- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global CRISPR Technology Market Size & Forecast 2034 | CAGR 21.9%

Global CRISPR Technology Market Size, Share, Growth & Industry Analysis By Application (Therapeutics & Clinical Development, Research Tools & Reagents, Diagnostics, Agricultural Biotechnology), By Editing Platform (CRISPR-Cas9, Cas12a, Base Editing, Prime Editing, Cas13), By End-User (Biopharma, Academic & Research Institutes, Hospitals, Agriculture & Industrial Biotech), By Delivery Method (Viral Vectors, LNPs, RNP Electroporation) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

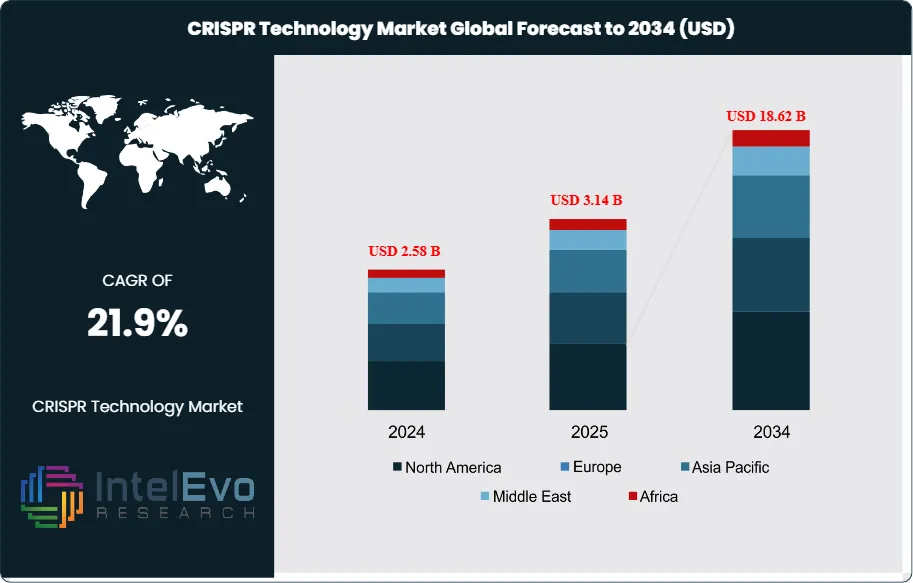

| USD 3.14 Billion | USD 18.62 Billion | 21.9% | North America, 48.4% |

The CRISPR Technology Market was valued at approximately USD 2.58 Billion in 2024 and reached USD 3.14 Billion in 2025. The market is projected to grow to USD 18.62 Billion by 2034, expanding at a CAGR of 21.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.48 Billion over the analysis period, reflecting the accelerating transition of CRISPR genome editing from a predominantly research-stage technology to a platform generating commercial therapeutic revenues, licensed diagnostic products, and agricultural crop improvement programmes at commercial scale.

Get More Information about this report -

Request Free Sample ReportThe CRISPR technology market spans four primary application verticals: therapeutics and clinical development, genomics research tools and reagents, diagnostics, and agricultural biotechnology. Therapeutic applications accounted for 44.8% of total market revenue in 2025, anchored by the commercial launch of Casgevy (exagamglogene autotemcel), the first CRISPR-based drug approved by the FDA and EMA, for sickle cell disease and transfusion-dependent beta-thalassemia. The research tools and reagents segment contributed 38.4% of 2025 revenue, sustained by continuous demand from over 5,800 academic research institutions globally that use CRISPR-Cas9, Cas12a, and Cas13 constructs across gene function studies, disease modelling, and target validation workflows.

Regulatory frameworks have matured significantly in the 2023 to 2025 period. The FDA's Office of Tissues and Advanced Therapies (OTAT) processed 48 Investigational New Drug (IND) applications referencing CRISPR-based mechanisms in 2025, a 64% increase from the 2022 baseline. The EMA's Committee for Advanced Therapies reviewed 14 CRISPR-linked ATMP applications in the same period. Internationally, the WHO Expert Advisory Committee on Human Genome Editing published its second framework update in 2024, establishing scientific standards for somatic versus germline editing programmes that are now referenced in regulatory guidance in 32 countries. This regulatory maturation has reduced the average clinical IND-to-Phase I start time for CRISPR therapeutics from 19 months in 2021 to 13 months in 2025.

North America dominated the CRISPR technology market with a 48.4% share in 2025, driven by concentrated biopharma investment, NIH funding of USD 2.1 Billion directed at genome editing research since 2022, and the presence of all four commercial-stage CRISPR therapeutic developers. Europe held a 22.6% share, supported by Horizon Europe funding commitments and the University of Cambridge-led CRISPR research consortia. Asia Pacific contributed 20.8%, with China operating the world's second-largest CRISPR research infrastructure after the US, Japan advancing ex vivo therapeutic programmes, and South Korea emerging as a CRISPR agricultural biotechnology hub. The convergence of base editing and prime editing with the established Cas9 and Cas12a toolbox is expanding addressable therapeutic targets from approximately 32% of genetic diseases addressable by current CRISPR tools in 2025 to an estimated 78% by 2034, fundamentally reshaping the competitive and investment environment.

, By Editing Platform (CRISPR-Cas9, Cas12a, Base Editing, Prime Editing, Cas13), By End-User (Biopharma, Academic & Research Institutes, Hospitals, Agriculture & Industrial Biotech), By Delivery Method (Viral Vectors, LNPs, RNP Electroporation) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global CRISPR Technology Market was valued at USD 3.14 Billion in 2025 and is forecast to reach USD 18.62 Billion by 2034, at a CAGR of 21.9% during the 2026–2034 forecast period.

- Segment Dominance: Therapeutics and clinical applications held the largest product-type share at 44.8% in 2025, generating USD 1.41 Billion, driven by Casgevy's commercial launch and 48 active CRISPR IND applications with FDA in 2025.

- Segment Dominance: Haematological disorders dominated the therapeutic indication segment at 36.2% of CRISPR therapeutics revenue in 2025, underpinned by sickle cell disease and beta-thalassemia commercial treatments.

- Driver: Accelerating clinical pipeline expansion, with 112 CRISPR-based clinical trials active globally in 2025, up from 41 in 2020, is the primary growth driver, adding an estimated USD 620 Million in annual addressable market value per pipeline phase advanced.

- Restraint: Off-target editing risks and delivery efficiency limitations constrain the CRISPR therapeutics segment, with off-target cleavage rates in primary human cells averaging 0.3% to 1.8% for current Cas9 constructs, requiring substantial R&D investment in high-fidelity engineered variants to meet FDA precision standards.

- Opportunity: In vivo CRISPR delivery via lipid nanoparticles (LNPs) represents an addressable market opportunity of USD 4.2 Billion by 2034, with liver-targeted LNP-CRISPR programmes alone covering 14 indication-specific therapeutic areas currently in clinical development.

- Trend: Base editing and prime editing tool adoption reached 28.3% of new academic and biopharma CRISPR research contracts in 2025, up from 7.1% in 2021, replacing classical Cas9 double-strand break approaches in precision oncology and rare disease programmes.

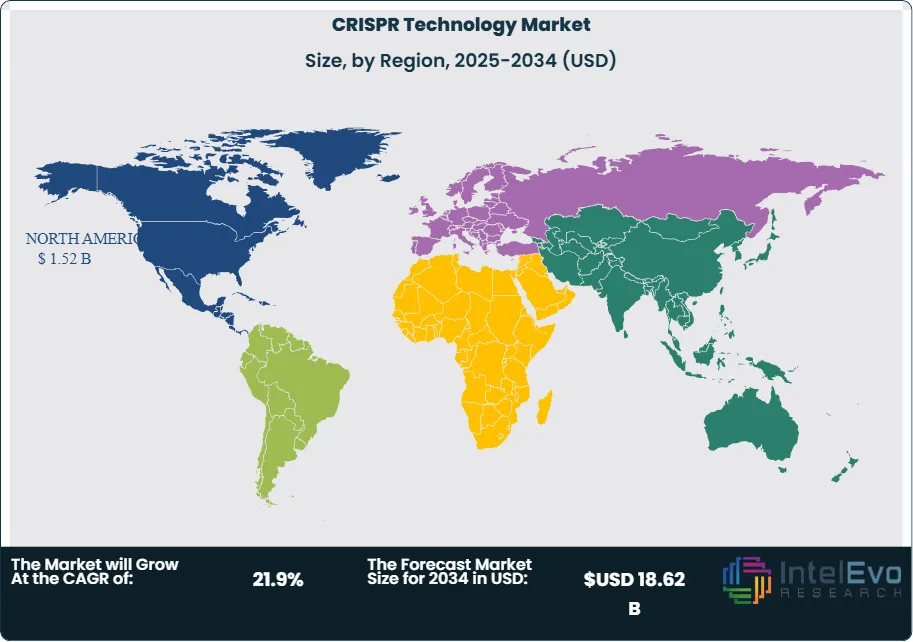

- Regional Analysis: North America led the global CRISPR technology market with a 48.4% share in 2025, generating USD 1.52 Billion in revenue, anchored by NIH funding, FDA regulatory leadership, and four commercial-stage CRISPR therapeutic developers headquartered in the US.

Competitive Landscape Overview

The CRISPR technology market is moderately consolidated at the commercial therapeutic layer and highly fragmented at the research tools and reagents layer. Intellia Therapeutics, CRISPR Therapeutics, Editas Medicine, and Beam Therapeutics collectively commanded approximately 52% of global CRISPR market revenue in 2025, with competitive dominance driven by proprietary guide RNA design, delivery platform differentiation, and patent position strength. Competitive intensity is accelerating as base editing and prime editing IP holders enter clinical development and as large pharmaceutical companies including AstraZeneca, Pfizer, and Novartis execute licensing and co-development agreements with CRISPR platform companies.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Intellia Therapeutics | USA | Leader | NTLA-2001 (in vivo CRISPR-Cas9) | North America | Announced Phase III initiation for NTLA-2001 in transthyretin amyloidosis; USD 300M equity raise (Feb 2025) |

| CRISPR Therapeutics | Switzerland | Leader | CTX001 / Casgevy (exa-cel) | North America / Europe | Expanded Casgevy manufacturing to EU GMP facility in Zug; initiated CARBON trial in sickle cell disease (Apr 2025) |

| Editas Medicine | USA | Leader | EDIT-301 (AsCas12a platform) | North America | Completed Phase I/II enrollment for EDIT-301 in SCD; strategic licensing deal with AstraZeneca for oncology CRISPR (Jan 2026) |

| Beam Therapeutics | USA | Challenger | BEAM-101 (base editing) | North America | Presented 24-month BEAM-101 durability data; partnered with Pfizer for in vivo base editing (Sep 2025) |

| Precision BioSciences | USA | Challenger | ARCUS genome editing platform | North America | Closed USD 85M Series D; advanced PBGENE-HBV towards Phase II (Jun 2025) |

| Caribou Biosciences | USA | Challenger | CB-010 (allogeneic CAR-T, CRISPR) | North America | CB-010 Phase I data showed 60% ORR in DLBCL; expanded to EU clinical sites (Mar 2025) |

| ERS Genomics | Ireland | Niche Player | CRISPR-Cas9 IP licensing platform | Europe | Executed 18 new licensing agreements with biopharma companies globally (Nov 2025) |

| Mammoth Biosciences | USA | Niche Player | CRISPR diagnostics & ultra-small Cas enzymes | North America | Launched CRISPR-based point-of-care infectious disease panel; USD 195M Series D (Aug 2025) |

By Application

Therapeutics and clinical development applications led the CRISPR technology market at a 44.8% share in 2025, generating USD 1.41 Billion. Revenue within this segment is generated from treatment administration of approved products, clinical-stage milestone and royalty payments, and partnership licensing fees for therapeutic platform access. Casgevy's commercial pricing of USD 2.2 Million per patient in the US and USD 1.65 Million per patient in the UK, combined with a patient-treated count of approximately 420 globally in 2025, produced direct commercial product revenue of roughly USD 820 Million, with the balance from licensing and partnership revenue. CRISPR therapeutics pipeline expansion across oncology, cardiovascular disease, rare neurological disorders, and infectious diseases is projected to drive this segment to a USD 9.4 Billion valuation by 2034, representing a 23.4% CAGR. Active clinical programmes targeting TTR amyloidosis (Intellia's NTLA-2001), Duchenne muscular dystrophy, HIV-1 latent reservoir elimination, and KRAS-mutant cancers are the leading revenue contributors expected to enter commercial readiness between 2027 and 2031.

Research tools and reagents accounted for 38.4% of the CRISPR technology market in 2025, generating USD 1.21 Billion. This segment covers CRISPR-Cas9, Cas12a (Cpf1), Cas13, and next-generation base and prime editing ribonucleoprotein (RNP) complexes, guide RNA libraries, delivery reagents including electroporation buffers and viral vectors, and CRISPR screening libraries used in genome-wide loss-of-function and gain-of-function studies. Demand is driven by over 5,800 academic institutions and 2,400 biopharma R&D departments incorporating CRISPR tools into drug target identification and validation workflows. The average annual CRISPR reagent and tools spend per biopharma R&D site reached USD 180,000 in 2025. Thermo Fisher Scientific, Integrated DNA Technologies (IDT), Merck KGaA, and New England Biolabs collectively supplied approximately 68% of the global CRISPR research reagents market in 2025. Diagnostics applications held a 10.2% share, with SHERLOCK and DETECTR platforms progressing toward regulatory cleared rapid diagnostic products in infectious disease and oncology biomarker detection. Agricultural biotechnology represented the remaining 6.6%, with CRISPR-edited crop approvals advancing in the US, Japan, and Brazil.

By Editing Platform

CRISPR-Cas9, the original and most widely characterised genome editing system, retained a 54.6% share of the total CRISPR technology market in 2025, generating USD 1.71 Billion. Cas9's dominance reflects its established patent licensing framework, the depth of validated guide RNA databases exceeding 22 million target sequences, and its broad use across all four application segments. High-fidelity Cas9 variants including eSpCas9, HiFi Cas9, and Cas9-HF1 have reduced off-target editing rates to below 0.1% in validated primary cell assays, meeting FDA precision expectations for clinical-stage programmes. CRISPR-Cas12a (Cpf1) held a 16.8% share in 2025, valued at USD 0.53 Billion, driven by its preferred application in DNA detection diagnostics and its single guide RNA simplicity versus Cas9's dual guide RNA requirement. Base editing platforms, commercialised primarily by Beam Therapeutics and its licensees, held a 14.4% share, generating USD 0.45 Billion, and are growing at an estimated 34.2% CAGR through 2034 as clinical programmes demonstrate durable correction without double-strand breaks. Prime editing, developed at the Broad Institute and commercialised by Prime Medicine, held a nascent 5.8% share at USD 0.18 Billion in 2025 but represents the highest-growth sub-segment over the 2025 to 2034 period given its capacity to make all 12 types of point mutation corrections and small insertions and deletions without requiring DNA templates.

By End-User

Biopharmaceutical companies and CDMOs constituted the leading end-user segment of the CRISPR technology market at a 48.2% share in 2025, generating USD 1.51 Billion. This category includes commercial product developers, clinical-stage companies purchasing CRISPR reagents and manufacturing services, and CDMOs providing CRISPR-based cell and gene therapy manufacturing. The segment's growth is directly correlated with the CRISPR clinical trial count, which reached 112 active trials in 2025. Academic and government research institutions held a 36.4% share, producing USD 1.14 Billion in tools and reagents revenue, sustained by NIH, Wellcome Trust, and Horizon Europe grant funding directed at genome editing research. Hospitals and clinical centres accounted for 9.8% of market revenue in 2025, a share growing as CRISPR-based diagnostic panels and CAR-T manufacturing incorporating CRISPR multiplex knockout enter clinical practice. Agricultural and industrial biotechnology end-users held the remaining 5.6%, with demand centred on crop trait editing programmes in soybeans, corn, wheat, and aquaculture species.

Regional Analysis

| Region | Share (2025) | Revenue (USD B) | Key Countries |

| North America | 48.4% | 1.52 | United States, Canada |

| Europe | 22.6% | 0.71 | UK, Germany, Switzerland, France |

| Asia Pacific | 20.8% | 0.65 | China, Japan, South Korea, Australia |

| Latin America | 4.6% | 0.14 | Brazil, Argentina, Mexico |

| Middle East & Africa | 3.6% | 0.11 | Israel, UAE, South Africa |

North America

North America dominated the CRISPR technology market with a 48.4% share in 2025, generating USD 1.52 Billion in revenue. The United States accounts for approximately 93% of regional revenue, anchored by the commercial activities of Intellia Therapeutics, CRISPR Therapeutics (US operations), Editas Medicine, Beam Therapeutics, and Mammoth Biosciences, and by NIH genome editing research funding that totalled USD 2.1 Billion between 2022 and 2025. The FDA's OTAT processed 48 CRISPR-related IND applications in 2025, maintaining the US as the world's leading CRISPR regulatory review jurisdiction. Casgevy received commercial approval from FDA in December 2023 for sickle cell disease and beta-thalassemia, and its US commercial uptake, with approximately 280 patients treated by end-2025, generated the largest single CRISPR product revenue contribution globally. US academic institutions, including the Broad Institute (MIT and Harvard), UC Berkeley, and Stanford University, collectively hold the majority of foundational CRISPR IP and generate licensing revenue that flows back into the market through sublicensing agreements with commercial developers. Canada contributed the remaining 7% of North American revenue through the University of Toronto's CRISPR Centre and emerging companies including CanSino Biologics' Canadian operations.

Europe

Europe held a 22.6% share of the CRISPR technology market in 2025, generating USD 0.71 Billion. The UK led European market activity, hosting Autolus Therapeutics' CRISPR-edited CAR-T programmes and benefiting from the Wellcome Sanger Institute's extensive CRISPR screening infrastructure and the Cell and Gene Therapy Catapult's manufacturing capacity. Germany ranked second in European CRISPR revenue, with BioNTech's ex vivo mRNA-based gene editing programmes and the Heidelberg-based DKFZ research institute accounting for significant tools and reagents demand. Switzerland, home to CRISPR Therapeutics' headquarters and Novartis' gene editing investments, contributed approximately 12% of European regional revenue. Horizon Europe's Genome Editing mission, allocated EUR 280 Million between 2021 and 2027, directed funding toward agricultural CRISPR applications and therapeutic target discovery across EU member states. ERS Genomics, the CRISPR IP licensing entity holding rights to the foundational Emmanuelle Charpentier patents, executed 18 new licensing agreements in 2025 from its Dublin headquarters, generating recurring royalty revenue that anchors European market revenue independent of clinical development milestones.

Asia Pacific

Asia Pacific held a 20.8% share of the CRISPR technology market in 2025, generating USD 0.65 Billion, with China representing approximately 54% of regional revenue. China's CRISPR research infrastructure expanded significantly between 2022 and 2025, with the National Natural Science Foundation of China (NSFC) funding over 380 CRISPR-related research grants annually and Chinese institutions publishing 28% of global CRISPR peer-reviewed papers in 2024. Commercial CRISPR activity in China is led by EdiGene, CorrectSequence Therapeutics, and Huigene Therapeutics, each advancing CRISPR-based haematology therapeutics through NMPA clinical trial approvals secured in 2024 and 2025. Japan's CRISPR market is anchored by the RIKEN Institute's prime editing research programme and by Takeda Pharmaceutical's co-development agreements with US CRISPR therapeutic companies for Asia Pacific commercialisation rights. South Korea's CRISPR agricultural programme, particularly the development of disease-resistant rice and high-yield soybeans under Rural Development Administration (RDA) coordination, represents the region's most commercially advanced CRISPR agricultural programme outside the US. Australia's CRISPR diagnostics market is expanding through the Commonwealth Scientific and Industrial Research Organisation's (CSIRO) CRISPR biosensor development programme targeting food safety and infectious disease detection.

Latin America

Latin America held a 4.6% share of the CRISPR technology market in 2025, generating USD 0.14 Billion, with Brazil accounting for approximately 58% of regional revenue. Brazil's CRISPR market benefits from Fiocruz's genome editing research capacity and EMBRAPA's agricultural biotechnology programme, which is developing CRISPR-edited drought-tolerant sugarcane and disease-resistant citrus varieties under Brazil's regulatory framework for genome editing that classifies small deletion edits as equivalent to conventional mutagenesis breeding, enabling faster commercial deployment. Argentina, hosting the largest per-capita CRISPR research publication rate in Latin America, contributes 22% of regional revenue through university research tools demand and emerging biotech company formations. Mexico's CRISPR market is nascent but growing as multinational biopharma companies establish R&D operations in Monterrey and Mexico City, creating demand for localised CRISPR reagent supply chains.

Middle East & Africa

The Middle East & Africa region held a 3.6% share of the CRISPR technology market in 2025, generating USD 0.11 Billion, with Israel representing the dominant national market at approximately 44% of regional revenue. Israel's Weizmann Institute of Science and Tel Aviv University maintain active CRISPR therapeutic and diagnostic development programmes, and Israeli biotech companies including Arctus Biotherapeutics and Seelos Biosciences license CRISPR-related IP from Israeli academic institutions for global commercialisation. The UAE's Mohammed Bin Rashid University of Medicine and Health Sciences is building CRISPR genomics research capacity under the UAE Genome Programme, which committed USD 100 Million to genome editing and precision medicine research through 2028. South Africa anchors the African CRISPR market through the University of Cape Town's H3Africa consortium participation and CRISPR-based malaria diagnostic research funded by the Bill & Melinda Gates Foundation. The region's market is projected to grow at 24.1% CAGR through 2034, the highest regional growth rate, from a low base as government science investments mature.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Application

- Therapeutics & Clinical Development

- Research Tools & Reagents

- Diagnostics

- Agricultural Biotechnology

By Editing Platform

- CRISPR-Cas9

- CRISPR-Cas12a (Cpf1)

- Base Editing

- Prime Editing

- CRISPR-Cas13 (RNA Editing)

By End-User

- Biopharmaceutical Companies & CDMOs

- Academic & Government Research Institutions

- Hospitals & Clinical Centres

- Agricultural & Industrial Biotechnology

By Delivery Method

- Viral Vectors (AAV, Lentiviral)

- Lipid Nanoparticles (LNP)

- Ribonucleoprotein (RNP) Electroporation

- Other Non-Viral Delivery

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.14 B |

| Forecast Revenue (2034) | USD 18.62 B |

| CAGR (2025-2034) | 21.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Application, (Therapeutics & Clinical Development, Research Tools & Reagents, Diagnostics, Agricultural Biotechnology), By Editing Platform, (CRISPR-Cas9, CRISPR-Cas12a (Cpf1), Base Editing, Prime Editing, CRISPR-Cas13 (RNA Editing)), By End-User, (Biopharmaceutical Companies & CDMOs, Academic & Government Research Institutions, Hospitals & Clinical Centres, Agricultural & Industrial Biotechnology), By Delivery Method, (Viral Vectors (AAV, Lentiviral), Lipid Nanoparticles (LNP), Ribonucleoprotein (RNP) Electroporation, Other Non-Viral Delivery) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | INTELLIA THERAPEUTICS, CRISPR THERAPEUTICS, EDITAS MEDICINE, BEAM THERAPEUTICS, PRECISION BIOSCIENCES, CARIBOU BIOSCIENCES, ERS GENOMICS, MAMMOTH BIOSCIENCES, PRIME MEDICINE, ARBOR BIOTECHNOLOGIES, METAGENOMI, EXCISION BIOTHERAPEUTICS, APERTURE THERAPEUTICS, INTEGRATED DNA TECHNOLOGIES (IDT), THERMO FISHER SCIENTIFIC, MERCK KGAA (SIGMA-ALDRICH), NEW ENGLAND BIOLABS, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Editing Platform (CRISPR-Cas9, Cas12a, Base Editing, Prime Editing, Cas13), By End-User (Biopharma, Academic & Research Institutes, Hospitals, Agriculture & Industrial Biotech), By Delivery Method (Viral Vectors, LNPs, RNP Electroporation) Industry Trends & Forecast 2026–2034")

, By Editing Platform (CRISPR-Cas9, Cas12a, Base Editing, Prime Editing, Cas13), By End-User (Biopharma, Academic & Research Institutes, Hospitals, Agriculture & Industrial Biotech), By Delivery Method (Viral Vectors, LNPs, RNP Electroporation) Industry Trends & Forecast 2026–2034")

, By Editing Platform (CRISPR-Cas9, Cas12a, Base Editing, Prime Editing, Cas13), By End-User (Biopharma, Academic & Research Institutes, Hospitals, Agriculture & Industrial Biotech), By Delivery Method (Viral Vectors, LNPs, RNP Electroporation) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the CRISPR Technology Market?

Global CRISPR technology market valued at USD 2.58B in 2024, reaching USD 18.62B by 2034, growing at a CAGR of 21.9% from 2026–2034.

Who are the major players in the CRISPR Technology Market?

INTELLIA THERAPEUTICS, CRISPR THERAPEUTICS, EDITAS MEDICINE, BEAM THERAPEUTICS, PRECISION BIOSCIENCES, CARIBOU BIOSCIENCES, ERS GENOMICS, MAMMOTH BIOSCIENCES, PRIME MEDICINE, ARBOR BIOTECHNOLOGIES, METAGENOMI, EXCISION BIOTHERAPEUTICS, APERTURE THERAPEUTICS, INTEGRATED DNA TECHNOLOGIES (IDT), THERMO FISHER SCIENTIFIC, MERCK KGAA (SIGMA-ALDRICH), NEW ENGLAND BIOLABS, OTHERS

Which segments covered the CRISPR Technology Market?

By Application, (Therapeutics & Clinical Development, Research Tools & Reagents, Diagnostics, Agricultural Biotechnology), By Editing Platform, (CRISPR-Cas9, CRISPR-Cas12a (Cpf1), Base Editing, Prime Editing, CRISPR-Cas13 (RNA Editing)), By End-User, (Biopharmaceutical Companies & CDMOs, Academic & Government Research Institutions, Hospitals & Clinical Centres, Agricultural & Industrial Biotechnology), By Delivery Method, (Viral Vectors (AAV, Lentiviral), Lipid Nanoparticles (LNP), Ribonucleoprotein (RNP) Electroporation, Other Non-Viral Delivery)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date