- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Cyclic Olefin Polymer Market Size, Trends & Forecast 2034 | 6.5% CAGR

Global Cyclic Olefin Polymer Market Size, Share, Analysis Report By Type (Copolymers, Homopolymers), Process Type (Blow Molding, Extrusion, Injection Molding), End-user (Automotive, F&B, Chemicals, Packaging, Pharma, Electronics, Optical), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

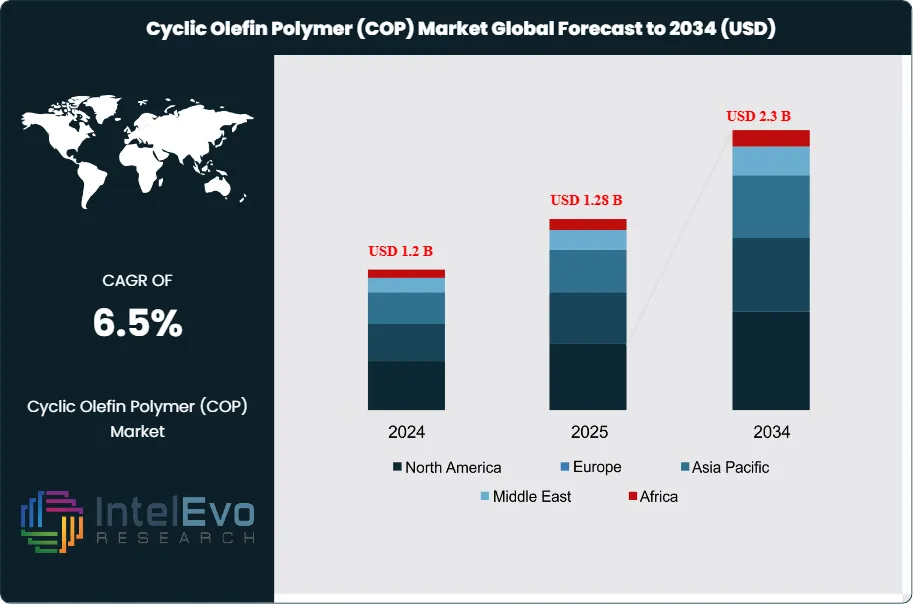

The Global Cyclic Olefin Polymer (COP) Market size is projected to reach approximately USD 2.3 billion by 2034, rising from USD 1.2 billion in 2024, growing at a CAGR of 6.5% during the forecast period from 2025 to 2034. The market growth is fueled by the increasing adoption of high-performance polymers in medical devices, optical components, and packaging applications due to their exceptional clarity, chemical resistance, and low moisture absorption. With industries shifting toward lightweight, recyclable materials, cyclic olefin polymers are emerging as the preferred alternative to traditional plastics across multiple sectors.

Get More Information about this report -

Request Free Sample ReportCyclic olefin polymer (COP) is a type of high-performance thermoplastic made from a combination of cyclic and linear olefins. Known for its excellent optical clarity, low moisture absorption, and high chemical resistance, COP is widely used in precision applications across industries such as healthcare, electronics, and packaging. In the medical field, COP is often chosen for diagnostic devices, drug delivery systems, and pharmaceutical packaging because it is biologically inert and can be sterilized without losing integrity. In electronics, its superior insulating properties make it ideal for use in displays and optical components. COP also provides a great barrier against moisture and gases, which makes it suitable for food and pharmaceutical packaging. Its strength, transparency, and ability to be molded with high precision give it an edge over traditional plastics like glass or PVC in applications requiring purity, clarity, and dimensional stability.

The cyclic olefin polymer (COP) market is witnessing steady growth, driven primarily by rising demand in the medical, pharmaceutical, and electronics sectors. Known for its excellent transparency, chemical resistance, and moisture barrier properties, COP is increasingly used in drug delivery systems, diagnostic devices, and sterile medical packaging. The material’s ability to withstand sterilization processes without degrading makes it ideal for sensitive healthcare applications. In addition, its use in high-end optical films, lenses, and electronic displays is expanding due to its clarity and dimensional stability. The packaging industry also benefits from COP’s non-reactive nature and superior barrier performance, making it suitable for preserving the integrity of pharmaceuticals and perishable goods. Technological advancements in polymer processing are further enhancing its capabilities, enabling wider adoption across precision industries. Regionally, Asia-Pacific leads in demand, supported by strong electronics manufacturing and growing healthcare infrastructure, while North America and Europe continue to drive innovation. As industries increasingly seek high-performance, sustainable materials, COP is positioned for continued market expansion.

The cyclic olefin polymer (COP) market in North America is experiencing steady growth, primarily driven by rising demand in sectors like pharmaceuticals, healthcare, and high-performance packaging. COP materials are increasingly used in medical applications such as drug delivery systems, diagnostic tools, and labware, thanks to their excellent clarity, high purity, and resistance to chemicals and moisture. These characteristics make them ideal for maintaining product integrity and meeting stringent regulatory standards.

The COVID-19 pandemic had a mixed impact on the cyclic olefin polymer (COP) market. Initially, the market experienced disruptions due to supply chain interruptions, workforce shortages, and slowed manufacturing activities across industries. However, the demand for COP surged in certain segments, particularly in medical and pharmaceutical applications. The polymer’s clarity, chemical resistance, and biocompatibility made it ideal for use in diagnostics, vials, syringes, and other healthcare products—critical during the pandemic.

, Process Type (Blow Molding, Extrusion, Injection Molding), End-user (Automotive, F&B, Chemicals, Packaging, Pharma, Electronics, Optical), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The cyclic olefin polymer market is expected to reach USD 2.3 billion by 2034, growing at a robust CAGR of 6.5%, indicating strong market expansion.

- Type Segment Dominance: The type segment is dominated by copolymers, accounting for over 58% of the market share. Copolymers are in high demand for their durability, clarity, and low moisture absorption, making them ideal for packaging that protects and preserves product quality.

- Process Type Segment Insights: Injection molding is anticipated to hold the largest market share. Injection molding is gaining popularity in the COP market due to the material's excellent clarity, low moisture absorption, and strong chemical resistance. These properties make COP ideal for producing precise, complex components in sectors like optics, medical devices, and packaging.

- Driver: The cyclic olefin polymer (COP) market is driven by rising demand in the medical and pharmaceutical sectors. COP’s excellent transparency, chemical resistance, and low moisture absorption make it ideal for drug packaging, syringes, and diagnostic devices—offering a safer, high-performance alternative to glass and conventional plastics.

- Restraint: A key restraint for the cyclic olefin polymer (COP) market is its high production cost compared to conventional plastics. This makes COP less accessible for price-sensitive applications, limiting its adoption primarily to specialized or high-end uses such as medical and optical industries.

- Opportunity: The cyclic olefin polymer (COP) market is seeing strong opportunity in medical and packaging applications due to its clarity, biocompatibility, and chemical resistance. Growing use in diagnostics, drug delivery, and optical components is driving demand, especially with the push for safer, high-performance materials.

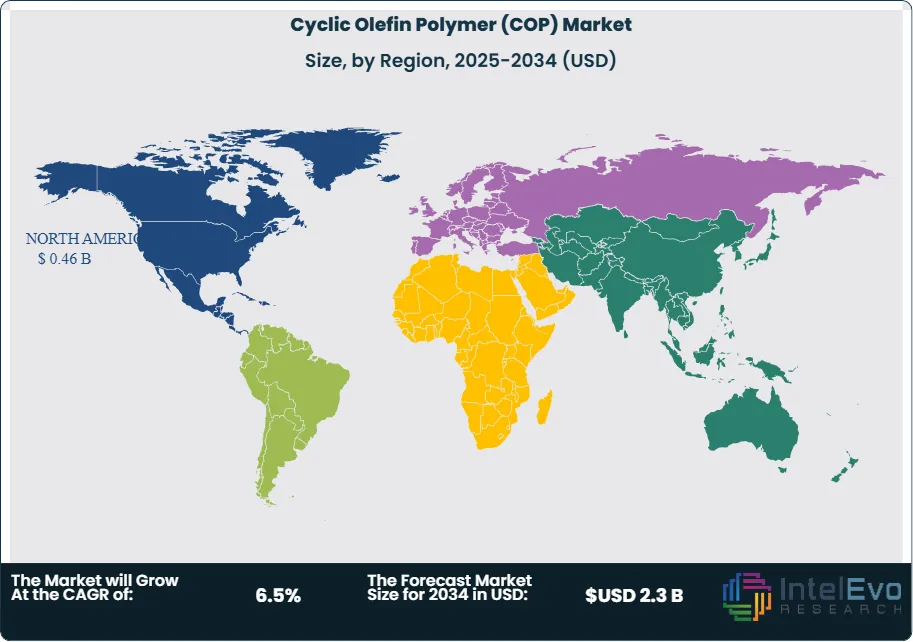

- Trend: The COP market is expanding globally, with manufacturers looking to tap into emerging markets in Asia-Pacific, Latin America, and the Middle East. Rapid industrialization and increasing consumer demand in these regions offer growth opportunities for COP manufacturers.

- Regional Analysis: The North American cyclic olefin polymer (COP) market is growing due to rising demand in healthcare, diagnostics, and electronics. COP's clarity, chemical resistance, and biocompatibility make it ideal for medical packaging and optical applications. The region’s strong pharmaceutical and tech sectors, along with a focus on high-performance materials, are driving this growth despite higher costs.

Type Analysis:

The type segment is divided into copolymers and homopolymers. The copolymers segment dominated the market, with a market share of around 58% accounting for 0.6 billion 2024. Copolymers are witnessing strong demand due to their unique combination of properties such as high chemical resistance, low moisture absorption, and excellent clarity. These features make them particularly valuable in the packaging sector, where maintaining product freshness and protecting sensitive contents are top priorities. Their ability to enhance shelf life and ensure product stability has positioned copolymers as a preferred material choice across food, pharmaceutical, and consumer goods packaging applications.

Process Type Analysis:

The process type segment is divided into blow molding, extrusion, and injection molding. The injection molding segment dominated the market, with a market share of around 40% accounting for 0.4 billion 2024. Injection molding is a widely used manufacturing process that allows for the mass production of complex and highly detailed plastic parts with precision and consistency. In the context of Cyclic Olefin Polymers (COP), this method is becoming increasingly popular because COP possesses unique properties that align well with the technical demands of modern applications.

End-user Analysis:

The end-user segment is divided into automotive, F&B, chemicals, packaging, pharma, electronics, and optical. The pharma segment dominated the market, with a market share of around 21% accounting for 0.2 billion 2024. Cyclic olefin polymer (COP) has become a favored material in the pharmaceutical industry, particularly for drug delivery systems and packaging, thanks to its outstanding transparency, low extractables, and excellent chemical resistance. Its inert properties make it ideal for sensitive applications like pre-filled syringes, vials, and blister packs, where maintaining drug purity is essential. As regulatory standards tighten and the pharmaceutical sector continues to grow globally, the demand for high-quality, reliable packaging materials like COP is rising. Its ability to preserve the stability and safety of medications makes it a go-to solution for manufacturers aiming to meet stringent quality requirements.

Region Analysis:

North America Leads With 38% Market Share in the Cyclic Olefin Polymer Market. The cyclic olefin polymer (COP) market in North America is witnessing significant growth, driven primarily by its expanding use in high-end applications such as healthcare, diagnostics, electronics, and premium packaging. COP is a unique class of polymer known for its excellent optical clarity, high chemical resistance, low moisture absorption, and superior dimensional stability. These attributes make it especially valuable in medical and pharmaceutical industries where material purity and performance are critical. The electronics and optics industries in North America are also adopting COP for its outstanding transparency, low birefringence, and heat resistance—ideal for use in camera lenses, optical films, and display components. As technological innovation progresses in consumer electronics and automotive displays, the demand for such materials continues to rise. Furthermore, the North American market benefits from a well-established pharmaceutical and medical device manufacturing base, advanced research facilities, and growing investments in healthcare infrastructure, particularly in the U.S. While the higher cost of COP compared to conventional polymers remains a barrier, its long-term advantages in performance and safety continue to drive its adoption across critical sectors.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Type

- Copolymers

- Homopolymers

By Product Type

- COP Films

- COP Sheets & Plates

- COP Tubes & Rods

- COP Pellets & Resins

- Others (Customized COP Products)

By Process Type

- Blow Molding

- Extrusion

- Injection Molding

By Application

- Medical Devices & Healthcare

- Packaging (Food & Beverages, Pharmaceuticals)

- Optical Components (Lenses, Displays)

- Electronics & Electrical

- Automotive Components

- Others (Consumer Goods, Industrial Applications)

By End-User Industry

- Healthcare & Medical

- Food & Beverage

- Electronics & Optical Devices

- Automotive

- Industrial & Manufacturing

- Others

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.28 B |

| Forecast Revenue (2034) | USD 2.3 B |

| CAGR (2025-2034) | 6.5% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Copolymers, Homopolymers), By Product Type (COP Films, COP Sheets & Plates, COP Tubes & Rods, COP Pellets & Resins, Others (Customized COP Products)), By Process Type (Blow Molding, Extrusion, Injection Molding), By Application (Medical Devices & Healthcare, Packaging (Food & Beverages, Pharmaceuticals), Optical Components (Lenses, Displays), Electronics & Electrical, Automotive Components, Others (Consumer Goods, Industrial Applications)), By End-User Industry (Healthcare & Medical, Food & Beverage, Electronics & Optical Devices, Automotive, Industrial & Manufacturing, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Borealis Group, MITSUI & CO. Ltd, Polysciences, Inc., Lyondellbasell Industries Holdings B.V., VELOX GmbH, Zeon Corporation, Topas Advanced Polymers, Inc., JSR Corporation, Entec Polymers, Ravago Group, Dow Chemical Company, INEOS Group, Idemitsu Kosan, SCHOTT, Sumitomo Chemical, Sk Chemicals |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Process Type (Blow Molding, Extrusion, Injection Molding), End-user (Automotive, F&B, Chemicals, Packaging, Pharma, Electronics, Optical), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Process Type (Blow Molding, Extrusion, Injection Molding), End-user (Automotive, F&B, Chemicals, Packaging, Pharma, Electronics, Optical), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Process Type (Blow Molding, Extrusion, Injection Molding), End-user (Automotive, F&B, Chemicals, Packaging, Pharma, Electronics, Optical), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Cyclic Olefin Polymer Market

Published Date : 11 Jun 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date