- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Crude Oil Desalter Market Size & Forecast 2034 | CAGR 4.6%

Global Crude Oil Desalter Market Size, Share, Growth & Industry Analysis By Technology (Single-Stage Electrostatic Desalters, Two-Stage Electrostatic Desalters, Dual-Frequency & AC/DC Desalters, Chemical-Assisted Systems), By Application (Atmospheric Distillation Feed Preparation, Heavy & Sour Crude Processing, Condensate Treatment, Refinery Revamp), By End User (Refineries, Upstream Processing Facilities, Integrated Complexes), By Component Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

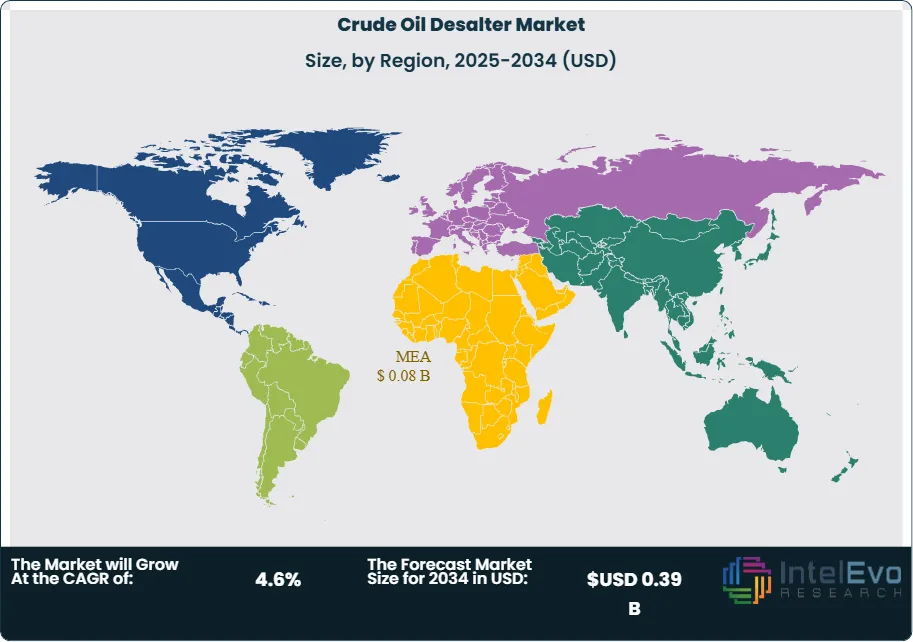

| USD 0.26 Billion | USD 0.39 Billion | 4.6% | Middle East & Africa, 31.0% |

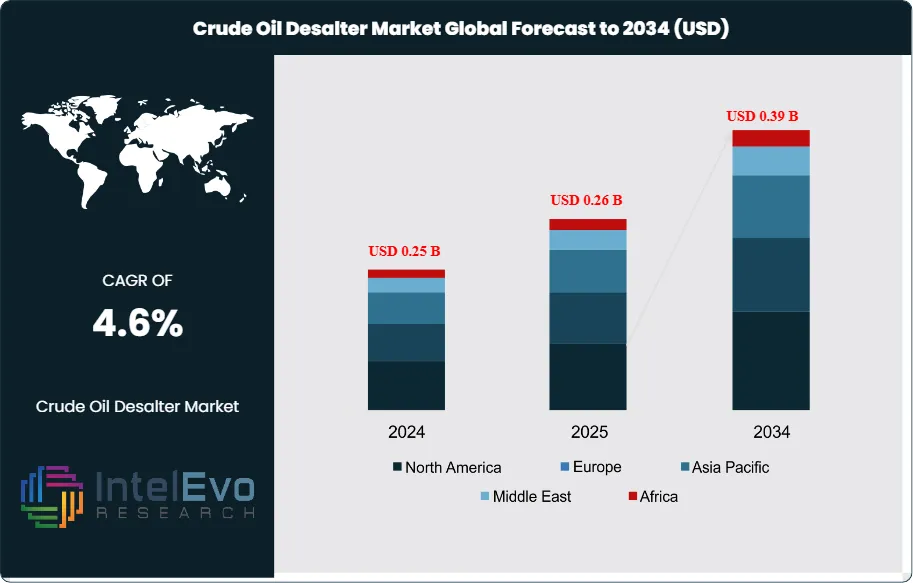

The Crude Oil Desalter Market was valued at approximately USD 0.25 Billion in 2024 and reached USD 0.26 Billion in 2025. The market is projected to grow to USD 0.39 Billion by 2034, expanding at a CAGR of 4.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 0.13 Billion over the analysis period. The crude oil desalter market sits at the front end of refinery economics because salt, solids, and residual water directly affect furnace fouling, overhead corrosion, catalyst life, and CDU reliability. AMPP notes that crude desalting remains one of the most important controls for refinery corrosion management, while refiners continue to face wider crude slates and tighter contamination tolerances.

Get More Information about this report -

Request Free Sample ReportCrude oil desalter demand in 2025 is tied more to refinery upgrades and feedstock flexibility than to greenfield refinery construction. The IEA expects 4.2 mb/d of new refining capacity globally by 2030, partly offset by 1.6 mb/d of closures, with most additions concentrated in Asia and the Middle East. That pattern supports steady orders for two-stage desalters, transformer-rectifier upgrades, mixing valves, wash-water optimization systems, and retrofit internals at high-conversion sites processing heavier and more acidic barrels. In the United States, EIA data show refining capacity changed little as of January 2025, which reinforces the retrofit-heavy nature of North American desalter spending rather than large new-build demand.

The crude oil desalter market also benefits from tougher operating standards inside refinery crude units. Poor desalting raises chloride loading, intensifies corrosion in overhead systems, and increases downstream maintenance cost. Operators are therefore spending on higher-efficiency electrostatic fields, improved interface controls, and digital monitoring to keep salt carryover below target levels and to protect hydrotreating catalysts. Sulzer states that mixing quality and electrostatic separation remain central to salt removal performance, while CECO Peerless highlights guarantee levels down to 5-10 PTB salt and 0.1-0.5 BS&W in designed service windows. Those performance thresholds matter more as refiners buy discounted opportunity crudes to defend margins.

Regional demand remains concentrated in crude-exporting and complex-refining hubs. Middle East & Africa led the crude oil desalter market with 31.0% share in 2025, equal to USD 0.08 Billion, supported by refinery expansions in Saudi Arabia, the UAE, Kuwait, and Nigeria. Asia Pacific held 25.0% share, lifted by India and China, while North America accounted for 20.0% on sustained turnaround and revamp activity. India remains a notable hotspot because domestic refining capacity is targeted to rise from 255 MMTPA to 300 MMTPA by 2030, creating fresh demand for desalting and crude-unit debottlenecking packages. The risk side centers on refinery overcapacity in some basins, delayed project sanctioning, and crude price volatility that can postpone revamps by one to two turnaround cycles.

, By Application (Atmospheric Distillation Feed Preparation, Heavy & Sour Crude Processing, Condensate Treatment, Refinery Revamp), By End User (Refineries, Upstream Processing Facilities, Integrated Complexes), By Component Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: Crude oil desalter market revenue stood at USD 0.26 Billion in 2025 and is projected to reach USD 0.39 Billion by 2034. That implies a 4.6% CAGR across 2025-2034.

- Segment Dominance: Single-stage electrostatic desalters led the crude oil desalter market by technology with 46.0% share in 2025, equal to USD 0.12 Billion. This segment stays dominant because it fits brownfield CDU revamps with lower capex and shorter shutdown windows.

- Segment Dominance: Atmospheric distillation feed preparation led the crude oil desalter market by application with 58.0% share in 2025, equal to USD 0.15 Billion. Most refinery installations remain tied to front-end crude unit protection rather than field treatment duty.

- Driver: Processing of heavier and higher-salt crude slates is the main growth driver. The IEA expects net global refining capacity growth through 2030, and India alone targets a rise to 300 MMTPA by 2030, which supports new and retrofit desalter demand.

- Restraint: Refinery overcapacity in parts of Asia and slow sanctioning of downstream projects limit order flow. Sulzer reported Chemtech orders down 20.3% year over year in H1 2025, partly due to refinery project postponements in Asia.

- Opportunity: Retrofit and digital control upgrades offer the largest near-term opening, estimated at USD 0.06 Billion between 2025 and 2034. SLB, Sulzer, Alfa Laval, and Veolia are all positioned to capture turnaround-linked spending through service, controls, power units, and water-treatment integration.

- Trend: Two-stage and dual-frequency desalting systems are gaining share in complex refineries. Dual-frequency and advanced electro-dynamic systems represented 12.0% of 2025 revenue and should rise to 15.5% by 2034 as refiners handle more variable crude blends.

- Regional Analysis: Middle East & Africa led the crude oil desalter market with 31.0% share and USD 0.08 Billion revenue in 2025. The region benefits from large export-refining hubs, residue-upgrading investments, and high exposure to sour crude processing.

Competitive Landscape Overview

Crude oil desalter market competition is moderately consolidated. The top four players held an estimated 43.0% of 2025 revenue, with competition shaped by process performance, installed base, turnaround support, and regional service reach rather than simple equipment price. Competitive intensity rose in 2025 as refinery customers asked for broader packages that combine internals, power systems, heat integration, wash-water treatment, and digital monitoring. Recent moves such as SLB's ChampionX acquisition, Sulzer's Bahrain expansion, and Veolia's full ownership of Water Technologies and Solutions increased service depth and cross-selling capacity.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | United States | Leader | NATCO ELECTRO-DYNAMIC DESALTER | North America, Middle East | Completed ChampionX acquisition in Jul 2025 |

| SULZER | Switzerland | Leader | Crude Oil Desalting Mixing and Separation Package | Europe, Middle East | Acquired Davies and Mills in Bahrain in Jan 2025 |

| AXENS | France | Leader | Axens Desalter Package | Middle East, Asia Pacific | Expanded Saudi manufacturing base in Apr 2025 |

| VEOLIA WATER TECHNOLOGIES | France | Leader | Crude Oil Desalter Services | Middle East, North America | Moved to full WTS ownership in May 2025 |

| CECO PEERLESS | United States | Challenger | Desalter/Dehydrator Systems | North America | Reported record order above USD 135 Million in Dec 2025 |

| NOV | United States | Challenger | Oil Separation and Stabilization Modules | North America, Latin America | Continued process module push in 2025 |

| ALFA LAVAL | Sweden | Challenger | Desalter Heat Exchanger Train | Europe, North America, Middle East | Opened expanded Gulf Coast service center in Jan 2026 |

| FRAMES | Netherlands | Niche Player | Process Treatment Packages | Middle East | Maintained process package supply presence in 2025 |

| DESALTERS LLC | United States | Niche Player | Trident Desalters Global | North America | Expanded OEM replacement and inspection support in 2025 |

| ERGIL | Türkiye | Niche Player | Electro Dynamic Desalter | Middle East, Central Asia | Promoted electrodynamic desalter offering in Nov 2025 |

By Technology

Crude oil desalter market by technology shows a clear split between proven electrostatic units and newer higher-flexibility systems. Single-stage electrostatic desalters held 46.0% share in 2025, equal to USD 0.12 Billion, because they remain the default choice for standard crude-unit duty in brownfield refineries. They suit light-to-medium crude processing and offer lower vessel count, lower electrical complexity, and easier retrofit execution during routine turnarounds. Two-stage electrostatic systems accounted for 34.0% share, or USD 0.09 Billion, and are strongest in sites processing heavier or more variable barrels where salt removal targets are tighter and wash-water staging improves separation stability. Dual-frequency and AC/DC systems represented 12.0% share, or USD 0.03 Billion, but this segment is the fastest-expanding because refiners need higher tolerance for crude conductivity swings and unstable emulsion behavior. Chemical-assisted and other specialty desalting systems held the remaining 8.0%, or about USD 0.02 Billion, mostly in niche crude slates and field-linked applications. SLB's NATCO platform and similar high-efficiency electro-dynamic systems support the move toward tighter process control, especially where refiners chase discounted sour crude and want to reduce downstream corrosion risk.

By Application

Crude oil desalter market by application remains dominated by atmospheric distillation feed preparation. This segment held 58.0% share in 2025, equal to USD 0.15 Billion, because nearly every refinery crude unit depends on desalting to manage chloride salts before preheat trains, furnaces, and the atmospheric column. Heavy and sour crude processing represented 24.0% share, or USD 0.06 Billion, and posted the strongest order activity in regions where refiners accept wider crude slates to capture feedstock discounts. Condensate and stabilized crude treatment held 10.0% share, or USD 0.03 Billion, supported by upstream and integrated condensate splitters in the Middle East and parts of Asia. Refinery revamp and debottlenecking projects accounted for 8.0%, or USD 0.02 Billion, but this segment has high strategic value because it often triggers bundled orders that include internals, heat exchangers, power units, instrumentation, and operator support. The application mix shows that the crude oil desalter market is not driven by stand-alone vessel sales alone. It is driven by broader unit reliability goals, corrosion control, turnaround timing, and product-quality economics. AMPP and refinery operators continue to treat desalter performance as a direct input into overhead corrosion management and catalyst preservation.

By End User

Crude oil desalter market by end user is led by downstream refineries, which captured 72.0% of 2025 revenue, or USD 0.19 Billion. This dominance reflects the simple fact that desalting is core refinery front-end equipment. Existing refinery sites also generate recurring service revenue through inspections, electrode replacement, transformer upgrades, wash-water tuning, and brine handling support. Upstream central processing facilities represented 18.0% share, or USD 0.05 Billion, where desalting duty is tied to export crude conditioning and terminal specifications. Petrochemical-integrated refining complexes accounted for 10.0%, or USD 0.03 Billion, and their importance is rising in Asia and the Middle East as operators align fuel output with petrochemical feed flexibility. End-user behavior also differs by procurement model. Large downstream refiners tend to favor proven suppliers with field-service depth and local references. Upstream buyers accept more modular solutions and faster-delivery packages. Integrated complexes prefer suppliers that can combine desalting, water treatment, and energy-efficiency measures inside one project scope. That is why vendors such as Veolia, Alfa Laval, and Axens compete beyond the vessel itself and position their offering around operating cost, turnaround duration, and water-quality compliance.

By Component

Crude oil desalter market by component shows vessels and settlers as the largest revenue pool at 41.0% in 2025, equal to USD 0.11 Billion, because pressure-rated shells, internals support, and fabrication remain the highest-ticket items in new installations. Internals, electrodes, mixing valves, and interface devices held 27.0% share, or USD 0.07 Billion, and this area sees frequent retrofit demand because refiners can improve performance without replacing the full shell. Transformers, power supplies, and control systems represented 18.0%, or USD 0.05 Billion, with growing momentum as older rectifier systems are replaced by smarter electrical packages that handle crude variability more effectively. Chemicals, aftermarket services, and spare parts made up the remaining 14.0%, or USD 0.04 Billion, but this slice carries strong margin value and repeat demand. NWL and similar suppliers remain relevant in power systems, while Veolia and specialist service firms benefit from recurring tuning and troubleshooting work. The component mix confirms that the crude oil desalter market has shifted from one-time capex to life-cycle revenue, especially in mature refining centers where installed base density is high and revamp economics are more attractive than major crude-unit replacement.

Regional Analysis

Middle East & Africa

Crude oil desalter market revenue in Middle East & Africa reached 31.0% share and USD 0.08 Billion in 2025, making it the largest regional block. Saudi Arabia, the UAE, Kuwait, and Nigeria led demand. The region benefits from a high concentration of sour-crude processing, export refineries, condensate splitters, and residue-upgrading programs. Saudi Aramco-linked refining infrastructure and ADNOC's refining chain keep demand firm for both new desalter trains and turnaround-related replacements. Nigeria added another layer of demand as large-scale refining capacity ramped and local crude conditioning gained importance. Regional buyers often seek high-capacity two-stage systems, corrosion-resistant internals, and integrated wash-water treatment because crude quality and throughput swings are material. The region also favors suppliers with field-service presence because unplanned crude-unit downtime carries high export and domestic product costs. Sulzer's Bahrain acquisition and Axens' deeper Saudi footprint fit this service-led regional pattern. Middle East & Africa should retain leadership through 2034 because downstream investments remain active and local refiners continue to process heavier and higher-sulfur barrels.

Asia Pacific

Crude oil desalter market revenue in Asia Pacific stood at 25.0% share and USD 0.07 Billion in 2025. China, India, Japan, and South Korea were the main contributors. China remains central because of its large crude throughput and extensive integrated refining base, even as overcapacity pressures restrain some project timing. India is the strongest growth pocket because domestic refinery capacity is expected to rise from 255 MMTPA to 300 MMTPA by 2030, with expansion programs at Panipat, Bina, Paradip, and other sites supporting front-end crude processing upgrades. Japan and South Korea add demand through efficiency-driven revamps and maintenance spending rather than new large refineries. Asia Pacific buyers are highly focused on crude flexibility because regional refiners balance Middle Eastern grades, Russian barrels in some channels, domestic production, and opportunistic imports. That crude-mix complexity raises demand for stronger interface control, wash-water optimization, and heat integration. The region will post the fastest volume growth in the crude oil desalter market, but project execution will remain uneven because some operators face thinner refining margins and longer investment approvals.

North America

Crude oil desalter market revenue in North America accounted for 20.0% share and USD 0.05 Billion in 2025. The United States dominated the region, followed by Canada and Mexico. U.S. demand is centered on Gulf Coast turnaround cycles, heavy-crude handling in selected refineries, and retrofits aimed at reliability rather than brand-new refinery builds. EIA data show that U.S. refining capacity was largely unchanged as of January 2025, confirming that brownfield spending remains the main driver. Canada supports demand through oil sands and heavy-crude conditioning related to export and refining interfaces, while Mexico continues to spend on refinery rehabilitation and crude-unit reliability. North American procurement favors installed-base service providers with local turnaround support, fast spare-parts access, and proven performance in difficult emulsions. Alfa Laval's expanded Gulf Coast service center directly strengthens this aftermarket channel. The region will remain a high-value service market through 2034 because crude-unit reliability, corrosion control, and debottlenecking economics outweigh appetite for new refinery megaprojects. A new Texas refinery proposal announced in March 2026 could add fresh equipment opportunities if it moves into execution.

Europe

Crude oil desalter market revenue in Europe reached 14.0% share and USD 0.04 Billion in 2025. Germany, France, the United Kingdom, and Italy formed the core demand base. Europe has fewer large refinery expansions than Asia or the Middle East, but it maintains steady desalter demand through compliance-driven upgrades, corrosion reduction, energy-efficiency projects, and crude flexibility improvements. European refiners face pressure from carbon policy, older asset age, and competitive imports, so many prefer revamps with fast payback rather than full crude-unit replacement. That supports demand for internals, smarter control packages, and heat exchanger upgrades. Sulzer and Alfa Laval are well placed in this environment because European customers value process efficiency, service quality, and engineering support during planned shutdowns. Italy is strategically important because conversion projects and bio-refining moves keep crude-side reliability spending alive even as some traditional fuels capacity faces long-term pressure. Europe will remain a mature but profitable region in the crude oil desalter market, with spending weighted toward replacement cycles and plant efficiency rather than new vessel count.

Latin America

Crude oil desalter market revenue in Latin America reached 10.0% share and USD 0.03 Billion in 2025. Brazil, Mexico, Argentina, and the rest of Latin America shaped demand. Brazil led on the back of complex refinery operations and continued attention to crude-unit reliability for domestic fuels and export products. Mexico supported demand through refinery rehabilitation and throughput restoration efforts, which often require front-end desalting improvements when crude quality varies. Argentina added a smaller but rising demand stream linked to Vaca Muerta development and the need to condition growing crude flows for transport and refining. Latin America remains more cyclical than North America or Europe because public-sector capex discipline and currency swings can delay projects. Even so, the region offers attractive retrofit work because many plants operate older crude-unit equipment and need incremental gains in corrosion control, salt removal, and water handling. Suppliers that provide short outage execution and modular replacement parts are best placed to win. Latin America should post selective but profitable growth through 2034, especially where local refiners raise utilization and widen crude-slate acceptance.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- Single-Stage Electrostatic Desalters

- Two-Stage Electrostatic Desalters

- Dual-Frequency and AC/DC Desalters

- Chemical-Assisted and Specialty Desalting Systems

By Application

- Atmospheric Distillation Feed Preparation

- Heavy and Sour Crude Processing

- Condensate and Stabilized Crude Treatment

- Refinery Revamp and Debottlenecking

By End User

- Downstream Refineries

- Upstream Central Processing Facilities

- Petrochemical-Integrated Refining Complexes

By Component

- Vessels and Settlers

- Internals, Electrodes, and Mixing Devices

- Transformers, Power Supplies, and Controls

- Chemicals, Aftermarket Services, and Spare Parts

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.26 B |

| Forecast Revenue (2034) | USD 0.39 B |

| CAGR (2025-2034) | 4.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Single-Stage Electrostatic Desalters, Two-Stage Electrostatic Desalters, Dual-Frequency and AC/DC Desalters, Chemical-Assisted and Specialty Desalting Systems), By Application, (Atmospheric Distillation Feed Preparation, Heavy and Sour Crude Processing, Condensate and Stabilized Crude Treatment, Refinery Revamp and Debottlenecking), By End User, (Downstream Refineries, Upstream Central Processing Facilities, Petrochemical-Integrated Refining Complexes), By Component, (Vessels and Settlers, Internals, Electrodes, and Mixing Devices, Transformers, Power Supplies, and Controls, Chemicals, Aftermarket Services, and Spare Parts) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, SULZER, AXENS, VEOLIA WATER TECHNOLOGIES, CECO PEERLESS, NOV, ALFA LAVAL, FRAMES, DESALTERS LLC, ERGIL, NWL, PETRO-TECHNA INTERNATIONAL, CANADIAN PETROLEUM PROCESSING EQUIPMENT, VME, AMR PROCESS, SANTACC ENERGY, OTSO ENERGY SOLUTIONS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Atmospheric Distillation Feed Preparation, Heavy & Sour Crude Processing, Condensate Treatment, Refinery Revamp), By End User (Refineries, Upstream Processing Facilities, Integrated Complexes), By Component Industry Trends & Forecast 2026–2034")

, By Application (Atmospheric Distillation Feed Preparation, Heavy & Sour Crude Processing, Condensate Treatment, Refinery Revamp), By End User (Refineries, Upstream Processing Facilities, Integrated Complexes), By Component Industry Trends & Forecast 2026–2034")

, By Application (Atmospheric Distillation Feed Preparation, Heavy & Sour Crude Processing, Condensate Treatment, Refinery Revamp), By End User (Refineries, Upstream Processing Facilities, Integrated Complexes), By Component Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Crude Oil Desalter Market?

Global crude oil desalter market valued at USD 0.25B in 2024, reaching USD 0.39B by 2034, growing at a CAGR of 4.6% from 2026–2034.

Who are the major players in the Crude Oil Desalter Market?

SLB, SULZER, AXENS, VEOLIA WATER TECHNOLOGIES, CECO PEERLESS, NOV, ALFA LAVAL, FRAMES, DESALTERS LLC, ERGIL, NWL, PETRO-TECHNA INTERNATIONAL, CANADIAN PETROLEUM PROCESSING EQUIPMENT, VME, AMR PROCESS, SANTACC ENERGY, OTSO ENERGY SOLUTIONS, Others

Which segments covered the Crude Oil Desalter Market?

By Technology, (Single-Stage Electrostatic Desalters, Two-Stage Electrostatic Desalters, Dual-Frequency and AC/DC Desalters, Chemical-Assisted and Specialty Desalting Systems), By Application, (Atmospheric Distillation Feed Preparation, Heavy and Sour Crude Processing, Condensate and Stabilized Crude Treatment, Refinery Revamp and Debottlenecking), By End User, (Downstream Refineries, Upstream Central Processing Facilities, Petrochemical-Integrated Refining Complexes), By Component, (Vessels and Settlers, Internals, Electrodes, and Mixing Devices, Transformers, Power Supplies, and Controls, Chemicals, Aftermarket Services, and Spare Parts)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date