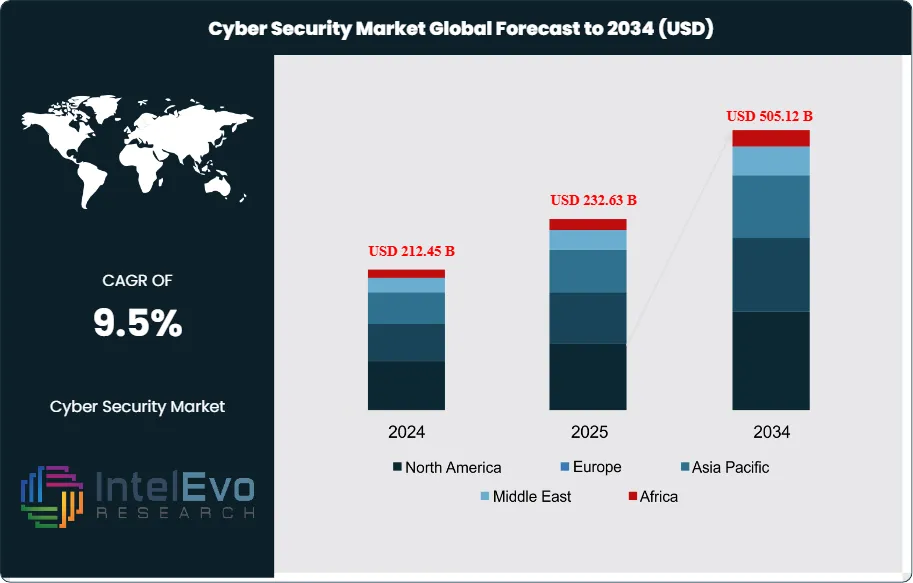

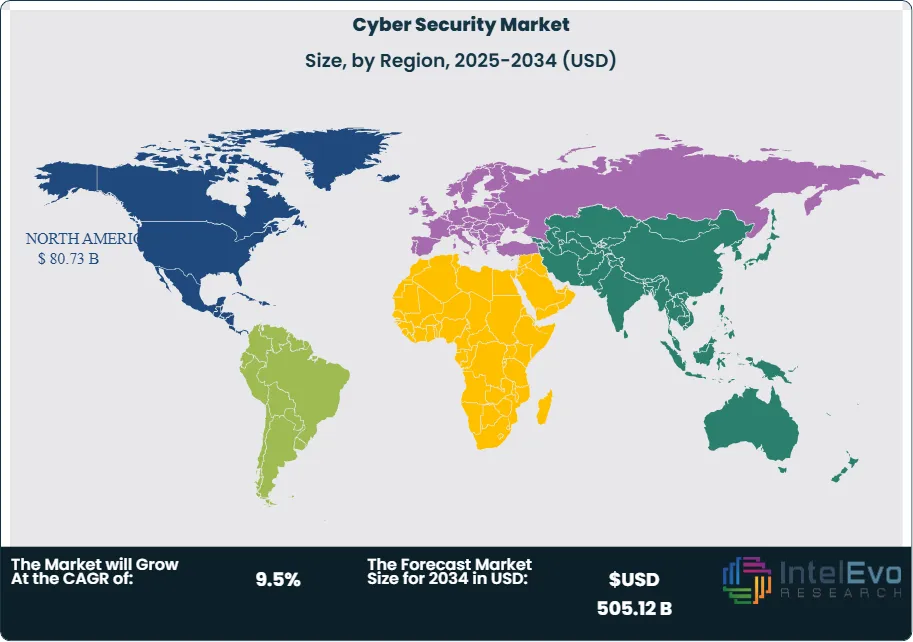

The Cyber Security Market is projected to be worth over USD 505.12 billion by 2034, up from approximately USD 212.45 billion in 2024, growing at a CAGR of 9.5% during the forecast period from 2024 to 2034. The global cyber security market encompasses a comprehensive suite of solutions, services, and advisory offerings designed to protect organizations’ digital assets, networks, and data from unauthorized access, cyberattacks, and information breaches.

This market represents one of the most critical and rapidly expanding segments within the broader technology and risk management industries, accounting for a significant and growing share of global IT and compliance spending. The cyber security ecosystem includes a diverse range of disciplines, from network and endpoint protection to cloud security, identity and access management, application security, and advanced threat intelligence. These solutions and services are deployed across all industries and organization sizes, reflecting the universal and escalating nature of cyber risk in the digital era.

Cyber security providers and consulting firms play a pivotal role in identifying vulnerabilities, analyzing complex threat landscapes, and leveraging their expertise to design and implement robust defense strategies. Their work enhances organizational resilience, ensures regulatory compliance, and safeguards competitive positioning in an increasingly interconnected world. The market’s growth is underpinned by the relentless pace of digital transformation, the proliferation of connected devices, and the rising sophistication of cyber threats. Key growth catalysts include the integration of artificial intelligence, machine learning, and automation into security platforms, enabling real-time threat detection, predictive analytics, and rapid incident response. The market also benefits from the expanding adoption of cloud computing, remote work, and digital-first business models, all of which require new approaches to securing distributed environments.

North America dominates the global cyber security market, a leadership position driven by the concentration of major technology vendors, advanced digital infrastructure, and stringent regulatory frameworks that mandate high levels of security and compliance. The region’s dominance is reinforced by the presence of leading cyber security firms, a mature enterprise client base, and a dynamic innovation ecosystem that continually drives the adoption of next-generation security solutions. Asia-Pacific represents the fastest-growing regional market, with a significant projected CAGR, fueled by rapid digitalization, expanding internet penetration, and increasing investments in cyber defense by both governments and private enterprises. The region’s growth is further supported by the rise of mobile-first economies, large-scale infrastructure projects, and a growing awareness of cyber risk among businesses of all sizes.

The COVID-19 pandemic fundamentally accelerated the adoption of cyber security solutions as organizations faced unprecedented operational disruptions, a surge in cyberattacks, and the urgent need to secure remote workforces. The crisis created immediate demand for endpoint protection, secure cloud access, and incident response services, as companies rapidly shifted to digital operations and remote collaboration. While initial economic uncertainty led some organizations to delay security investments, the long-term impact has been overwhelmingly positive, with cyber security now recognized as a core pillar of business continuity, digital trust, and organizational resilience.

Rising geopolitical tensions, state-sponsored cyberattacks, and the weaponization of digital infrastructure have significantly influenced cyber security demand patterns, creating opportunities for advanced threat intelligence, critical infrastructure protection, and government-led cyber defense initiatives. International regulations, data privacy laws, and cross-border data transfer restrictions have driven demand for specialized compliance solutions, risk assessment services, and advisory expertise in navigating complex regulatory environments. Additionally, the increasing emphasis on supply chain security and digital sovereignty has created substantial opportunities for cyber security providers specializing in third-party risk management, secure software development, and business continuity planning that address evolving global threats.

Key Takeaways

MarketGrowth: The Global Cyber Security Market is expected to reach over USD 500 billion by 2034, fueled by digital transformation, cloud adoption, and the escalating threat landscape.

SolutionTypeDominance: Network security and cloud security lead market share due to the need for perimeter defense and secure digital transformation.

EnterpriseSizeDominance: Large enterprises dominate, driven by complex operational requirements, regulatory obligations, and substantial security budgets.

DeliveryModelDominance: Managed Security Services (MSS) and cloud-based security solutions are the fastest-growing delivery models, offering scalability and 24/7 protection.

Industry Vertical Dominance: BFSI, healthcare, and government sectors hold the largest shares, owing to regulatory complexity, sensitive data, and critical infrastructure protection needs.

Driver: Key drivers accelerating growth include digital transformation, regulatory compliance, and the increasing sophistication of cyber threats.

Restraint: Growth is hindered by a global talent shortage, integration complexity, and rising costs of advanced security solutions.

Opportunity: The market is poised for expansion due to opportunities like AI-powered security, zero trust architecture, and emerging market penetration.

Trend: Emerging trends including XDR (Extended Detection and Response), quantum-safe cryptography, and supply chain security are reshaping the market.

Regional Analysis: North America leads due to technology concentration and regulatory maturity. Asia-Pacific shows high promise due to rapid digitalization and government investment.

Solution Type Analysis:

Network Security remains foundational, encompassing firewalls, intrusion detection/prevention systems (IDS/IPS), and network segmentation. The segment is evolving with next-generation firewalls (NGFWs) and network traffic analytics to address encrypted traffic and advanced persistent threats (APTs). Cloud Security is the fastest-growing segment, driven by the migration of workloads to public, private, and hybrid clouds. Solutions such as Cloud Security Posture Management (CSPM), Cloud Access Security Brokers (CASB), and cloud workload protection platforms (CWPP) are critical for visibility, compliance, and threat protection in cloud environments. Endpoint Security is essential for protecting distributed devices, especially in remote and hybrid work settings. Modern endpoint protection platforms (EPP) and endpoint detection and response (EDR) solutions leverage AI and behavioral analytics to detect and respond to threats in real time. Identity and Access Management (IAM) is central to zero trust strategies, providing single sign-on (SSO), multi-factor authentication (MFA), and privileged access management (PAM) to control user access and prevent unauthorized activities. Application Security addresses vulnerabilities in software development and deployment, with solutions such as web application firewalls (WAF), runtime application self-protection (RASP), and DevSecOps practices. Security Operations and Threat Intelligence are increasingly automated, with Security Information and Event Management (SIEM), Security Orchestration, Automation, and Response (SOAR), and threat intelligence platforms enabling rapid detection, investigation, and response.

Enterprise Size Analysis:

Large Enterprises maintain a commanding position in the cyber security market, driven by complex operational demands, global footprints, and significant regulatory obligations. These organizations face multifaceted challenges, including protecting sensitive data, ensuring compliance across jurisdictions, and defending against targeted attacks. Their market dominance is reinforced by the ability to invest in advanced security architectures, build in-house security operations centers (SOCs), and engage with leading vendors for bespoke solutions. Small and Medium Enterprises (SMEs) are increasingly adopting cyber security solutions, motivated by the growing threat of ransomware, supply chain attacks, and regulatory requirements. Cloud-based and managed security services are particularly attractive to SMEs, offering enterprise-grade protection without the need for large in-house teams.

Delivery Model Analysis:

Managed Security Services (MSS) and cloud-based security solutions are experiencing exceptional growth, reflecting a shift toward scalable, cost-efficient, and globally accessible protection. MSS providers offer 24/7 monitoring, threat intelligence, and incident response, making advanced security accessible to organizations of all sizes. On-premises solutions persist in highly regulated industries and regions with strict data residency requirements, offering greater control but at higher cost and complexity. Hybrid models are emerging, combining on-premises and cloud-based security to balance control, scalability, and compliance.

Industry Vertical Analysis:

BFSI (Banking, Financial Services, and Insurance) leads the cyber security market, accounting for over 25% of total spending. The sector’s exposure to financial crime, regulatory scrutiny, and digital transformation drives demand for advanced security, fraud detection, and compliance solutions. Healthcare is a high-growth vertical, facing unique challenges in protecting patient data, complying with regulations (e.g., HIPAA), and securing telehealth platforms. Ransomware attacks and data breaches have made cyber security a top priority for healthcare providers. Government and Critical Infrastructure are prime targets for nation-state actors and cyber terrorists. Investment in cyber defense, threat intelligence, and incident response is critical to national security and public safety. Retail and E-Commerce face persistent threats from payment card fraud, account takeover, and supply chain attacks. The adoption of omnichannel engagement and digital payment systems necessitates robust data protection and fraud prevention. Manufacturing and Industrial sectors are increasingly targeted as IT and operational technology (OT) converge. Securing industrial control systems (ICS) and supply chains is essential to prevent disruptions and ensure safety.

Region Analysis:

North America holds a commanding position in the global cyber security market, driven by a concentration of technology vendors, advanced infrastructure, and regulatory maturity. The United States leads in innovation, investment, and cyber security talent. Asia-Pacific is the fastest-growing regional market, propelled by rapid digitalization, expanding internet access, and government-led cyber security initiatives. Major economies such as China, India, Japan, and Australia are investing heavily in cyber defense and regulatory frameworks. Europe maintains a substantial presence, characterized by mature digital markets, complex regulatory environments (e.g., GDPR), and a strong focus on data privacy and critical infrastructure protection. Latin America, Middle East, and Africa are emerging markets with growing awareness and investment in cyber security, driven by digital transformation, regulatory developments, and increasing cyber threats.

Service Type (Network Security, Endpoint Security, Cloud Security, Identity and Access Management (IAM), Application Security, Security Operations and Threat Intelligence, Managed Security Services (MSS), Consulting and Advisory Services), Enterprise Size (Small & Medium Enterprises (SMEs), Large Enterprises), Delivery Model (On-premises Security, Cloud-based Security, Hybrid Security, Managed Security Services (MSS)), Industry Vertical (BFSI, Healthcare, Government, Retail & E-Commerce, Manufacturing & Industrial, IT & Telecom, Energy & Utilities)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Palo Alto Networks, Cisco Systems, Fortinet, CrowdStrike, Check Point Software Technologies, Microsoft, IBM Security, Trend Micro, Symantec (Broadcom), McAfee

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA CYBER SECURITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA CYBER SECURITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA CYBER SECURITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL CYBER SECURITY CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis:

Palo Alto Networks: Palo Alto Networks stands as a global leader in cyber security, renowned for its next-generation firewalls, advanced threat intelligence, and integrated security platforms. The company’s competitive advantage lies in its continuous innovation—particularly in cloud security, AI-driven threat detection, and automation. Palo Alto’s Prisma Cloud and Cortex XDR platforms are widely adopted for securing hybrid and multi-cloud environments, while its Unit 42 threat intelligence division provides cutting-edge research and rapid response to emerging threats. The company’s global reach, robust partner ecosystem, and commitment to R&D ensure it remains at the forefront of defending enterprises against sophisticated cyberattacks.

Cisco Systems: Cisco is a dominant force in network security, offering a comprehensive portfolio that spans firewalls, intrusion prevention, secure access, and cloud security. Cisco’s competitive strength is rooted in its ability to integrate security across networking, data center, and collaboration platforms, providing end-to-end protection for organizations of all sizes. The company’s SecureX platform unifies visibility and automation, while its Talos Intelligence Group delivers real-time threat intelligence. Cisco’s global presence, trusted brand, and focus on secure connectivity make it a preferred partner for enterprises navigating digital transformation and remote work challenges.

Fortinet: Fortinet is recognized for its high-performance security fabric, which integrates firewalls, endpoint protection, SD-WAN, and cloud security into a unified platform. The company’s FortiGate appliances are industry benchmarks for speed and reliability, while its Security Fabric architecture enables seamless policy enforcement across complex environments. Fortinet’s competitive edge comes from its custom ASIC technology, broad product portfolio, and ability to deliver scalable, cost-effective solutions for both large enterprises and SMEs. The company’s focus on automation and AI-driven threat detection positions it as a leader in the evolving cyber security landscape.

CrowdStrike: CrowdStrike has revolutionized endpoint security with its cloud-native Falcon platform, which leverages AI and behavioral analytics for real-time threat detection and response. The company’s strength lies in its rapid deployment, scalability, and ability to protect distributed workforces. CrowdStrike’s threat intelligence and managed detection and response (MDR) services are highly regarded, making it a go-to provider for organizations seeking proactive defense against ransomware, nation-state attacks, and advanced persistent threats. Its continuous innovation in XDR (Extended Detection and Response) and partnerships with leading cloud providers reinforce its market leadership.

Check Point Software Technologies: Check Point is a pioneer in cyber security, known for its comprehensive threat prevention, cloud security, and mobile protection solutions. The company’s Infinity architecture delivers unified security management across networks, cloud, and endpoints, while its SandBlast technology provides advanced threat emulation and zero-day protection. Check Point’s competitive advantage is its focus on prevention-first strategies, robust research capabilities, and global support network. The company continues to expand its offerings through acquisitions and R&D, addressing emerging threats in IoT, cloud, and supply chain security.

Microsoft: Microsoft has rapidly emerged as a cyber security powerhouse, leveraging its Azure cloud platform, Defender suite, and integrated identity solutions. The company’s competitive strength is its ability to embed security across its vast ecosystem—spanning cloud, endpoint, identity, and productivity tools. Microsoft’s investment in AI-driven threat detection, security automation, and compliance solutions has made it a trusted partner for enterprises undergoing digital transformation. Its global threat intelligence, extensive telemetry, and seamless integration with business applications provide holistic protection for organizations worldwide.

IBM Security: IBM Security is a leader in security operations, threat intelligence, and managed security services. The company’s QRadar SIEM and SOAR platforms are widely adopted for incident detection, investigation, and response. IBM’s X-Force research team delivers deep threat analysis and rapid response capabilities, while its consulting arm helps organizations design and implement robust security architectures. IBM’s focus on AI, automation, and hybrid cloud security enables it to address the complex needs of large enterprises and regulated industries.

Market Key Players

Palo Alto Networks

Cisco Systems

Fortinet

CrowdStrike

Check Point Software Technologies

Microsoft

IBM Security

Trend Micro

Symantec (Broadcom)

McAfee

Driver:

Digital Transformation and Expanding Attack Surface:

The accelerating pace of digital transformation across all industries is the primary growth driver for the global cyber security market. As organizations migrate to cloud platforms, adopt IoT devices, and enable remote or hybrid workforces, their digital footprints expand dramatically. This creates unprecedented demand for advanced cyber security solutions to protect sensitive data, ensure business continuity, and maintain customer trust. The complexity of integrating new technologies—such as AI, machine learning, and automation—into business operations further amplifies the need for robust security frameworks. Organizations are investing record budgets in cyber security modernization, with global spending projected to exceed $250 billion by 2026. This driver is reinforced by the shortage of internal cyber expertise and the existential risk posed by cyberattacks, making security a board-level priority and a fundamental requirement for digital business survival.

Regulatory Complexity and Compliance Requirements:

The growing complexity of global regulatory environments is a sustained driver for cyber security investment. Industries such as financial services, healthcare, and critical infrastructure face increasingly sophisticated data protection and privacy mandates (e.g., GDPR, CCPA, HIPAA, NIS2). These regulations require expert interpretation, implementation guidance, and ongoing compliance monitoring. The demand for compliance-driven security solutions is particularly acute in regions like the European Union and North America, where regulatory frameworks are most developed and penalties for non-compliance are severe. Organizations must not only implement technical controls but also develop proactive risk management strategies and maintain auditable records to navigate complex and frequently changing regulatory landscapes.

Restraints:

Talent Shortage and Workforce Capacity Constraints:

The global cyber security industry faces a critical talent shortage, with millions of unfilled positions worldwide. This shortage spans both experienced security architects and emerging talent with specialized skills in areas like cloud security, threat intelligence, and incident response. The talent gap constrains the ability of organizations to scale their security operations, maintain high standards, and respond to evolving threats. Competition from technology companies, managed security service providers, and alternative career paths exacerbates the challenge, driving up costs and attrition rates. While organizations are investing in recruitment, training, and automation, the fundamental supply-demand imbalance continues to pressure margins and delivery capacity.

Rising Costs and Budget Pressures:

The cost of acquiring, deploying, and maintaining advanced cyber security solutions is rising, driven by the need for continuous innovation, regulatory compliance, and skilled personnel. At the same time, organizations face increasing pressure to demonstrate the ROI of security investments and manage costs in the face of economic uncertainty. The commoditization of certain security services through automation and cloud-based delivery models can reduce billable hours for traditional services, forcing vendors to innovate and differentiate their offerings. Additionally, the democratization of security knowledge and the growth of in-house security teams challenge the traditional value proposition of external providers, requiring continuous adaptation and value demonstration.

Opportunities:

Artificial Intelligence and Advanced Analytics Integration:

The convergence of artificial intelligence and machine learning with cyber security creates substantial opportunities for next-generation defense capabilities. AI-powered security platforms can analyze vast datasets, detect anomalies, and automate threat response at unprecedented speed and scale. This enables organizations to move from reactive to proactive security postures, reducing dwell time and improving resilience. The opportunity extends to developing industry-specific AI models, automated incident response systems, and intelligent risk assessment tools that combine human expertise with machine intelligence. Vendors that successfully integrate AI capabilities can achieve significant competitive advantages through improved accuracy, faster response, and the ability to address complex, evolving threats.

Emerging Market Expansion and SME Security Solutions:

Developing regions across Asia-Pacific, Latin America, and Africa present significant growth opportunities, driven by rapid digitalization, increasing cyber risk awareness, and government-led security initiatives. These markets offer substantial untapped potential due to expanding entrepreneurial ecosystems, regulatory modernization, and growing demand for affordable, scalable security solutions among small and medium enterprises (SMEs). The opportunity includes developing cost-effective, cloud-based security services, local partnership strategies, and specialized offerings tailored to the unique needs of emerging markets, such as mobile-first security and digital leapfrogging strategies.

Trends:

Zero Trust Architecture and Identity-Centric Security:

The cyber security industry is undergoing a fundamental shift toward zero trust models, which require continuous verification of users, devices, and applications—regardless of location. This trend is driven by the dissolution of traditional network perimeters and the rise of remote work. Zero trust adoption encompasses identity and access management (IAM), micro-segmentation, and least-privilege access, enabling organizations to reduce the risk of lateral movement and data breaches. The approach is particularly relevant for cloud security, hybrid environments, and organizations with distributed workforces.

XDR, Automation, and Modular Security Platforms:

The market is experiencing rapid adoption of Extended Detection and Response (XDR) solutions, which unify threat detection and response across endpoints, networks, and cloud environments. This trend moves away from siloed, point solutions toward integrated, modular security platforms that provide holistic visibility and faster incident response. Automation and orchestration (SOAR) are streamlining security operations, reducing response times, and enabling organizations to scale their defenses efficiently. Modularization allows organizations to select and combine security capabilities as needed, providing flexibility, scalability, and cost predictability.

Supply Chain Security and Third-Party Risk Management:

High-profile supply chain attacks have underscored the need for comprehensive third-party risk management and continuous monitoring of vendor ecosystems. Organizations are investing in secure software development practices, software bill of materials (SBOM), and advanced threat intelligence to mitigate risks associated with external partners and suppliers.

Privacy-Enhancing Technologies and Quantum-Safe Cryptography:

With data privacy regulations tightening and quantum computing on the horizon, organizations are adopting privacy-enhancing technologies (PETs) such as encryption, tokenization, and secure multi-party computation. Research and development in quantum-resistant cryptography are accelerating, preparing the industry for the next wave of security challenges.

Recent Developments:

In June 2025: Palo Alto Networks announced the launch of its Quantum-Safe Security Suite, a pioneering set of encryption and threat prevention tools designed to protect cloud and enterprise environments against future quantum computing threats. This suite integrates seamlessly with Palo Alto’s Prisma Cloud and Cortex platforms, enabling organizations to future-proof their data security strategies as quantum computing capabilities advance.

In May 2025: Microsoft unveiled its Unified Security Management Platform, which brings together Microsoft Defender, Sentinel, and Entra under a single, AI-powered dashboard. This platform offers real-time threat intelligence, automated incident response, and compliance management for hybrid and multi-cloud environments, addressing the growing complexity of enterprise security operations.

In April 2025: CrowdStrike expanded its Falcon XDR platform with new AI-driven threat hunting and automated response features. The update leverages generative AI to identify sophisticated attack patterns and reduce response times, further strengthening CrowdStrike’s position in the extended detection and response (XDR) market.

In March 2025: Fortinet announced a strategic partnership with Google Cloud to deliver integrated Secure Access Service Edge (SASE) solutions. This collaboration aims to provide organizations with unified network and security management, optimized for remote and hybrid workforces, and enhanced protection against cloud-based threats.

In February 2025: Check Point Software Technologies introduced Infinity AI Copilot, an AI-powered assistant that automates threat analysis, policy recommendations, and incident response across Check Point’s Infinity security architecture. This innovation is designed to help security teams address talent shortages and manage increasingly complex threat landscapes.

In January 2025: IBM Security launched its Quantum-Ready Encryption Services, offering consulting and implementation support for organizations preparing for the post-quantum era. The service includes risk assessments, migration planning, and deployment of quantum-resistant cryptographic algorithms.

Frequently Asked Questions

How big is the Cyber Security Market?

Global cyber security market is expected to grow from USD 212.45 Bn in 2024 to over USD 505.12 Bn by 2034, expanding at a CAGR of 9.5%. Explore key drivers, and trends.

Who are the major players in the Cyber Security Market?

Palo Alto Networks, Cisco Systems, Fortinet, CrowdStrike, Check Point Software Technologies, Microsoft, IBM Security, Trend Micro, Symantec (Broadcom), McAfee

Which segments covered the Cyber Security Market?

Service Type (Network Security, Endpoint Security, Cloud Security, Identity and Access Management (IAM), Application Security, Security Operations and Threat Intelligence, Managed Security Services (MSS), Consulting and Advisory Services), Enterprise Size (Small & Medium Enterprises (SMEs), Large Enterprises), Delivery Model (On-premises Security, Cloud-based Security, Hybrid Security, Managed Security Services (MSS)), Industry Vertical (BFSI, Healthcare, Government, Retail & E-Commerce, Manufacturing & Industrial, IT & Telecom, Energy & Utilities)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, Enterprise Size (SMEs, Large Enterprises), Delivery Model (On-Premises, Cloud-Based, Hybrid, MSS), Industry Vertical (BFSI, Healthcare, Government, Retail & E-Commerce, Manufacturing, IT & Telecom, Energy & Utilities), Region & Key Players – Segment Overview, Market Dynamics, Trends & Forecast 2025–2034")

, Enterprise Size (SMEs, Large Enterprises), Delivery Model (On-Premises, Cloud-Based, Hybrid, MSS), Industry Vertical (BFSI, Healthcare, Government, Retail & E-Commerce, Manufacturing, IT & Telecom, Energy & Utilities), Region & Key Players – Segment Overview, Market Dynamics, Trends & Forecast 2025–2034")

, Enterprise Size (SMEs, Large Enterprises), Delivery Model (On-Premises, Cloud-Based, Hybrid, MSS), Industry Vertical (BFSI, Healthcare, Government, Retail & E-Commerce, Manufacturing, IT & Telecom, Energy & Utilities), Region & Key Players – Segment Overview, Market Dynamics, Trends & Forecast 2025–2034")

, Enterprise Size (SMEs, Large Enterprises), Delivery Model (On-Premises, Cloud-Based, Hybrid, MSS), Industry Vertical (BFSI, Healthcare, Government, Retail & E-Commerce, Manufacturing, IT & Telecom, Energy & Utilities), Region & Key Players – Segment Overview, Market Dynamics, Trends & Forecast 2025–2034")