and SaaS platforms command the leading position at 62.8% of global market revenue in 2025, driven by enterprise demand for always-current regulatory intelligence feeds, AI-automated control testing, and multi-jurisdiction workflow orchestration in a single environment.

- Segment Dominance: By end-user vertical, the BFSI sector holds the largest share at 34.2% of global compliance workflow automation revenue in 2025, anchored by AML, KYC, SOX, and Basel regulatory obligations that require continuous automated workflow management across large, geographically distributed compliance operations.

- Driver: Regulatory volume acceleration — with an estimated 1,100 new or amended regulatory requirements issued globally per business day in 2025 across financial services, healthcare, and ESG domains — is making manual compliance change management operationally untenable, compelling organizations to invest in automated regulatory tracking, obligation mapping, and control update workflows.

- Restraint: Integration complexity with legacy ERP, core banking, and document management systems adds an estimated 22–31% to total compliance platform implementation costs and extends deployment timelines by 4–9 months, disproportionately affecting mid-market enterprises and limiting near-term market conversion of identified demand.

- Opportunity: EU CSRD and SEC climate disclosure mandates are creating an addressable incremental compliance automation market of USD 2.8 Billion by 2034, as public companies globally require automated ESG data collection, materiality assessment, and structured narrative disclosure workflows aligned to ISSB and TCFD reporting standards.

- Trend: Generative AI-powered regulatory change management — enabling natural-language parsing of regulatory publications, automated control gap identification, and AI-drafted remediation workflow generation — reached 41.3% adoption among enterprise compliance automation deployments in 2025, up from 11.6% in 2022, and is redefining the ROI expectation for compliance platform investment.

- Regional Analysis: North America is the dominant region with a 41.6% share at USD 3.09 Billion in 2025, reflecting the highest regulatory mandate density per enterprise globally, mature GRC software procurement cycles, and the combined budget impact of SEC climate rules, state data privacy laws, and financial services regulatory intensification.

Competitive Landscape Overview

The compliance workflow automation market is moderately consolidated, with the top four vendors — ServiceNow, IBM, SAP, and MetricStream — collectively holding approximately 48.3% of global revenue in 2025. Platform breadth, AI integration depth, and pre-built regulatory content library size are the primary competitive dimensions, with enterprise customers prioritizing vendors offering the widest coverage of active regulatory frameworks across their operating jurisdictions. The market experienced a surge in M&A activity in 2024–2025 as platform vendors acquired AI regulatory analytics startups to accelerate generative AI capability development. New entrants specializing in vertical-specific compliance automation — particularly ESG disclosure, AI governance, and third-party risk management — are intensifying competition in rapidly growing sub-segments while avoiding direct confrontation with established GRC platform incumbents on breadth.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| ServiceNow | USA | Leader | ServiceNow GRC & IRM | North America / Europe | Launched AI-powered Policy & Compliance Copilot in Now Platform, Feb 2025 |

| IBM Corporation | USA | Leader | IBM OpenPages with Watson | North America / Europe | Acquired Accera AI compliance analytics firm for USD 340M, May 2025 |

| SAP SE | Germany | Challenger | SAP GRC Access Control | Europe / North America | Integrated Joule AI assistant into SAP GRC workflow engine, Aug 2025 |

| MetricStream | USA | Challenger | MetricStream GRC Platform | North America | Raised USD 175M Series F to expand AI-native compliance automation, Jan 2025 |

| Workiva | USA | Challenger | Workiva ESG & Compliance Cloud | North America / Europe | Launched SEC climate disclosure automation module, Apr 2025 |

| NICE Actimize | Israel/USA | Niche Player | NICE Actimize AML Compliance | North America / Europe | Deployed generative AI for SAR narrative automation across 60+ banks, Jul 2025 |

| Galvanize (Diligent) | Canada | Niche Player | HighBond Compliance Platform | North America | Merged with Diligent; unified board and compliance workflows, Oct 2025 |

| Riskonnect | USA | Niche Player | Riskonnect RMIS & Compliance | North America | Expanded compliance workflow modules for healthcare sector, Mar 2025 |

By Offering

The compliance workflow automation market by offering is led by software and SaaS platforms, which represent 62.8% of global revenue at USD 4.66 Billion in 2025. This segment encompasses purpose-built GRC platforms, RegTech SaaS applications, integrated risk management suites, and AI-native compliance orchestration tools that automate regulatory obligation tracking, policy lifecycle management, audit evidence collection, and board-level compliance reporting. Enterprise SaaS subscriptions average USD 180,000–2.4 Million annually depending on module scope and user count, with multi-year contracts of 3–5 years standard for large financial institutions and healthcare organizations. The software segment is growing at 14.1% CAGR through 2034, with AI-augmented platforms commanding 18–24% pricing premiums over conventional rule-based GRC software, reflecting the productivity gains delivered by automated regulatory change management and AI-generated audit narratives.

Professional services represent 19.6% of market revenue at USD 1.45 Billion in 2025, encompassing implementation services, custom workflow configuration, regulatory content library buildout, and user training. Average implementation engagements for enterprise GRC platform deployments range from USD 120,000 to USD 1.8 Million, with complexity driven by the number of regulatory frameworks in scope, integration points with source systems, and geographic footprint. Managed compliance services account for 11.4% at USD 846 Million, growing at 15.3% CAGR as mid-market organizations lacking internal compliance technology teams outsource platform management, regulatory monitoring, and reporting to specialist managed service providers. Consulting and advisory services represent the remaining 6.2% at USD 460 Million, primarily serving regulatory strategy and technology selection engagements.

By Deployment Mode

Cloud-based SaaS deployment leads the compliance workflow automation market at 68.4% of 2025 revenue, equivalent to USD 5.07 Billion. Cloud GRC platforms offer continuous regulatory update feeds maintained by vendor content teams, eliminating the 6–12 month regulatory library update lag characteristic of on-premise systems. Multi-tenant SaaS architectures reduce per-organization compliance technology total cost of ownership by 31–44% versus on-premise deployment over five-year contract periods, a decisive factor in enterprise technology selection. Major cloud compliance platform vendors including ServiceNow, Workiva, and MetricStream release regulatory content updates on weekly to monthly cycles, covering more than 350–500 active regulatory frameworks globally. Cloud adoption is accelerating in Europe, where DORA's digital resilience requirements and CSRD's annual reporting obligations favor always-current SaaS platforms over static on-premise solutions.

On-premise deployments retain a 19.8% share at USD 1.47 Billion in 2025, concentrated in government agencies, defense contractors, and systemically important financial institutions (SIFIs) subject to data sovereignty requirements, FedRAMP authorization mandates, or internal IT governance policies precluding third-party cloud data processing. This segment is contracting at 3.1% annually as cloud security clearance frameworks mature and FedRAMP-authorized versions of major GRC platforms reach availability. Hybrid deployments represent 11.8% at USD 876 Million, serving organizations maintaining on-premise core banking or EHR systems that require compliance workflow integration while migrating peripheral compliance functions to cloud environments.

By Application

Regulatory change management and policy and procedure management collectively represent the largest application cluster in the compliance workflow automation market, accounting for 29.4% of revenue at USD 2.18 Billion in 2025. Regulatory change management automates the monitoring of regulatory publications from agencies including the SEC, OCC, FCA, EMA, and ESMA; extracts obligation changes using NLP; maps changes to affected policies and controls; and initiates update workflows with accountability assignment and deadline tracking. The application is growing at 16.2% CAGR — the fastest among all application segments — driven by regulatory publication volume growth of 8.3% annually since 2020 and the commercial availability of LLMs fine-tuned on regulatory text corpora that deliver obligation extraction accuracy rates exceeding 91%.

Audit management and reporting accounts for 21.6% of market revenue at USD 1.60 Billion in 2025. Automation in this segment reduces audit cycle times by 28–42% through automated evidence request distribution, electronic audit trail capture, and AI-generated findings narratives. Risk assessment and controls testing represents 18.2% at USD 1.35 Billion, with automated controls testing frequency increasing from annual to continuous in leading deployments. AML and KYC compliance automation holds 14.8% at USD 1.10 Billion, driven by FinCEN's beneficial ownership rule enforcement and FATF Recommendation 16 payment transparency requirements. ESG and sustainability compliance automation accounts for 8.4% at USD 624 Million and is the fastest-emerging sub-segment. Data privacy compliance and third-party risk management represent the remaining 7.6% at USD 564 Million.

By Enterprise Size

Large enterprises with more than 1,000 employees dominate the compliance workflow automation market, representing 71.6% of global revenue at USD 5.31 Billion in 2025. This segment encompasses global financial institutions, multinational corporations, healthcare systems, and regulated utilities that operate across multiple jurisdictions with complex, overlapping regulatory obligations requiring enterprise-grade workflow orchestration. Average contract values for large enterprise compliance automation platforms range from USD 400,000 to USD 6.2 Million annually, with multi-module deployments spanning regulatory change management, audit, risk, and reporting functions. Large enterprises typically deploy compliance automation platforms integrated with SAP, Oracle, Workday, or Salesforce core systems, requiring vendor-provided integration connectors and implementation services.

Small and medium enterprises represent 28.4% of market revenue at USD 2.11 Billion in 2025 and are growing at a 15.8% CAGR — materially faster than the large enterprise segment at 11.6% — as purpose-built SME compliance SaaS platforms emerge at accessible price points of USD 12,000–95,000 annually. SME demand is particularly strong in financial services (community banks, credit unions, and regional broker-dealers subject to FINRA and state regulatory obligations), healthcare (physician groups and regional hospitals subject to HIPAA and state privacy laws), and technology companies subject to SOC 2, GDPR, and CCPA. Vendor platforms including Drata, Vanta, and Secureframe are capturing SME compliance automation demand through product-led growth models that reduce implementation timelines to 4–8 weeks.

By End-User Vertical

The BFSI vertical is the dominant end-user of compliance workflow automation, accounting for 34.2% of global revenue at USD 2.54 Billion in 2025. Banks, insurance carriers, asset managers, and payment processors face the highest regulatory obligation density globally, with US bank holding companies subject to an estimated 300+ active federal and state regulatory requirements. AML transaction monitoring workflow automation, BSA/AML suspicious activity report (SAR) narrative generation, SOX 302/404 controls documentation, and Basel III capital adequacy reporting are the primary BFSI automation buying centers. Global systemically important banks (G-SIBs) allocate an average of 4.1% of total operating expenditure to compliance functions, with technology tools representing 21–28% of that allocation in 2025.

Healthcare and life sciences represent 18.6% at USD 1.38 Billion in 2025, driven by HIPAA audit workflow automation, FDA 21 CFR Part 11 and Part 820 quality system compliance, CMS Conditions of Participation documentation, and No Surprises Act billing transparency requirements. Government and public sector accounts for 12.4% at USD 920 Million, with FISMA compliance workflow automation and state-level ethics and procurement compliance driving US federal and municipal adoption. Energy and utilities hold 10.8% at USD 801 Million, with NERC CIP critical infrastructure protection compliance and EPA emissions reporting the primary workflow automation use cases. Retail and e-commerce represents 9.6% at USD 712 Million, led by PCI DSS and state consumer data privacy compliance. IT and telecommunications account for 8.2% at USD 608 Million, with the EU AI Act and NIS2 Directive compliance driving platform adoption. Other verticals collectively represent the remaining 6.2%.

Regional Analysis

North America Compliance Workflow Automation Market

North America leads the global compliance workflow automation market with a 41.6% share at USD 3.09 Billion in 2025. The United States accounts for 87.3% of regional revenue at USD 2.70 Billion, driven by the world's most complex regulatory environment — spanning SEC, CFTC, OCC, FinCEN, CFPB, HIPAA, FDA, EPA, FTC, and 50+ state regulatory frameworks — combined with the highest enterprise compliance technology investment ratios globally. The SEC's finalized climate disclosure rules and the DOL's updated fiduciary rules are each generating net-new compliance automation budget authorizations across public companies and retirement plan administrators. A 2025 compliance technology survey indicates 63.4% of US Fortune 500 companies have active GRC platform modernization programs, up from 41.2% in 2022. Canada contributes 8.9% of North American revenue, with OSFI's B-20 mortgage guidelines and FINTRAC AML modernization driving financial services adoption. Mexico accounts for 3.8%, with compliance automation adoption accelerating among maquiladora operators and domestic financial institutions subject to CNBV digital banking requirements.

Europe Compliance Workflow Automation Market

Europe holds 29.3% of global compliance workflow automation revenue at USD 2.17 Billion in 2025. The region is experiencing the most concentrated regulatory activation of any global market, with DORA (effective January 2025), CSRD (phased reporting from 2025), EU AI Act (enforcement commencing August 2026), updated AMLD6 requirements, and NIS2 Directive (transposed across EU member states) collectively generating compliance program investment across financial services, technology, energy, and manufacturing sectors simultaneously. Germany is the largest European market at 24.6% of European revenue, reflecting the country's concentration of financial institutions under BaFin supervision, large automotive and manufacturing conglomerates with complex ESG reporting obligations, and SAP's installed base providing a compliance automation upgrade pathway. The UK contributes 21.3% of European revenue, maintaining substantial compliance automation demand despite Brexit regulatory divergence, driven by PRA and FCA supervisory intensification. France represents 16.8% and the Netherlands 12.4% of European SMP revenue, with both markets heavily driven by EU financial regulation compliance.

Asia Pacific Compliance Workflow Automation Market

Asia Pacific accounts for 18.4% of global compliance workflow automation revenue at USD 1.37 Billion in 2025 and is the fastest-growing region at 14.8% CAGR through 2034. Japan leads the region at 28.4% of APAC revenue at USD 389 Million, driven by Japan Financial Services Agency (JFSA) conduct of business rules, FISC security guidelines for financial institutions, and the country's expanding ESG disclosure requirements for Tokyo Stock Exchange prime market listed companies. China contributes 24.6% of APAC revenue at USD 337 Million, with PBOC AML regulations, CBIRC insurance compliance requirements, and PIPL data privacy obligations generating enterprise platform demand. India represents 18.2% at USD 249 Million, with RBI's digital banking compliance framework, SEBI's ESG reporting mandates for top-listed companies, and the Digital Personal Data Protection Act 2023 activating compliance automation investment. Singapore accounts for 12.6% at USD 173 Million, positioned as APAC's compliance technology hub under MAS TRM and AML framework requirements.

Latin America Compliance Workflow Automation Market

Latin America holds 6.4% of global compliance workflow automation revenue at USD 475 Million in 2025. Brazil is the dominant market at 48.2% of regional revenue at USD 229 Million, driven by BACEN resolution 4,557 risk management requirements, CVM securities regulation, LGPD data protection enforcement, and a maturing corporate governance framework that is compelling publicly listed companies to invest in GRC automation. Mexico contributes 27.6% of LATAM revenue at USD 131 Million, with CNBV anti-money laundering regulation and Banxico payment system compliance driving financial sector adoption. Colombia represents 10.4% of regional revenue at USD 49 Million, with expanding Superfinanciera de Colombia risk framework requirements driving mid-market bank adoption. The region faces adoption headwinds from fragmented regulatory frameworks that differ materially across national jurisdictions, limiting the applicability of pre-configured regulatory content libraries maintained by global GRC platform vendors.

Middle East & Africa Compliance Workflow Automation Market

The Middle East and Africa region accounts for 4.3% of global compliance workflow automation revenue at USD 319 Million in 2025. The UAE leads regional demand at 34.8% of MEA revenue at USD 111 Million, driven by CBUAE AML and sanctions compliance requirements, DIFC and ADGM financial services regulation, and the UAE's proactive digital economy strategy that positions technology adoption, including RegTech, as a national competitiveness priority. Saudi Arabia represents 28.4% of MEA revenue at USD 91 Million, with SAMA's regulatory framework for banks and insurance companies and Vision 2030's corporate governance enhancement agenda driving platform investment among Saudi public companies and financial institutions. South Africa accounts for 19.6% of MEA revenue at USD 63 Million, representing the primary compliance technology market on the African continent, anchored by FSCA financial sector supervision and the Protection of Personal Information Act (POPIA) enforcement. Regional growth is constrained by lower enterprise digitalization maturity outside Gulf Cooperation Council markets and limited availability of pre-built regulatory content covering GCC-specific regulatory frameworks.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software / SaaS Platforms

- Professional Services

- Managed Compliance Services

- Consulting & Advisory

By Deployment Mode

- Cloud-Based (SaaS)

- On-Premise

- Hybrid

By Application

- Regulatory Change Management

- Policy & Procedure Management

- Audit Management & Reporting

- Risk Assessment & Controls Testing

- Anti-Money Laundering (AML) / KYC

- ESG & Sustainability Compliance

- Data Privacy Compliance (GDPR, CCPA)

- Third-Party / Vendor Risk Management

By Enterprise Size

- Large Enterprises (>1,000 employees)

- Small & Medium Enterprises (SMEs)

By End-User Vertical

- Banking, Financial Services & Insurance (BFSI)

- Healthcare & Life Sciences

- Government & Public Sector

- Energy & Utilities

- Retail & E-Commerce

- IT & Telecommunications

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.42 B |

| Forecast Revenue (2034) | USD 22.18 B |

| CAGR (2025-2034) | 12.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Software / SaaS Platforms, Professional Services, Managed Compliance Services, Consulting & Advisory), By Deployment Mode (Cloud-Based (SaaS), On-Premise, Hybrid), By Application (Regulatory Change Management, Policy & Procedure Management, Audit Management & Reporting, Risk Assessment & Controls Testing, Anti-Money Laundering (AML) / KYC, ESG & Sustainability Compliance, Data Privacy Compliance (GDPR, CCPA), Third-Party / Vendor Risk Management), By Enterprise Size (Large Enterprises (>1,000 employees), Small & Medium Enterprises (SMEs)), By End-User Vertical (Banking, Financial Services & Insurance (BFSI), Healthcare & Life Sciences, Government & Public Sector, Energy & Utilities, Retail & E-Commerce, IT & Telecommunications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SERVICENOW, IBM CORPORATION, SAP SE, METRICSTREAM, WORKIVA, NICE ACTIMIZE, GALVANIZE (DILIGENT), RISKONNECT, NCONTRACTS, NAVEX GLOBAL, WOLTERS KLUWER FINANCE, RISK & REGULATORY REPORTING, ORACLE FINANCIAL SERVICES, ROPES & GRAY RISK (RISK & COMPLIANCE), DRATA, VANTA, SECUREFRAME, LOGICGATE, SAFEBASE, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Regulatory Change Management, Audit Management, AML/KYC, ESG Compliance, Data Privacy Compliance, Vendor Risk Management), By End-User Vertical, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Regulatory Change Management, Audit Management, AML/KYC, ESG Compliance, Data Privacy Compliance, Vendor Risk Management), By End-User Vertical, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Regulatory Change Management, Audit Management, AML/KYC, ESG Compliance, Data Privacy Compliance, Vendor Risk Management), By End-User Vertical, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Compliance Workflow Automation Market?

The Global Compliance Workflow Automation Market was valued at USD 6.57 Billion in 2024 and is projected to reach USD 22.18 Billion by 2034, growing at a CAGR of 12.9% from 2026 to 2034, driven by increasing regulatory complexities, rising adoption of AI-powered compliance management platforms, and growing demand for automated risk and governance workflows.

Who are the major players in the Compliance Workflow Automation Market?

SERVICENOW, IBM CORPORATION, SAP SE, METRICSTREAM, WORKIVA, NICE ACTIMIZE, GALVANIZE (DILIGENT), RISKONNECT, NCONTRACTS, NAVEX GLOBAL, WOLTERS KLUWER FINANCE, RISK & REGULATORY REPORTING, ORACLE FINANCIAL SERVICES, ROPES & GRAY RISK (RISK & COMPLIANCE), DRATA, VANTA, SECUREFRAME, LOGICGATE, SAFEBASE, OTHERS

Which segments covered the Compliance Workflow Automation Market?

By Offering (Software / SaaS Platforms, Professional Services, Managed Compliance Services, Consulting & Advisory), By Deployment Mode (Cloud-Based (SaaS), On-Premise, Hybrid), By Application (Regulatory Change Management, Policy & Procedure Management, Audit Management & Reporting, Risk Assessment & Controls Testing, Anti-Money Laundering (AML) / KYC, ESG & Sustainability Compliance, Data Privacy Compliance (GDPR, CCPA), Third-Party / Vendor Risk Management), By Enterprise Size (Large Enterprises (>1,000 employees), Small & Medium Enterprises (SMEs)), By End-User Vertical (Banking, Financial Services & Insurance (BFSI), Healthcare & Life Sciences, Government & Public Sector, Energy & Utilities, Retail & E-Commerce, IT & Telecommunications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Compliance Workflow Automation Market

Published Date : 14 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date