- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Connected Gym Equipment Market Size, Share | CAGR 21.1%

Global Connected Gym Equipment Market Size, Share, Analysis By Product Type (Smart Treadmills, Stationary Bicycles, Connected Rowing Machines, Smart Ellipticals, Connected Dumbbells & Kettlebells), By Connectivity (Wi-Fi, Bluetooth, Cellular), By End-User (Commercial Fitness Centers, Residential Smart Homes, Corporate Wellness, Hospitality & Luxury Hotels) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 3.03 Billion | USD 16.97 Billion | 21.1% | North America, 39.0% |

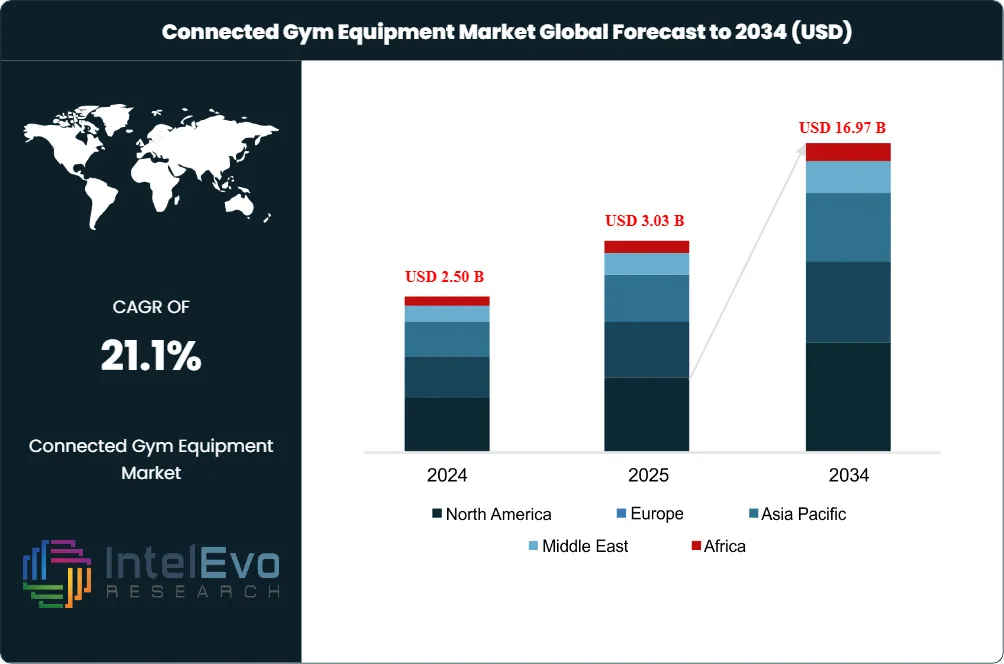

The Connected Gym Equipment Market was valued at USD 2.50 Billion in 2024 and USD 3.03 Billion in 2025. The market is projected to reach USD 16.97 Billion by 2034, expanding at a CAGR of 21.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.94 Billion over the analysis period. The connected gym equipment market includes cardio machines, strength systems, interactive bikes, treadmills, rowing machines, smart mirrors, app-linked benches, and commercial gym-floor devices that transmit workout data into mobile apps, club software, or cloud dashboards.

Get More Information about this report -

Request Free Sample ReportDemand in the connected gym equipment market is being pulled by two buyer groups with different economics. Commercial operators such as Life Time, Basic-Fit, Planet Fitness, EoS Fitness, Fitness First, and YMCA affiliates invest in connected cardio and strength systems because member retention now depends on personalization, progress tracking, and guided workouts. Home buyers remain selective after the pandemic demand spike, but Peloton Interactive, iFIT, Tonal, Hydrow, and Johnson Health Tech continue to capture recurring subscription revenue when hardware is tied to content and coaching.

The market is moving from screen-attached hardware toward data-rich fitness infrastructure because clubs want each treadmill, bike, rower, cable station, and strength machine to behave like a connected endpoint. The Health & Fitness Association reported that global fitness-industry revenue rose 8.0% in 2024, memberships increased 6.0%, and facilities expanded nearly 4.0%, creating a larger installed base for networked equipment. WHO data showing 31.0% of adults and 80.0% of adolescents below recommended physical-activity levels also supports policy interest in accessible fitness programs.

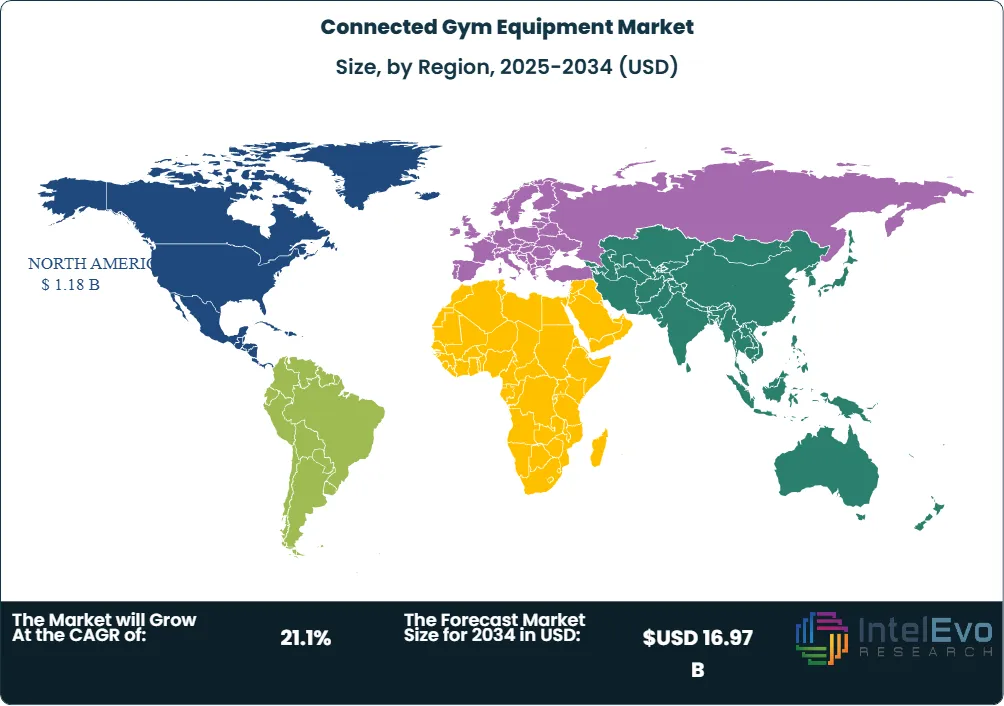

North America led the connected gym equipment market with 39.0% share in 2025, equal to USD 1.18 Billion, supported by U.S. health-club density, high household broadband penetration, and Peloton, Life Fitness, Precor, Tonal, and EGYM commercial activity. Europe followed at 27.5%, led by Germany, the United Kingdom, Italy, France, and the Nordics, where Technogym, EGYM, and Basic-Fit are shaping connected-club standards. Asia Pacific is forecast to post the fastest regional CAGR at 24.4% through 2034 because China, Japan, South Korea, India, and Australia are upgrading gyms, hotels, residential towers, and corporate wellness facilities.

The connected gym equipment market outlook through 2034 depends on four forces: AI-driven training plans, commercial refurbishment cycles, subscription attachment rates, and interoperability between equipment brands and club-management systems. Peloton's March 2026 Commercial Series, EGYM's January 2026 merger agreement with Playlist, and Technogym's 2025 revenue record show that vendors are rebuilding growth around commercial buyers rather than pure home-fitness hardware.

Market Definition & Scope

The connected gym equipment market is defined as commercial and consumer fitness equipment with embedded sensors, screens, wireless modules, software interfaces, and cloud connectivity that measure exercise performance and deliver digital coaching. The market encompasses connected treadmills, bikes, ellipticals, rowers, strength machines, smart benches, cable systems, interactive mirrors, recovery equipment, and integrated equipment software used by gyms, hotels, workplaces, medical fitness centers, and households.

This analysis includes hardware revenue, embedded software, equipment-linked subscriptions, installation services, service contracts, and digital features sold with connected machines. It excludes standalone fitness apps, smartwatches, unconnected dumbbells, basic mechanical treadmills, yoga platforms, and broad club-management software unless the software is bundled with equipment. The connected gym equipment market sits inside the larger fitness equipment and connected fitness markets, with approximately 15.7% share of the global fitness equipment category in 2025.

, By Connectivity (Wi-Fi, Bluetooth, Cellular), By End-User (Commercial Fitness Centers, Residential Smart Homes, Corporate Wellness, Hospitality & Luxury Hotels) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The connected gym equipment market expands from USD 3.03 Billion in 2025 to USD 16.97 Billion by 2034 at a 21.1% CAGR, creating USD 13.94 Billion in absolute dollar opportunity.

- Segment Dominance: Cardiovascular equipment led by connected treadmills, bikes, ellipticals, and rowers held 56.5% share in 2025, equal to USD 1.71 Billion.

- Segment Dominance: Commercial gyms and fitness clubs accounted for 49.0% of 2025 demand, or USD 1.48 Billion, because operators are refreshing cardio floors and strength circuits.

- Driver: Global health-club revenue grew 8.0% in 2024 and membership rose 6.0%, increasing the replacement pool for connected gym equipment.

- Restraint: Hardware prices ranging from USD 1,500 for connected home bikes to more than USD 12,000 for commercial cardio units slow adoption in price-sensitive clubs.

- Opportunity: AI-enabled strength training represents a USD 3.35 Billion revenue opportunity by 2034 as EGYM, Technogym, Tonal, and Life Fitness convert analog strength areas into data-capturing zones.

- Trend: Equipment vendors are adding cross-platform integrations, with EGYM connecting more than 200 partner products and Peloton pushing connected workouts into commercial locations in 2026.

- Regional: North America led with 39.0% share and USD 1.18 Billion in 2025, while Asia Pacific is forecast to grow fastest at 24.4% CAGR through 2034.

Key Insights Summary

- The connected gym equipment market benefits from commercial fitness recovery, with 2024 industry revenue up 8.0%, memberships up 6.0%, and facility count up nearly 4.0% in the 2025 Health & Fitness Association dataset.

- Peloton Interactive ended Q2 FY2026 with 2.661 Million paid connected fitness subscriptions, down 7.0% year over year, showing why the company is moving toward gym-floor distribution.

- Technogym reported 2025 revenue of EUR 901 Million, up 11.5% year over year, with commercial and consumer channels both growing by more than 11.0%.

- Playlist and EGYM disclosed more than USD 800 Million in 2025 combined net revenue and USD 785 Million in new equity funding as part of their January 2026 merger plan.

- Peloton and Precor previewed a connected bike and connected treadmill in March 2026, with global shipping planned for fall 2026 and broader availability targeted for early 2027.

- Fitness First plans to deploy EGYM Genius AI across 220 German clubs by summer 2026 after a pilot that began in 2025.

- WHO physical-activity data show that 1.8 Billion adults were insufficiently active in 2022, creating a public-health demand case for accessible digital fitness infrastructure.

Competitive Landscape Overview

The connected gym equipment market is moderately consolidated, with Technogym, Peloton Interactive, Life Fitness, Johnson Health Tech, EGYM, and iFIT controlling the most visible connected product families. The top four suppliers held an estimated 42.0% of 2025 revenue when commercial equipment, home hardware, and equipment-linked subscriptions are combined. Competition is based on hardware reliability, content depth, facility software integration, service response time, and recurring revenue attachment.

Competition is shifting toward commercial endpoints because the home-fitness boom left many households with underused bikes and treadmills. Peloton's commercial push through Precor, EGYM's Playlist transaction, and Technogym's club-focused digital ecosystem show that vendors are chasing operators with recurring member traffic rather than one-time household buyers. Smaller brands such as Tonal, Hydrow, CLMBR, Ergatta, and FightCamp compete on high-engagement niches, but financing costs and subscriber acquisition expenses make scale harder.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Technogym S.p.A. | Italy | Leader | Biostrength, Artis, Excite, Technogym Ecosystem | Europe, North America, APAC | Reported EUR 901 Million 2025 revenue and expanded connected wellness systems across commercial and consumer channels |

| Peloton Interactive, Inc. | United States | Leader | Bike, Tread, Row, Precor Commercial Series | North America, Europe | Previewed Commercial Series bike and treadmill in March 2026 for high-use gym locations |

| Life Fitness, LLC | United States | Leader | Life Fitness Connect, Symbio, Hammer Strength | North America, Europe, Middle East | Showcased connected cardio, software, and partner integrations at HFA 2026 |

| EGYM GmbH | Germany | Leader | EGYM Smart Strength, Fitness Hub, Genius AI | Europe, North America | Entered Playlist merger plan in January 2026 with USD 785 Million in new equity funding |

| Johnson Health Tech Co., Ltd. | Taiwan | Challenger | Matrix, Vision, Horizon, BowFlex JRNY | Asia Pacific, North America | Integrated BowFlex, Schwinn Fitness, and JRNY brands after the 2024 asset purchase |

| iFIT Inc. | United States | Challenger | NordicTrack and ProForm iFIT equipment | North America, Europe | Continued connected treadmill, bike, rower, and strength equipment distribution through retail channels |

| Tonal Systems, Inc. | United States | Niche Player | Tonal connected strength system | United States | Maintained premium connected strength focus after prior capital restructuring |

| Hydrow, Inc. | United States | Niche Player | Hydrow connected rowing machines | United States, UK | Focused on immersive rowing content and lower-footprint connected home equipment |

| Core Health & Fitness, LLC | United States | Challenger | Star Trac, StairMaster, Schwinn commercial equipment | North America, Europe | Expanded connected console and commercial cardio options for club operators |

| True Fitness Technology, Inc. | United States | Niche Player | TRUE cardio and connected consoles | North America | Competed in premium commercial cardio refresh cycles with connected display options |

Segmentation Analysis

The connected gym equipment market is segmented by equipment type, end-user, connectivity model, and price tier, with each segment shaped by replacement cycles, subscription attachment, and facility workflow needs.

By Equipment Type

The connected gym equipment market by equipment type is led by cardiovascular equipment, which held 56.5% share in 2025, or USD 1.71 Billion. Connected treadmills, bikes, ellipticals, stair climbers, and rowers generate high usage hours in clubs, hotels, and apartments because they support guided workouts and simple performance metrics. Peloton, Precor, Life Fitness, Technogym, Matrix Fitness, Concept2, Hydrow, and iFIT compete in this segment with screens, heart-rate integration, Bluetooth, Wi-Fi, and cloud dashboards. Commercial buyers favor cardio because it is visible on the gym floor and easier to monetize through member engagement analytics.

Connected strength equipment accounted for 27.0% share in 2025, equal to USD 0.82 Billion, and is the fastest-growing equipment type through 2034. EGYM Smart Strength, Technogym Biostrength, Tonal, Vitruvian, Speediance, and Life Fitness connected strength systems convert load, range of motion, tempo, and repetition data into training plans. Strength systems grow faster than cardio because clubs want measurable coaching without adding one trainer per member. Compared with cardio, connected strength has lower installed base today but higher software value because each movement profile builds a longitudinal training record.

Interactive mirrors, smart benches, rowers, boxing systems, and specialty equipment represented 16.5% share in 2025, equal to USD 0.50 Billion. Hydrow, Ergatta, FightCamp, CLMBR, Lululemon Studio legacy Mirror users, and Forme target households and boutique studios that value content immersion. This category remains fragmented because product lifecycles are shorter and replacement demand is less predictable than commercial cardio. The procurement checklist for specialty connected gym equipment should prioritize warranty terms, content continuity, service coverage, and open data export.

By End-User

The connected gym equipment market by end-user is led by commercial gyms and fitness clubs with 49.0% share in 2025, or USD 1.48 Billion. Chains such as Planet Fitness, Life Time, EoS Fitness, Basic-Fit, Fitness First, and YMCA networks buy connected equipment to reduce coaching friction and gather usage data. The EoS Fitness launch of EGYM Genius AI in 2025 and the Fitness First rollout plan for 220 German clubs in 2026 signal how AI software can lift the value of existing machines. Commercial gyms spend more per site than homes because uptime, service-level agreements, and analytics matter.

Home fitness users accounted for 31.5% share in 2025, or USD 0.95 Billion, led by Peloton Bike, Peloton Tread, iFIT-enabled NordicTrack products, Tonal, Hydrow, and BowFlex JRNY-connected devices. Home buyers favor compact systems, monthly subscriptions, financing plans, and brand-led classes. Demand is weaker than the 2020-2021 surge because many consumers returned to clubs, but premium households still buy equipment when AI coaching replaces in-person instruction. Home segment growth depends on churn control and content renewal, not only hardware shipment volume.

Hospitality, corporate wellness, medical fitness, multifamily housing, universities, and public-sector facilities captured 19.5% share in 2025, or USD 0.59 Billion. Hotels and residential towers buy connected cardio because app-linked workouts improve amenity value without permanent staffing. Medical fitness centers and senior-wellness operators prefer connected strength equipment because range, force, and adherence data support safer progressive training. This segment grows as employers and property developers use wellness amenities to reduce churn, support return-to-office programs, and differentiate premium real estate.

By Connectivity Model

The connected gym equipment market by connectivity model is led by integrated hardware and cloud platforms, which held 61.0% share in 2025. Technogym Ecosystem, EGYM Ecosystem, Peloton Commercial Series, Life Fitness Connect, Precor digital consoles, and iFIT link equipment, user profiles, workouts, and operator dashboards into a single purchase decision. Integrated models win in commercial settings because service teams can support hardware, software, and account access under one vendor relationship. They also help facilities calculate connected gym equipment ROI by measuring utilization, repeat visits, and class participation.

App-linked equipment without full club software accounted for 25.0% share in 2025. BowFlex JRNY, NordicTrack iFIT, Hydrow, Tonal, and several Bluetooth-enabled cardio brands allow users to track workouts and stream coaching without deep operator systems. This model fits home and small-studio buyers because it limits implementation time and monthly cost. Open integration modules represented 14.0% share, led by EGYM partnerships, Apple GymKit-compatible equipment, Garmin, Strava, Polar, and heart-rate systems. Open models gain share as operators demand freedom to connect multiple brands on one floor.

By Price Tier

The connected gym equipment market by price tier is led by premium commercial systems, which held 46.0% share in 2025. These products cost from roughly USD 6,000 to more than USD 12,000 per unit and include Technogym, Life Fitness, Precor, Matrix Fitness, EGYM, and high-end connected strength equipment. Premium systems are preferred by clubs with high traffic because they offer stronger frames, replaceable consoles, better uptime, and multi-year support. Mid-tier connected equipment held 34.0% share, serving hotels, apartment gyms, schools, and independent clubs that need connected features without flagship pricing.

Consumer and entry-level connected equipment represented 20.0% share in 2025. Products in this tier range from approximately USD 500 app-linked bikes to USD 3,500 smart strength machines, with subscriptions adding USD 10 to USD 59 per month. Price sensitivity is high because buyers compare connected gym equipment against outdoor running, free mobile apps, and low-cost gym memberships. Vendors in this tier need financing, refurbished units, trade-in programs, and lower subscription friction to convert undecided buyers.

Regional Analysis

North America led the connected gym equipment market with 39.0% share and USD 1.18 Billion in 2025. The United States accounted for the largest portion because Peloton, Precor, Life Fitness, Tonal, iFIT, BowFlex, EGYM North America, and major club chains operate across dense metropolitan markets. Commercial demand is supported by gym refurbishments, multifamily amenities, hotel fitness upgrades, and corporate wellness programs. Peloton's March 2026 Commercial Series preview and Life Fitness digital partnerships indicate that North American vendors are prioritizing high-use facilities after the home-hardware correction.

Europe held 27.5% share of the connected gym equipment market in 2025, equal to USD 0.83 Billion. Germany, the United Kingdom, Italy, France, Spain, and the Nordics form the core demand cluster. Technogym's Italian manufacturing and digital ecosystem, EGYM's German installed base, and Basic-Fit's multi-country club footprint make Europe a software-led commercial market. Fitness First's plan to introduce EGYM Genius AI across 220 German clubs by summer 2026 shows how operators use connected equipment to standardize coaching at scale.

Asia Pacific accounted for 23.0% share in 2025, or USD 0.70 Billion, and is forecast to record the fastest CAGR at 24.4% through 2034. China, Japan, South Korea, India, Australia, and Singapore are upgrading gyms, hotels, residential complexes, and medical wellness facilities. Johnson Health Tech, Matrix Fitness, Technogym, Life Fitness, iFIT, and local Chinese manufacturers compete on price and connected-console functionality. Growth is driven by urban apartment living, rising gym penetration, and stronger acceptance of app-guided training in younger consumer cohorts.

Latin America represented 6.5% share of the connected gym equipment market in 2025, equal to USD 0.20 Billion. Brazil, Mexico, Chile, Colombia, and Argentina lead demand through club-chain expansion, hotel refurbishment, and private wellness centers. Operators remain price-sensitive, so mid-tier treadmills, bikes, and app-linked strength systems sell faster than premium AI strength circuits. Distributor financing and after-sales service coverage are decisive because import duties and currency volatility increase total ownership cost.

Middle East & Africa held 4.0% share in 2025, or USD 0.12 Billion. The United Arab Emirates, Saudi Arabia, Qatar, South Africa, and Israel represent the highest-value national markets. Demand is concentrated in premium hotels, residential towers, private clubs, and public wellness programs aligned with tourism and preventive-health agendas. Gulf buyers often prefer Technogym, Life Fitness, Matrix Fitness, Precor, and EGYM because luxury positioning and service reliability matter more than entry pricing.

Country Analysis

The United States connected gym equipment market reached USD 1.06 Billion in 2025 and is forecast to grow at a 20.2% CAGR through 2034. Demand is driven by large club chains, apartment gyms, hospitality fitness rooms, university recreation centers, and at-home subscribers. Peloton reported 2.661 Million paid connected fitness subscriptions in Q2 FY2026, while its Precor unit is developing connected commercial bikes and treadmills for gym floors. U.S. buyers are also influenced by employer wellness spending and chronic-disease prevention programs tied to physical activity.

Germany's connected gym equipment market reached approximately USD 0.25 Billion in 2025 and is projected to grow at a 22.5% CAGR through 2034. EGYM is the country's most visible connected strength and AI software player, while Fitness First plans a 220-club Genius AI rollout by summer 2026. Germany also benefits from dense urban club networks, employer wellness adoption, and a strong rehabilitation culture. Compared with the United States, German buyers put more weight on data protection, operator workflow, and equipment interoperability.

China's connected gym equipment market reached approximately USD 0.29 Billion in 2025 and is forecast to grow at a 26.0% CAGR through 2034. Urban households, boutique studios, hotels, and residential developments are adopting connected bikes, treadmills, and strength products. Johnson Health Tech and Matrix Fitness use Asian manufacturing scale, while domestic brands compete with lower-cost app-linked equipment. China grows faster than Europe because gym penetration remains lower, smart-device adoption is high, and connected consoles fit mobile-first consumer behavior.

Japan's connected gym equipment market reached approximately USD 0.14 Billion in 2025 and is forecast to grow at a 19.8% CAGR through 2034. Demand is shaped by aging demographics, compact living spaces, rehabilitation needs, and premium hotel fitness investment. Technogym, Life Fitness, Johnson Health Tech, Matrix Fitness, and domestic wellness operators target compact connected cardio and safer strength systems. Japan's market differs from India and China because buyers prioritize reliability, low noise, smaller footprints, and service continuity.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Equipment Type

- Connected Treadmills

- Connected Exercise Bikes

- Connected Rowing Machines

- Connected Elliptical Trainers

- Connected Strength Training Equipment

- Connected Functional Training Equipment

- Connected Smart Mirrors

- Connected Multi-Gym Systems

- Others

By End-User

- Residential Users

- Commercial Fitness Centers

- Health Clubs and Gym Chains

- Hotels and Hospitality

- Corporate Wellness Centers

- Rehabilitation and Physiotherapy Centers

- Educational Institutions

- Others

By Connectivity Model

- Wi-Fi Enabled Equipment

- Bluetooth-Enabled Equipment

- Cloud-Connected Fitness Equipment

- Artificial Intelligence (AI)-Powered Equipment

- Internet of Things (IoT)-Connected Equipment

- Subscription-Based Connected Platforms

- App-Integrated Fitness Equipment

- Others

By Price Tier

- Premium

- Mid-Range

- Economy

- Commercial-Grade

- Luxury Smart Fitness Equipment

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.03 B |

| Forecast Revenue (2034) | USD 16.97 B |

| CAGR (2025-2034) | 21.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment Type, (Connected Treadmills, Connected Exercise Bikes, Connected Rowing Machines, Connected Elliptical Trainers, Connected Strength Training Equipment, Connected Functional Training Equipment, Connected Smart Mirrors, Connected Multi-Gym Systems, Others), By End-User, (Residential Users, Commercial Fitness Centers, Health Clubs and Gym Chains, Hotels and Hospitality, Corporate Wellness Centers, Rehabilitation and Physiotherapy Centers, Educational Institutions, Others), By Connectivity Model, (Wi-Fi Enabled Equipment, Bluetooth-Enabled Equipment, Cloud-Connected Fitness Equipment, Artificial Intelligence (AI)-Powered Equipment, Internet of Things (IoT)-Connected Equipment, Subscription-Based Connected Platforms, App-Integrated Fitness Equipment, Others), By Price Tier, (Premium, Mid-Range, Economy, Commercial-Grade, Luxury Smart Fitness Equipment, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | TECHNOGYM S.P.A., PELOTON INTERACTIVE, INC., LIFE FITNESS, LLC, EGYM GMBH, JOHNSON HEALTH TECH CO., LTD., IFIT INC., PRECOR INCORPORATED, MATRIX FITNESS, TONAL SYSTEMS, INC., HYDROW, INC., BOWFLEX, INC., CORE HEALTH & FITNESS, LLC, TRUE FITNESS TECHNOLOGY, INC., CONCEPT2, INC., CLMBR, ERGATTA, INC., FIGHTCAMP, VITRUVIAN, SPEEDIANCE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Connectivity (Wi-Fi, Bluetooth, Cellular), By End-User (Commercial Fitness Centers, Residential Smart Homes, Corporate Wellness, Hospitality & Luxury Hotels) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Trends & Forecast 2026-2034")

, By Connectivity (Wi-Fi, Bluetooth, Cellular), By End-User (Commercial Fitness Centers, Residential Smart Homes, Corporate Wellness, Hospitality & Luxury Hotels) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Trends & Forecast 2026-2034")

, By Connectivity (Wi-Fi, Bluetooth, Cellular), By End-User (Commercial Fitness Centers, Residential Smart Homes, Corporate Wellness, Hospitality & Luxury Hotels) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Connected Gym Equipment Market?

The Global Connected Gym Equipment Market was valued at USD 2.50 Billion in 2024 and USD 3.03 Billion in 2025, and is projected to reach USD 16.97 Billion by 2034, growing at a CAGR of 21.1% from 2026 to 2034. Market growth is driven by AI-powered fitness, IoT-enabled equipment, and connected digital wellness solutions.

Who are the major players in the Connected Gym Equipment Market?

TECHNOGYM S.P.A., PELOTON INTERACTIVE, INC., LIFE FITNESS, LLC, EGYM GMBH, JOHNSON HEALTH TECH CO., LTD., IFIT INC., PRECOR INCORPORATED, MATRIX FITNESS, TONAL SYSTEMS, INC., HYDROW, INC., BOWFLEX, INC., CORE HEALTH & FITNESS, LLC, TRUE FITNESS TECHNOLOGY, INC., CONCEPT2, INC., CLMBR, ERGATTA, INC., FIGHTCAMP, VITRUVIAN, SPEEDIANCE, Others

Which segments covered the Connected Gym Equipment Market?

By Equipment Type, (Connected Treadmills, Connected Exercise Bikes, Connected Rowing Machines, Connected Elliptical Trainers, Connected Strength Training Equipment, Connected Functional Training Equipment, Connected Smart Mirrors, Connected Multi-Gym Systems, Others), By End-User, (Residential Users, Commercial Fitness Centers, Health Clubs and Gym Chains, Hotels and Hospitality, Corporate Wellness Centers, Rehabilitation and Physiotherapy Centers, Educational Institutions, Others), By Connectivity Model, (Wi-Fi Enabled Equipment, Bluetooth-Enabled Equipment, Cloud-Connected Fitness Equipment, Artificial Intelligence (AI)-Powered Equipment, Internet of Things (IoT)-Connected Equipment, Subscription-Based Connected Platforms, App-Integrated Fitness Equipment, Others), By Price Tier, (Premium, Mid-Range, Economy, Commercial-Grade, Luxury Smart Fitness Equipment, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Connected Gym Equipment Market

Published Date : 03 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date