- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Creator Economy Platform Market Size, Share & Forecast | CAGR 22.4%

Global Creator Economy Platform Market Size, Share, Analysis By Platform Type (Distribution Platforms, Monetization Platforms, Community Engagement Platforms), By Content Format (Video, Written Content, Audio & Podcasting, Live Streaming, Gaming Content), By Monetization Model (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips & Affiliate Revenue), By Creator Tier (Individual Creators, Businesses & Brands, Media Companies) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 178.40 Billion | USD 1,100.00 Billion | 22.4% | North America, 37.5% |

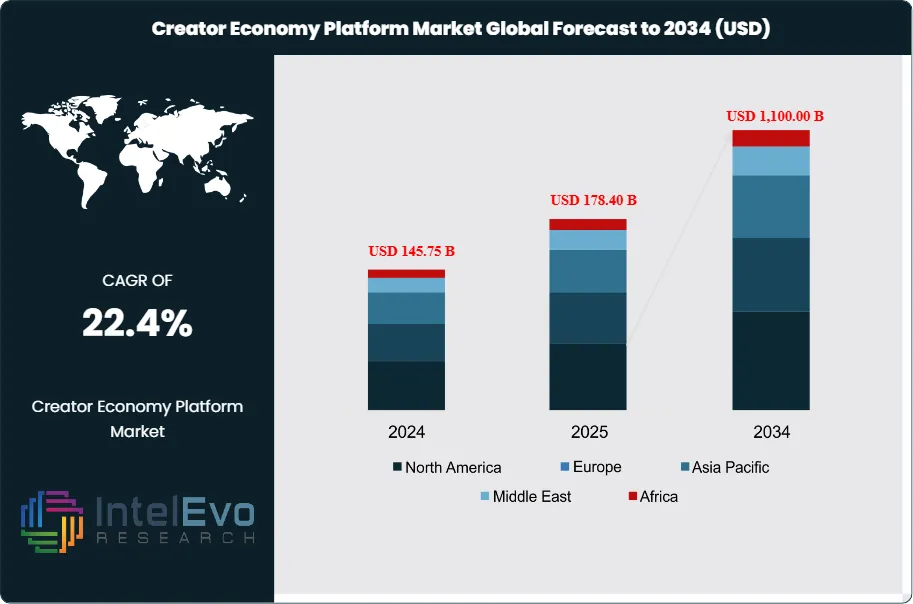

The Creator Economy Platform Market was valued at approximately USD 145.75 Billion in 2024 and reached USD 178.40 Billion in 2025. The market is projected to grow to USD 1,100.00 Billion by 2034, expanding at a CAGR of 22.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 921.60 Billion over the analysis period, making the creator economy platform market one of the fastest-expanding digital media categories tracked by the Interactive Advertising Bureau and government statistical agencies in the United States, the European Union, and India.

Get More Information about this report -

Request Free Sample ReportDemand acceleration is anchored in measurable creator spending by advertisers. The Interactive Advertising Bureau reported U.S. creator ad spend reached USD 37.1 billion in 2025, a 26% year-on-year rise and nearly four times the growth rate of overall digital advertising. Alphabet Inc. disclosed in its Q4 2025 earnings that YouTube advertising revenue exceeded USD 60 billion for the full year, up from USD 50 billion in 2024. YouTube has distributed more than USD 70 billion to creators, artists, and media partners across the three fiscal years ending 2024, the single-largest payout scale globally, redirecting advertiser budgets from legacy broadcast inventory to creator inventory.

Regulatory pressure is intensifying across all major jurisdictions. The European Commission opened formal Digital Services Act proceedings against TikTok in May 2025 over advertising transparency deficiencies under Article 39. The proposed Digital Fairness Act entered its consultation phase in October 2025. The U.S. Federal Trade Commission updated its Endorsement Guides under 16 CFR Part 255 in 2024 and extended disclosure obligations to AI-generated virtual influencers, tightening compliance cost for every platform that hosts sponsored creator content.

Technology and platform investment remains intense. Alphabet Inc., ByteDance Ltd., Meta Platforms, Inc., and Amazon.com, Inc. together operate the four largest distribution surfaces for creators. The TikTok USDS Joint Venture LLC closed on January 22, 2026, transferring operational control of TikTok U.S. to a consortium led by Oracle Corporation, Silver Lake, and MGX, with ByteDance retaining a 19.9% minority stake. Meta Platforms launched its Creator Monetization Suite in May 2025. Patreon, Inc. surpassed USD 3.5 billion in cumulative creator payouts, and Substack Inc. raised USD 100 million at a USD 1.1 billion valuation in July 2025.

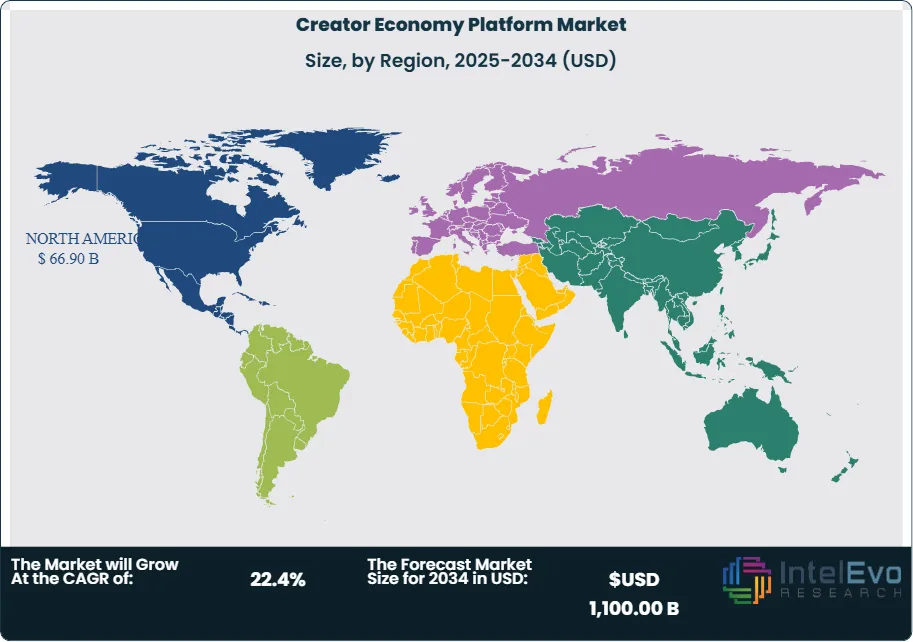

Regional trajectories diverge meaningfully. North America accounted for 37.5% of global revenue in 2025, anchored by the United States at approximately USD 61.20 Billion. Asia Pacific is the fastest-growing region, propelled by the Government of India's USD 1 billion creator-economy fund announced by the Ministry of Information and Broadcasting in March 2025 at WAVES 2025. Europe is advancing regulatory consolidation under the Digital Services Act and forthcoming Digital Fairness Act. The forecast through 2034 projects continued outperformance of creator-platform spend versus traditional media categories.

Market Definition & Scope

The creator economy platform market is defined as the collective set of digital platforms, software tools, and monetization infrastructure that enable independent creators, influencers, publishers, and media entities to produce, distribute, and monetize content directly to audiences. The market encompasses distribution platforms such as YouTube, TikTok, and Instagram; monetization platforms such as Patreon, Substack, and Kajabi; community engagement platforms such as Discord and Circle; and creator commerce infrastructure spanning tipping, subscriptions, digital products, and live-commerce tooling.

This analysis includes platform gross transaction revenue, creator payouts, advertising revenue attributable to creator inventory, subscription revenue, and creator commerce GMV. The analysis excludes consumer streaming services without creator monetization tooling (Netflix, Inc. and Disney+), traditional social-commerce GMV unrelated to creators, and enterprise marketing-automation software. The creator economy platform market sits within the parent Global Digital Media and Entertainment market, representing an estimated 8-10% share of that parent in 2025.

, By Content Format (Video, Written Content, Audio & Podcasting, Live Streaming, Gaming Content), By Monetization Model (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips & Affiliate Revenue), By Creator Tier (Individual Creators, Businesses & Brands, Media Companies) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global creator economy platform market grew from USD 178.40 Billion in 2025 and is projected to reach USD 1,100.00 Billion by 2034, registering a 22.4% CAGR across the forecast period.

- Segment Dominance (Platform Type): Distribution platforms led with 60.2% revenue share in 2025, driven by YouTube, TikTok, and Instagram aggregating over 4 billion monthly creator-content consumers.

- Segment Dominance (Content Format): Video formats captured 52.3% of platform revenue in 2025, with short-form video accounting for the fastest engagement growth on TikTok and Instagram Reels.

- Driver: Advertising migration to creator inventory drove USD 37.1 billion in U.S. creator ad spend in 2025, a 26% annual increase and four times the growth rate of overall digital advertising.

- Restraint: Platform dependency remains the largest constraint; algorithm changes reduced organic reach 50-80% overnight in historical episodes including Instagram's 2016 algorithmic feed shift and Facebook's 2018 publisher throttle.

- Opportunity: Independent monetization infrastructure represents a USD 210-240 Billion addressable opportunity through 2034, spanning memberships, newsletters, digital products, and creator commerce.

- Trend: Enterprise-grade AI tooling reached 40%+ adoption among professional creators in 2025, with Alphabet Inc. integrating Veo-powered video generation directly into YouTube Studio.

- Regional: North America captured 37.5% global share in 2025, equivalent to USD 66.90 Billion, led by the United States at approximately USD 61.20 Billion.

Key Insights Summary

- The creator economy platform market delivered USD 178.40 Billion in 2025 platform revenue, with YouTube alone reporting over USD 60 billion in full-year 2025 advertising revenue per Alphabet Inc.'s Q4 2025 earnings disclosure.

- U.S. creator ad spend reached USD 37.1 billion in 2025 according to the Interactive Advertising Bureau, up from USD 13.9 billion in 2021, and is projected to reach USD 43.9 billion in 2027.

- YouTube distributed over USD 70 billion to creators, artists, and media companies across the three fiscal years ending 2024, establishing the single largest creator-payout channel globally.

- TikTok's U.S. operations were transferred on January 22, 2026 to TikTok USDS Joint Venture LLC under Oracle Corporation, Silver Lake, and MGX, delivering 80.1% American ownership while ByteDance retained a 19.9% minority stake below the statutory 20% threshold.

- Patreon, Inc. crossed USD 3.5 billion in cumulative creator payouts by August 2025, serving over 250,000 active creators, and Substack Inc. closed a USD 100 million Series C in July 2025 at a USD 1.1 billion valuation led by BOND and The Chernin Group.

- The Government of India allocated a USD 1 billion fund for creators at WAVES 2025 in March 2025, alongside approximately USD 47 million for the Indian Institute of Creative Technology in Mumbai.

Competitive Landscape Overview

The creator economy platform market is moderately consolidated at the distribution layer and fragmented at the monetization layer. The four largest players by creator-adjacent revenue, namely Alphabet Inc., ByteDance Ltd., Meta Platforms, Inc., and Amazon.com, Inc., together capture an estimated 58-63% of global creator-platform revenue in 2025. Competition at the distribution layer is driven by algorithmic recommendation performance, creator monetization depth, and advertiser integration. Competition at the monetization layer, spanning Patreon, Inc., Substack Inc., Kajabi, Inc., and Discord, Inc., is driven by take-rate economics, community tooling, and cross-platform portability. Industry transaction data points to 81 disclosed M&A transactions completed in 2025, a 17.4% increase over 2024. Strategic repositioning is intensifying as creators increasingly demand ownership of audience data and diversified revenue beyond any single platform.

Competitive Landscape Matrix

| Company | Headquarters | Market Position | Key Offering | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Alphabet Inc. (YouTube) | Mountain View, US | Leader | YouTube Partner Program, Shorts, Memberships | Global | Unified Creator Partnerships platform rolled out across 7 markets in Q1 2026 |

| ByteDance Ltd. / TikTok USDS JV LLC | Beijing / Los Angeles | Leader | TikTok short-form video, Creator Rewards, Shop | APAC, North America | US operations transferred to Oracle-Silver Lake-MGX joint venture on January 22, 2026 |

| Meta Platforms, Inc. | Menlo Park, US | Leader | Instagram, Facebook, Threads, Reels monetization | Global | Creator Monetization Suite launched across Instagram and Facebook in May 2025 |

| Amazon.com, Inc. (Twitch) | Seattle, US | Leader | Twitch livestreaming, subscriptions, bits | North America, Europe | Twitch expanded Partner Plus eligibility tiers in Q4 2025 |

| Patreon, Inc. | San Francisco, US | Challenger | Membership tiers, paid chats, live video | North America, Europe | Surpassed USD 3.5 billion lifetime creator payouts by August 2025 |

| Substack Inc. | San Francisco, US | Challenger | Paid newsletters, podcasts, Notes, Substack app | North America, Europe | Closed USD 100 million Series C at USD 1.1 billion valuation in July 2025 |

| Spotify AB | Stockholm, Sweden | Challenger | Podcasts, Spotify for Creators, audio advertising | Global | Expanded Partner Program monetization for video podcasts through 2025 |

| Snap Inc. | Santa Monica, US | Niche Player | Spotlight, Stories monetization, AR Lens Studio | North America | Revenue-share enhancements to Spotlight announced late 2025 |

| Kajabi, Inc. | Irvine, US | Niche Player | Course, membership, and digital-product commerce | North America | Crossed USD 10 billion in cumulative creator sales in August 2025 |

| Discord, Inc. | San Francisco, US | Niche Player | Creator communities, Server Subscriptions | Global | Filed confidentially for IPO in January 2026 |

Segmentation Analysis

Segmentation analysis of the global creator economy platform market reveals four primary axes: by platform type, by content format, by monetization model, and by creator tier. Distribution platforms dominated with 60.2% share in 2025, while subscription-based monetization is the fastest-growing revenue channel across the forecast period.

By Platform Type

Distribution platforms held 60.2% of global creator economy platform revenue in 2025, equivalent to approximately USD 107.40 Billion, anchored by YouTube, TikTok, Instagram, and Facebook. These platforms combine algorithmic reach, advertising inventory, and native monetization products such as YouTube Partner Program, TikTok Creator Rewards, and Instagram Reels bonuses. Alphabet Inc. disclosed YouTube advertising revenue above USD 60 billion in 2025, a 20% year-on-year increase. Distribution platforms grow more slowly than monetization platforms but retain structural dominance because advertiser budgets and creator audience discovery still concentrate here. Meta Platforms, Inc. launched a unified Creator Monetization Suite in May 2025 consolidating in-stream advertising, Reels bonuses, and brand-collaboration tooling across Instagram and Facebook.

Monetization platforms captured 18.7% of revenue in 2025, approximately USD 33.40 Billion, and are projected to grow at 28-32% CAGR through 2034. Patreon, Inc., Substack Inc., Kajabi, Inc., Gumroad Inc., and Buy Me a Coffee form the core cluster. Patreon crossed USD 3.5 billion cumulative creator payouts and Kajabi crossed USD 10 billion cumulative creator sales in August 2025. Substack closed a USD 100 million Series C at a USD 1.1 billion valuation in July 2025. Community engagement platforms, led by Discord, Inc., Circle, and Mighty Networks, contributed 12.4% share, with Discord, Inc. filing confidentially for its IPO in January 2026.

By Content Format

Video dominated the creator economy platform market with 52.3% revenue share in 2025, worth approximately USD 93.30 Billion, led by YouTube, TikTok, Instagram Reels, and Twitch. Short-form video grew fastest, with TikTok's viral discovery engine and Instagram Reels together accounting for the bulk of incremental creator-minutes in 2025. YouTube reported over 88 billion monthly watch-time minutes across its top-tier creator portfolios, with 71% occurring on connected television devices. Spotter and Comscore announced a creator-content measurement partnership in January 2026, addressing long-standing advertiser demand for broadcast-calibre audience verification on YouTube creator inventory.

Written content, including newsletters and blogs, held 14.8% share (approximately USD 26.40 Billion) and is led by Substack Inc., Medium, Ghost Foundation, and Beehiiv. Audio and podcasting captured 12.6% share, with Spotify AB, Apple Inc., and YouTube investing heavily in podcast monetization; global podcast ad spending reached approximately USD 4.46 billion in 2025 per industry association tracking. Live-streaming commanded 10.4% share, led by Twitch (Amazon.com, Inc.), YouTube Live, and TikTok Live, while gaming-specific content held 7.1%. Written and audio segments deliver higher per-user revenue than video despite smaller aggregate audiences, because subscription economics dominate these formats.

By Monetization Model

Advertising remained the largest monetization channel in 2025 at 41.2% of global platform revenue, equivalent to approximately USD 73.50 Billion. The Interactive Advertising Bureau reported U.S. creator ad spend reached USD 37.1 billion in 2025, a 26% year-on-year increase, with paid amplification of creator content projected to grow 56% to USD 11.1 billion in 2026. Subscriptions and memberships captured 22.5% share (USD 40.10 Billion) and are the fastest-growing channel, projected at 30-35% CAGR through 2034 as creators prioritize recurring revenue over algorithm-dependent advertising payouts.

Brand partnerships held 18.4% share (USD 32.80 Billion) as advertisers shifted budgets to creator-led sponsored content. Merchandise and creator commerce captured 10.7% share, led by Shopify Inc., Fourthwall, and YouTube Shopping, while tips, donations, and affiliate commissions comprised 7.2%. Subscription-platform economics favor creators and platforms simultaneously: Patreon charges 5-12% of creator earnings and Substack takes a 10% flat cut, compared to the 30-55% revenue share typical on advertising-led distribution surfaces.

By Creator Tier

Individual content creators commanded 58.7% of creator economy platform revenue in 2025, equivalent to approximately USD 104.70 Billion, reflecting the proliferation of independent creators across YouTube, TikTok, Instagram, Twitch, and Patreon. More than 207 million people globally identified as content creators in 2025, with Brazil leading at approximately 105 million and the United States at approximately 86.5 million. Professional creators, defined as those earning full-time income, numbered around 4 million globally. Over 50% of creators earn less than USD 15,000 annually while fewer than 5% exceed USD 100,000.

Businesses and brands held 26.9% share, driven by enterprise creator-marketing spend, in-house influencer teams, and brand-owned creator studios. Media companies held 14.2% share, reflecting the migration of legacy publishers onto creator platforms. Paramount Skydance's acquisition of The Free Press for USD 150 million in October 2025 and the appointment of Bari Weiss as editor-in-chief of CBS News signaled the collapse between the creator economy and legacy media. Platforms now cater to all three tiers with tiered monetization products and enterprise dashboards.

Regional Analysis

Regional analysis of the global creator economy platform market shows North America at 37.5% share in 2025, Asia Pacific at 28.4%, Europe at 22.8%, Latin America at 6.8%, and Middle East & Africa at 4.5%. Asia Pacific is the fastest-growing region through 2034.

North America:

North America held 37.5% of global creator economy platform market revenue in 2025, worth approximately USD 66.90 Billion. The United States led the region at approximately USD 61.20 Billion, followed by Canada at USD 4.20 Billion and Mexico at USD 1.50 Billion. The Interactive Advertising Bureau reported U.S. creator ad spend at USD 37.1 billion in 2025. YouTube Creator Partnerships, launched in seven markets in Q1 2026, extends brand-collaboration tooling globally. The Federal Trade Commission's 2024 Endorsement Guides update, now covering AI-generated virtual influencers, raised compliance cost across the region. New York State passed synthetic-media advertising disclosure legislation taking effect mid-2026.

Europe:

Europe contributed 22.8% of global creator economy platform revenue in 2025, equivalent to approximately USD 40.70 Billion. The United Kingdom, Germany, and France together accounted for nearly 40% of the region's social media advertising spend. The European Commission opened formal Digital Services Act proceedings against TikTok in May 2025 over advertising transparency gaps, and reached a preliminary view in October 2025 that Meta Platforms failed to provide users with simple mechanisms to report illegal content. The EU AI Act reaches a major transparency milestone on August 2, 2026, when AI-generated content disclosure obligations become enforceable. The proposed Digital Fairness Act is expected to reshape influencer disclosure harmonization across the 27 EU member states.

Asia Pacific:

Asia Pacific captured 28.4% of global creator economy platform revenue in 2025, valued at approximately USD 50.70 Billion, and is the fastest-growing region at projected CAGR above 30% through 2034. China led by platform revenue through Douyin (ByteDance Ltd.), Bilibili, and Kuaishou. India followed with approximately 2 to 2.5 million active creators influencing over USD 350 billion in annual consumer spending per Ministry of Information and Broadcasting data released at WAVES 2025 in May 2025. Japan and South Korea combined for approximately 18% of the regional total, supported by strong livestreaming and gaming content economies. YouTube disclosed USD 1.8 billion contribution to India's GDP in 2024 and committed USD 100 million across fiscal 2025 and 2026.

Latin America:

Latin America held 6.8% of global creator economy platform revenue in 2025, approximately USD 12.10 Billion, led by Brazil with roughly 105 million self-identified content creators, the largest creator population globally in absolute terms. Mexico and Colombia followed as growth engines for short-form video and live commerce. TikTok, YouTube, and Instagram dominate the region's distribution layer, while local monetization infrastructure remains underdeveloped. Brazil's e-commerce integration with creator platforms accelerated in 2025 through Mercado Libre and Shopify partnerships. Brazil's consumer-protection authority Senacon intensified enforcement on undisclosed sponsored content through late 2025.

Middle East & Africa:

Middle East & Africa contributed 4.5% of global creator economy platform revenue in 2025, approximately USD 8.00 Billion, anchored by the United Arab Emirates, Saudi Arabia, and South Africa. MGX, the Abu Dhabi-based technology investment firm, took a 15% stake in TikTok USDS Joint Venture LLC in January 2026, the region's largest single creator-economy infrastructure investment. Saudi Arabia's General Entertainment Authority expanded creator-focused funding through 2025 as part of Vision 2030. South Africa leads sub-Saharan Africa in creator monetization via YouTube Partner Program, while Nigeria emerged as a meaningful creator base with strong Afrobeats and short-form video output.

Country Analysis

United States:

The United States creator economy platform market was valued at approximately USD 61.20 Billion in 2025 and is projected to grow at a CAGR of 19.3% through 2034. The Interactive Advertising Bureau reported U.S. creator ad spend at USD 37.1 billion in 2025, a 26% year-on-year increase. YouTube alone paid approximately USD 20 billion to U.S. creators in 2025. The Federal Trade Commission's updated Endorsement Guides under 16 CFR Part 255 extended disclosure obligations to AI-generated virtual influencers and tightened brand co-liability. New York State's synthetic-media advertising disclosure law is fully enacted with a fixed mid-2026 enforcement date. The Influencer Marketing Factory's January 2026 survey of 1,000 U.S. creators found 45.6% now earn between USD 10,000 and USD 100,000 annually, evidencing the emergence of a creator middle class.

India:

India's creator economy platform market was valued at approximately USD 12.50 Billion in 2025 and is projected to grow at 28-30% CAGR through 2034, the fastest among large economies. The Ministry of Information and Broadcasting announced a USD 1 billion creator-economy fund in March 2025 at WAVES 2025, alongside a Rs. 391 crore (approximately USD 47 million) allocation for the Indian Institute of Creative Technology in Mumbai. YouTube contributed USD 1.8 billion to India's GDP and supported 930,000 jobs in its creative ecosystem in 2024. Between 2 million and 2.5 million active creators influenced over USD 350 billion in annual consumer spending in 2025, with direct creator revenues of USD 20-25 billion projected to reach USD 100-125 billion by 2030 per Ministry of Information and Broadcasting data released at WAVES 2025. India's Digital Personal Data Protection Act enters additional enforcement phases through 2026.

United Kingdom:

The United Kingdom creator economy platform market was valued at approximately USD 9.80 Billion in 2025 and is projected to grow at 21-23% CAGR through 2034. The UK accounts for roughly 6.6% of global Patreon traffic, the second-highest nationally after the United States. The Advertising Standards Authority enforces mandatory "Ad" or "Advert" labelling at the start of sponsored posts. Ofcom's age-assurance rules under the Online Safety Act continued scaling through 2025 and 2026, affecting age-restricted content monetization on OnlyFans, Twitch, and similar platforms. The UK's restrictions on online advertising for certain food categories take effect with fixed 2026 implementation dates, materially affecting creator collaborations in the food-and-beverage vertical.

Germany:

Germany's creator economy platform market was valued at approximately USD 8.90 Billion in 2025 and is projected to grow at 20-22% CAGR through 2034. Germany accounts for approximately 4.9% of global Patreon traffic, the third-largest creator consumer market globally. The Federal Cartel Office, Bundeskartellamt, continues to scrutinize large platforms under the Digital Markets Act. The Medienanstalten state media authorities enforce a stricter disclosure regime than most European jurisdictions, applying fines up to EUR 500,000 for undisclosed commercial content. German creators cluster disproportionately in education, automotive, and gaming content, with Spotify AB's podcast monetization showing strong traction among German-language publishers through 2025.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Platform Type

- Distribution Platforms

- Monetization Platforms

- Community Engagement Platforms

By Content Format

- Video

- Written Content (Newsletters & Blogs)

- Audio & Podcasting

- Live-Streaming

- Gaming Content

By Monetization Model

- Advertising

- Subscriptions & Memberships

- Brand Partnerships

- Merchandise & Creator Commerce

- Tips, Donations & Affiliate Commissions

By Creator Tier

- Individual Content Creators

- Businesses & Brands

- Media Companies

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 178.40 B |

| Forecast Revenue (2034) | USD 1,100.00 B |

| CAGR (2025-2034) | 22.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Platform Type, (Distribution Platforms, Monetization Platforms, Community Engagement Platforms), By Content Format, (Video, Written Content (Newsletters & Blogs), Audio & Podcasting, Live-Streaming, Gaming Content), By Monetization Model, (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips, Donations & Affiliate Commissions), By Creator Tier, (Individual Content Creators, Businesses & Brands, Media Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ALPHABET INC. (YOUTUBE), BYTEDANCE LTD. / TIKTOK USDS JOINT VENTURE LLC, META PLATFORMS, INC., AMAZON.COM, INC. (TWITCH), PATREON, INC., SUBSTACK INC., SPOTIFY AB, SNAP INC., PINTEREST, INC., DISCORD, INC., KAJABI, INC., GUMROAD, INC., SHOPIFY INC., LINKTREE PTY LTD., OF GROUP LTD. (ONLYFANS), CAMEO (BARON APP, INC.), BUY ME A COFFEE, TEACHABLE, INC., VIMEO.COM, INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Content Format (Video, Written Content, Audio & Podcasting, Live Streaming, Gaming Content), By Monetization Model (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips & Affiliate Revenue), By Creator Tier (Individual Creators, Businesses & Brands, Media Companies) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Content Format (Video, Written Content, Audio & Podcasting, Live Streaming, Gaming Content), By Monetization Model (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips & Affiliate Revenue), By Creator Tier (Individual Creators, Businesses & Brands, Media Companies) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

, By Content Format (Video, Written Content, Audio & Podcasting, Live Streaming, Gaming Content), By Monetization Model (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips & Affiliate Revenue), By Creator Tier (Individual Creators, Businesses & Brands, Media Companies) Industry Region & Key Players, Market Dynamics, Competitive Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Creator Economy Platform Market?

The Global Creator Economy Platform Market was valued at USD 145.75 Billion in 2024 and is projected to reach USD 1,100.00 Billion by 2034, growing at a CAGR of 22.4% from 2026 to 2034. Growth is driven by increasing creator monetization opportunities, influencer marketing adoption, social commerce expansion, subscription-based revenue models, AI-powered content creation tools, live streaming platforms, digital communities, and growing investments in the global creator economy ecosystem.

Who are the major players in the Creator Economy Platform Market?

ALPHABET INC. (YOUTUBE), BYTEDANCE LTD. / TIKTOK USDS JOINT VENTURE LLC, META PLATFORMS, INC., AMAZON.COM, INC. (TWITCH), PATREON, INC., SUBSTACK INC., SPOTIFY AB, SNAP INC., PINTEREST, INC., DISCORD, INC., KAJABI, INC., GUMROAD, INC., SHOPIFY INC., LINKTREE PTY LTD., OF GROUP LTD. (ONLYFANS), CAMEO (BARON APP, INC.), BUY ME A COFFEE, TEACHABLE, INC., VIMEO.COM, INC., Others

Which segments covered the Creator Economy Platform Market?

By Platform Type, (Distribution Platforms, Monetization Platforms, Community Engagement Platforms), By Content Format, (Video, Written Content (Newsletters & Blogs), Audio & Podcasting, Live-Streaming, Gaming Content), By Monetization Model, (Advertising, Subscriptions & Memberships, Brand Partnerships, Merchandise & Creator Commerce, Tips, Donations & Affiliate Commissions), By Creator Tier, (Individual Content Creators, Businesses & Brands, Media Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Creator Economy Platform Market

Published Date : 01 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date