- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Conversational AI & Virtual Agents Market Size & Forecast 2034

Global Conversational AI and Virtual Agents Market Size, Share, and In-Depth Analysis By Component (Solutions, Services, Professional Services, Managed Services), By Deployment (Cloud, On-Premises), By Technology (NLP, Machine Learning, ASR, Text-to-Speech), By End User (BFSI, Healthcare, IT & Telecom, Retail & eCommerce, Education) Industry Outlook, Regional Analysis, Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034

Report Overview

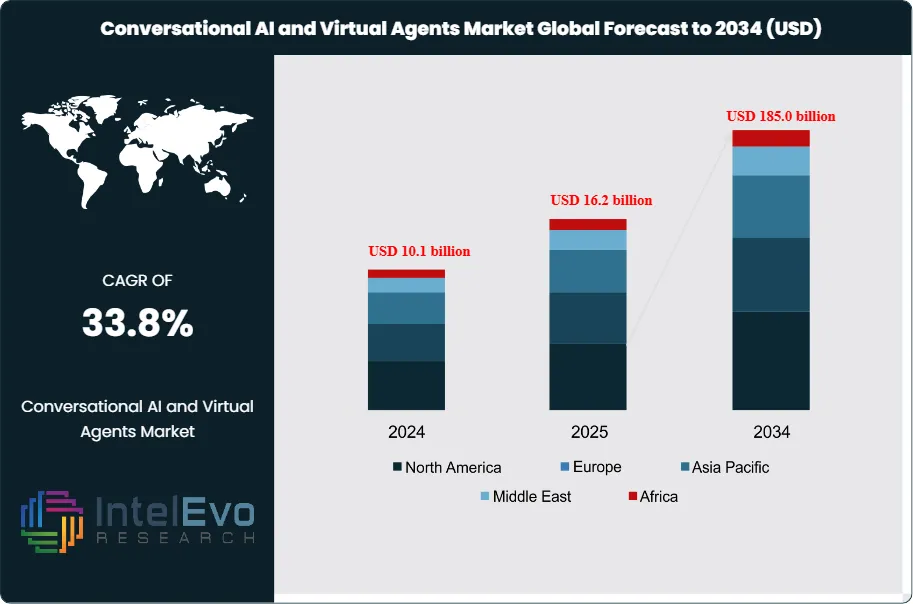

The Conversational AI and Virtual Agents Market is estimated to reach approximately USD 16.2 billion in 2025 and is projected to expand significantly to around USD 185.0 billion by 2034. Based on an estimated USD 18.0 billion market size in 2026, the market is expected to register a robust CAGR of about 33.8% during the forecast period from 2026 to 2034. This rapid expansion is driven by accelerating enterprise adoption of AI-powered customer engagement solutions, rising deployment of virtual agents across contact centers, banking, healthcare, and e-commerce, and continuous advances in natural language processing and generative AI. Growing demand for scalable, always-on customer support and cost-efficient automation further positions conversational AI as a core component of enterprise digital transformation strategies, supporting strong market momentum across global platforms.

Get More Information about this report -

Request Free Sample ReportThis trajectory reflects rapid adoption of AI-driven dialogue systems across customer-facing and internal workflows. Enterprises deploy text and voice interfaces to automate high-volume interactions, shorten response times, and standardize service quality across channels and regions.

The market centers on platforms and solutions that simulate human dialogue, interpret intent, and execute tasks through natural language. Advances in large language models, speech recognition, and multimodal interfaces raise automation rates and reduce the need for human intervention in routine queries. On the demand side, sectors such as banking, telecommunications, retail, healthcare, and travel seek to manage rising interaction volumes without proportional increases in headcount. On the supply side, global cloud providers, independent software vendors, and specialized startups scale subscription and usage-based offerings, pushing down unit costs and expanding addressable demand.

Customer experience and operational efficiency remain primary growth drivers. Enterprises use virtual agents to provide 24/7 support, personalize journeys, and reduce call-center load, which translates into measurable cost savings and higher satisfaction scores. Cloud-native architectures and API-driven integration accelerate deployment across web, mobile, contact centers, and internal service desks. At the same time, technology complexity and integration with legacy systems create execution risk, while model accuracy, latency, and language coverage differentiate leading vendors from followers.

Regulation and enterprise risk governance shape adoption patterns. Data protection rules, sector-specific compliance requirements, and emerging AI governance frameworks influence how organizations design, deploy, and monitor conversational systems. Concerns around data security, hallucinations, and algorithmic bias drive investment in model oversight, encryption, and audit trails. Vendors that embed transparent controls, regional data hosting, and responsible AI capabilities gain advantage in regulated verticals such as financial services and healthcare.

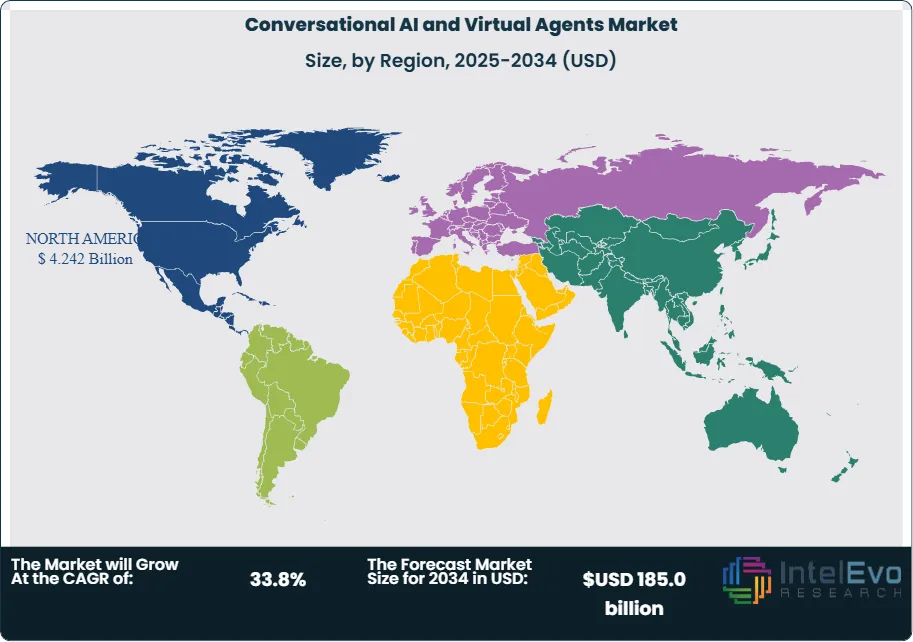

Regionally, North America leads adoption, accounting for 42.7% of global revenue in 2024 and generating about USD 5.8 Billion, with the U.S. projected to reach USD 4.67 Billion and grow at a 26.7% CAGR. Europe accelerates under strong focus on compliance and customer service transformation. Asia-Pacific emerges as a high-growth investment hotspot, supported by expanding digital economies, mobile-first engagement, and large multilingual populations. Across regions, rising labor costs, talent shortages in service roles, and rapid digitalization position conversational AI and virtual agents as a strategic pillar of enterprise transformation agendas.

, By Deployment (Cloud, On-Premises), By Technology (NLP, Machine Learning, ASR, Text-to-Speech), By End User (BFSI, Healthcare, IT & Telecom, Retail & eCommerce, Education) Industry Outlook, Regional Analysis, Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Conversational AI & Virtual Agents market generates 16.2 billion in 2025 and is projected to reach USD 185.0 billion by 2034, reflecting a 33.8% CAGR over 2026-2034.

- Segment Dominance: The Solutions segment dominates with 80.3% revenue share, 2024, indicating strong preference for packaged platforms over services. This segment is set to maintain leadership with estimated: 78.0% share, 2034 as enterprises standardize on scalable AI stacks.

- Segment Dominance: On-premises deployments hold 64.7% of the market, 2024, underscoring demand for tighter control over data and integration. Within the technology stack, NLP capabilities contribute 35.8% share, 2024 as core engines for virtual agent performance.

- Driver: Automation of BFSI interactions, which account for over 27.9% of total spending, 2024, acts as a major adoption driver for conversational AI. Institutions target efficiency gains of estimated: 15.0% reduction in service costs, 2024 by shifting routine queries to virtual agents.

- Restraint: High upfront integration and compliance costs constrain adoption, with estimated: 20.0% of large enterprises, 2024 delaying full-scale rollouts. Data privacy and security concerns add friction, particularly in regulated sectors representing estimated: 35.0% of addressable demand, 2024.

- Opportunity: Vendors see substantial upside in cloud-native and SME-focused offerings, expected to represent estimated: 40.0% of new deployments, 2034. Cross-channel integration into contact centers, apps, and messaging platforms can unlock incremental revenue of estimated: 25.0 billion USD, 2034.

- Trend: A clear trend emerges toward hybrid and cloud deployment, with the on-premises share projected to fall from 64.7% in 2024 to estimated: 45.0% share, 2034. At the same time, enterprises shift from FAQ bots to task-oriented virtual agents that drive estimated: 60.0% of transaction volumes, 2034.

- Regional Analysis: North America leads with 42.7% share and 5.8 billion USD revenue, 2024, while the U.S. market reaches 4.67 billion USD, 2024 and is forecast to grow at 26.7% CAGR over 2024-2034. Asia-Pacific and Europe emerge as fast followers, together targeted to reach estimated: 55.0% combined share, 2034 as digital customer engagement accelerates.

By Type

The market continues to show strong preference for solution-based platforms in 2025. Software-led offerings accounted for more than 80 percent of total spending in 2024 and remain the primary choice for enterprises that need fast deployment and consistent performance. Organizations adopt prebuilt conversational AI platforms because they connect easily to existing IT systems and provide measurable improvements in service response times and workflow efficiency. This pattern remains consistent across retail, telecom, banking, and healthcare, where firms seek predictable outputs and lower integration risk.

Growth in this segment also reflects the maturity of natural language processing and machine learning tools. Vendors now provide refined conversational models that support multilingual communication and improved intent recognition. As you expand customer engagement programs in 2025, these solutions give you the ability to run automated support, inbound service, and sales assistance without heavy custom development. Their role grows as enterprises look for reliable automation that reduces operational spending and supports continuous availability.

Virtual agents play a growing part in 24-hour customer support structures. Companies in sectors with high inquiry volumes continue to rely on software-led deployments because they maintain steady performance and reduce staff dependence during peak periods. As conversational systems integrate more advanced speech and text capabilities, demand for packaged solutions is expected to increase through 2030.

By Application

Pavers, retaining walls, and similar application areas adopt conversational AI to improve planning, procurement, and maintenance workflows. Firms in construction and materials distribution use AI-driven systems to guide customers through selection, scheduling, and order tracking. This segment gains further traction as suppliers shift toward digital platforms in 2025, where automated agents handle routine requests for specifications, pricing, and installation support.

Pavers remain the largest application segment due to the frequent customer need for detailed guidance and the high volume of inquiries related to residential and commercial projects. Retaining wall applications grow steadily as builders use conversational tools to reduce delays in documentation, scheduling, and contractor coordination. Other applications expand as companies adopt virtual assistants for equipment rentals, product catalog navigation, and post-installation support.

Across all applications, virtual agents lower processing time and reduce pressure on service teams. Firms that deploy these tools report shorter service cycles and fewer manual errors, which strengthens adoption across expanding markets.

By End-Use

Residential building applications show accelerated adoption as homeowners seek faster responses for installation, repairs, and service scheduling. Virtual agents support real-time assistance and guide users through product selection and vendor coordination. Commercial buildings adopt these systems at a similar pace to manage maintenance requests, customer interactions, and building service operations. Enterprises with multi-location facilities find these tools valuable for consistent communication and centralized control.

Industrial buildings adopt conversational systems to address higher complexity in equipment management and safety protocols. Automated agents assist with support tickets, compliance queries, and inventory checks, reducing manual effort for on-site teams. As you implement AI programs within industrial settings, these tools provide structured workflows and consistent reliability.

The shift toward automated communication across these three segments strengthens overall market demand. As digital transformation gains pace in 2025, virtual agents become a primary interface for daily service interactions across residential, commercial, and industrial environments.

By Region

North America held more than 42 percent of global spending in 2024 and continues to set the pace for adoption in 2025. Strong investment from the banking, telecom, and retail sectors supports this lead. Enterprises in the United States and Canada maintain aggressive deployment pipelines driven by the need for customer-centric engagement and high service capacity. Robust AI research programs and strong vendor presence reinforce this regional advantage.

Europe follows with steady expansion as regulators encourage responsible AI deployment and companies integrate virtual agents into customer-facing operations. Sectors such as financial services, utilities, and government adopt these tools to improve response accuracy and reduce operational strain. Asia Pacific shows the highest growth rate due to broad digital adoption, multilingual environments, and rapid investment in AI-based communication systems. Countries such as China, India, and Japan prioritize automation within retail, banking, and public services.

Latin America and the Middle East & Africa progress steadily as infrastructure strengthens and enterprises shift toward digital service models. Rising mobile usage and expanding online service channels drive adoption across various industries. These regions are expected to gain additional momentum through 2030 as virtual agents become essential for cost-effective customer engagement.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Solutions

- Services

- Professional Services

- Training and Consulting

- System Integration and Implementation

- Support and Maintenance

- Managed Services

By Deployment

- On-Premises

- Cloud

By Technology

- Natural Language Processing (NLP)

- ML and Deep Learning

- Automatic Speech Recognition (ASR)

- Text to Speech

- Text-based

By End User

- BFSI

- Healthcare

- IT and Telecom

- Retail and eCommerce

- Education

- Media and Entertainment

- Automotive

- Others (Government, Hospitality, Manufacturing, etc.)

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 16.2 billion |

| Forecast Revenue (2034) | USD 185.0 billion |

| CAGR (2025-2034) | 33.8% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component(Solutions, Services), By Deployment (On-Premises, Cloud), By Technology (Natural Language Processing (NLP), ML and Deep Learning, Automatic Speech Recognition (ASR), Text to Speech, Text-based), By End User (BFSI, Healthcare, IT and Telecom, Retail and eCommerce, Education, Media and Entertainment, Automotive, Others (Government, Hospitality, Manufacturing, etc.)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Google, Oracle, Conversica, Inc., Amazon Web Services, Inc., Kasisto, Nuance Communications, Inc., Artificial Solutions, FIS, Solvvy, Cognigy, IBM, Pypestream Inc., Avaamo, SAP SE, Jio Haptik Technologies Limited, Rasa Technologies Inc., Microsoft, Salesforce, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premises), By Technology (NLP, Machine Learning, ASR, Text-to-Speech), By End User (BFSI, Healthcare, IT & Telecom, Retail & eCommerce, Education) Industry Outlook, Regional Analysis, Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

, By Deployment (Cloud, On-Premises), By Technology (NLP, Machine Learning, ASR, Text-to-Speech), By End User (BFSI, Healthcare, IT & Telecom, Retail & eCommerce, Education) Industry Outlook, Regional Analysis, Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

, By Deployment (Cloud, On-Premises), By Technology (NLP, Machine Learning, ASR, Text-to-Speech), By End User (BFSI, Healthcare, IT & Telecom, Retail & eCommerce, Education) Industry Outlook, Regional Analysis, Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Conversational AI and Virtual Agents Market?

Conversational AI and Virtual Agents Market

Who are the major players in the Conversational AI and Virtual Agents Market?

Google, Oracle, Conversica, Inc., Amazon Web Services, Inc., Kasisto, Nuance Communications, Inc., Artificial Solutions, FIS, Solvvy, Cognigy, IBM, Pypestream Inc., Avaamo, SAP SE, Jio Haptik Technologies Limited, Rasa Technologies Inc., Microsoft, Salesforce, Others

Which segments covered the Conversational AI and Virtual Agents Market?

By Component(Solutions, Services), By Deployment (On-Premises, Cloud), By Technology (Natural Language Processing (NLP), ML and Deep Learning, Automatic Speech Recognition (ASR), Text to Speech, Text-based), By End User (BFSI, Healthcare, IT and Telecom, Retail and eCommerce, Education, Media and Entertainment, Automotive, Others (Government, Hospitality, Manufacturing, etc.))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Conversational AI and Virtual Agents Market

Published Date : 30 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date