- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Cross-Border Payment Orchestration Market Size, Share | CAGR 16.2%

Global Cross-Border Payment Orchestration Market Size, Share, Growth Analysis By Component (Platform & Software, Implementation & Managed Services, Advisory Solutions), By Payment Mode (B2B, B2C, C2C Remittance), By End-User (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare), By Enterprise Size (Large Enterprises, SMEs), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

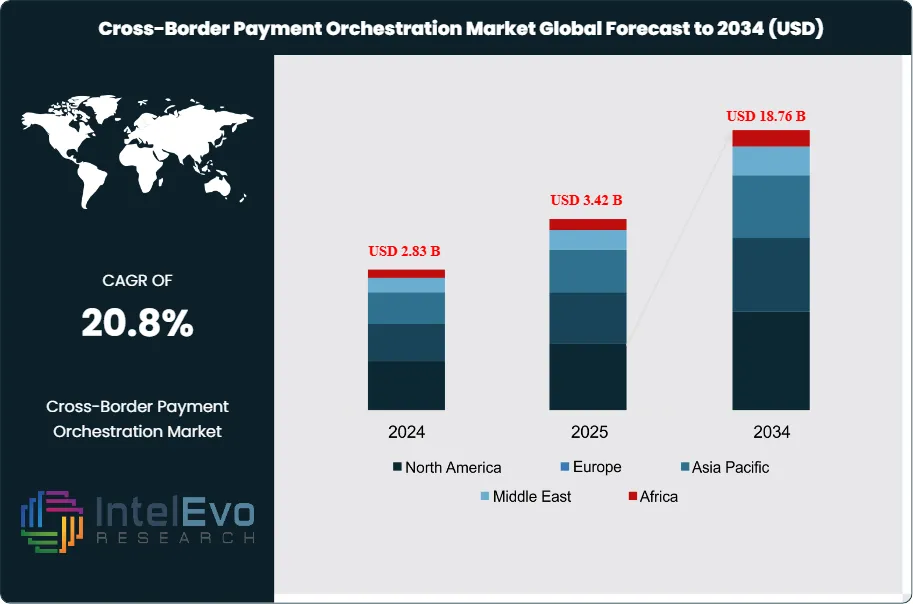

| USD 3.42 Billion | USD 18.76 Billion | 20.8% | North America, 34.6% |

The Cross-Border Payment Orchestration Market was valued at approximately USD 2.83 Billion in 2024 and reached USD 3.42 Billion in 2025. The market is projected to grow to USD 18.76 Billion by 2034, expanding at a CAGR of 20.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 15.34 Billion over the analysis period — an expansion driven by the convergence of global B2B payment volume growth, the structural obsolescence of correspondent banking for real-time digital commerce, and a regulatory reformation cycle across three major currency blocs that is simultaneously opening new payment rail access and mandating transparency standards that favor orchestration software over opaque legacy intermediation chains.

Get More Information about this report -

Request Free Sample ReportThe cross-border payment orchestration category is analytically distinct from cross-border payment processing: processing refers to the movement of funds across borders through a chosen rail; orchestration refers to the software intelligence layer that determines which rail to use, in which currency, at which moment, through which compliance pathway, and at what cost — then executes, monitors, reconciles, and reports the transaction across multiple institutional participants simultaneously. This distinction is commercially significant because the orchestration layer's value proposition scales with payment complexity: a single-corridor, single-currency business with one banking partner requires no orchestration. An e-commerce platform operating in 60 countries, receiving payments in 40 currencies through 18 local payment methods, settling to 12 currency accounts across 8 banking partners, and reporting to 6 regulatory jurisdictions requires orchestration software to maintain any competitive payment acceptance cost and speed.

Three specific triggers explain the market's current 20.8% CAGR. The first is the volume inflection in global B2B cross-border payments, which reached USD 150 trillion in annualized flow by end-2024, according to cross-referenced data from SWIFT gpi and BIS Triennial Survey estimates. SME internationalization — specifically the expansion of digital-native businesses into cross-border commerce without establishing local banking infrastructure — drove a disproportionate share of new payment orchestration demand, as SMEs generating USD 50,000–5 million in annual cross-border revenue require API-accessible orchestration platforms rather than the bespoke treasury management systems historically available only to multinational corporations. Stripe reported that 36% of its 2024 payment volume originated from businesses with fewer than 50 employees conducting cross-border transactions — a customer cohort that did not exist as a meaningful payment orchestration buyer segment before 2020.

The second trigger is the proliferation of real-time payment infrastructure across emerging markets that creates both new routing opportunities and new orchestration complexity. India's Unified Payments Interface processed 18.4 billion transactions in December 2024, Brazil's PIX processed 6.8 billion monthly transactions, and Singapore's PayNow linked 12 bilateral instant payment corridors as of mid-2025. Each new real-time rail represents a potential faster and cheaper routing alternative to correspondent banking for specific corridors — but also requires orchestration software to evaluate its suitability, manage its compliance requirements, monitor its availability, and integrate its settlement data into multi-rail reconciliation workflows. An enterprise treasury team managing payment flows across 10 countries in 2019 typically needed to interface with 3–4 banking rails; the same flows in 2025 involve 8–14 rails including local real-time networks, requiring orchestration platforms to replace what was previously a manually manageable banking relationship portfolio.

The third trigger is regulatory: the EU's Instant Payments Regulation, requiring European banks to offer SEPA Instant Credit Transfer at standard pricing from January 2025 and to receive instant payments from October 2025, eliminated the fee premium that had previously discouraged instant payment adoption across 36 SEPA member states. This single regulatory event added approximately EUR 1.4 trillion in annual payment volume to SEPA Instant rails that orchestration software must now evaluate alongside SWIFT, card networks, and bilateral API rails for European payment routing. A contrarian observation qualifies the market's apparent uniformity of growth: revenue concentration is intensifying more rapidly than total market growth suggests. The top five cross-border payment orchestration platforms captured an estimated 58.4% of market revenue in 2025, up from 44.7% in 2022 — a consolidation dynamic driven by the network effects of multi-rail connectivity, where each additional currency and payment method connection increases the platform's value for all existing clients and raises switching costs for any client that would lose accumulated routing logic and compliance rule sets on migration.

, By Payment Mode (B2B, B2C, C2C Remittance), By End-User (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare), By Enterprise Size (Large Enterprises, SMEs), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global cross-border payment orchestration market reached USD 3.42 Billion in 2025 and is forecast to reach USD 18.76 Billion by 2034 at a CAGR of 20.8% over the 2026–2034 period, driven by B2B payment volume growth to USD 150 trillion annually, real-time rail proliferation across emerging markets, and the EU Instant Payments Regulation eliminating SEPA Instant price premiums from January 2025.

- Segment Dominance (By Component): Platform and software solutions captured 62.8% of component revenue at USD 2.15 Billion in 2025, because multi-rail routing logic, compliance rule engines, and FX optimization algorithms require continuous software iteration that one-time professional services engagements cannot maintain — and because SaaS delivery generates recurring revenue at 5–8x the margin of equivalent consulting-led implementation.

- Segment Dominance (By Payment Mode): B2B cross-border payments held 54.3% of mode-segmented revenue at USD 1.86 Billion in 2025, anchored by corporate treasury demand for multi-rail routing that minimizes the 1.5–3.5% blended cost of correspondent banking intermediation on the USD 150 trillion annual B2B international payment flow — a cost reduction opportunity that generates measurable CFO-level ROI justification.

- Driver: Real-time payment rail proliferation — India UPI's 18.4 billion December 2024 transactions, Brazil PIX's 6.8 billion monthly volume, and 12 bilateral PayNow corridors — expanded the orchestration-relevant rail universe from 3–4 banking connections per corridor in 2019 to 8–14 addressable rails per corridor in 2025, making intelligent routing software operationally necessary rather than merely economically beneficial.

- Restraint: AML/CFT compliance fragmentation across 196 jurisdictions — with FATF Recommendation 16 Travel Rule implementation varying by country in transaction threshold, data format, and counterparty verification depth — forces payment orchestration platforms to maintain jurisdiction-specific compliance rule engines that collectively add USD 2.8–4.6 million annually in regulatory technology development costs, compressing margins and creating a structural barrier for sub-scale entrants.

- Opportunity: Stablecoin payment settlement orchestration represents an addressable market expansion of USD 3.2–5.8 Billion by 2030, as MiCA-regulated EUR-stablecoins and U.S. STABLE Act-authorized dollar stablecoins create regulated on-chain payment rails that orchestration platforms can route alongside traditional banking rails — enabling sub-second, near-zero-cost settlement that reduces the total cost of cross-border payment acceptance by 60–75% for early platform adopters.

- Trend: AI-driven dynamic FX routing and payment success rate optimization reached 47% feature adoption among Tier-1 orchestration platform clients in North America in 2025 versus 21% in Asia Pacific, with documented payment success rate improvements of 8–14 percentage points through ML-based retry logic and real-time bank connectivity health monitoring — translating to USD 180–340 million in recovered payment revenue for a mid-size e-commerce platform processing USD 2 billion in annual cross-border volume.

- Regional Analysis: North America held 34.6% of global cross-border payment orchestration revenue at USD 1.18 Billion in 2025, anchored by the concentration of global e-commerce platforms and marketplace operators in San Francisco, New York, and Seattle that process the world's highest per-company cross-border payment volumes and drive platform feature development investment through enterprise contract values averaging USD 1.2–8 million annually.

Competitive Landscape Overview

The cross-border payment orchestration market is moderately consolidated, with the top four platforms — Stripe, Adyen, Wise Platform, and Airwallex — collectively accounting for an estimated 51.3% of total market revenue in 2025, with concentration intensifying from 44.7% in 2022 as network effects compound with rail breadth. Competition operates on four distinct axes: rail coverage depth (number of supported currencies, local payment methods, and real-time networks); compliance automation completeness (jurisdiction count covered by automated AML/CFT, sanctions screening, and Travel Rule compliance); FX pricing competitiveness (spread above interbank mid-market rate); and API developer experience (time-to-first-transaction, documentation quality, and sandbox fidelity). The competitive landscape bifurcates between full-stack platforms that combine payment orchestration with multi-currency account infrastructure and FX treasury management (Stripe, Adyen, Airwallex, Wise Platform) and infrastructure-layer specialists that provide orchestration rails to banks and fintechs on a white-label or API basis without consumer-facing products (Currencycloud, Banking Circle, Nium, Thunes). In 2025, SWIFT's Strategic Roadmap for Instant and Frictionless Payments — particularly its gpi Instant interoperability standard — created a competitive dynamic where SWIFT is simultaneously the infrastructure that orchestration platforms route through and a competitive threat as SWIFT positions gpi as a competing orchestration layer for its 11,000+ bank members. Three Central Bank Digital Currency pilot programs in Singapore (Project Nexus), the EU (digital euro wholesale pilot), and the UAE (mBridge) are developing settlement infrastructure that, once operational, would represent additional orchestration routing options that platform vendors are beginning to integrate in anticipation.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (2024–2026) |

| Stripe | USA | Leader | Stripe Connect Global + Stripe Treasury | North America / Europe | Launched Stripe Stablecoin Financial Accounts in Jan 2026, enabling businesses in 101 countries to hold USDC and USDB balances and settle cross-border transactions at near-zero FX cost, processing USD 1.4 trillion in total payment volume in 2024. |

| Adyen | Netherlands | Leader | Adyen Unified Commerce Cross-Border Platform | Europe / North America / APAC | Expanded Adyen's direct acquiring network to 37 countries in 2025, adding local acquiring in Brazil, Mexico, and Saudi Arabia to eliminate cross-border interchange fees for Adyen-acquiring merchants, reducing payment acceptance costs by 18–32% in new markets. |

| Wise Platform | UK | Leader | Wise Platform API (B2B Infrastructure) | Europe / Asia Pacific / North America | Launched Wise Platform multi-currency account infrastructure for banks and fintechs in Q1 2025, enabling 14 partner banks — including Standard Chartered and N26 — to offer Wise's real exchange rate to retail and SME customers under white-label arrangements. |

| Airwallex | Australia / HK | Leader | Airwallex Global Payments Infrastructure | Asia Pacific / Europe | Secured USD 300 million Series F at a USD 5.6 billion valuation in Sep 2025; launched Airwallex Embedded Finance suite enabling non-financial platforms to embed multi-currency accounts and cross-border payment rails into SaaS products without becoming licensed e-money institutions. |

| Nium | Singapore | Challenger | Nium Real-Time Payments Network | Asia Pacific / Europe / North America | Achieved SWIFT Partner status in Nov 2025, enabling Nium's 100+ currency real-time payment network to interoperate with SWIFT gpi for 11,000+ bank members; processed USD 8 billion in annualized GMV across 190+ countries. |

| Rapyd | Israel / UK | Challenger | Rapyd Collect, Disburse & Wallet Suite | Europe / Asia Pacific | Acquired PayU's GPO (Global Payment Organization) business in Q3 2025 for USD 610 million, adding 18 new payment method integrations across Latin America and Southeast Asia and expanding Rapyd's local payment rail coverage to 65 countries. |

| Currencycloud | UK (Visa) | Challenger | Currencycloud Spark B2B FX Platform | Europe / North America | Integrated Currencycloud's multi-currency wallet infrastructure into Visa B2B Connect's settlement layer in Mar 2025, enabling near-instant cross-border wholesale payments across 30 currencies without correspondent banking intermediaries. |

| Thunes | Singapore | Challenger | Thunes Cross-Border Payment Network | Asia Pacific / Africa / Middle East | Extended Thunes Direct Global Network to 130+ countries in Oct 2025 by adding mobile money wallet payout rails across 18 African markets and real-time bank transfer capabilities in Indonesia, Vietnam, and Bangladesh. |

| Banking Circle | Luxembourg | Niche Player | Banking Circle Super-Correspondent Platform | Europe | Launched Banking Circle Payment Account for European fintechs and banks in Feb 2026, providing direct access to TARGET2 and SEPA Instant Credit Transfer rails without correspondent bank intermediation, reducing settlement times from T+1 to under 10 seconds for EUR-denominated cross-border flows. |

| Flutterwave | Nigeria / USA | Niche Player | Flutterwave Send App & Business API | Africa / North America | Processed USD 34 billion in annualized payment volume across Africa in 2025; launched Flutterwave FX Engine with real-time African currency conversion across 16 currency pairs in Aug 2025, enabling intra-African B2B settlement at market-rate FX with sub-minute processing. |

By Component

Platform and software solutions captured 62.8% of the cross-border payment orchestration market at USD 2.15 Billion in 2025 — a dominance grounded in the fundamental economics of multi-rail payment routing, where the software logic that selects, executes, and reconciles payment routes must update continuously as rail availability, FX rates, correspondent bank liquidity, and regulatory requirements change in real time. A corporate treasury team routing USD 50 million monthly across 15 currency corridors through a manually managed banking relationship model makes routing decisions based on standing agreements updated quarterly; the same treasury team using an orchestration platform makes routing decisions updated every 15 seconds based on live FX spreads, payment network latency data, and bank connectivity health scores. This real-time optimization function cannot be replicated through professional services engagements — it requires software infrastructure that persists, learns, and updates continuously. Stripe's pricing data shows that merchants using Stripe's adaptive acceptance optimization — which routes retry attempts across alternative acquirers based on bank response codes — recover an average 3.2% of payment volume that would otherwise fail, translating to USD 6.4 million in recovered annual revenue for a platform processing USD 200 million in cross-border transactions.

Services retained 37.2% of component revenue at USD 1.27 Billion in 2025, concentrated in three high-value professional services categories: compliance implementation consulting for jurisdiction-specific AML/CFT rule engine configuration; treasury optimization advisory for multi-currency hedging strategy integrated with orchestration platform FX exposure data; and technical integration services for connecting legacy ERP and accounting systems to orchestration API outputs. The services segment's sustained relevance reflects the genuine complexity of cross-border payment compliance: a platform operating in 60 countries must implement 60 distinct AML transaction monitoring thresholds, 47 sanctions screening list configurations, and 36 FATF Recommendation 16 Travel Rule data formats — an implementation complexity that generates 400–800 hours of billable professional services per new market entry. Managed services, representing approximately 28% of total services revenue, are growing fastest at an estimated 24.3% annually, as enterprise clients with compliance-intensive cross-border operations prefer vendor-operated compliance monitoring to internal regulatory technology investment.

By Payment Mode

B2B cross-border payments generated 54.3% of mode-segmented revenue at USD 1.86 Billion in 2025 — a dominance that reflects the intersection of highest payment volume, highest friction cost, and therefore highest orchestration ROI among all payment mode categories. Corporate-to-corporate international payments average USD 2,000–250,000 per transaction, involve multi-step correspondent banking chains that add 1.5–3.5% in aggregate fees and 2–5 business days in settlement time, and require invoice reconciliation, dual-approval workflows, and regulatory reporting that manual treasury processes manage at high operational cost. The World Bank's Remittance Prices Worldwide database confirms that corporate cross-border payments through traditional correspondent networks carry blended costs 3.8–6.2x higher than comparable domestic payment equivalents — a gap that payment orchestration platforms partially close through direct rail access, batch optimization, and FX netting that eliminates redundant currency conversion steps. Airwallex's enterprise client data indicates that B2B treasury teams using multi-rail orchestration platforms reduce blended cross-border payment costs by 42–67% compared with single-bank correspondent relationships, generating ROI timelines of 4–8 months on platform subscription costs at USD 200,000–1.2 million annually.

B2C cross-border payments held 31.4% of mode-segmented revenue at USD 1.07 Billion in 2025, growing at 22.8% annually — driven by e-commerce marketplace internationalization, digital subscription platform expansion, and gig economy platform disbursements to international contractors. C2C remittances at 14.3% represent the smallest mode segment by orchestration software revenue despite representing the largest share of cross-border payment transaction count — because remittance-focused platforms (Wise, Remitly, WorldRemit) have internalized orchestration logic within proprietary technology rather than purchasing external orchestration software, and because per-transaction orchestration value is lowest for the small-denomination, high-volume consumer remittance category. The fastest-growing B2C sub-application is cross-border subscription billing, where platforms like Netflix, Spotify, and Salesforce require orchestration software to manage local payment method acceptance, currency conversion, failed payment retry logic, and involuntary churn reduction across 190+ country market deployments simultaneously.

By End-User

Banking and financial institutions represented 38.6% of end-user demand at USD 1.32 Billion in 2025, their dominant position reflecting the structural transformation of correspondent banking economics. Traditional correspondent banking — where a payment traverses 3–6 correspondent bank relationships before reaching its destination — carries average per-transaction fees of USD 25–45 for standard SWIFT MT payments, a cost structure that is commercially uncompetitive for the high-frequency, low-value cross-border payments that digital commerce generates. Barclays, Standard Chartered, and ING have each publicly disclosed correspondent banking relationship rationalization programs that reduced their active correspondent partner count by 30–45% between 2020 and 2024, replacing correspondent intermediation with direct API connections to payment orchestration platforms for corridors where volume justifies direct rail investment. This rationalization trend converts banks from passive correspondent network participants into active orchestration platform buyers, generating a procurement category that did not exist at meaningful scale before 2022.

E-commerce and retail at 28.4% (USD 0.971 Billion) is the fastest-growing end-user segment at an estimated 25.6% annually, driven by the cross-border commerce expansion of marketplace platforms that require payment acceptance in 40–80 local currencies and disbursement to sellers in 100+ countries simultaneously. Shopify's 2024 disclosure that 46% of Shopify merchant revenue derived from cross-border sales — up from 31% in 2021 — indicates the scale of cross-border payment orchestration demand embedded in e-commerce infrastructure. Travel and hospitality at 14.7%, healthcare at 9.8%, and other industries at 8.5% complete the end-user distribution, with healthcare cross-border payment orchestration growing fastest within the secondary segments as medical tourism platforms and international health insurance administrators require compliant cross-border reimbursement workflows across jurisdictions with distinct privacy frameworks (HIPAA, GDPR, PDPA).

By Enterprise Size

Large enterprises held 61.4% of enterprise-size segmented revenue at USD 2.10 Billion in 2025, reflecting the commercial logic that orchestration value scales with payment volume and corridor complexity: a multinational corporation processing USD 500 million annually in cross-border payments achieves USD 7.5–17.5 million in annual fee savings from optimized orchestration that a USD 2 million payment volume SME cannot replicate at proportional scale. Large enterprise orchestration contracts carry average annual contract values of USD 1.2–8 million, covering dedicated implementation resources, custom compliance rule engine configuration, direct banking relationship brokering, and SLA-backed uptime guarantees that command premium pricing above self-service SME tiers. The specific competitive dynamic within large enterprise orchestration is that the top five global enterprise treasury management system vendors — SAP, Oracle, Kyriba, ION Group, and FIS Integrity — are integrating payment orchestration API connectivity into their core treasury platforms, creating partnership or acquisition pressure on standalone orchestration vendors as ERP buyers prefer integrated treasury-to-payment workflows over point-solution API relationships. SMEs contributed 38.6% at USD 1.32 Billion in 2025, growing at 24.7% annually as API-first self-service orchestration platforms lower the minimum viable payment volume threshold for orchestration investment from USD 50 million (2020 benchmark) to USD 2 million (2025 benchmark).

Regional Analysis

North America

Concentration of the world's highest-revenue e-commerce platforms, digital marketplace operators, and SaaS companies in San Francisco, Seattle, and New York — organizations generating cross-border payment volumes that individually exceed the total payment flows of entire emerging market countries — anchored North America's cross-border payment orchestration market at 34.6% of global revenue and USD 1.18 Billion in 2025. The United States accounts for approximately 88% of North American market revenue, driven by the payment orchestration procurement of platform economy leaders: Uber's 70-country driver disbursement network, Airbnb's host payout operations across 220 countries and territories, and Amazon Marketplace's seller payment settlement in 200+ markets collectively require orchestration platforms managing thousands of daily routing decisions across dozens of active currency corridors. The U.S. Treasury's Financial Crimes Enforcement Network (FinCEN) Travel Rule implementation guidance, issued in final form in 2024, created a compliance procurement cycle among U.S.-regulated money services businesses that generated significant managed compliance service revenue for orchestration platforms offering automated Travel Rule data transmission. Canada contributed the regional balance, with Toronto-headquartered Shopify's cross-border merchant payment orchestration requirements driving Canadian fintech infrastructure investment — Shopify disclosed processing USD 235 billion in total merchant payment volume in 2024, with cross-border transactions representing the fastest-growing component.

Europe

Two intersecting regulatory developments transformed the European cross-border payment orchestration market's competitive dynamics in 2025, generating procurement activity that pushed the region to 28.8% global share worth USD 0.985 Billion. The EU Instant Payments Regulation's January 2025 mandatory offering requirement for SEPA Instant Credit Transfer — at fees no higher than standard SEPA Credit Transfer — eliminated the pricing barrier that had restricted SEPA Instant adoption to early adopters, adding approximately EUR 1.4 trillion in annual payment volume to instant rails that orchestration software must now evaluate alongside SWIFT and card network routing. The Payment Services Directive 3 consultation process, published for industry response in Q2 2025, introduced proposed mandatory open banking data sharing requirements extending to corporate treasury data — a regulatory development that Adyen, Banking Circle, and Currencycloud are pre-positioning to exploit through treasury orchestration platform features ahead of PSD3 final implementation. Germany led European demand through Deutsche Bank's Frankfurt-headquartered corporate treasury client base adopting multi-rail orchestration for EUR/USD/GBP corridors, supplemented by SAP's Walldorf-campus treasury management system integrations that connect SAP S/4HANA cash management modules to orchestration platform APIs across 18,000+ European enterprise SAP clients. The Netherlands, home to Adyen's Amsterdam headquarters and the highest concentration of European cross-border e-commerce platform operators per capita, represented the region's highest orchestration software spend density.

Asia Pacific

Real-time payment rail proliferation concentrated across Singapore's PayNow bilateral corridors, India's UPI international expansion to 10 partner countries, and Malaysia's DuitNow cross-border linkage with Thailand's PromptPay and Singapore's PayNow, propelled Asia Pacific's cross-border payment orchestration market to 25.4% global share at USD 0.869 Billion in 2025 — the fastest-growing major region at an estimated 26.2% annually. Singapore dominated APAC orchestration platform vendor concentration, with Nium, Airwallex (APAC operations), Thunes, and Rapyd (APAC division) all maintaining primary operational infrastructure in Singapore's Monetary Authority-regulated fintech environment. India's Reserve Bank of India expanded UPI cross-border capabilities to 10 bilateral corridors by mid-2025 — including UAE, Singapore, Bhutan, Nepal, and six additional markets — converting India's 18.4 billion monthly UPI transactions into a significant cross-border orchestration routing destination that international platforms require software integration to access. China's cross-border payment landscape, dominated by CNAPS (China National Advanced Payment System) and Alipay's international payment services, generated orchestration demand primarily from multinational corporations managing CNY settlement for Chinese supplier payments — a corridor where Airwallex and Nium compete with domestic Chinese orchestration providers including LianLian Pay and PingPong, which collectively process an estimated USD 28 billion in annual cross-border e-commerce settlement for Chinese export merchants.

Latin America

Brazil's PIX instant payment infrastructure — processing 6.8 billion monthly transactions by end-2024 and achieving 74% adult population enrollment within three years of launch, faster than any comparable real-time payment system globally — became the defining orchestration integration priority for international platforms seeking Brazilian market access, pushing Latin America's cross-border payment orchestration market to USD 0.233 Billion (6.8% global share) in 2025. PIX's open API architecture and Banco Central do Brasil's mandatory participation rules for financial institutions above BRL 500 million in assets created a standardized integration point that international orchestration platforms could connect to via a single API endpoint rather than bilateral banking relationships — reducing Brazilian market entry complexity for orchestration vendors by an estimated 18 months of banking partnership negotiation. Rapyd's July 2025 acquisition of PayU's Global Payment Organization business, adding PIX, OXXO (Mexico), and PSE (Colombia) local payment method coverage across 18 Latin American markets, established Rapyd as the most comprehensive Latin America cross-border orchestration provider by payment method breadth. Chile's Comisión para el Mercado Financiero's 2025 open finance regulation, requiring banks and fintechs to expose standardized APIs for payment initiation, created a Chilean payment orchestration market dynamic analogous to PSD2 in Europe — where regulatory-mandated API access creates the infrastructure prerequisite for third-party orchestration platform development.

Middle East & Africa

Saudi Arabia's Vision 2030 financial sector development targets — specifically the Monetary Authority's (SAMA) Instant Payment System Sarie infrastructure and the strategic goal of reducing cash payment share from 61% to 24% of consumer transactions by 2030 — combined with the UAE Central Bank's Instant Payment Platform IPP's interoperability linkage with India's UPI and Bahrain's Fawri+ real-time payment network, created the MEA cross-border payment orchestration market's fastest-developing regulatory tailwind, pushing the region to USD 0.150 Billion (4.4% share) in 2025. The UAE's position as a global financial hub, with the Abu Dhabi Global Market and Dubai International Financial Centre collectively hosting 850+ licensed fintech companies as of 2025, generates disproportionate cross-border payment orchestration procurement relative to the country's domestic GDP, as ADGM and DIFC-registered entities use UAE regulatory infrastructure to orchestrate payment flows across African, Asian, and European corridors simultaneously. Flutterwave's August 2025 launch of its FX Engine — providing real-time African currency conversion across 16 currency pairs from Nigerian naira to Kenyan shilling to Ghanaian cedi — addressed the primary friction in intra-African B2B payment orchestration: the absence of direct currency conversion without USD or EUR intermediate legs that add 2.8–4.6% in cross-currency conversion costs to intra-continental trade payment flows. Nigeria, as Africa's largest economy and largest remittance recipient at USD 20.5 billion in 2024, represents the single highest-priority orchestration integration in the continental African market, with Flutterwave and Thunes competing for inbound corridor dominance.

Market Key Segments

By Component

- Platform / Software

- Services (Implementation, Managed, Advisory)

By Payment Mode

- B2B (Business-to-Business)

- B2C (Business-to-Consumer)

- C2C (Consumer-to-Consumer / Remittance)

By End-User

- Banking & Financial Institutions

- E-Commerce & Retail

- Travel & Hospitality

- Healthcare

- Other Industries

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.42 B |

| Forecast Revenue (2034) | USD 18.76 B |

| CAGR (2025-2034) | 20.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Platform / Software, Services (Implementation, Managed, Advisory)), By Payment Mode, (B2B (Business-to-Business), B2C (Business-to-Consumer), C2C (Consumer-to-Consumer / Remittance)), By End-User, (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare, Other Industries), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | STRIPE, ADYEN, WISE PLATFORM, AIRWALLEX, NIUM, RAPYD, CURRENCYCLOUD (VISA), THUNES, BANKING CIRCLE, FLUTTERWAVE, PAYONEER, FISERV (CROSS-BORDER SOLUTIONS), FIS (WORLDPAY), PAYPAL (BRAINTREE GLOBAL), LIANLIANGLOBAL, PINGPONG FINANCIAL, EARTHPORT (VISA), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Payment Mode (B2B, B2C, C2C Remittance), By End-User (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare), By Enterprise Size (Large Enterprises, SMEs), Industry Trends & Forecast 2026-2034")

, By Payment Mode (B2B, B2C, C2C Remittance), By End-User (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare), By Enterprise Size (Large Enterprises, SMEs), Industry Trends & Forecast 2026-2034")

, By Payment Mode (B2B, B2C, C2C Remittance), By End-User (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare), By Enterprise Size (Large Enterprises, SMEs), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Cross-Border Payment Orchestration Market?

The Global Cross-Border Payment Orchestration Market was valued at USD 2.83 Billion in 2024 and is projected to reach USD 18.76 Billion by 2034, growing at a CAGR of 20.8% from 2026 to 2034, driven by rising cross-border e-commerce transactions, increasing demand for real-time international payment processing, API-based payment orchestration platforms, AI-powered fraud detection, blockchain-enabled settlements, and ISO 20022 payment modernization initiatives worldwide.

Who are the major players in the Cross-Border Payment Orchestration Market?

STRIPE, ADYEN, WISE PLATFORM, AIRWALLEX, NIUM, RAPYD, CURRENCYCLOUD (VISA), THUNES, BANKING CIRCLE, FLUTTERWAVE, PAYONEER, FISERV (CROSS-BORDER SOLUTIONS), FIS (WORLDPAY), PAYPAL (BRAINTREE GLOBAL), LIANLIANGLOBAL, PINGPONG FINANCIAL, EARTHPORT (VISA), Others

Which segments covered the Cross-Border Payment Orchestration Market?

By Component, (Platform / Software, Services (Implementation, Managed, Advisory)), By Payment Mode, (B2B (Business-to-Business), B2C (Business-to-Consumer), C2C (Consumer-to-Consumer / Remittance)), By End-User, (Banking & Financial Institutions, E-Commerce & Retail, Travel & Hospitality, Healthcare, Other Industries), By Enterprise Size, (Large Enterprises, Small & Medium Enterprises (SMEs))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cross-Border Payment Orchestration Market

Published Date : 28 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date