- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

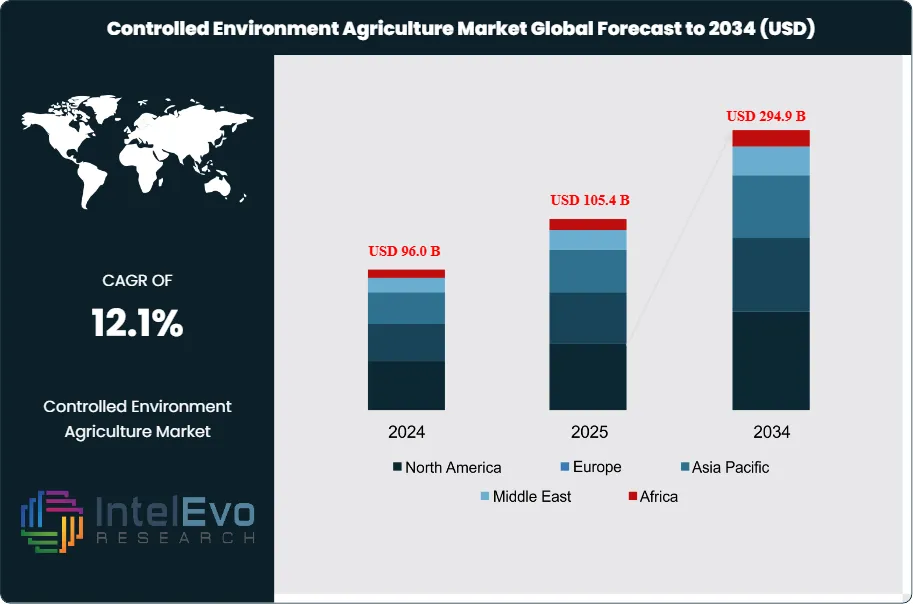

Global Controlled Environment Agriculture Market Size | CAGR of 12.1%

Global Controlled Environment Agriculture Market Size, Share, Analysis By Facility (Greenhouses, Vertical, Indoor, Container Farms), By Method (Hydroponics, Aeroponics, Aquaponics, Soil), By Crop (Leafy Greens, Fruits, Vegetables, Herbs, Flowers), By Component (Hardware, Software, Services), By End-User Region, Key Players – Dynamics, Precision Farming & Indoor AgTech Automation Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 105.4 Billion | USD 294.9 Billion | 12.1% | North America, 38.5% |

The Controlled Environment Agriculture Market was valued at USD 96.0 Billion in 2024 and is estimated to reach USD 105.4 Billion in 2025. The market is projected to grow to USD 294.9 Billion by 2034, expanding at a CAGR of 12.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 189.5 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe Controlled Environment Agriculture market sits at the intersection of food security policy, water scarcity, and retailer consolidation around year-round local supply. United States Department of Agriculture (USDA) data shows that domestic CEA facilities expanded by more than 28% between 2020 and 2024, and Signify field trials confirm leafy-green yields can reach 30 times open-field output per acre. Hydroponic systems use up to 90% less water than soil-based farming, a margin that drives procurement decisions across drought-exposed states such as California, Arizona, and Texas.

The competitive set has reshaped sharply since 2023. Bowery Farming wound down operations in November 2024, AeroFarms moved through Chapter 11 reorganization and stakeholder rescue financing in December 2025, and Plenty Unlimited Inc. filed Chapter 11 protection on March 23, 2025 before emerging on May 29, 2025 with a strategy concentrated on vertical strawberries with Driscoll's. The 80 Acres Farms and Soli Organic combination announced on August 18, 2025 created an indoor farming network with first-year revenues approaching USD 200 Million across more than 17,000 retail locations.

Regulatory framing tightens through 2026. The FDA Food Traceability Final Rule under FSMA Section 204 carried a January 20, 2026 compliance date covering leafy greens, fresh-cut produce, herbs, tomatoes, peppers, sprouts, and other items dominant in CEA portfolios. The agency proposed a 30-month extension to July 2028, while the FY 2026 appropriations bill imposed funding limits on Rule 204 enforcement and required quarterly industry engagement on flexibilities. Operators preparing lot-code traceability systems gained a procurement advantage with retailers who continue to require Key Data Elements regardless of FDA enforcement timing.

Asia Pacific demand growth runs ahead of every other region, anchored by Singapore's 30 by 30 food self-sufficiency target, Japan's plant factory stock, and intelligent greenhouse build-outs across China's peri-urban corridors. North America led on installed base in 2025, with the United States supported by USDA Urban Agriculture and Innovative Production grants of USD 14.4 Million announced on January 8, 2025 and a controlled-environment crop insurance program introduced in October 2023. Through 2034, market share will redistribute toward operators with proven unit economics. Energy costs above USD 2 per kilogram now disqualify new venture funding rounds, automation embeds across seeding and harvest, and infrastructure capital from pension funds and retail-strategic investors increasingly displaces early-stage venture money.

Market Definition & Scope

The Controlled Environment Agriculture market covers food and ornamental crop production within enclosed structures where light, temperature, humidity, carbon dioxide, and nutrient delivery are actively regulated. The market encompasses commercial greenhouses, vertical farms, plant factories with artificial lighting, growth chambers, container farms, and high tunnels equipped with active climate control. Core technology stacks include LED horticultural lighting, hydroponic and aeroponic nutrient delivery, automated environmental controls, IoT sensors, and HVAC systems engineered for plant production.

Scope includes hardware (lighting, HVAC, irrigation, fertigation, sensors, automation), software (climate management, crop scheduling, traceability), and operating services across crop categories ranging from leafy greens and tomatoes to berries, mushrooms, herbs, and cannabis. Open-field organic farming, rooftop agriculture without climate control, traditional unheated tunnels, and aquaculture for fish are explicitly excluded. The Controlled Environment Agriculture category sits within the broader smart agriculture and precision farming parent market and accounted for approximately 4.9% of total smart farming revenue in 2025. The geographic scope spans North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

, By Method (Hydroponics, Aeroponics, Aquaponics, Soil), By Crop (Leafy Greens, Fruits, Vegetables, Herbs, Flowers), By Component (Hardware, Software, Services), By End-User Region, Key Players – Dynamics, Precision Farming & Indoor AgTech Automation Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Global Controlled Environment Agriculture market grew from USD 105.4 Billion in 2025 toward an expected USD 294.9 Billion by 2034 at a CAGR of 12.1%.

- Segment Dominance: Greenhouses held the largest facility-type share at 41.0% in 2025, equivalent to USD 43.2 Billion in revenue, given lower capital intensity than fully indoor systems.

- Segment Dominance: Hydroponics led the growing-method category at 47.0% share in 2025, equivalent to USD 49.5 Billion, driven by adoption in leafy-green and herb production.

- Driver: FSMA Section 204 traceability requirements covering leafy greens, herbs, fresh-cut produce, tomatoes, peppers, and sprouts pushed retailers to commit to indoor and greenhouse suppliers with digital lot-code records, even after the FDA proposed a 30-month compliance extension to July 2028.

- Restraint: Energy expense remained the dominant operating cost for fully indoor operators, accounting for approximately 50% of total costs and contributing to 14 indoor-farming bankruptcies tracked across 2025 with combined historical funding above USD 1.37 Billion.

- Opportunity: The Asia Pacific region was projected to add roughly USD 17.5 Billion in incremental revenue by 2034, anchored by Japan, Singapore, China, South Korea, and India under national food security mandates.

- Trend: Off-take agreements and infrastructure-class capital displaced early-stage venture money during 2025, with deal flow concentrated on operators reporting gross margins above 30%.

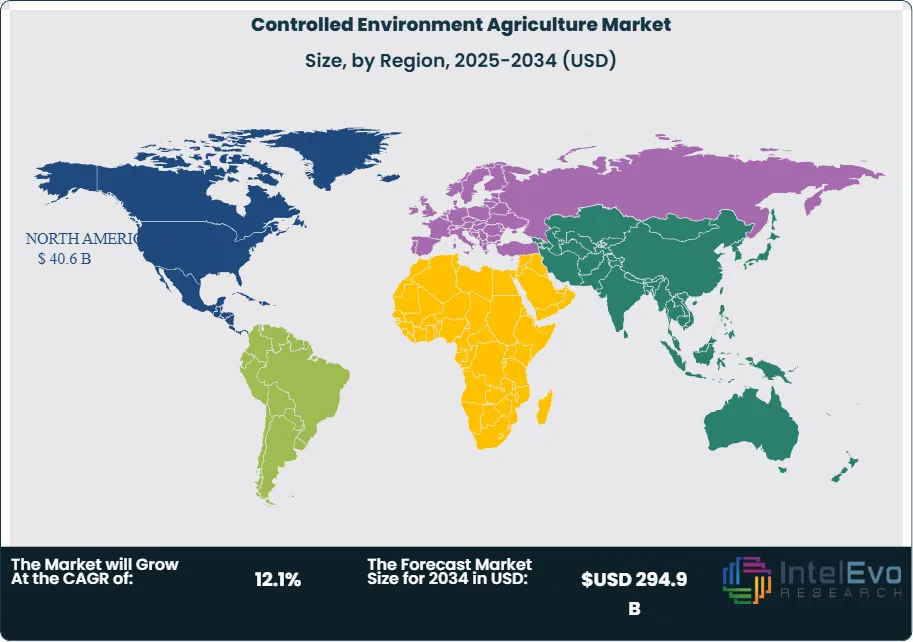

- Regional: North America held the largest regional share at 38.5%, equivalent to USD 40.6 Billion in 2025, supported by USDA grants and consumer preference for pesticide-free, locally grown produce.

Key Insights Summary

- Per Signify's company disclosures, lit greenhouse coverage worldwide is on track to reach roughly 30% of total surface area in 2025, climbing from approximately 20% in 2020, with LED systems capturing more than half of the lit footprint.

- Opened in September 2024, the Plenty Richmond Farm in Virginia was engineered with Driscoll's to harvest above 4 million pounds of strawberries annually within roughly 40,000 square feet, using vertical towers approaching 30 feet in height.

- USDA data referenced across industry reporting in 2025 indicated that more than 2,000 vertical farming modules were operating across the United States, with 70% deploying LED-based light recipes and 90% lower water draw versus soil farming.

- After closing its August 2025 combination with Soli Organic, 80 Acres Farms reached an annual production capacity range of 15 to 20 million pounds of fresh produce across seven sites, supplying over 17,000 retail outlets.

- Operated by Crop One Holdings with Emirates Flight Catering near Dubai International Airport, Bustanica spans 330,000 square feet and was sized to harvest more than 6,000 pounds of leafy greens daily.

- On January 8, 2025, the U.S. Department of Agriculture committed USD 14.4 Million in grants and technical assistance under the Urban Agriculture and Innovative Production initiative, building on USD 53.7 Million already invested since 2020.

- FAO data referenced in 2024 industry analysis indicated that vertical farming adoption across Asia accelerated nearly 33% during the year, with 1 hectare of vertical modules capable of yielding up to 45 times the leafy-green output of an open-field hectare.

Competitive Landscape Overview

The Controlled Environment Agriculture market remained moderately consolidated in 2025. Top four players combined controlled approximately 22-26% of global revenue, with the rest of the field split across regional greenhouse operators, technology suppliers, and emerging vertical farm specialists. The Netherlands, the United States, and Japan continued to anchor technology supply, while production volume concentrated in North America and Western Europe.

Competition shifted from venture-funded land-grab to operator quality. Energy efficiency, off-take agreements with grocery chains, and proprietary breeding programs replaced footprint expansion as the primary differentiators. Bankruptcies through 2024 and 2025 - including Bowery Farming's wind-down, AeroFarms's restructuring, and Plenty's Chapter 11 - cleared distressed assets that survivors picked up at discounted prices, including 80 Acres Farms' purchase of facilities and IP from vertical farming pioneer Kalera.

Strategic capital from retailers, infrastructure investors, and food groups now dominates fresh deal flow. Taylor Farms's March 2026 purchase of Equinox Growers from Generate Capital, Walmart's continued partnership with the Plenty/Driscoll's strawberry program, and the Public Investment Fund of Saudi Arabia's role in earlier AeroFarms Riyadh build illustrate how the market's largest incumbents secured supply alongside specialist operators.

Competitive Landscape Matrix

| Company | Headquarters | Position | Key Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Signify N.V. | Eindhoven, Netherlands | Leader | Philips horticulture LED systems with GrowWise control | Europe, North America, APAC | Rolled out the GrowWise smart spectrum algorithm in June 2025 |

| 80 Acres Farms | Hamilton, Ohio, US | Leader | GroLoop platform; vertical and indoor herb production | United States | Closed the combination with Soli Organic on August 18, 2025 |

| Gotham Greens | Brooklyn, New York, US | Leader | Hydroponic greenhouse leafy greens and prepared foods | United States | Brought Lee Quackenbush in as CFO on March 24, 2026 |

| Taylor Farms | Salinas, California, US | Leader | CEA leafy greens for retail and foodservice salads | North America | Took ownership of Equinox Growers from Generate Capital on March 24, 2026 |

| Plenty Unlimited | San Francisco, California, US | Challenger | Vertical strawberry towers with Driscoll's genetics | United States | Exited Chapter 11 reorganization on May 29, 2025 |

| Crop One Holdings | Dubai, UAE / California, US | Challenger | Bustanica indoor farm; airline catering supply | Middle East, North America | Continued daily Bustanica leafy-green output above 6,000 lbs through 2025 |

| Little Leaf Farms | Devens, Massachusetts, US | Challenger | Hydroponic greenhouse baby greens | Northeast US | Banked a USD 90 Million growth round led by Cavallo Ventures during 2024 |

| AeroFarms | Newark, New Jersey, US | Niche Player | Aeroponic microgreens supply for U.S. retail | United States | Secured emergency stakeholder financing on December 19, 2025 |

| Heliospectra AB | Gothenburg, Sweden | Niche Player | Intelligent LED lighting for greenhouses | Europe, North America | Continued upgrades to its data-driven control system through Q1 2026 |

Segmentation Analysis

The Controlled Environment Agriculture market is segmented across five primary classifications: facility type, growing method, crop, component, and end-user. Each segmentation reflects distinct capital requirements, operating economics, and adoption patterns shaped by retailer demand and regulatory pressure.

By Facility Type

The greenhouse segment captured 41.0% of CEA revenue in 2025, equivalent to USD 43.2 Billion, supported by lower capital intensity per square foot and suitability for tomatoes, peppers, cucumbers, and leafy greens at scale. Operators including Gotham Greens, Mucci Farms, NatureSweet, and Houweling's Group concentrated production in this segment, with Gotham Greens running 13 hydroponic greenhouses totaling more than 1.8 million square feet across nine U.S. states. Greenhouses outperformed vertical farms on energy intensity, drawing roughly 4 to 10 times less power per kilogram of output.

Vertical farms accounted for 27.0% of revenue at USD 28.5 Billion in 2025, but the segment also recorded the bulk of bankruptcies during 2024 and 2025. Plant factories with artificial lighting, growth chambers, and container farms together held the remaining 32.0%, equivalent to USD 33.7 Billion, with container farm specialists such as Freight Farms and Growcer concentrated in remote and emergency-supply deployments. Greenhouses delivered 14 percentage points more share than vertical farms in 2025, a gap industry analysis indicates will narrow only modestly through 2034 as automation reduces vertical-farm operating cost per kilogram.

By Growing Method

Hydroponics led the growing-method category at 47.0% revenue share in 2025, equivalent to USD 49.5 Billion. The technique conserves water above 90% versus soil farming and matches well with leafy-green economics across vertical and greenhouse formats. Aeroponics held 14.0% share at USD 14.8 Billion, dominated by AeroFarms' patented systems and adopted by Singrow and Aerospring Hydroponics for high-density urban deployments. Aquaponics accounted for 9.5% at USD 10.0 Billion, with Sky Greens in Singapore and Nelson & Pade Inc. in the United States representing the segment. Soil-based organic indoor systems and other methods filled the remaining 29.5% at USD 31.1 Billion, anchored by Soli Organic's USDA-certified herb production.

By Crop

Leafy greens, including lettuce, kale, spinach, and arugula, captured 38.0% of revenue in 2025 at USD 40.1 Billion, owing to short growth cycles of 28 to 35 days and high yield per square meter. Tomatoes and vine crops held 19.0% at USD 20.0 Billion, dominated by Dutch and Canadian greenhouse exporters. Herbs and microgreens covered 14.0% at USD 14.8 Billion, with AeroFarms' patented microgreen technology, Soli Organic's organic culinary herb leadership, and Square Roots' modular distribution. Strawberries and berries reached 9.0% at USD 9.5 Billion, with Driscoll's-Plenty Sweet vertical strawberries and Oishii's Omakase Berry redefining premium pricing. Mushrooms held 8.0% at USD 8.4 Billion. Cannabis and other specialty crops collectively accounted for 12.0% at USD 12.6 Billion.

By Component

Hardware contributed 55.0% of revenue in 2025, equivalent to USD 58.0 Billion, with horticultural lighting alone accounting for 37.1% of total CEA revenue. Signify's Philips GrowWise control system was deployed across more than 750 horticultural sites worldwide by mid-2025, defining the lighting benchmark. Climate control and HVAC followed, with Hoogendoorn, Priva, and Argus Control Systems Ltd. holding leading positions. Services represented 28.0% of the market at USD 29.5 Billion, covering installation, agronomy advisory, and managed services. Software accounted for 17.0% at USD 17.9 Billion, including AI-driven yield forecasting tools such as Square Roots' Sage assistant brought to market in mid-2025.

By End-User

Commercial growers held 53.1% of CEA revenue in 2025 at USD 56.0 Billion, anchored by 80 Acres Farms, Gotham Greens, Taylor Farms, Mucci Farms, and Little Leaf Farms. Retail and grocery chains operating private-label CEA programs accounted for 22.0% at USD 23.2 Billion, supported by partnerships such as Walmart-Plenty and Whole Foods-Gotham Greens. Foodservice and institutional buyers contributed 14.5% at USD 15.3 Billion, including Emirates Flight Catering's offtake from Crop One's Bustanica facility. Research and educational institutes plus other end-users filled the remaining 10.4% at USD 11.0 Billion, including USDA-funded Cooperative Extension programs at Land-Grant Universities.

Regional Analysis

The Controlled Environment Agriculture market spans five regions with sharply differentiated capital intensity, regulatory framing, and adoption maturity. Combined, the five regions accounted for approximately 100% of global revenue in 2025.

North America held 38.5% global share at USD 40.6 Billion in 2025, anchored by the United States and Canada. USDA Urban Agriculture and Innovative Production grants and a controlled-environment-specific crop insurance program brought policy support, while California, Texas, and Arizona water restrictions accelerated greenhouse procurement contracts. Canada's CEA build-out responded to long winters and grant programs from Agriculture and Agri-Food Canada. North American demand growth slowed during the venture correction of 2024 and 2025, then reaccelerated through retail-driven offtake agreements.

Europe captured 28.5% global share at USD 30.0 Billion in 2025, anchored by the Netherlands, Spain, Germany, France, and the United Kingdom. The European Union's Farm to Fork strategy, REACH compliance for nutrient and substrate inputs, and rising electricity costs after 2022 reshaped operator economics. Dutch greenhouse exporters including Royal Brinkman, Certhon, Richel Group, and Koppert Cress dominated technology supply, while Planet Farms in Italy and Nordic Harvest in Denmark expanded large-scale vertical operations. Energy-trading participation, enabled by Signify's GrowWise control upgrade in mid-2025, opened a new revenue line for Dutch and Belgian growers via Automatic Frequency Restoration Reserve.

Asia Pacific reached 22.5% global share at USD 23.7 Billion in 2025 and posted the fastest growth across all five regions. Singapore's 30 by 30 food self-sufficiency target, Japan's plant factory infrastructure, and China's peri-urban smart greenhouse build-outs anchored demand. China held 38.4% of APAC revenue, supported by intelligent greenhouse policy. Japanese operators including Spread Co. Ltd. and Mirai Co. Ltd. continued to scale plant factories with artificial lighting, while Korean and Singaporean players including Sky Greens and Singrow expanded across institutional and retail segments. India's Krishi 24/7 program, launched with Google and the Wadhwani Institute for Artificial Intelligence in November 2023, signaled emerging interest at scale.

Latin America accounted for 5.5% global share at USD 5.8 Billion in 2025, with Mexico's protected-cultivation tomato industry representing the largest national submarket. Brazil's sustainable farming policy and growing private-equity interest drove pilot and pre-commercial vertical farm rollouts, while Chile and Argentina expanded berry-focused greenhouse production for export markets.

Middle East & Africa captured 5.0% global share at USD 5.3 Billion in 2025, propelled by Gulf food-security mandates and water-scarcity policies. The UAE's National Food Security Strategy 2051, highlighted at Gulfood 2026, sustained Bustanica's daily output above 6,000 pounds and supported new investment from Mawarid Holding via its Plenty joint venture. Saudi Arabia's Public Investment Fund continued vertical-farm partnerships. South Africa anchored sub-Saharan growth through agritech-startup investment.

Country Analysis

The Controlled Environment Agriculture market concentrates across four national markets that together accounted for over 50% of global revenue in 2025. Each country reflects a distinct policy stack, technology mix, and retail-buyer dynamic.

The United States led globally with USD 28.5 Billion in 2025 revenue and a country-level CAGR of 11.8% through 2034. USDA Office of Urban Agriculture and Innovative Production grants of USD 14.4 Million in January 2025, the controlled-environment crop insurance program introduced in October 2023, and the FDA Food Traceability Final Rule under FSMA Section 204 collectively shape procurement decisions. State initiatives including New York's hydroponics partnership programs, California's water restrictions in the Central Valley, and Texas drought-relief provisions added regional layers. Domestic incumbents including Gotham Greens, 80 Acres Farms, Taylor Farms, Plenty, Little Leaf Farms, BrightFarms, Local Bounti, and Eden Green Technology supplied retailers including Whole Foods, Walmart, Kroger, Albertsons, Publix, and Harris Teeter.

China held USD 9.1 Billion in 2025 revenue at a country CAGR of 14.5%, supported by intelligent greenhouse build-outs in peri-urban areas around Beijing, Shanghai, Guangzhou, and Shenzhen. Sky Greens-style multi-tier vertical systems, the Krishi-equivalent smart farming initiatives launched under the 14th Five-Year Plan, and provincial subsidy programs anchored expansion. Domestic LED suppliers and the AeroFarms-Public Investment Fund Riyadh facility's technology transfer signaled cross-border investment flow.

The Netherlands recorded USD 8.7 Billion in 2025 at a country CAGR of 9.6%, lower than emerging markets but anchored on the deepest greenhouse technology stack worldwide. Dutch suppliers including Priva, Hoogendoorn, Royal Brinkman, Certhon, and Koppert Biological Systems exported climate-control, irrigation, and biological pest-management technology globally. Westland-region tomato and pepper production continued to set the global benchmark for yield per square meter, while the Greenport Holland Express logistics network shipped greenhouse output across the European Union within 24 to 36 hours.

Japan registered USD 5.2 Billion in 2025 at a country CAGR of 13.4%. Spread Co. Ltd., Mirai Co. Ltd., and other plant factory operators continued capacity build-out under government smart-farming subsidies addressing high population density and limited arable land. Japan's regulatory acceptance of LED-grown produce in school lunch programs and retail channels including AEON Co. Ltd. and Seven & i Holdings reinforced demand. Energy costs remained the binding constraint, with operators concentrating on premium leafy greens and high-margin strawberries.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Facility Type

- Greenhouses

- Vertical Farms

- Indoor Farms

- Container Farms

- Others

By Growing Method

- Hydroponics

- Aeroponics

- Aquaponics

- Soil-Based Cultivation

By Crop

- Leafy Greens

- Fruits & Vegetables

- Herbs & Microgreens

- Flowers & Ornamentals

- Others

By Component

- Hardware

- Software

- Services

By End-User

- Commercial Growers

- Research Institutions

- Retail & Grocery Chains

- Food Service Providers

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 105.4 B |

| Forecast Revenue (2034) | USD 294.9 B |

| CAGR (2025-2034) | 12.1% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Facility Type, (Greenhouses, Vertical Farms, Indoor Farms, Container Farms, Others), By Growing Method, (Hydroponics, Aeroponics, Aquaponics, Soil-Based Cultivation), By Crop, (Leafy Greens, Fruits & Vegetables, Herbs & Microgreens, Flowers & Ornamentals, Others), By Component, (Hardware, Software, Services), By End-User, (Commercial Growers, Research Institutions, Retail & Grocery Chains, Food Service Providers, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SIGNIFY N.V., 80 ACRES FARMS, GOTHAM GREENS, TAYLOR FARMS, PLENTY UNLIMITED INC., AEROFARMS, CROP ONE HOLDINGS, LITTLE LEAF FARMS, BRIGHTFARMS, MUCCI FARMS, NATURESWEET, HOUWELING'S GROUP, REVOL GREENS, LOCAL BOUNTI, EDEN GREEN TECHNOLOGY, SPREAD CO. LTD., MIRAI CO. LTD., SKY GREENS, HELIOSPECTRA AB, ARGUS CONTROL SYSTEMS LTD., PRIVA, HOOGENDOORN, RICHEL GROUP, CERTHON, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Method (Hydroponics, Aeroponics, Aquaponics, Soil), By Crop (Leafy Greens, Fruits, Vegetables, Herbs, Flowers), By Component (Hardware, Software, Services), By End-User Region, Key Players – Dynamics, Precision Farming & Indoor AgTech Automation Trends & Forecast 2026-2034")

, By Method (Hydroponics, Aeroponics, Aquaponics, Soil), By Crop (Leafy Greens, Fruits, Vegetables, Herbs, Flowers), By Component (Hardware, Software, Services), By End-User Region, Key Players – Dynamics, Precision Farming & Indoor AgTech Automation Trends & Forecast 2026-2034")

, By Method (Hydroponics, Aeroponics, Aquaponics, Soil), By Crop (Leafy Greens, Fruits, Vegetables, Herbs, Flowers), By Component (Hardware, Software, Services), By End-User Region, Key Players – Dynamics, Precision Farming & Indoor AgTech Automation Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Controlled Environment Agriculture Market?

Global Controlled Environment Agriculture Market was valued at USD 105.4 Billion in 2025 and is projected to reach USD 294.9 Billion by 2034, growing at a CAGR of 12.1% during 2026–2034. Explore market trends, growth drivers, opportunities, segmentation, competitive landscape, and industry insights.

Who are the major players in the Controlled Environment Agriculture Market?

SIGNIFY N.V., 80 ACRES FARMS, GOTHAM GREENS, TAYLOR FARMS, PLENTY UNLIMITED INC., AEROFARMS, CROP ONE HOLDINGS, LITTLE LEAF FARMS, BRIGHTFARMS, MUCCI FARMS, NATURESWEET, HOUWELING'S GROUP, REVOL GREENS, LOCAL BOUNTI, EDEN GREEN TECHNOLOGY, SPREAD CO. LTD., MIRAI CO. LTD., SKY GREENS, HELIOSPECTRA AB, ARGUS CONTROL SYSTEMS LTD., PRIVA, HOOGENDOORN, RICHEL GROUP, CERTHON, Others

Which segments covered the Controlled Environment Agriculture Market?

By Facility Type, (Greenhouses, Vertical Farms, Indoor Farms, Container Farms, Others), By Growing Method, (Hydroponics, Aeroponics, Aquaponics, Soil-Based Cultivation), By Crop, (Leafy Greens, Fruits & Vegetables, Herbs & Microgreens, Flowers & Ornamentals, Others), By Component, (Hardware, Software, Services), By End-User, (Commercial Growers, Research Institutions, Retail & Grocery Chains, Food Service Providers, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Controlled Environment Agriculture Market

Published Date : 15 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date