- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Confectionery Packaging Market Size, Share & Growth Analysis | 4.7% CAGR

Global Confectionery Packaging Market Size, Share & Industry Analysis By Material Type (Plastic, Paper & Paperboard, Aluminum Foil, Biodegradable Materials), By Packaging Type (Flexible Packaging, Rigid Packaging, Cartons, Pouches, Wrappers, Bags), By Application (Chocolate Confectionery, Sugar Confectionery, Gum & Jelly Products), By Distribution Channel (Retail Stores, Supermarkets & Hypermarkets, E-commerce) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Sustainability Trends & Forecast 2025–2034

Report Overview

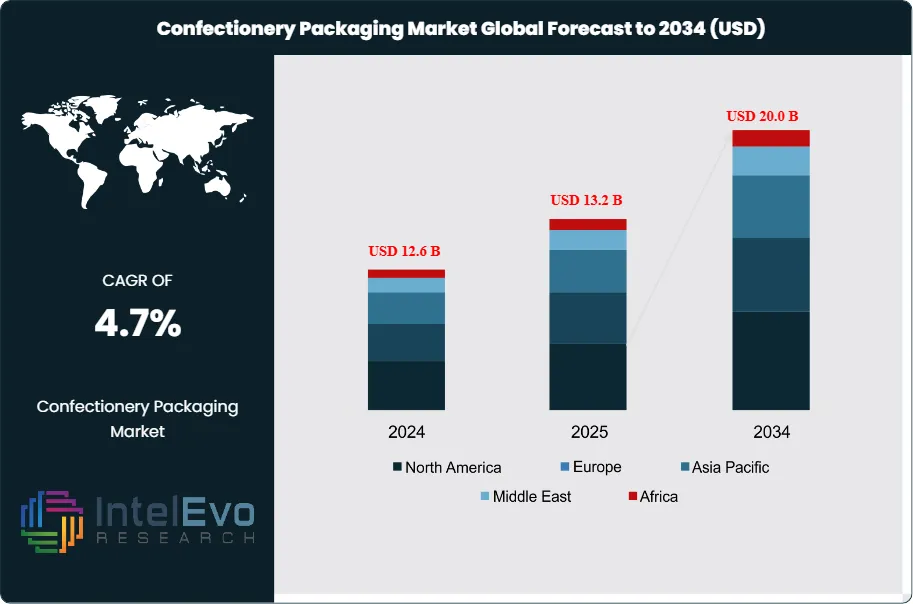

The Confectionery Packaging Market was valued at USD 12.6 Billion in 2024 and is estimated to reach approximately USD 13.2 Billion in 2025. Driven by rising demand for convenient and sustainable packaging solutions, increasing consumption of chocolates and sugar confectionery products, and growing adoption of innovative packaging formats by manufacturers, the market is projected to grow from about USD 13.8 Billion in 2026 to nearly USD 20.0 Billion by 2034, registering a compound annual growth rate (CAGR) of around 4.7% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportThis market supplies the primary and secondary packs used for chocolates, candies, gums, and related products across mass, premium, and artisanal tiers. Brand owners demand packaging that protects against moisture and oxygen ingress, preserves aroma, and maintains surface finish under temperature swings. Suppliers respond with a broad mix of flexible films, foils and laminates, cartons, and rigid formats such as tins, with conversion capability and print quality serving as differentiators in competitive bids.

Demand growth tracks confectionery volume, premiumization, and seasonal peaks. In the U.S., confectionery sales reached USD 48 billion in 2023, and projections target USD 61 billion by 2028, with seasonal occasions accounting for 64% of sales. Penetration remains broad, with over 98% of Americans purchasing chocolate, candy, gum, or mints in 2023. Consumer behavior continues to reward packaging upgrades. Survey findings indicate that over 60% of consumers rate features such as easy-open and resealability as essential, and about 60% are willing to pay up to a 14% premium for these benefits. Another study reports that 81% notice new packaging designs and 39% purchase products because of design changes, reinforcing packaging’s role as a revenue driver rather than a cost-only input.

Supply-side economics remain sensitive to resin, aluminum, paper, and energy pricing, as well as capacity utilization at film extrusion, metallization, and carton converting lines. Regulation increasingly shapes material choices. Food-contact compliance, labeling rules, and producer-responsibility regimes accelerate shifts toward recyclable mono-material structures, lightweighting, and lower-ink coverage. These shifts raise qualification costs and create execution risk when barrier performance and machinability degrade.

Technology investment is also reshaping competition. Digital printing expands short runs for limited editions and seasonal campaigns. Automation improves line efficiency and defect control. AI-driven artwork checking, demand sensing, and design-to-shelf optimization reduce changeover time and scrap. Smart packaging, including QR-enabled engagement and traceability, supports e-commerce protection and brand authentication.

Regionally, Asia-Pacific leads incremental volume, supported by rising snacking in India and Southeast Asia, while North America and Western Europe sustain value growth through premium gifting and sustainability-led redesigns. Investment hotspots include India, Indonesia, Vietnam, Mexico, and Central/Eastern Europe, where converters expand capacity near confectionery manufacturing clusters and export corridors. Capital activity also signals strategic intent; Mars, Incorporated’s USD 35.9 billion acquisition of Kellanova at USD 83.50 per share, reflecting a 44% premium to the prior 30-day average and a 33% premium to the 52-week high, underscores continued consolidation across snacking ecosystems that influence packaging demand and specifications.

, By Packaging Type (Flexible Packaging, Rigid Packaging, Cartons, Pouches, Wrappers, Bags), By Application (Chocolate Confectionery, Sugar Confectionery, Gum & Jelly Products), By Distribution Channel (Retail Stores, Supermarkets & Hypermarkets, E-commerce) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Sustainability Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market grows from 12.0 billion USD, 2024 to 19.0 billion USD, 2034 at a 4.7% CAGR, 2024-2034.

- Segment Dominance : Flexible packaging leads at 56.5%, 2024, supported by scale economics and weight reduction across high-volume SKUs.

- Segment Dominance: Plastic accounts for 53.4%, 2024, driven by low-cost conversion and strong barrier performance for freshness retention.

- Driver: Chocolate confectionery drives demand with 42.1%, 2024, as brands expand premium formats and gifting assortments.

- Restraint: Regulation and material scrutiny constrain plastics adoption, estimated: 2.0% cost uplift, 2024, from compliance, redesign, and qualification cycles.

- Opportunity: Sustainability-led redesign expands growth white space, estimated: 1.2 billion USD, 2030, in recyclable and compostable confectionery packs.

- Trend: Converters accelerate digitalization for short runs and customization, estimated: 28.0% of print volume, 2028, shifting to digital and automated workflows.

- Regional Analysis: North America leads with 37.2%, 2024, backed by high confectionery consumption and rising demand for sustainable packaging formats.

By Type

Flexible packaging remains the dominant format in the global confectionery packaging market as the industry moves into 2025. The segment accounted for approximately 56.5 percent of total packaging demand in 2024, supported by its low material intensity, lower logistics cost, and compatibility with high-speed confectionery production lines. Flexible films, wraps, and pouches provide strong moisture and oxygen barriers, which is critical for chocolates and sugar-based products with sensitivity to humidity and temperature variation.

Growth in this segment is reinforced by sustainability-driven material shifts. Brand owners are increasing the use of recyclable mono-material films and downgauged structures to meet regulatory and retailer requirements. Flexible packaging also supports digital printing and short production runs, which are increasingly used for seasonal launches and promotional assortments. These factors position flexible formats as the primary growth engine through 2030, with volume growth tracking closely to global confectionery output.

Rigid packaging holds a smaller but stable share, largely tied to premium and gift-oriented confectionery. Boxes, tins, and molded containers are preferred for high-value chocolates and seasonal collections where presentation, protection, and reusability influence purchasing decisions. Improvements in recyclability and lightweight rigid formats are expected to sustain measured growth, particularly in premium segments.

By Material Type

Plastic remains the leading material, accounting for roughly 53.4 percent of confectionery packaging usage in 2024. Its dominance reflects cost efficiency, strong barrier performance, and broad compatibility with flexible and rigid formats. Plastic enables extended shelf life, transparency for product visibility, and consistent sealing performance across high-volume production environments.

Paper and paperboard continue to gain share as sustainability expectations tighten. Although their overall penetration remains lower than plastics, demand is rising among premium and environmentally positioned brands. Folding cartons, paper wraps, and coated paper solutions are increasingly adopted for secondary packaging, particularly in Europe and North America, where regulatory pressure on plastics is strongest.

Glass and metal serve niche but strategic roles. Glass is primarily used for gourmet chocolates and gift assortments, where inert material properties and premium aesthetics justify higher costs. Metal, including tins and aluminum containers, supports seasonal, collectible, and reusable formats. Both materials benefit from high recycling rates, which supports their continued use in selective applications.

By Confectionery Type

Chocolate confectionery represents the largest demand base for packaging, accounting for approximately 42.1 percent of total market consumption in 2024. Strong global demand, premiumization trends, and gifting occasions drive consistent investment in protective and visually differentiated packaging formats. Barrier performance, temperature resistance, and surface finish remain central design priorities.

Sugar confectionery forms a substantial secondary segment. Candies and toffees require moisture-resistant, durable, and low-cost packaging solutions. Bright graphics and portion-based formats support volume growth, particularly in products targeted at children and impulse purchases. Gums rely on compact, portable packaging that preserves flavor and texture, with blister packs and resealable pouches remaining common.

Fruit and nut-based confectionery continues to expand from a smaller base, supported by health-oriented snacking trends. Packaging demand centers on resealability and freshness retention. Other confectionery types remain fragmented, with packaging demand closely aligned to specific shelf-life and branding requirements.

By Region

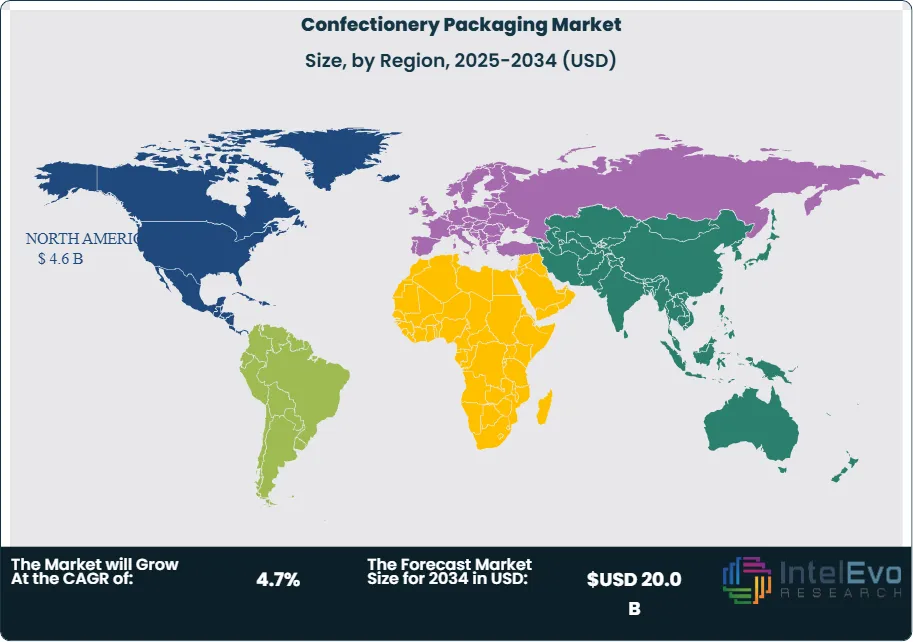

North America remains the largest regional market, holding approximately 37.2 percent share and generating an estimated USD 4.6 billion in confectionery packaging revenue in 2024. High per-capita confectionery consumption, advanced retail infrastructure, and strong adoption of sustainable packaging formats underpin regional leadership. Brand investment in premium and seasonal packaging continues to support value growth.

Europe follows closely, supported by a mature confectionery industry and strict environmental regulation. Demand for recyclable and paper-based solutions is particularly strong in Germany, France, and the United Kingdom. Premium chocolate consumption sustains demand for rigid and high-quality secondary packaging.

Asia Pacific represents the fastest-growing region through 2030. Rising disposable incomes, urbanization, and expanding retail channels in China, India, and Southeast Asia are driving confectionery volumes and packaging demand. Flexible, cost-efficient formats dominate new capacity additions. Latin America and the Middle East and Africa show steady growth, supported by expanding retail networks, youthful demographics, and increasing chocolate consumption.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Packaging Type

- Flexible Packaging

- Rigid Packaging

Material Type

- Plastic

- Paper and Paperboard

- Glass

- Metal

Confectionery Type

- Chocolate Confectionery

- Sugar Confectionery

- Gums

- Fruit and Nuts

- Other Confectionery Types

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 13.2 Billion |

| Forecast Revenue (2034) | USD 20.0 B |

| CAGR (2025-2034) | 4.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Flexible Packaging, Rigid Packaging), By Material Type (Plastic, Paper and Paperboard, Glass, Metal), By Confectionery Type (Chocolate, Sugar Confectionery, Gums, Fruit and Nuts, Other Types) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Constantia Flexibles, Amcor plc, Huhtamaki, PPC Flex Company Inc., Smurfit Kappa, Berry Global Inc., C-P Flexible Packaging, Mondi Group, WestRock Company, Sonoco Products Company, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Packaging Type (Flexible Packaging, Rigid Packaging, Cartons, Pouches, Wrappers, Bags), By Application (Chocolate Confectionery, Sugar Confectionery, Gum & Jelly Products), By Distribution Channel (Retail Stores, Supermarkets & Hypermarkets, E-commerce) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Sustainability Trends & Forecast 2025–2034")

, By Packaging Type (Flexible Packaging, Rigid Packaging, Cartons, Pouches, Wrappers, Bags), By Application (Chocolate Confectionery, Sugar Confectionery, Gum & Jelly Products), By Distribution Channel (Retail Stores, Supermarkets & Hypermarkets, E-commerce) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Sustainability Trends & Forecast 2025–2034")

, By Packaging Type (Flexible Packaging, Rigid Packaging, Cartons, Pouches, Wrappers, Bags), By Application (Chocolate Confectionery, Sugar Confectionery, Gum & Jelly Products), By Distribution Channel (Retail Stores, Supermarkets & Hypermarkets, E-commerce) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Sustainability Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Confectionery Packaging Market?

The Global Confectionery Packaging Market was valued at USD 12.6 Billion in 2024 and is projected to reach USD 20.0 Billion by 2034, growing at a CAGR of 4.7% from 2026–2034. Explore market trends, innovative packaging solutions, sustainability initiatives, key drivers, and competitive landscape shaping the confectionery packaging industry.

Who are the major players in the Confectionery Packaging Market?

Constantia Flexibles, Amcor plc, Huhtamaki, PPC Flex Company Inc., Smurfit Kappa, Berry Global Inc., C-P Flexible Packaging, Mondi Group, WestRock Company, Sonoco Products Company, Other Key Players

Which segments covered the Confectionery Packaging Market?

By Type (Flexible Packaging, Rigid Packaging), By Material Type (Plastic, Paper and Paperboard, Glass, Metal), By Confectionery Type (Chocolate, Sugar Confectionery, Gums, Fruit and Nuts, Other Types)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Confectionery Packaging Market

Published Date : 06 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date