- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Continuous Pharma Manufacturing Market Size & Forecast | CAGR 11.6%

Global Continuous Pharmaceutical Manufacturing Market Size, Share, Growth & Industry Analysis By Technology (Continuous OSD Manufacturing, Continuous Bioprocessing, Continuous API Flow Chemistry, Continuous Lyophilization & Fill-Finish), By End-User (Pharma Companies, CDMOs, Research Institutes), By Offering (Equipment, Software, Services) Industry Trends, Market Dynamics & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 3.42 Billion | USD 9.18 Billion | 11.6% | North America, 43.6% |

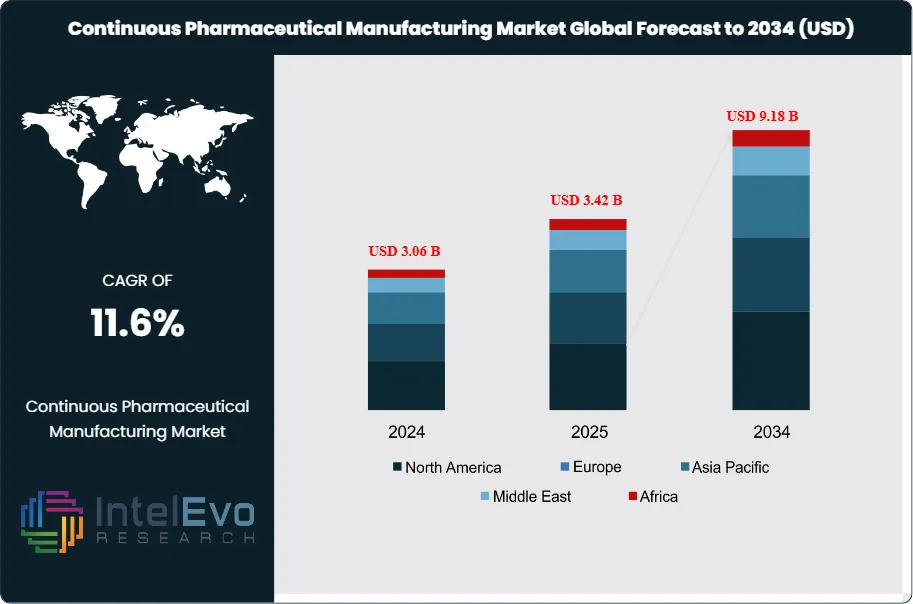

The Continuous Pharmaceutical Manufacturing Market was valued at approximately USD 3.06 Billion in 2024 and reached USD 3.42 Billion in 2025. The market is projected to grow to USD 9.18 Billion by 2034, expanding at a CAGR of 11.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.76 Billion over the analysis period, reflecting the pharmaceutical industry's accelerating transition away from batch-based production toward integrated, real-time-release manufacturing platforms.

Get More Information about this report -

Request Free Sample ReportContinuous pharmaceutical manufacturing (CPM) refers to production processes in which raw materials are fed into and finished products are extracted from the production system without interruption. Unlike traditional batch manufacturing — which involves discrete, sequential production steps with intermediate hold and test cycles — CPM integrates unit operations such as granulation, blending, compression, coating, and API synthesis into an unbroken material flow. This integration reduces cycle times by 60–80%, cuts in-process inventory, and enables real-time process monitoring aligned with FDA's Process Analytical Technology (PAT) framework.

Demand-side drivers are firmly in place. Patent expirations on high-volume small-molecule drugs are compelling manufacturers to adopt CPM as a tool for cost reduction, as continuous processes reduce facility footprint by up to 40% compared to batch equivalents. Simultaneously, the FDA's 2019 guidance on emerging technology and its Quality by Design (QbD) framework have de-risked regulatory submissions for CPM-based processes, increasing new product applications incorporating continuous technology. The EMA has similarly issued positive opinions on continuous manufacturing processes in line with ICH Q13 guidelines, which took effect across major regulatory jurisdictions in 2024.

On the supply side, equipment manufacturers have extended their continuous manufacturing portfolios beyond small-molecule oral solid dosage forms into continuous bioprocessing, continuous API synthesis via flow chemistry, and sterile fill-finish integration. This portfolio expansion is widening the addressable application base for CPM technology and supporting market growth across a broader range of product classes.

North America holds the largest share of the continuous pharmaceutical manufacturing market at 43.6% in 2025, anchored by FDA regulatory support and concentrated investment from large integrated pharmaceutical companies and CDMOs based in the United States. Europe represents the second-largest region, with Germany, Switzerland, Ireland, and the United Kingdom constituting the primary manufacturing hubs. Asia Pacific is the fastest-growing regional market, with China, India, and Japan investing in continuous manufacturing infrastructure to support domestic pharmaceutical production and export competitiveness. The continuous pharmaceutical manufacturing market is also benefiting from integration with artificial intelligence and digital twin technologies, which improve real-time process control, reduce batch failure rates, and support predictive maintenance — factors that collectively strengthen the investment case for CPM adoption through 2034.

, By End-User (Pharma Companies, CDMOs, Research Institutes), By Offering (Equipment, Software, Services) Industry Trends, Market Dynamics & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global continuous pharmaceutical manufacturing market was valued at USD 3.42 Billion in 2025 and is projected to reach USD 9.18 Billion by 2034, expanding at a CAGR of 11.6% during the forecast period 2026–2034.

- Segment Dominance: By technology, continuous oral solid dosage (OSD) manufacturing leads with approximately 48.3% of market revenue in 2025, driven by its extensive application in small-molecule drug production across branded and generic pharmaceutical manufacturers.

- Segment Dominance: By end-user, integrated pharmaceutical manufacturers account for the largest share at 54.7% of market revenue in 2025, as large pharma companies lead CPM investment through direct technology adoption and strategic CDMO partnerships.

- Driver: FDA regulatory support through the ICH Q13 guideline on continuous manufacturing, effective from 2024, has reduced submission uncertainty and is directly accelerating CPM adoption across NDA and ANDA filings in the United States and EU.

- Restraint: High capital expenditure requirements for CPM line installation — averaging USD 15–30 Million per production suite — constrain adoption among small and mid-sized generic manufacturers, limiting market penetration in cost-sensitive segments by an estimated 10–15%.

- Opportunity: The application of continuous manufacturing to API synthesis via flow chemistry represents an incremental addressable revenue opportunity exceeding USD 2.1 Billion through 2034, as flow reactors achieve improved safety profiles and yield rates versus batch chemistry for hazardous and exothermic reactions.

- Trend: Digital twin integration within CPM lines is gaining traction, with approximately 21.4% of new continuous manufacturing installations incorporating digital process simulation tools in 2025, enabling real-time-release testing and reducing physical QC sampling requirements by 30–45%.

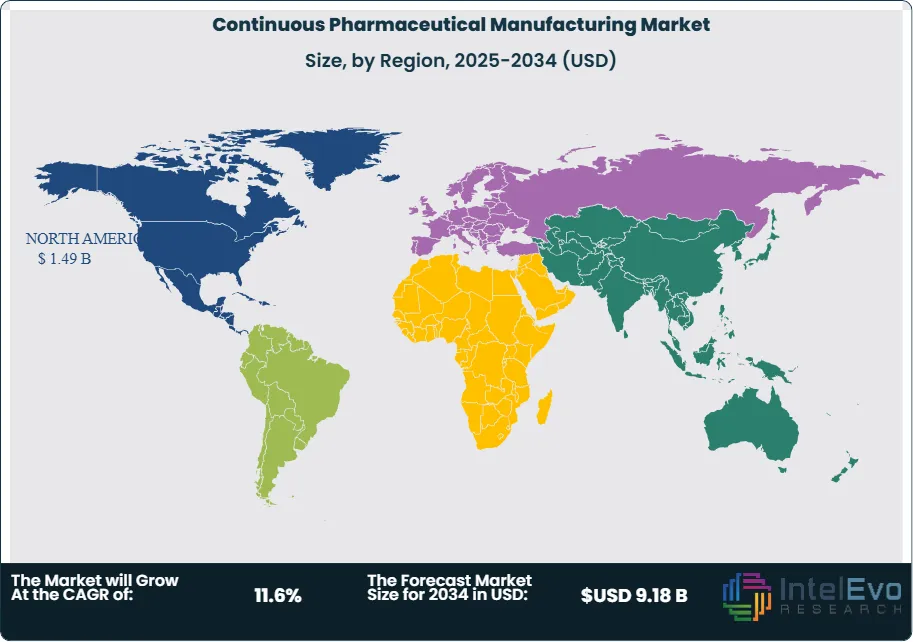

- Regional Analysis: North America leads the global continuous pharmaceutical manufacturing market with a 43.6% share in 2025, generating approximately USD 1.49 Billion in revenue, underpinned by FDA's active promotion of CPM and heavy investment by US-based pharmaceutical manufacturers.

Competitive Landscape Overview

The continuous pharmaceutical manufacturing market is moderately consolidated, with the top four players — GEA Group, Thermo Fisher Scientific, Sartorius AG, and Siemens AG — collectively accounting for approximately 46.8% of global market revenue in 2025. Competition is primarily technology-driven, with suppliers differentiating on integrated line architecture, PAT-sensor compatibility, regulatory submission support, and digital process control software. M&A activity has increased since 2023, as equipment manufacturers pursue acquisitions of PAT software developers and flow chemistry specialists to build vertically integrated CPM platforms.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product | Geo Strength | Recent Strategic Move (2024–2026) |

| GEA Group | Germany | Leader | GAIA Continuous Tablet Line | Europe / Global | Jan 2025: Expanded continuous OSD line portfolio with a new integrated wet granulation-to-compression module targeting generics manufacturers. |

| Thermo Fisher Scientific | USA | Leader | Thermo Scientific TSG Continuous Granulator | North America / Global | Apr 2025: Launched an AI-driven process control module for its continuous OSD platform, targeting FDA PAT-compliant real-time release. |

| Sartorius AG | Germany | Leader | BioStat Continuous Bioprocessing Platform | Europe / Global | Jun 2025: Signed a development agreement with a major European CDMO to co-develop a fully integrated continuous bioprocessing line for biologics. |

| Siemens AG | Germany | Leader | SIMATIC Pharma Suite (Digital Twin) | Europe / North America | Mar 2025: Introduced a digital twin module specifically for continuous pharma lines, integrating with FDA Part 11-compliant data management systems. |

| Hosokawa Micron | Japan | Challenger | Continuous Blending & Granulation Systems | Asia Pacific / Europe | Feb 2026: Entered a distribution partnership with an Indian generics manufacturer to deploy continuous OSD lines across three production sites. |

| Glatt GmbH | Germany | Challenger | ConsiGma Continuous Processing Platform | Europe | Nov 2024: Launched an upgraded ConsiGma tablet line with integrated NIR-based PAT monitoring for real-time blend uniformity analysis. |

| Freund Corporation | Japan | Challenger | GPCG Continuous Fluid Bed Processor | Asia Pacific | Aug 2025: Secured contracts with two Japanese generics manufacturers for continuous film-coating system installations. |

| Continuous Pharmaceuticals (CP) | UK | Niche Player | Continuus Flow Chemistry Platform | Europe / North America | May 2025: Completed a USD 28 Million Series B funding round to scale its continuous API synthesis platform for hazardous reaction chemistry. |

| Continuus Pharmaceuticals | USA | Niche Player | Integrated Continuous Manufacturing (ICM) System | North America | Jan 2026: Partnered with a US-based generics manufacturer to deploy its end-to-integrated API-to-tablet continuous manufacturing system at commercial scale. |

| Pfizer CentreOne | USA | Niche Player | Continuous Manufacturing CDMO Services | North America | Sep 2025: Expanded its continuous manufacturing CDMO service offering to external clients, leveraging infrastructure built for internal Pfizer products. |

By Technology

The continuous pharmaceutical manufacturing market by technology is led by continuous oral solid dosage (OSD) manufacturing systems, which account for approximately 48.3% of total market revenue in 2025, valued at USD 1.65 Billion. This segment encompasses continuous granulation, blending, direct compression, film coating, and integrated wet or dry granulation-to-compression lines. OSD is the most commercially mature CPM technology, with multiple FDA-approved products manufactured via continuous OSD processes, including Prezista (darunavir) by Johnson & Johnson — one of the earliest commercial-scale continuous manufacturing approvals. Equipment in this category typically integrates roller compactor or twin-screw granulator units with in-line blend monitoring via near-infrared (NIR) spectroscopy. The OSD segment is growing at a 10.8% CAGR through 2034, driven by generic manufacturers seeking cost reduction through continuous processing and large pharma companies advancing continuous manufacturing for new molecular entities under FDA's Emerging Technology Program.

Continuous bioprocessing represents the second-largest technology segment at 26.4% of market revenue in 2025, or USD 0.90 Billion. This segment includes perfusion bioreactors, continuous downstream processing with periodic counter-current chromatography (PCC), and integrated upstream-to-downstream continuous biologics production lines. The FDA's growing acceptance of continuous bioprocessing, reinforced by ICH Q13, has accelerated adoption among biopharmaceutical manufacturers seeking to reduce manufacturing cost per gram for high-volume biologics such as monoclonal antibodies and recombinant proteins. Continuous bioprocessing reduces buffer consumption by 30–50% and equipment footprint by up to 60% versus traditional batch bioreactors at equivalent output. This segment is projected to grow at 13.2% CAGR through 2034, the fastest among all technology segments.

Continuous API synthesis via flow chemistry accounts for 16.8% of market revenue in 2025 at USD 0.57 Billion. Flow reactors enable precise control of reaction temperature, pressure, and residence time, making them particularly advantageous for exothermic and hazardous chemical reactions that present safety challenges in large-batch stirred-tank reactors. Regulatory submissions incorporating flow chemistry-derived APIs have increased substantially since 2022, as ICH Q13 guidance provides a clear framework for process description and validation. The remaining 8.5% of market revenue is distributed across continuous lyophilization, continuous sterile fill-finish, and other emerging continuous dosage form technologies that are still in early-to-mid adoption phases.

By End-User

By end-user, integrated pharmaceutical manufacturers represent the largest segment within the continuous pharmaceutical manufacturing market, generating 54.7% of revenue in 2025 at USD 1.87 Billion. Large integrated pharma companies — including those within the global top 20 by revenue — have driven the first wave of CPM adoption, investing capital in continuous manufacturing lines for internally developed products where long product lifecycle economics justify the upfront conversion cost. These manufacturers also operate dedicated technology development programs aligned with FDA's Emerging Technology Program and EMA's PRIME scheme, positioning continuous manufacturing as a quality differentiation tool in regulatory submissions. CDMOs comprise the second-largest end-user group at 28.9% of revenue in 2025, or USD 0.99 Billion. CDMOs serve diverse client pipelines and are well-positioned to amortize continuous manufacturing equipment investment across multiple product campaigns. Academic research institutes, technology development organizations, and government-funded manufacturing centers account for 11.4% of market revenue, primarily through equipment procurement for process development and technology demonstration programs. Other end-users make up the remaining 5.0%.

By Offering

By offering, equipment and systems constitute the largest revenue category in the continuous pharmaceutical manufacturing market at 62.4% of 2025 market value, or USD 2.13 Billion. This category includes all physical CPM line components: granulators, blenders, compressors, coaters, bioreactors, flow reactors, and filtration systems, as well as integrated turnkey continuous manufacturing lines supplied by full-system vendors. Software and digital solutions, encompassing process analytical technology (PAT) platforms, manufacturing execution systems (MES) integrated with continuous process data, and digital twin simulation software, represent 22.6% of market revenue at USD 0.77 Billion. Software is the fastest-growing offering category at 16.4% CAGR through 2034, as manufacturers invest in data infrastructure to support real-time release testing and regulatory compliance. Services — including process development consulting, technology transfer, validation support, and regulatory filing assistance — account for the remaining 15.0% at USD 0.51 Billion.

Regional Analysis

North America Continuous Pharmaceutical Manufacturing Market

North America holds a 43.6% share of the global continuous pharmaceutical manufacturing market in 2025, generating approximately USD 1.49 Billion in revenue. The United States is the dominant market, driven by FDA's consistent institutional support for CPM since at least 2016, when Commissioner-level endorsements of continuous manufacturing began appearing in agency communications. The FDA's Emerging Technology Program, which provides early technical engagement for manufacturers developing novel production platforms, had processed over 50 CPM-related requests by 2024, with many resulting in NDA and ANDA approvals for continuously manufactured drug products. Major pharmaceutical companies headquartered in New Jersey, Illinois, Indiana, and Massachusetts have invested cumulatively over USD 800 Million in continuous manufacturing infrastructure within the United States between 2019 and 2025. Canada contributes to regional demand through its National Research Council-supported pharmaceutical process intensification programs and a growing CDMO sector in Ontario and Quebec with CPM capabilities. The North America continuous pharmaceutical manufacturing market is projected to grow at a 10.9% CAGR through 2034, reaching USD 3.79 Billion.

Europe Continuous Pharmaceutical Manufacturing Market

Europe accounts for 29.4% of the continuous pharmaceutical manufacturing market in 2025 at USD 1.01 Billion. Germany, Switzerland, and Ireland are the primary manufacturing hubs, hosting the European operations of several global pharmaceutical leaders with CPM lines operating at commercial scale. The EMA's adoption of ICH Q13 as a formal guideline in 2024 resolved previous regulatory uncertainty and accelerated CPM-related submissions in the EU. Switzerland's pharmaceutical cluster — anchored by Novartis and Roche — has invested substantially in continuous manufacturing process development, with Novartis operating a dedicated continuous manufacturing development facility in Basel. Ireland's position as a preferred EU pharmaceutical manufacturing location has attracted CPM investment from US-headquartered pharma companies seeking EU manufacturing presence, with several facilities in County Cork and Dublin incorporating continuous processing lines. The United Kingdom, post-Brexit, continues to develop CPM capabilities through its Medicines Manufacturing Innovation Centre (MMIC) in Glasgow, a public-private research facility providing continuous manufacturing scale-up services to the UK pharma sector. Europe's continuous pharmaceutical manufacturing market is expected to grow at a 11.3% CAGR through 2034.

Asia Pacific Continuous Pharmaceutical Manufacturing Market

Asia Pacific represents 18.8% of the global continuous pharmaceutical manufacturing market in 2025 at USD 0.64 Billion and is the fastest-growing region with a projected CAGR of 14.2% through 2034. China's pharmaceutical manufacturing sector is undergoing technology modernization, with the National Medical Products Administration (NMPA) issuing guidance in 2023 aligning with ICH Q13 principles and encouraging continuous manufacturing adoption among domestic producers. Several large Chinese generic pharmaceutical groups have announced CPM pilot programs as part of broader quality system upgrades. India's generics manufacturing sector, which supplies approximately 20% of global generic drug volume by value, is beginning to invest in continuous manufacturing to improve cost competitiveness and quality consistency, supported by the government's Production Linked Incentive (PLI) scheme for pharmaceuticals. Japan's pharmaceutical industry, dominated by established domestic innovators and generics manufacturers, is investing in continuous manufacturing for solid dosage forms and bioprocessing applications, with regulatory clarity provided by PMDA guidelines aligning with ICH Q13. South Korea's growing CDMO sector contributes to regional demand.

Latin America Continuous Pharmaceutical Manufacturing Market

Latin America holds a 5.2% share of the continuous pharmaceutical manufacturing market in 2025, valued at approximately USD 0.18 Billion. Brazil is the dominant regional market, with ANVISA's progressive regulatory alignment with international standards supporting CPM technology adoption among domestic pharmaceutical manufacturers. Fiocruz and Instituto Butantan, Brazil's major public health pharmaceutical producers, have each evaluated continuous manufacturing for vaccine and API production. Mexico's pharmaceutical sector, partly oriented toward supplying the US market, is exploring continuous manufacturing as a competitive tool, with several CDMO facilities near Mexico City and Guadalajara conducting pilot studies. Argentina contributes to regional demand through its active domestic pharmaceutical industry, which serves both local and South American export markets. Infrastructure constraints, including limited access to domestic PAT equipment suppliers and qualified engineering talent for CPM line design, moderate growth relative to other regions, but multilateral investment from international pharma equipment companies is bridging these gaps. Latin America's CPM market is projected to grow at 9.6% CAGR through 2034.

Middle East & Africa Continuous Pharmaceutical Manufacturing Market

The Middle East and Africa region accounts for 3.0% of global continuous pharmaceutical manufacturing market revenue in 2025 at USD 0.10 Billion. Saudi Arabia and the UAE are the primary markets within the Gulf Cooperation Council (GCC), where National Transformation Programs and Vision 2030 initiatives are driving investment in domestic pharmaceutical production and manufacturing modernization. Saudi Arabia's Saudi Food and Drug Authority (SFDA) has taken steps to align drug manufacturing guidelines with ICH standards, including ICH Q13, creating a regulatory foundation for CPM adoption. South Africa represents the most developed pharmaceutical manufacturing base in sub-Saharan Africa, with several manufacturers evaluating continuous processing for generic oral solid dosage forms. The MEA region's CPM market remains early-stage, with activity concentrated in technology awareness, feasibility assessments, and small-scale pilot installations. International pharmaceutical equipment suppliers are actively engaging GCC-based manufacturers through demonstration projects and public-private investment frameworks. MEA's continuous pharmaceutical manufacturing market is projected to grow at a 12.1% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- Continuous Oral Solid Dosage (OSD) Manufacturing

- Continuous Bioprocessing

- Continuous API Synthesis (Flow Chemistry)

- Continuous Lyophilization & Sterile Fill-Finish

- Other Continuous Dosage Form Technologies

By End-User

- Integrated Pharmaceutical Manufacturers

- Contract Development & Manufacturing Organizations (CDMOs)

- Academic Research Institutes & Technology Development Centers

- Other End-Users

By Offering

- Equipment & Systems

- Software & Digital Solutions (PAT, MES, Digital Twin)

- Services (Process Development, Validation, Regulatory Support)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.42 B |

| Forecast Revenue (2034) | USD 9.18 B |

| CAGR (2025-2034) | 11.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Continuous Oral Solid Dosage (OSD) Manufacturing, Continuous Bioprocessing, Continuous API Synthesis (Flow Chemistry), Continuous Lyophilization & Sterile Fill-Finish, Other Continuous Dosage Form Technologies), By End-User, (Integrated Pharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Academic Research Institutes & Technology Development Centers, Other End-Users), By Offering, (Equipment & Systems, Software & Digital Solutions (PAT, MES, Digital Twin), Services (Process Development, Validation, Regulatory Support)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GEA GROUP, THERMO FISHER SCIENTIFIC, SARTORIUS AG, SIEMENS AG, HOSOKAWA MICRON GROUP, GLATT GMBH, FREUND CORPORATION, CONTINUOUS PHARMACEUTICALS (CP), CONTINUUS PHARMACEUTICALS, PFIZER CENTREONE, JOHNSON & JOHNSON (JANSSEN SUPPLY CHAIN), ELI LILLY AND COMPANY, VERTEX PHARMACEUTICALS, HOVIONE, LONZA GROUP, CHARLES RIVER LABORATORIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Pharma Companies, CDMOs, Research Institutes), By Offering (Equipment, Software, Services) Industry Trends, Market Dynamics & Forecast 2026–2034")

, By End-User (Pharma Companies, CDMOs, Research Institutes), By Offering (Equipment, Software, Services) Industry Trends, Market Dynamics & Forecast 2026–2034")

, By End-User (Pharma Companies, CDMOs, Research Institutes), By Offering (Equipment, Software, Services) Industry Trends, Market Dynamics & Forecast 2026–2034")

Frequently Asked Questions

How big is the Continuous Pharmaceutical Manufacturing Market?

Global Continuous pharma manufacturing market valued at USD 3.06B in 2024, reaching USD 9.18B by 2034, growing at a CAGR of 11.6% from 2026–2034.

Who are the major players in the Continuous Pharmaceutical Manufacturing Market?

GEA GROUP, THERMO FISHER SCIENTIFIC, SARTORIUS AG, SIEMENS AG, HOSOKAWA MICRON GROUP, GLATT GMBH, FREUND CORPORATION, CONTINUOUS PHARMACEUTICALS (CP), CONTINUUS PHARMACEUTICALS, PFIZER CENTREONE, JOHNSON & JOHNSON (JANSSEN SUPPLY CHAIN), ELI LILLY AND COMPANY, VERTEX PHARMACEUTICALS, HOVIONE, LONZA GROUP, CHARLES RIVER LABORATORIES, Others

Which segments covered the Continuous Pharmaceutical Manufacturing Market?

By Technology, (Continuous Oral Solid Dosage (OSD) Manufacturing, Continuous Bioprocessing, Continuous API Synthesis (Flow Chemistry), Continuous Lyophilization & Sterile Fill-Finish, Other Continuous Dosage Form Technologies), By End-User, (Integrated Pharmaceutical Manufacturers, Contract Development & Manufacturing Organizations (CDMOs), Academic Research Institutes & Technology Development Centers, Other End-Users), By Offering, (Equipment & Systems, Software & Digital Solutions (PAT, MES, Digital Twin), Services (Process Development, Validation, Regulatory Support))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Continuous Pharmaceutical Manufacturing Market

Published Date : 30 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date