- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

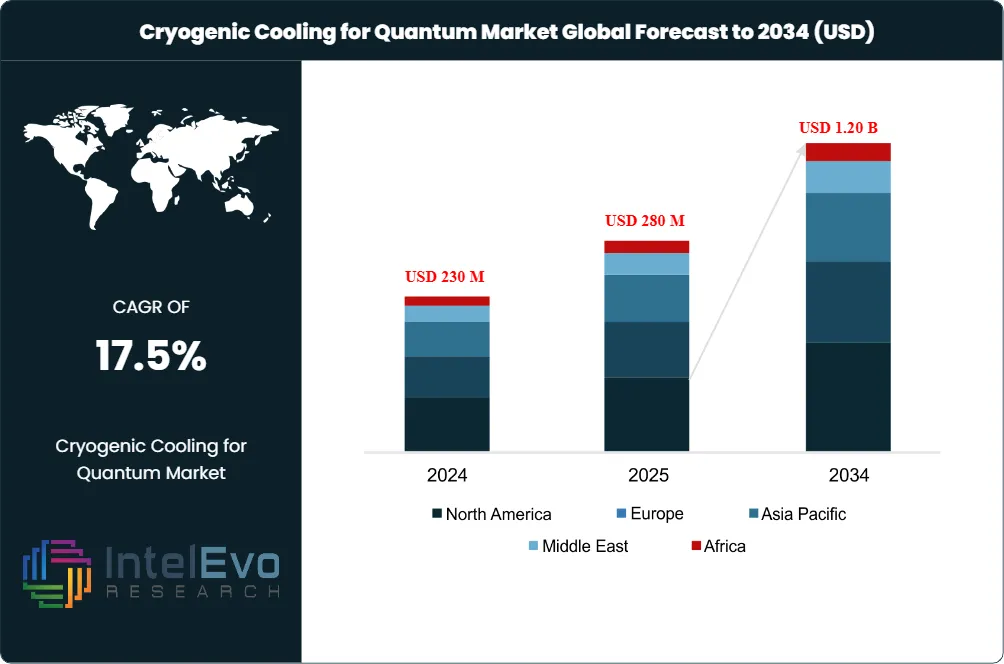

Global Cryogenic Cooling for Quantum Market Size, Share | CAGR 17.5%

Global Cryogenic Cooling for Quantum Market Size, Share Analysis By Product (Dilution, Cryocoolers, Pulse Tube, GM, Closed-Cycle, Temp Control), By Temp (Below 10mK, 10-20mK, 21-50mK, Above 50mK), By Application (Computing, Processors/Qubits, Communication, Cryptography, Sensing, Simulation), By End-User, By Architecture Region & Key Players-Industry Segment Overview, Market Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

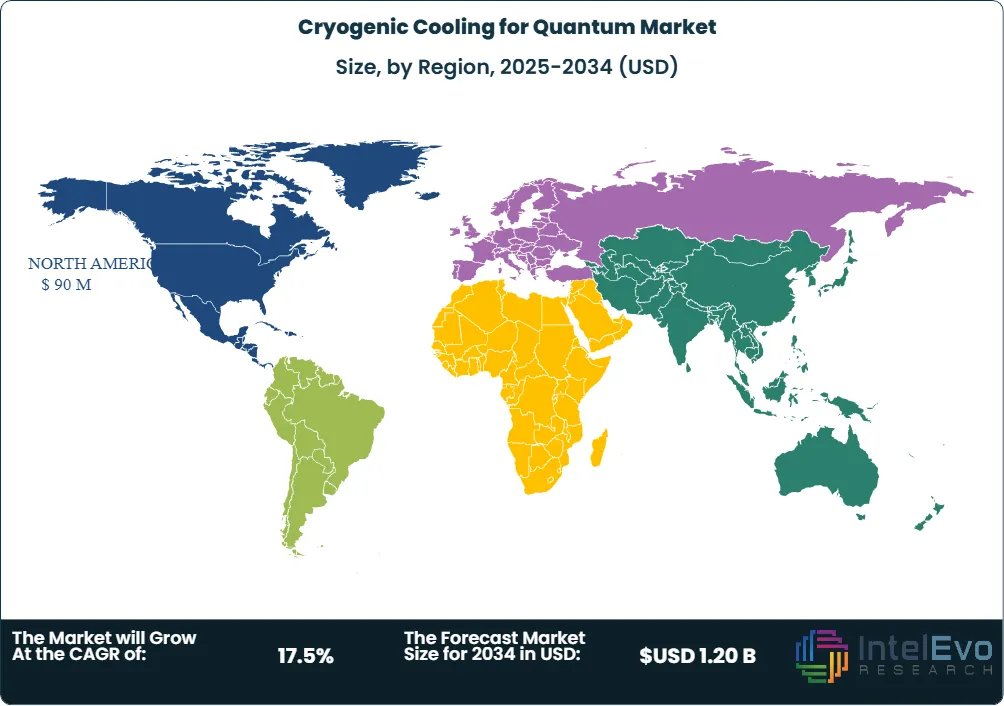

| USD 280 Million | USD 1.20 Billion | 17.5% | Europe, 38.0% |

The Cryogenic Cooling for Quantum Market was valued at USD 230 Million in 2024 and USD 280 Million in 2025. The market is projected to reach USD 1.20 Billion by 2034, expanding at a CAGR of 17.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 920 Million over the analysis period. Demand is driven by superconducting quantum processor scaling at IBM, Google, Rigetti, and AWS, sub-kelvin cryostat deployments in fundamental physics research, and accelerating commercial quantum data center construction at IBM Poughkeepsie and emerging hyperscaler facilities.

Get More Information about this report -

Request Free Sample ReportThe cryogenic cooling for quantum market is anchored by Bluefors XLD, LD, and KIDE platforms, Quantum Design Oxford Triton and Proteox dilution refrigerators, FormFactor HPD systems, Maybell Quantum Icebox, Leiden Cryogenics CF-CS81 series, and Air Liquide Cryoconcept HEXA platforms. Dilution refrigerators cool to millikelvin (mK) temperatures using helium-3 (He-3) and helium-4 (He-4) isotope mixtures, providing the operating environment for superconducting transmon qubits at IBM Heron R2, Google Willow 105-qubit, AWS Emerald 54-qubit, and Rigetti Ankaa-2 84-qubit processors. Quantum computing applications captured approximately 58 to 64% of dilution refrigerator demand in 2025.

Cryogen-free dry dilution refrigerators captured approximately 64% of the cryogenic cooling for quantum market in 2025, reaching roughly USD 169 Million in segment revenue, anchored by pulse-tube-cryocooler-based pre-cooling that eliminates liquid helium dependence. Wet dilution refrigerators retained 32% revenue share through scanning tunneling microscopy and vibration-sensitive applications. Pulse-tube coolers feature in approximately 56 to 58% of newly manufactured units, with low-vibration designs comprising 36% of recent purchases and modular configurations accounting for 38% of new product launches. Approximately 47% of new units in 2023 and 2024 were designed for sub-10 mK research, indicating deepening research penetration across superconducting and topological quantum computing platforms.

Europe led the cryogenic cooling for quantum market with approximately 38.0% revenue share in 2025, equivalent to roughly USD 106 Million in regional revenue, anchored by Bluefors (Helsinki, Finland), Quantum Design Oxford (Abingdon, UK), Leiden Cryogenics (Leiden, Netherlands), Air Liquide Cryoconcept (Sassenage, France), and ICEoxford (Witney, UK). North America captured 32% revenue share through FormFactor, Maybell Quantum, and Bluefors-Cryomech (Syracuse, NY operations). Asia Pacific captured 25% share with China at 25% pre-export-restriction declining due to 2023 embargo restrictions. March 2026's Bluefors Modular Cryogenic Platform launch and January 2026's Quantum Design acquisition of Oxford NanoScience redrew competitive positioning at year-end 2025 through Q1 2026.

Market Definition & Scope

The cryogenic cooling for quantum market is defined as the global commercial activity covering dilution refrigerators, pulse-tube cryocoolers, sub-kelvin cryostats, gas handling systems, vacuum chambers, and integrated cryogenic platforms purpose-built for quantum computing, fundamental physics research, and quantum sensor applications. The market includes cryogen-free dry dilution refrigerators (Bluefors XLD/LD/KIDE, Quantum Design Oxford Triton/Proteox, Leiden Cryogenics CF-CS81), wet dilution refrigerators using liquid helium pre-cooling, sub-kelvin adiabatic demagnetization refrigerators (ADRs), and emerging modular cryogenic platforms including Bluefors Modular Cryogenic Platform announced March 2026.

This analysis includes systems operating below 100 mK base temperature, with the dominant segment cooling below 10 mK for superconducting qubit operation. Excluded are general industrial cryogenic systems for medical MRI, liquid-natural-gas processing, and air-separation plants, classical helium-liquefaction equipment without quantum integration, and standalone pulse-tube cryocoolers without dilution refrigerator integration. The cryogenic cooling for quantum market sits within the broader quantum computing hardware parent market, capturing the cooling-infrastructure layer essential for superconducting and topological quantum processor operation alongside Compute Express Link (CXL) interconnects and microwave control electronics.

, By Temp (Below 10mK, 10-20mK, 21-50mK, Above 50mK), By Application (Computing, Processors/Qubits, Communication, Cryptography, Sensing, Simulation), By End-User, By Architecture Region & Key Players-Industry Segment Overview, Market Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The cryogenic cooling for quantum market grew from USD 280 Million in 2025 toward a forecast value of USD 1.20 Billion by 2034 at a 17.5% CAGR.

- Segment Dominance: Cryogen-free dry dilution refrigerators captured approximately 64% revenue share in 2025, anchored by Bluefors, Quantum Design Oxford, Leiden Cryogenics, and FormFactor pulse-tube-based platforms.

- Segment Dominance: Quantum computing applications held approximately 58 to 64% of 2025 demand, anchored by IBM, Google, AWS, Rigetti, and Origin Quantum superconducting processor cooling.

- Driver: Superconducting qubit count growth toward IBM Kookaburra 1,386-qubit per chip and 4,158-qubit multi-chip configurations through 2027 anchors sustained cooling-infrastructure demand.

- Restraint: Dilution refrigerator capital costs ranging USD 500,000 to USD 1.5 Million per unit and helium supply chain volatility constrain academic and SME adoption.

- Opportunity: Modular cryogenic platforms represent the largest forecast-period opportunity, with March 2026's Bluefors Modular Cryogenic Platform supporting hundreds of thousands of qubits per single platform.

- Trend: Sub-10 mK research penetration deepened in 2024 and 2025, with approximately 47% of newly introduced units designed for sub-10 mK research environments.

- Regional: Europe led with 38.0% share in 2025 equivalent to roughly USD 106 Million, while Asia Pacific captured 25% share constrained by 2023 China export restrictions.

Key Insights Summary

- Bluefors launched the Modular Cryogenic Platform in March 2026 at the APS Global Physics Summit in Denver, supporting hundreds of thousands of qubits per platform with first multi-module delivery scheduled for late 2026.

- Quantum Design completed acquisition of the Oxford NanoScience division of Oxford Instruments in January 2026, combining Triton dilution refrigerators with Quantum Design measurement options under the Quantum Design Oxford brand.

- Bluefors operates more than 1,800 systems globally with 18 years of quantum cooling experience, anchoring partnerships with IBM, Rigetti, Intel, and Google quantum-cooling deployments.

- IBM Project Goldeneye demonstrated the world's largest dilution refrigerator by experimental volume, requiring 10 times less lab space than current commercially available fridges to accommodate equivalent quantum hardware.

- IBM Quantum System Two deploys with the Bluefors KIDE cryogenic platform, a modular system designed to connect multiple processors together starting in 2025.

- Bluefors completed its acquisition of Cryomech (Syracuse, NY) in March 2023 expanding U.S. presence to nearly 600 employees across Finland, Germany, the Netherlands, and the United States.

- February 2025's Bluefors Ultra-Compact LD launch integrated the LD cryostat, Gas Handling System Generation 2, and pulse tube compressor into one space-efficient system with 8-14 dB lower sound levels than the standard Bluefors LD.

Competitive Landscape Overview

The cryogenic cooling for quantum market is highly consolidated, with the top three vendors (Bluefors, Quantum Design Oxford, and FormFactor) collectively representing an estimated 60 to 65% of 2025 revenue. Bluefors holds the dominant position with approximately 28% revenue share per industry analysis, anchored by 1,800-plus installations globally, the XLD and LD dilution refrigerator series, the KIDE modular platform supporting IBM Quantum System Two, and the March 2026 Modular Cryogenic Platform launch. Quantum Design Oxford (formed January 2026 through Quantum Design's acquisition of Oxford NanoScience) anchors the second-largest position through Triton, Proteox, and sub-kelvin cryostat-and-magnet integration.

Competitive evolution centers on three axes: scalability for hundreds-of-thousands-qubit deployments, modular architecture enabling incremental capacity expansion, and energy-and-helium-efficiency. FormFactor (formerly High Precision Devices, HPD) anchors the U.S. enterprise position. Maybell Quantum Industries' Icebox platform competes on density per cryostat. Leiden Cryogenics (Netherlands), Air Liquide Cryoconcept (France), ULVAC Cryogenics (Japan), Zero Point Cryogenics (Canada), ICEoxford (UK), and Cryomagnetics round out the competitive set. Strategic moves through 2025 included February 2025's Bluefors Ultra-Compact LD launch, June 2024's Bluefors-Oxford Instruments dispute resolution, January 2026's Quantum Design acquisition of Oxford NanoScience, and March 2026's Bluefors Modular Cryogenic Platform launch supporting fault-tolerant quantum computing.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Bluefors Oy | Finland | Leader | XLD, LD, KIDE, Modular Cryogenic Platform | Europe, North America, Asia Pacific | Mar 2026 launched Modular Cryogenic Platform |

| Quantum Design Oxford (Oxford NanoScience) | UK/USA | Leader | Triton, Proteox, sub-kelvin cryostats, magnets | Europe, North America | Jan 2026 Quantum Design acquired Oxford NanoScience |

| FormFactor Inc. | USA | Leader | FormFactor HPD dilution refrigerators, cryostats | North America | Continued quantum cryogenic expansion through 2025 |

| Maybell Quantum Industries | USA | Leader | Icebox dense quantum cryogenic platform | North America | 2025 expanded Icebox high-density qubit deployments |

| Leiden Cryogenics BV | Netherlands | Challenger | CF-CS81 series, MNK126-700, MK-series | Europe, North America | Continued European research-installation expansion |

| Air Liquide (Cryoconcept) | France | Challenger | HEXA, OPTIMA, sub-kelvin custom cryostats | Europe | Continued Cryoconcept integration through 2025 |

| ULVAC Cryogenics Inc. | Japan | Challenger | ULVAC dilution refrigerators, pulse-tube cryocoolers | Asia Pacific, North America | Continued Asia Pacific quantum infrastructure expansion |

| Zero Point Cryogenics | Canada | Niche Player | ZP-Series dilution refrigerators | North America | 2025 expanded enterprise Canadian quantum deployments |

| ICEoxford Ltd. | UK | Niche Player | DRY ICE dilution refrigerators, cryostats | Europe | Continued UK quantum research-base expansion |

| Origin Quantum / Hefei National Lab | China | Niche Player | Domestic dry-DR for Origin Wukong systems | Asia Pacific | 2025 expanded domestic dry-DR supply for Wuyuan cloud |

Segmentation Analysis

The cryogenic cooling for quantum market is segmented by product type, base temperature, application, end-user, and technology architecture, each producing distinct competitive and adoption patterns across the forecast period.

By Product Type

Cryogen-free dry dilution refrigerators (CFDR) captured approximately 64% of cryogenic cooling for quantum market revenue in 2025, equivalent to roughly USD 179 Million, anchored by pulse-tube-cryocooler-based pre-cooling that eliminates liquid helium consumption. Bluefors XLD/LD/KIDE, Quantum Design Oxford Triton/Proteox, FormFactor HPD, Maybell Quantum Icebox, Leiden Cryogenics CF-CS81, and ICEoxford DRY ICE anchor the CFDR segment. Wet dilution refrigerators (WDR) retained approximately 32% revenue share, dominated by extreme-vibration-sensitive applications including scanning tunneling microscopy (STM) and certain condensed-matter experiments. Adiabatic demagnetization refrigerators (ADRs) and other sub-kelvin systems represented the remaining 4% share.

By Base Temperature

Sub-10 mK base-temperature systems captured approximately 77% of cryogenic cooling for quantum market revenue in 2025, the dominant operating range for superconducting transmon qubits at IBM Heron R2, Google Willow, AWS Emerald, and Rigetti Ankaa-2 processors operating at approximately 25 mK. Approximately 47% of new dilution refrigerator units introduced in 2023 and 2024 were designed for sub-10 mK research, indicating continued shift toward fault-tolerant quantum computing operating ranges. Base-temperature 10-100 mK systems held approximately 21% revenue share, supporting nano-research and condensed-matter physics workloads. Above-100 mK systems represented the remaining 2% share.

By Application

Quantum computing applications captured approximately 58 to 64% of cryogenic cooling for quantum market revenue in 2025, equivalent to roughly USD 165 to 180 Million, anchored by IBM, Google, AWS, Rigetti, IonQ, Quantinuum, Origin Quantum, and Fujitsu-RIKEN superconducting and trapped-ion processor cooling. Astronomical observation held approximately 17% share, anchored by CMB-S4 and Simons Observatory cosmic-microwave-background detector cooling. Nano research and condensed-matter physics captured approximately 18% share at academic laboratories including Forschungszentrum Julich, RIKEN, and the U.S. Department of Energy National Laboratories. Low-temperature detection and other applications represented the remaining 7% share.

By End-User

Quantum computing companies and hyperscalers captured approximately 42% of cryogenic cooling for quantum market revenue in 2025, anchored by IBM Quantum, Google Quantum AI, AWS Center for Quantum Computing, Rigetti, IonQ, Quantinuum, Microsoft, Origin Quantum, and Fujitsu. National laboratories held approximately 28% share at U.S. Department of Energy NQISRC sites including Fermilab SQMS, Argonne, and Oak Ridge National Laboratory, alongside Forschungszentrum Julich, RIKEN, and the U.K. National Quantum Computing Centre. Academic and research universities captured 22% share at MIT, Caltech, Stanford, ETH Zurich, Delft University of Technology, and the University of Tokyo. Government and defense end-users including DARPA programs represented the remaining 8% share.

By Technology Architecture

Stand-alone fixed-volume dilution refrigerators captured approximately 78% of cryogenic cooling for quantum market revenue in 2025, anchored by traditional Bluefors XLD, Quantum Design Oxford Triton, and Leiden Cryogenics installations. Modular and expandable platforms represented approximately 12% emerging share, led by Bluefors KIDE supporting IBM Quantum System Two and the March 2026 Bluefors Modular Cryogenic Platform with first multi-module delivery in late 2026. Custom-engineered super-fridges including IBM Project Goldeneye captured 4% share for proof-of-concept large-volume systems. Integrated platforms with control electronics and cabling pre-installed represented the remaining 6% share. Modular architecture is forecast to grow fastest through 2030.

Regional Analysis

The global cryogenic cooling for quantum market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with European vendor concentration and accelerating North American hyperscaler procurement driving the geographic mix.

North America

North America captured approximately 32% of cryogenic cooling for quantum market revenue in 2025, equivalent to roughly USD 90 Million in regional revenue. The United States anchors regional supply through FormFactor (Beaverton, Oregon with HPD operations in Boulder, Colorado), Maybell Quantum Industries (Denver), and Bluefors-Cryomech (Syracuse, NY) with approximately one-third of Bluefors' global employees in New York State. Demand concentrates at IBM Yorktown Heights, Google Quantum AI Santa Barbara, AWS Center for Quantum Computing at Caltech, Rigetti Berkeley, SEEQC Elmsford, and U.S. Department of Energy National Laboratories. The U.S. National Quantum Initiative Act funded more than USD 1.2 Billion through fiscal year 2025. Canada anchors regional supply through Zero Point Cryogenics (Edmonton).

Europe

Europe led the cryogenic cooling for quantum market with 38.0% share in 2025, equivalent to roughly USD 106 Million in regional revenue. Finland anchors regional supply through Bluefors (Helsinki) operating with more than 1,800 installations globally. The United Kingdom anchors supply through Quantum Design Oxford (Abingdon, formerly Oxford NanoScience), ICEoxford (Witney), and the National Quantum Computing Centre. The Netherlands anchors supply through Leiden Cryogenics (Leiden) and demand at QuTech and Delft University of Technology. France contributes through Air Liquide Cryoconcept (Sassenage). Germany anchors demand through Forschungszentrum Julich's IBM Quantum System Two installation and Munich Quantum Valley. The European Union Quantum Flagship committed EUR 1 Billion over ten years.

Asia Pacific

Asia Pacific captured approximately 25% of cryogenic cooling for quantum market revenue in 2025, valued near USD 70 Million. Japan anchors regional supply through ULVAC Cryogenics (Yokohama) and Taiyo Nippon Sanso (Tokyo), with demand at Fujitsu-RIKEN's April 2025 256-qubit superconducting installation and the post-Fugaku roadmap. China anchors demand through Origin Quantum (Hefei), QuantumCTek, SpinQ Technology, and the Hefei National Laboratory, with market share constrained by post-2023 export-restriction limits on Western dilution refrigerator technology. India anchors emerging demand through QpiAI's April 2025 25-qubit launch. South Korea contributes through Samsung Electronics quantum-program investments. Australia contributes through the University of Sydney quantum research.

Latin America

Latin America accounted for approximately 3% of cryogenic cooling for quantum market revenue in 2025. Brazil leads regional adoption through the National Laboratory for Scientific Computing (LNCC) and emerging quantum-research programs at the University of Sao Paulo. Mexico contributes through CINVESTAV academic research and emerging quantum-pilot programs. Argentina, Chile, and Colombia represent emerging demand pockets supported by university research grants. Regional growth is constrained by limited cryogenic infrastructure, helium-supply-chain access, and dilution-refrigerator-import logistics.

Middle East & Africa

Middle East and Africa held approximately 2% of cryogenic cooling for quantum market revenue in 2025. The United Arab Emirates anchors regional demand through the Quantum Research Center at Technology Innovation Institute (Abu Dhabi). Saudi Arabia's KAUST quantum initiative drives secondary demand. Israel contributes through the Hebrew University of Jerusalem and Weizmann Institute of Science quantum research. South Africa contributes through the Centre for High Performance Computing. Vision 2030 funding supports gradual capacity additions through 2027.

Country Analysis

United States

The United States cryogenic cooling for quantum market reached approximately USD 80 Million in 2025, with country CAGR tracking near 18% through 2034. Demand concentrates at IBM Yorktown Heights, Google Quantum AI Santa Barbara, AWS Center for Quantum Computing at Caltech, Rigetti Berkeley, SEEQC Elmsford, and the U.S. Department of Energy National Quantum Information Science Research Centers including Fermilab SQMS, Argonne, Brookhaven, and Oak Ridge. Domestic supply concentrates at FormFactor HPD (Boulder, Colorado), Maybell Quantum Industries (Denver), and Bluefors-Cryomech (Syracuse, NY). The U.S. National Quantum Initiative Act and the CHIPS and Science Act allocated more than USD 1.2 Billion through fiscal year 2025.

Finland

Finland's cryogenic cooling for quantum market reached approximately USD 45 Million in 2025, the largest single-country market within Europe given Bluefors' Helsinki headquarters and global supply leadership, with country CAGR near 18% through 2034. Bluefors Oy operates with more than 1,800 installations globally across 18 years of quantum cooling experience, supplying IBM, Google, Rigetti, Intel, and AWS. IQM Quantum Computers (Espoo) anchors domestic quantum-system demand alongside academic research at Aalto University. The Finnish government's Business Finland and Academy of Finland support quantum-research grants. Finland's competitive moat rests on Helsinki-area cryogenic engineering talent and the March 2026 Modular Cryogenic Platform launch supporting fault-tolerant quantum computing infrastructure.

Germany

Germany's cryogenic cooling for quantum market reached approximately USD 30 Million in 2025, with country CAGR near 18% through 2034. The IBM Quantum System Two installation at Forschungszentrum Julich anchors regional cloud access and dilution refrigerator demand. Munich Quantum Valley, the Karlsruhe Institute of Technology, and the Max Planck Institute for Quantum Optics anchor academic-research demand. The Federal Ministry of Education and Research (BMBF) committed EUR 3 Billion through 2026 for quantum technology, with the Munich Quantum Valley initiative and the German Aerospace Center (DLR) Quantum Computing Initiative anchoring regional infrastructure. BMW, Volkswagen, Mercedes-Benz, BASF, and Deutsche Bank drive industrial demand through the IBM Quantum Network.

Japan

Japan's cryogenic cooling for quantum market reached approximately USD 40 Million in 2025, the largest single-country market within Asia Pacific with country CAGR near 19% through 2034. ULVAC Cryogenics (Yokohama) and Taiyo Nippon Sanso (Tokyo) anchor domestic vendor supply alongside imported Bluefors and Quantum Design Oxford systems. Demand concentrates at the Fujitsu-RIKEN April 2025 256-qubit superconducting quantum computer at the RIKEN Center for Computational Science campus in Kobe, with the post-Fugaku roadmap targeting 1,000 qubits by 2026. Toyota, Hitachi, NEC, Toshiba, and Mitsubishi Chemical Holdings drive industrial demand. The METI Q-LEAP program and Cabinet Office Moonshot Goal 6 target fault-tolerant quantum computing by 2050, with the Green Innovation Fund allocating JPY 2 Trillion through 2030.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Product Type

- Dilution Refrigerators

- Cryocoolers

- Pulse Tube Cryocoolers

- Gifford-McMahon (GM) Cryocoolers

- Closed-Cycle Cryogenic Systems

- Cryogenic Temperature Control Systems

- Cryogenic Vacuum Systems

- Cryogenic Measurement and Monitoring Systems

- Quantum Cooling Infrastructure Components

- Others

By Base Temperature

- Below 10 Millikelvin (mK)

- 10–20 Millikelvin (mK)

- 21–50 Millikelvin (mK)

- 51–100 Millikelvin (mK)

- 101 Millikelvin–1 Kelvin

- Above 1 Kelvin

- Others

By Application

- Quantum Computing Systems

- Quantum Processors and Qubits

- Quantum Communication

- Quantum Cryptography

- Quantum Sensing and Metrology

- Quantum Simulation

- Quantum Research and Development

- Superconducting Quantum Computing

- Trapped Ion Quantum Systems

- Photonic Quantum Systems

- Neutral Atom Quantum Systems

- Others

By End-User

- Quantum Computing Companies

- Research and Academic Institutions

- Government Research Laboratories

- National Quantum Initiatives and Agencies

- Semiconductor Manufacturers

- Telecommunications Companies

- Healthcare and Life Sciences Organizations

- Defense and Aerospace Organizations

- Technology Companies

- Industrial Research Organizations

- Others

By Technology Architecture

- Superconducting Quantum Architecture

- Trapped Ion Quantum Architecture

- Photonic Quantum Architecture

- Neutral Atom Quantum Architecture

- Spin Qubit Architecture

- Topological Quantum Architecture

- Quantum Annealing Systems

- Hybrid Quantum-Classical Architecture

- Silicon-Based Quantum Architecture

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 280 M |

| Forecast Revenue (2034) | USD 1.20 B |

| CAGR (2025-2034) | 17.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Dilution Refrigerators, Cryocoolers, Pulse Tube Cryocoolers, Gifford-McMahon (GM) Cryocoolers, Closed-Cycle Cryogenic Systems, Cryogenic Temperature Control Systems, Cryogenic Vacuum Systems, Cryogenic Measurement and Monitoring Systems, Quantum Cooling Infrastructure Components, Others), By Base Temperature, (Below 10 Millikelvin (mK), 10–20 Millikelvin (mK), 21–50 Millikelvin (mK), 51–100 Millikelvin (mK), 101 Millikelvin–1 Kelvin, Above 1 Kelvin, Others), By Application, (Quantum Computing Systems, Quantum Processors and Qubits, Quantum Communication, Quantum Cryptography, Quantum Sensing and Metrology, Quantum Simulation, Quantum Research and Development, Superconducting Quantum Computing, Trapped Ion Quantum Systems, Photonic Quantum Systems, Neutral Atom Quantum Systems, Others), By End-User, (Quantum Computing Companies, Research and Academic Institutions, Government Research Laboratories, National Quantum Initiatives and Agencies, Semiconductor Manufacturers, Telecommunications Companies, Healthcare and Life Sciences Organizations, Defense and Aerospace Organizations, Technology Companies, Industrial Research Organizations, Others), By Technology Architecture, (Superconducting Quantum Architecture, Trapped Ion Quantum Architecture, Photonic Quantum Architecture, Neutral Atom Quantum Architecture, Spin Qubit Architecture, Topological Quantum Architecture, Quantum Annealing Systems, Hybrid Quantum-Classical Architecture, Silicon-Based Quantum Architecture, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BLUEFORS OY, QUANTUM DESIGN OXFORD (OXFORD NANOSCIENCE), FORMFACTOR INC., MAYBELL QUANTUM INDUSTRIES, LEIDEN CRYOGENICS BV, AIR LIQUIDE (CRYOCONCEPT), ULVAC CRYOGENICS INC., ZERO POINT CRYOGENICS, ICEOXFORD LTD., QUANTUM DESIGN INC., TAIYO NIPPON SANSO CORPORATION, CRYOMAGNETICS INC., JANISULT, SHI CRYOGENICS GROUP, MONTANA INSTRUMENTS CORPORATION, MEYER TOOL & MANUFACTURING INC., BENYUAN QUANTUM TECHNOLOGY (HEFEI), PHYSIKE TECHNOLOGY, LAKE SHORE CRYOTRONICS INC., CRYOMECH INC. (BLUEFORS), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Temp (Below 10mK, 10-20mK, 21-50mK, Above 50mK), By Application (Computing, Processors/Qubits, Communication, Cryptography, Sensing, Simulation), By End-User, By Architecture Region & Key Players-Industry Segment Overview, Market Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Temp (Below 10mK, 10-20mK, 21-50mK, Above 50mK), By Application (Computing, Processors/Qubits, Communication, Cryptography, Sensing, Simulation), By End-User, By Architecture Region & Key Players-Industry Segment Overview, Market Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Temp (Below 10mK, 10-20mK, 21-50mK, Above 50mK), By Application (Computing, Processors/Qubits, Communication, Cryptography, Sensing, Simulation), By End-User, By Architecture Region & Key Players-Industry Segment Overview, Market Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Cryogenic Cooling for Quantum Market?

The Global Cryogenic Cooling for Quantum Market was valued at USD 230 Million in 2024 and USD 280 Million in 2025, and is projected to reach USD 1.20 Billion by 2034, growing at a CAGR of 17.5% from 2026 to 2034. Market growth is driven by quantum computing advancements, superconducting qubits, dilution refrigerators, and cryogenic cooling technologies.

Who are the major players in the Cryogenic Cooling for Quantum Market?

BLUEFORS OY, QUANTUM DESIGN OXFORD (OXFORD NANOSCIENCE), FORMFACTOR INC., MAYBELL QUANTUM INDUSTRIES, LEIDEN CRYOGENICS BV, AIR LIQUIDE (CRYOCONCEPT), ULVAC CRYOGENICS INC., ZERO POINT CRYOGENICS, ICEOXFORD LTD., QUANTUM DESIGN INC., TAIYO NIPPON SANSO CORPORATION, CRYOMAGNETICS INC., JANISULT, SHI CRYOGENICS GROUP, MONTANA INSTRUMENTS CORPORATION, MEYER TOOL & MANUFACTURING INC., BENYUAN QUANTUM TECHNOLOGY (HEFEI), PHYSIKE TECHNOLOGY, LAKE SHORE CRYOTRONICS INC., CRYOMECH INC. (BLUEFORS), Others

Which segments covered the Cryogenic Cooling for Quantum Market?

By Product Type, (Dilution Refrigerators, Cryocoolers, Pulse Tube Cryocoolers, Gifford-McMahon (GM) Cryocoolers, Closed-Cycle Cryogenic Systems, Cryogenic Temperature Control Systems, Cryogenic Vacuum Systems, Cryogenic Measurement and Monitoring Systems, Quantum Cooling Infrastructure Components, Others), By Base Temperature, (Below 10 Millikelvin (mK), 10–20 Millikelvin (mK), 21–50 Millikelvin (mK), 51–100 Millikelvin (mK), 101 Millikelvin–1 Kelvin, Above 1 Kelvin, Others), By Application, (Quantum Computing Systems, Quantum Processors and Qubits, Quantum Communication, Quantum Cryptography, Quantum Sensing and Metrology, Quantum Simulation, Quantum Research and Development, Superconducting Quantum Computing, Trapped Ion Quantum Systems, Photonic Quantum Systems, Neutral Atom Quantum Systems, Others), By End-User, (Quantum Computing Companies, Research and Academic Institutions, Government Research Laboratories, National Quantum Initiatives and Agencies, Semiconductor Manufacturers, Telecommunications Companies, Healthcare and Life Sciences Organizations, Defense and Aerospace Organizations, Technology Companies, Industrial Research Organizations, Others), By Technology Architecture, (Superconducting Quantum Architecture, Trapped Ion Quantum Architecture, Photonic Quantum Architecture, Neutral Atom Quantum Architecture, Spin Qubit Architecture, Topological Quantum Architecture, Quantum Annealing Systems, Hybrid Quantum-Classical Architecture, Silicon-Based Quantum Architecture, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Cryogenic Cooling for Quantum Market

Published Date : 20 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date