- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Confidential Computing Market Size, Share & Forecast | CAGR 24.3%

Global Confidential Computing Market Size, Share, Analysis By Component (Hardware – TEE Processors, Secure Enclaves, HSMs; Software & Platforms; Managed and Professional Services), By Technology (Trusted Execution Environments, Multi-Party Computation, Zero-Knowledge Proofs, Fully Homomorphic Encryption), By Deployment Mode (Cloud, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Manufacturing) Industry Trends, Security Innovations & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 5.2 Billion | USD 36.8 Billion | 24.3% | North America, 44.2% |

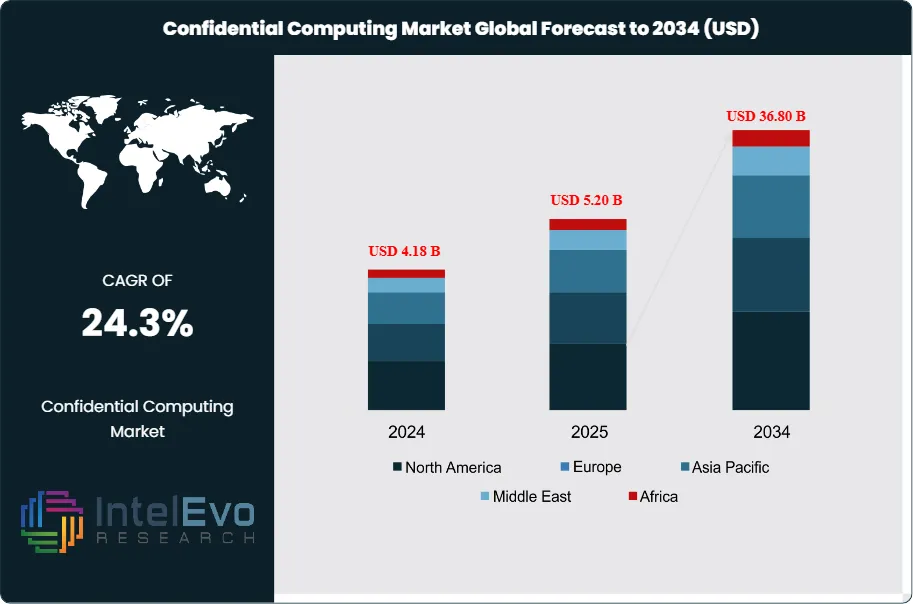

The Confidential Computing Market was valued at approximately USD 4.18 Billion in 2024 and reached USD 5.20 Billion in 2025. The market is projected to grow to USD 36.80 Billion by 2034, expanding at a CAGR of 24.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 31.6 Billion over the analysis period. The confidential computing market addresses a foundational gap in cloud security by protecting data-in-use inside hardware-isolated trusted execution environments, completing the data protection triad alongside encryption at rest and in transit. This capability has moved from a niche infrastructure feature to a board-level procurement priority as AI workloads, sovereign data mandates, and cross-organization analytics create structural demand for computer environments that no administrator, cloud operator, or hypervisor can access.

Get More Information about this report -

Request Free Sample ReportTrusted execution environment technology, led by Intel Trust Domain Extensions, AMD Secure Encrypted Virtualization with Secure Nested Paging, and Arm's Confidential Compute Architecture, underpins the majority of production deployments. The Confidential Computing Consortium, a Linux Foundation project, has accelerated interoperability through open attestation standards, and the release of open-source TEE frameworks including Enarx and Gramine has lowered onboarding friction for enterprises migrating regulated workloads. GPU-based confidential computing reached commercial scale in 2025 through NVIDIA's H100 and H200 attestation support, unlocking confidential AI inference for financial modeling, genomic analysis, and national security applications.

Regulatory pressure is acting as an unambiguous demand accelerator. The EU AI Act, GDPR data localization enforcement, the US Executive Order on AI safety, HIPAA de-identification alternatives under confidential multi-party analytics, and FIPS 140-3 compliance requirements for federal cloud are all pulling procurement forward. Financial services and government clients in particular are specifying TEE-backed compute as a contractual requirement for third-party data processing, creating a wave of retrofitting and new deployment that will sustain double-digit volume growth through the mid-2030s. North America holds 44.2% of 2025 market value at USD 2.30 Billion, anchored by hyper-scaler capacity and federal agency demand, while Asia Pacific is the fastest-growing region as Japan, South Korea, and Australia embed confidential compute requirements into critical infrastructure and digital government programs.

Technology investment is reshaping cost and ease of use. Container-native TEE runtimes, policy-as-code attestation, and confidential Kubernetes node pools are making confidential computing accessible without requiring application rewrites. Analyst procurement data indicates that enterprises deploying confidential computing for AI training and inference report a 35-48% reduction in compliance friction for cross-border data sharing. These productivity gains, combined with declining TEE instance premiums on major cloud platforms, are widening the total addressable market across SME and mid-market segments through 2027-2030.

, By Technology (Trusted Execution Environments, Multi-Party Computation, Zero-Knowledge Proofs, Fully Homomorphic Encryption), By Deployment Mode (Cloud, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Manufacturing) Industry Trends, Security Innovations & Forecast 2026-2034")

Key Takeaways

- Market Growth: The confidential computing market was valued at USD 5.2 Billion in 2025 and is projected to reach USD 36.8 Billion by 2034, at a CAGR of 24.3% across the 2026-2034 forecast period.

- Segment Dominance: Hardware solutions, primarily silicon TEE implementations from Intel, AMD, and Arm, held 52.8% of market value in 2025, reflecting the foundational role of processor-level trust roots.

- Segment Dominance: BFSI led vertical demand with 28.6% share in 2025, driven by cross-organization analytics, fraud model sharing, and regulatory obligations under DORA, PCI DSS 4.0, and Basel IV data governance rules.

- Driver: Rapid adoption of confidential AI inference, where enterprises process proprietary models and sensitive data inside attested GPU enclaves, contributed an estimated 22% of 2025 market value growth and is the fastest-expanding use case.

- Restraint: Application porting complexity remains the primary barrier. Lifting and shifting workloads into TEE environments requires software refactoring for memory and threading constraints, adding 4-12 weeks of engineering time and limiting adoption among organizations without dedicated cloud engineering headcount.

- Opportunity: Confidential multi-party computation for regulated data collaboration, specifically in genomics, financial crime analytics, and government intelligence sharing, represents an addressable incremental opportunity estimated at USD 4.8 Billion between 2025 and 2030.

- Trend: GPU-backed confidential computing reached commercial scale in 2025 with NVIDIA H100 TEE-IO attestation, enabling encrypted AI model weights and inference data to remain protected throughout the full GPU execution cycle.

- Regional Analysis: North America led the confidential computing market in 2025 with 44.2% share and USD 2.30 Billion in revenue, supported by hyperscaler native TEE offerings, CMMC 2.0 procurement requirements, and FedRAMP-authorized confidential instances.

Competitive Landscape Overview

The confidential computing market is moderately consolidated at the silicon and hyperscaler layers and fragmented among software abstraction, platform, and managed service providers. The four largest participants, covering silicon TEE IP and hyperscaler deployment infrastructure, accounted for an estimated 58.4% of commercial spend in 2025. Competition at the infrastructure layer is technology-driven, anchored by processor architecture and attestation root-of-trust capabilities. Platform vendors compete on developer experience, multi-TEE portability, and attestation policy management. Hyperscalers are embedding confidential compute natively into AI services and regulated industry offerings, raising the competitive baseline and narrowing the market window for standalone software abstraction vendors that do not differentiate on confidential AI or multi-party use cases.

Competitive Landscape Matrix

| Company | Headquarters | Market Position | Key Platform / Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Intel Corporation | United States | Leader | Intel TDX and SGX (Trust Domain Extensions) | North America, Europe, Asia Pacific | Expanded TDX attestation support via Intel Trust Authority for multi-cloud in 2025 |

| Microsoft | United States | Leader | Azure Confidential Computing (DCesv5, DCsv3 VMs) | North America, Europe, Asia Pacific | Integrated confidential computing into Azure OpenAI workloads for regulated clients in 2025 |

| AMD | United States | Leader | AMD SEV-SNP (Secure Encrypted Virtualization) | North America, Europe, Asia Pacific | Launched 5th Gen EPYC with enhanced SEV-SNP and memory integrity extensions in 2025 |

| Google Cloud | United States | Leader | Confidential GKE and Confidential VMs (N2D, C2D) | North America, Europe, Asia Pacific | Extended Confidential Space attestation to Vertex AI inference workloads in 2025 |

| IBM Corporation | United States | Challenger | IBM Secure Execution for Linux (LinuxONE, z16) | North America, Europe | Expanded IBM Hyper Protect Services for AI model confidentiality on z16 in 2025 |

| Amazon Web Services | United States | Challenger | AWS Nitro Enclaves and AWS Graviton Enclaves | North America, Europe, Asia Pacific | Added Nitro Enclave support to Amazon Bedrock for confidential AI inference in 2025 |

| Fortanix | United States | Challenger | Data Security Manager and Confidential AI Platform | North America, Europe | Raised Series C extension to expand confidential AI platform in early 2025 |

| NVIDIA Corporation | United States | Challenger | Confidential Computing on H100 and H200 Tensor Core GPUs | North America, Asia Pacific | Enabled full TEE-IO confidential GPU attestation with Intel TDX and AMD SEV in 2025 |

| Anjuna Security | United States | Niche Player | Anjuna Seaglass (multi-TEE runtime abstraction) | North America, Europe | Launched Anjuna Cloud Zero Trust to support regulated workloads across AWS, Azure, and GCP in 2025 |

| Arm Limited | United Kingdom | Niche Player | Arm CCA (Confidential Compute Architecture) and TrustZone | Europe, Asia Pacific | Released CCA firmware framework for NVIDIA Tegra and Qualcomm SoC platforms in 2025 |

By Component

Hardware captured 52.8% of the confidential computing market at approximately USD 2.75 Billion in 2025. This segment encompasses silicon TEE intellectual property, secure enclave processors, hardware security modules integrated with TEE attestation, and the Arm TrustZone and CCA architectures embedded in mobile and edge SoCs. Processor vendors license TEE capability through silicon and receive revenue through platform royalties and cloud instance fees. Intel's Xeon Scalable with TDX, AMD's EPYC 5th generation with SEV-SNP, and NVIDIA's H100 and H200 GPU confidential compute extensions are the primary hardware revenue contributors. Unit pricing premiums for TEE-capable instances on major cloud platforms remain in the 10-22% range over standard compute, though this differential is compressing as TEE support becomes baseline across new silicon generations.

Software and platforms held 31.4% at USD 1.63 Billion in 2025. This segment covers TEE runtime abstraction libraries such as Open Enclave SDK and Gramine, confidential AI platform tooling, policy-as-code attestation engines, and multi-TEE management consoles. Vendor differentiation rests on portability across Intel SGX, TDX, AMD SEV, and Arm CCA, with buyers increasingly requiring a single runtime that operates across multiple cloud and on-premise environments. Services contributed 15.8% at USD 0.82 Billion, covering managed attestation, confidential computing consultancy, deployment engineering, and compliance advisory for regulated industries adopting TEE-backed data processing at scale.

By Technology

Trusted Execution Environments dominated the confidential computing market with 58.6% share at approximately USD 3.05 Billion in 2025. TEEs use hardware memory encryption, access controls, and remote attestation to guarantee that code and data inside an enclave cannot be observed or tampered with by any privileged software stack including hypervisors and operating systems. Intel TDX and SGX, AMD SEV-SNP, and Arm CCA are the dominant implementations. Attestation through the Security Protocol and Data Model and through Intel Trust Authority and AMD Attestation Service provides cryptographic proof of TEE state to remote parties, enabling cross-organizational data collaboration without operational trust.

Multi-Party Computation held 18.4% share at USD 0.96 Billion, serving use cases where multiple organizations jointly compute outputs on combined datasets without exposing individual inputs. MPC protocols are gaining traction in financial crime analytics, federated credit scoring, and joint clinical trial analysis. Zero-Knowledge Proofs captured 12.8% at USD 0.67 Billion, primarily in blockchain verification, digital identity, and regulatory reporting where computation correctness must be publicly verifiable without revealing underlying data. Other approaches including fully homomorphic encryption and secure function evaluation contributed 10.2%, with FHE advancing from academic research toward performance-feasible production use cases for encrypted database queries and private machine learning inference.

By Deployment Mode

Cloud deployment accounted for 62.5% of confidential computing market value in 2025 at USD 3.25 Billion. Hyperscaler-native TEE offerings from Microsoft Azure, Google Cloud, AWS, and IBM Cloud have removed the infrastructure barrier and made confidential instances consumable on demand. Cloud deployment supports the attestation service integrations that regulated use cases require and provides the elastic scale necessary for batch genomics, fraud analytics, and AI inference workloads. On-premise deployment held 24.2% at USD 1.26 Billion, concentrated in defense, intelligence, central banking, and critical infrastructure environments that cannot route data through hyperscaler infrastructure regardless of security controls. Hybrid deployment captured 13.3% at USD 0.69 Billion, primarily among enterprises operating a mix of on-site SGX or SEV nodes for highly classified workloads and cloud TEE instances for volume analytics.

By Vertical

BFSI led vertical demand at 28.6% share in 2025, equivalent to USD 1.49 Billion. Cross-bank fraud analytics, confidential credit risk model sharing, derivatives pricing collaboration, and central bank digital currency prototype environments are the primary use cases. Government and defense held 18.2% at USD 0.95 Billion, driven by CMMC 2.0, FedRAMP-authorized TEE instances, and classified workload migration to confidential cloud. IT and telecommunications captured 17.8% at USD 0.93 Billion, covering platform infrastructure, confidential SaaS tenancy, and 5G network function protection. Healthcare followed at 16.4% or USD 0.85 Billion, anchored by federated clinical research, genomic data analysis under HIPAA, and confidential AI diagnostic model hosting. Manufacturing contributed 8.4% through IP protection in connected factory and digital twin workloads, with remaining verticals accounting for 10.6%.

Regional Analysis

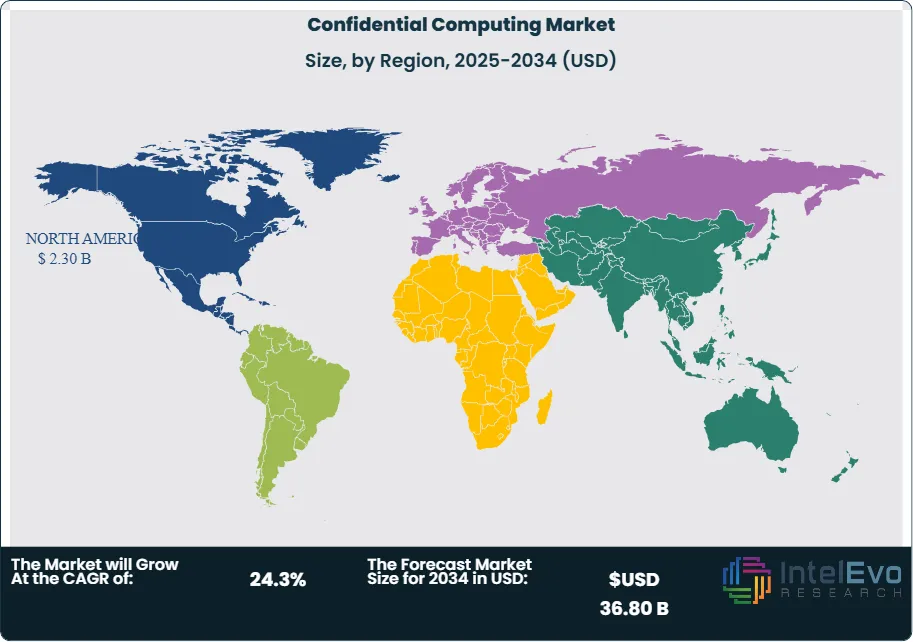

North America

North America led the confidential computing market in 2025 with 44.2% share and USD 2.30 Billion in revenue. The United States dominates, with hyperscaler investment concentrated in Northern Virginia, the Pacific Northwest, and Texas supporting the largest installed base of TEE-capable cloud infrastructure globally. Federal procurement is a structural demand driver. CMMC 2.0 Level 3 requirements, FedRAMP High authorization for confidential compute instances, and NSA guidance on cryptographic data protection are mandating TEE-backed execution for defense contractors and civilian agency workloads. The DoD Cloud Computing Security Requirements Guide and DISA IL5 and IL6 authorizations are creating a guaranteed procurement lane for confidential cloud through 2030. Canada contributes through an active federal cloud adoption program, the Canadian Centre for Cyber Security's cloud guidance, and financial services regulation under OSFI B-10 third-party risk guidelines that are beginning to reference data-in-use protection. Mexico participates primarily through multinational financial institutions operating shared services.

Europe

Europe captured 26.6% share at USD 1.38 Billion in 2025. Germany leads regional activity, with Bundesamt fur Sicherheit in der Informationstechnik Cloud Computing compliance catalogue requirements and strong industrial adoption of confidential computing for automotive IP protection and supply chain analytics. France follows, supported by ANSSI cloud security requirements and a growing sovereign cloud ecosystem including OVHcloud and Outscale that are building TEE-capable infrastructure. The United Kingdom ranks third, driven by NCSC cloud security guidance, active financial services adoption in London, and post-Brexit data sovereignty requirements. The Netherlands rounds out the top four as the primary European hyperscaler hub and testing ground for GDPR-aligned cross-border confidential compute architectures. The EU AI Act's requirements for transparency and data governance over AI systems are increasingly pointing enterprises toward TEE-backed AI inference as a compliance mechanism. GAIA-X workstreams are also specifying confidential compute as a baseline requirement for federated data spaces.

Asia Pacific

Asia Pacific held 21.2% share at USD 1.10 Billion in 2025 and is the fastest-growing regional market. Japan leads the region, with the Ministry of Economy, Trade and Industry promoting trusted data sharing frameworks under the Data Free Flow with Trust initiative and the Digital Agency standardizing TEE requirements for government cloud. China follows with domestic TEE adoption driven by Loongson, Hygon, and Phytium processor development programs alongside national cybersecurity standards under the Multi-Level Protection Scheme that address data-in-use isolation. South Korea is a third major market, with KISA guidance on cloud security and active adoption in financial services and semiconductor IP protection. Australia advances through ACSC Essential Eight controls, the Security of Critical Infrastructure Act, and federal cloud certification programs that increasingly specify data-in-use protection for sensitive workloads. The combined regulatory posture across the region is generating sustained demand across public sector, financial services, and technology verticals through 2034.

Latin America

Latin America accounted for 4.4% share at USD 0.23 Billion in 2025. Brazil leads the region, driven by LGPD enforcement, Banco Central do Brasil Resolution 4,893 on cloud services, and the active digitalization of federal health and tax administration systems under the RNDS and e-CAC programs. Mexico follows through CNBV requirements for financial sector cloud security and multinational enterprise deployments from the automotive and manufacturing sectors. Argentina contributes via BCRA financial cloud guidance and a growing Buenos Aires technology services cluster. Latin American adoption is currently concentrated among Tier 1 financial institutions and multinational subsidiary operations, with government adoption emerging through Brazilian federal programs. Channel development through regional system integrators and hyperscaler marketplace availability is accelerating SME access to confidential compute capabilities.

Middle East & Africa

The Middle East & Africa region held 3.6% share at USD 0.19 Billion in 2025. The UAE leads regional activity, with Abu Dhabi's ADGM data protection framework, Dubai's DIFC data privacy law, and the UAE Cybersecurity Council's cloud computing guidelines all referencing data-in-use protection for regulated workloads. Saudi Arabia follows through NCA Essential Cybersecurity Controls, Vision 2030 cloud infrastructure programs, and SAMA cloud framework requirements for banking sector data sovereignty. Israel contributes significantly through its defense technology base, with military and intelligence sector adoption of TEE infrastructure ahead of commercial markets. South Africa anchors sub-Saharan Africa through POPIA enforcement, SARB cybersecurity expectations, and JSE-listed financial institution compliance programs. Sovereign cloud infrastructure build-out programs in the UAE and Saudi Arabia are expected to drive the most substantial regional capacity expansion through 2028.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Hardware (TEE Processors, Secure Enclaves, HSMs)

- Software & Platforms (TEE Runtimes, Attestation Services, Confidential AI Tooling)

- Services (Managed Attestation, Consulting, Deployment Engineering)

By Technology

- Trusted Execution Environments (TEE)

- Multi-Party Computation (MPC)

- Zero-Knowledge Proofs (ZKP)

- Others (Fully Homomorphic Encryption, Secure Function Evaluation)

By Deployment Mode

- Cloud

- On-Premise

- Hybrid

By Vertical

- BFSI

- Government & Defense

- IT & Telecommunications

- Healthcare

- Manufacturing

- Others (Retail, Energy, Education)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.20 B |

| Forecast Revenue (2034) | USD 36.80 B |

| CAGR (2025-2034) | 24.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware (TEE Processors, Secure Enclaves, HSMs), Software & Platforms (TEE Runtimes, Attestation Services, Confidential AI Tooling), Services (Managed Attestation, Consulting, Deployment Engineering)), By Technology, (Trusted Execution Environments (TEE), Multi-Party Computation (MPC), Zero-Knowledge Proofs (ZKP), Others (Fully Homomorphic Encryption, Secure Function Evaluation)), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Vertical, (BFSI, Government & Defense, IT & Telecommunications, Healthcare, Manufacturing, Others (Retail, Energy, Education)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | INTEL CORPORATION, MICROSOFT CORPORATION, ADVANCED MICRO DEVICES (AMD), GOOGLE CLOUD (ALPHABET INC.), AMAZON WEB SERVICES (AWS), IBM CORPORATION, NVIDIA CORPORATION, ARM LIMITED, FORTANIX, INC., ANJUNA SECURITY, EDGELESS SYSTEMS GMBH, DECENTRIQ AG, OPAQUE SYSTEMS, CAPE PRIVACY, COSMIAN, PROFIAN (STEWARD CCS), RED HAT (IBM) - CONFIDENTIAL CONTAINERS, OVHCLOUD, ALIBABA CLOUD, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Trusted Execution Environments, Multi-Party Computation, Zero-Knowledge Proofs, Fully Homomorphic Encryption), By Deployment Mode (Cloud, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Manufacturing) Industry Trends, Security Innovations & Forecast 2026-2034")

, By Technology (Trusted Execution Environments, Multi-Party Computation, Zero-Knowledge Proofs, Fully Homomorphic Encryption), By Deployment Mode (Cloud, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Manufacturing) Industry Trends, Security Innovations & Forecast 2026-2034")

, By Technology (Trusted Execution Environments, Multi-Party Computation, Zero-Knowledge Proofs, Fully Homomorphic Encryption), By Deployment Mode (Cloud, On-Premise, Hybrid), By Vertical (BFSI, Government & Defense, Healthcare, IT & Telecommunications, Manufacturing) Industry Trends, Security Innovations & Forecast 2026-2034")

Frequently Asked Questions

How big is the Confidential Computing Market?

The Global Confidential Computing Market was valued at USD 4.18 Billion in 2024 and is projected to reach USD 36.80 Billion by 2034, growing at a CAGR of 24.3% from 2026 to 2034. Growth is driven by increasing demand for data privacy, secure cloud computing, trusted execution environments (TEEs), confidential AI workloads, zero-trust security frameworks, and regulatory compliance across BFSI, healthcare, government, and enterprise sectors worldwide.

Who are the major players in the Confidential Computing Market?

INTEL CORPORATION, MICROSOFT CORPORATION, ADVANCED MICRO DEVICES (AMD), GOOGLE CLOUD (ALPHABET INC.), AMAZON WEB SERVICES (AWS), IBM CORPORATION, NVIDIA CORPORATION, ARM LIMITED, FORTANIX, INC., ANJUNA SECURITY, EDGELESS SYSTEMS GMBH, DECENTRIQ AG, OPAQUE SYSTEMS, CAPE PRIVACY, COSMIAN, PROFIAN (STEWARD CCS), RED HAT (IBM) - CONFIDENTIAL CONTAINERS, OVHCLOUD, ALIBABA CLOUD, OTHERS

Which segments covered the Confidential Computing Market?

By Component, (Hardware (TEE Processors, Secure Enclaves, HSMs), Software & Platforms (TEE Runtimes, Attestation Services, Confidential AI Tooling), Services (Managed Attestation, Consulting, Deployment Engineering)), By Technology, (Trusted Execution Environments (TEE), Multi-Party Computation (MPC), Zero-Knowledge Proofs (ZKP), Others (Fully Homomorphic Encryption, Secure Function Evaluation)), By Deployment Mode, (Cloud, On-Premise, Hybrid), By Vertical, (BFSI, Government & Defense, IT & Telecommunications, Healthcare, Manufacturing, Others (Retail, Energy, Education))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Confidential Computing Market

Published Date : 29 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date