- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Crude Oil Flow Improvers Market Size, Share & Forecast 2034 | CAGR 5.4%

Global Crude Oil Flow Improvers Market Size, Share, Analysis By Product Type (Asphaltene Inhibitors, Paraffin Inhibitors, Hydrate Inhibitors, Scale Inhibitors), By Application (Extraction, Transportation, Refinery), By End-Use Industry (Upstream, Midstream, Downstream), Industry Segment Overview, Market Dynamics, Competitive Strategies, Key Players, Regional Insights, Trends & Forecast 2026–2034

Report Overview

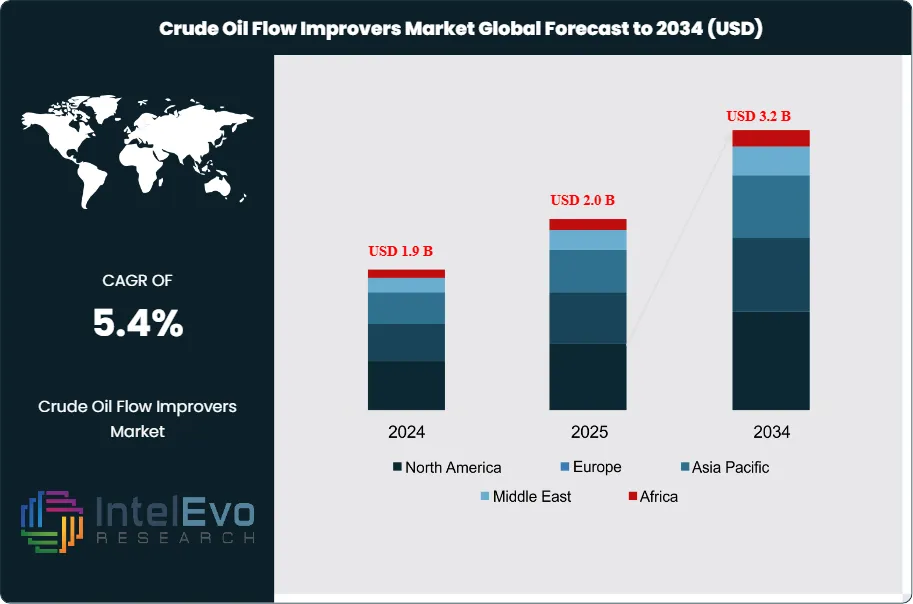

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.0 Billion | USD 3.2 Billion | 5.4% | North America, 30% |

The Crude Oil Flow Improvers Market is estimated at USD 1.9 billion in 2024 and is on track to reach roughly USD 3.2 billion by 2034, The market is further estimated to reach approximately USD 2.0 billion in 2025, and is expected to expand at a compound annual growth rate (CAGR) of around 5.4% during the forecast period from 2026 to 2034. Growth is driven by increasing upstream oil and gas activity, rising demand for efficient flow assurance solutions in complex reservoirs, and expanding production of heavy and unconventional crude. Additionally, advancements in low-dose chemical formulations and digital monitoring systems are further supporting market expansion globally.

Get More Information about this report -

Request Free Sample ReportFlow improvers underpin flow assurance across production, gathering, and pipeline transport. Operators apply these chemistries to manage wax and asphaltene deposition, lower apparent viscosity in colder operating windows, and sustain throughput as crude properties fluctuate. Demand rises with the continued spread of horizontal drilling and hydraulic fracturing, which increases exposure to variable flow regimes and paraffinic crude slates. Operators also widen use beyond long-haul lines into gathering systems and terminals to reduce pressure losses and stabilize flow across mixing points in the petroleum value chain.

Demand and supply forces remain closely tied to operating efficiency and chemical input economics. Midstream throughput programs keep drag-reducing agents at about 35% of 2024 revenue, while paraffin-control additives contribute roughly 40% as operators seek fewer pigging cycles and lower pumping energy. Pipeline and transportation applications represent about 45% of spending, with production and wellsite use near 30% as treatment shifts upstream to prevent solids formation earlier in the system. On the supply side, product performance depends on polymer and surfactant availability, while formulation costs track petrochemical feedstocks and regional manufacturing capacity.

Regulatory influences increasingly shape procurement and product design. EU REACH obligations, tighter aquatic-toxicity screening, and expanding chemical disclosure requirements raise testing and documentation costs and push portfolios toward lower-hazard ingredients. Key risks include crude price volatility that can slow completion activity, performance variability when crude blends or water cut changes, and operational exposure if under-dosing reduces throughput and triggers remediation. Digital connectivity adds cyber and data integrity risk where dosing and monitoring systems link to control networks.

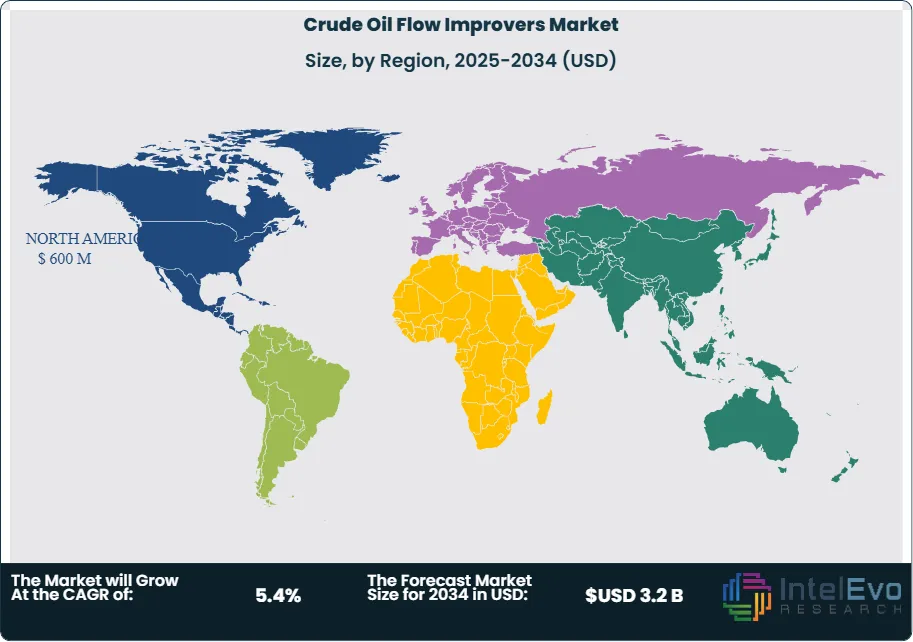

Technology effects now drive differentiation. Suppliers use AI to accelerate formulation screening and tailor additives to basin-specific crude fingerprints, while operators deploy automation in injection skids, inline sensors, and predictive analytics to keep viscosity and deposition within operating limits. Digitally managed programs can cut chemical overuse by an estimated 8–12% while improving consistency. North America leads with about 40% of 2024 revenue, anchored by the Permian and other shale corridors. The Middle East and Latin America remain high-value regions for capacity additions tied to large export streams, while Asia-Pacific is an investment hotspot for new pipelines and storage expansions, supporting faster-than-average growth through 2034.

, By Application (Extraction, Transportation, Refinery), By End-Use Industry (Upstream, Midstream, Downstream), Industry Segment Overview, Market Dynamics, Competitive Strategies, Key Players, Regional Insights, Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market expands from 1.8 billion USD, 2023 to 3.0 billion USD, 2033 and sustains 5.4% CAGR, 2026-2034. It reaches estimated: 1.9 billion USD, 2024 as the baseline for the 2026-2034 horizon.

- Segment Dominance : Paraffin inhibitors lead the product mix with 30.5%, 2023 due to stronger wax-control performance in pipelines. The segment records estimated: 0.6 billion USD, 2023 in revenue contribution.

- Segment Dominance: Extraction drives application demand with 44.8%, 2023 as operators prioritize flow optimization at the wellsite. The segment represents estimated: 0.8 billion USD, 2023 in spending.

- Driver: Hydraulic fracturing activity and government-backed oil and gas development increase treatment volumes by estimated: 6.0%, 2024. Low-dose hydrate inhibitors reduce chemical intensity by estimated: 10.0%, 2024 through improved efficacy per unit injected.

- Restraint: Crude price volatility and tightening environmental rules constrain deployment, raising compliance and reformulation costs by estimated: 5.0%, 2024. Geopolitical disruptions add estimated: 2.0% supply risk premium, 2024 to specialty chemical logistics.

- Opportunity: Rising crude output strengthens demand for paraffin and asphaltene control, lifting addressable demand by estimated: 0.3 billion USD, 2024. Operators expand inhibitor programs to protect throughput, targeting estimated: 3.0% uplift in pipeline utilization, 2024.

- Trend: Suppliers apply AI and automation to accelerate formulation and dosing optimization, cutting time-to-qualification by estimated: 15.0%, 2024. Digital monitoring improves treatment precision, reducing overtreatment by estimated: 8.0%, 2024.

- Regional Analysis: North America leads revenue with estimated: 0.7 billion USD, 2023 and maintains scale through shale-driven throughput needs. Asia Pacific posts the fastest growth at estimated: 6.5% CAGR, 2024-2034, while Middle East & Africa grows at estimated: 4.0% CAGR, 2024-2034.

Competitive Landscape

The Global Crude Oil Flow Improvers Market is moderately consolidated, with the top five chemical and oilfield service companies controlling an estimated 38.0%–45.0% of 2025 market revenue. Competition is chemistry-driven and service-integrated, where formulation performance, field validation, and the ability to bundle flow assurance with production chemicals and digital monitoring systems shape market share more than pricing alone. Competitive intensity increased in 2025–2026 as operators prioritized integrated chemical programs and long-term service contracts, favoring suppliers with global field support and regulatory-compliant portfolios.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| BASF SE | Germany | Leader | Paraffin inhibitors, drag reducing agents, flow improver chemistries | Europe, North America, Asia | Expanded oilfield chemicals portfolio and sustainable formulations in 2025. |

| CLARIANT AG | Switzerland | Leader | Asphaltene inhibitors, pour point depressants, flow assurance chemicals | Europe, Middle East, Latin America | Strengthened production chemicals segment and Middle East presence in 2025. |

| BAKER HUGHES | US | Leader | Integrated flow assurance and production chemicals solutions | North America, Middle East, offshore global | Expanded digital production chemistry monitoring solutions in 2025. |

| SLB | US | Leader | Flow assurance, production chemistry, and digital optimization tools | Global, strong offshore footprint | Advanced integrated production systems and digital chemical management in 2025. |

| HALLIBURTON | US | Leader | Flow improvers, paraffin control, and production enhancement chemicals | North America, Middle East | Expanded production chemicals and well lifecycle services in 2025. |

| ECOLAB (NALCO WATER) | US | Challenger | Specialty chemicals for flow assurance and water treatment | North America, Europe, offshore | Enhanced digital water and flow management platforms in 2025. |

| SOLVAY | Belgium | Challenger | Specialty polymers and flow improver additives | Europe, Asia-Pacific | Focused on sustainable chemical solutions and energy sector applications in 2025. |

| DORF KETAL | India | Challenger | Specialty oilfield chemicals including flow improvers | Middle East, Asia-Pacific | Expanded manufacturing capacity and regional distribution in 2025. |

| KEMIRA | Finland | Niche Player | Chemical solutions for oilfield and industrial applications | Europe, North America | Strengthened oil & gas chemical portfolio and sustainability initiatives in 2025. |

| INNOSPEC INC. | US | Niche Player | Fuel additives and oilfield specialty chemicals | North America, Europe | Expanded specialty chemical offerings and global supply network in 2025. |

Summary Insight:

The market is shifting toward integrated flow assurance solutions combining chemistry, digital monitoring, and field services. Companies with strong R&D capabilities, global supply chains, and regulatory-compliant formulations are gaining share, while smaller players compete through niche chemistries and regional presence. Long-term contracts and performance-based chemical programs are expected to define competitive positioning through 2034.

By Type

As of 2025, paraffin inhibitors remain the largest product category within the crude oil flow improvers market, accounting for over 30% of global demand. Their widespread adoption reflects the persistent challenge of wax deposition in onshore and offshore pipelines, particularly in colder environments and long-distance transport systems. Operators prioritize these inhibitors to maintain flow continuity and reduce unplanned shutdowns linked to paraffin precipitation, which can raise operating costs by up to 20% if left unmanaged.

Asphaltene inhibitors represent the second-largest product group, supported by rising production of heavy and unconventional crude. These formulations help control asphaltene agglomeration that can impair reservoir permeability and pipeline integrity. Scale inhibitors and hydrate inhibitors also play a critical role, especially in offshore developments, where mineral scaling and hydrate formation pose safety and flow risks. Together, non-paraffin solutions account for roughly 45% of total product revenue, reflecting diversified chemical programs tailored to crude composition.

By 2030, suppliers increasingly focus on multi-functional formulations that address wax, scale, and asphaltene risks simultaneously. This shift improves chemical efficiency and lowers treatment frequency, supporting steady product-level growth at an estimated CAGR of 5% through the mid-2030s.

By Application

Extraction continues to dominate application demand in 2025, representing approximately 45% of market revenue. Flow improvers play a direct role at the wellhead and near-wellbore zones, where high viscosity and pressure differentials restrict crude mobility. Early-stage chemical treatment improves drawdown efficiency and supports higher recovery factors, especially in mature fields and shale reservoirs.

Pipeline transportation forms the second-largest application segment, driven by expanding cross-border and export infrastructure. Flow improvers reduce frictional losses and wax accumulation, enabling operators to move higher volumes without major capital upgrades. Refinery applications account for a smaller but stable share, where additives support feedstock handling and minimize fouling during pre-processing.

As upstream projects extend into deeper reservoirs and longer laterals, demand concentrates further at the extraction stage. This reinforces chemical usage early in the value chain, where intervention yields the highest operational return.

By End-Use

Upstream oil and gas operators represent the primary end-use group, accounting for more than half of global consumption in 2025. National oil companies and large independents deploy flow improvers to stabilize production profiles and manage complex crude blends. Midstream operators follow, using these chemicals to protect pipeline assets and sustain throughput reliability.

Downstream end users, including refineries and storage terminals, show moderate adoption. Their focus centers on handling variability in incoming crude quality rather than volume growth. Across all end-use segments, chemical spending remains closely linked to drilling activity and throughput utilization.

By Region

North America leads the global market with close to 30% revenue share in 2025, supported by shale production in the Permian, Eagle Ford, and Bakken basins. High drilling intensity and long pipeline networks sustain consistent demand for paraffin and asphaltene control solutions.

Asia Pacific is the fastest-growing region, posting an estimated CAGR of 6% through 2034. Growth is driven by offshore exploration, pipeline expansion, and rising crude output in China, India, and Southeast Asia. The Middle East and Africa record moderate growth, anchored by offshore developments and enhanced recovery projects, particularly in the Gulf region and West Africa. Europe and Latin America maintain steady demand, shaped by mature fields and infrastructure maintenance priorities.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Asphaltene Inhibitors

- Paraffin Inhibitors

- Hydrate Inhibitors

- Scale Inhibitors

By Application

- Transportation

- Extraction

- Refinery

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.0 B |

| Forecast Revenue (2034) | USD 3.2 B |

| CAGR (2025-2034) | 5.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Asphaltene Inhibitors, Paraffin Inhibitors, Hydrate Inhibitors, Scale Inhibitors), By Application, (Transportation, Extraction, Refinery) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Evonik Industries, Halliburton, Infineum, British Petroleum, Dorf Ketal Chemicals India Private Limited, Schlumberger, Lubrizol Specialty Products, Inc., National Oil Varco, BASF SE, Weatherford International, Total S.A., Nalco Champion, ExxonMobil, Clariant, Baker Hughes |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Extraction, Transportation, Refinery), By End-Use Industry (Upstream, Midstream, Downstream), Industry Segment Overview, Market Dynamics, Competitive Strategies, Key Players, Regional Insights, Trends & Forecast 2026–2034")

, By Application (Extraction, Transportation, Refinery), By End-Use Industry (Upstream, Midstream, Downstream), Industry Segment Overview, Market Dynamics, Competitive Strategies, Key Players, Regional Insights, Trends & Forecast 2026–2034")

, By Application (Extraction, Transportation, Refinery), By End-Use Industry (Upstream, Midstream, Downstream), Industry Segment Overview, Market Dynamics, Competitive Strategies, Key Players, Regional Insights, Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Crude Oil Flow Improvers Market?

The Global Crude Oil Flow Improvers Market was valued at USD 2.0 Billion in 2025, projected to hit USD 3.2 Billion by 2034, growing at a CAGR of 5.3% from 2026–2034, driven by rising upstream activity, heavy crude production, and demand for efficient flow assurance solutions.

Who are the major players in the Crude Oil Flow Improvers Market?

Evonik Industries, Halliburton, Infineum, British Petroleum, Dorf Ketal Chemicals India Private Limited, Schlumberger, Lubrizol Specialty Products, Inc., National Oil Varco, BASF SE, Weatherford International, Total S.A., Nalco Champion, ExxonMobil, Clariant, Baker Hughes

Which segments covered the Crude Oil Flow Improvers Market?

By Product, (Asphaltene Inhibitors, Paraffin Inhibitors, Hydrate Inhibitors, Scale Inhibitors), By Application, (Transportation, Extraction, Refinery)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Crude Oil Flow Improvers Market

Published Date : 25 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date