- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Data Loss Prevention (DLP) Market Size, Share & Forecast | 24% CAGR

Global Data Loss Prevention (DLP) Market Size, Share & Analysis By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector) Industry Regions & Key Players – Cybersecurity Threat Landscape & Forecast 2025–2034

Report Overview

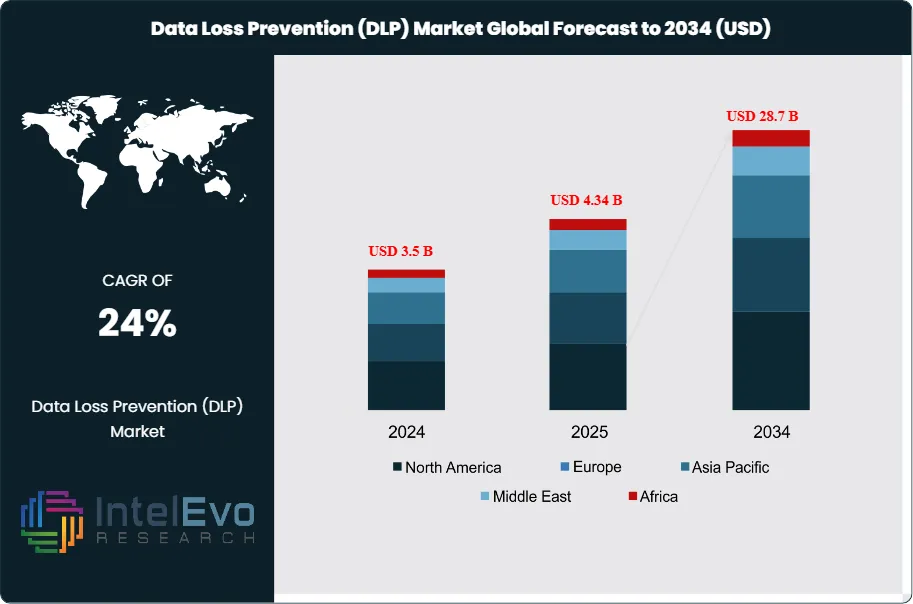

The Data Loss Prevention (DLP) Market, valued at USD 3.5 billion in 2024, is projected to reach USD 28.7 billion by 2034, growing at a CAGR of 24% from 2025 to 2034, driven by escalating cyber threats and regulatory compliance requirements, offering strategic opportunities for enterprises, governments, and technology providers. Data Loss Prevention solutions have become a cornerstone of modern cybersecurity strategies, enabling organizations to prevent sensitive data from being lost, misused, or accessed by unauthorized entities. By leveraging deep content inspection and contextual security analysis, DLP systems safeguard data in use, in transit, and at rest, ensuring compliance with evolving regulations while mitigating the risks of both accidental and malicious breaches. The rapid expansion of enterprise data volumes, alongside the widespread adoption of cloud services and remote work, has amplified vulnerabilities, making advanced DLP solutions essential for securing business-critical assets.

Get More Information about this report -

Request Free Sample ReportThe market’s growth trajectory is reinforced by the increasing sophistication of cyberattacks, coupled with the rising cost of breaches. Global enterprises face mounting financial, operational, and reputational risks, with average breach costs surpassing USD 3.8 million and disproportionately higher impacts in sectors such as healthcare and finance. Additionally, small and mid-sized enterprises remain particularly vulnerable, with data loss often resulting in business closure within months of an incident, underscoring the urgent need for scalable and cost-effective DLP deployments.

Technological advancements are further shaping market evolution. The integration of artificial intelligence (AI) and machine learning (ML) into DLP platforms is enhancing detection accuracy and adaptive response capabilities, enabling faster threat identification and mitigation. Moreover, convergence with adjacent security solutions—such as intrusion detection systems (IDS) and security information and event management (SIEM)—is fostering demand for holistic, integrated cybersecurity frameworks.

Regionally, North America leads the market, supported by stringent data privacy regulations, high digital adoption, and the prevalence of large enterprises with substantial security budgets. Europe follows, driven by GDPR compliance and heightened enterprise investments in risk management. Meanwhile, Asia-Pacific is emerging as a high-growth region, fueled by rapid digital transformation, rising internet penetration, and increasing government emphasis on data protection frameworks.

Overall, the Data Loss Prevention market represents a critical enabler of digital resilience. With escalating cyber risks, regulatory scrutiny, and the global shift toward cloud-driven ecosystems, investments in next-generation DLP solutions will be indispensable for organizations seeking to safeguard sensitive information and maintain trust in an increasingly data-centric economy.

Market Size, Share & Analysis By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector) Industry Regions & Key Players – Cybersecurity Threat Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Data Loss Prevention (DLP) market is projected to expand from USD 3.5 billion in 2024 to USD 28.7 billion by 2034, advancing at a CAGR of 24% (2025–2034). Growth is driven by rising cyber threats, regulatory compliance demands, and increasing data volumes across industries.

- Deployment Model: Cloud-based DLP solutions accounted for over 60.5% of the global market in 2023, reflecting the widespread shift toward cloud infrastructure and the need for real-time, scalable data security frameworks.

- Application Area: The storage/data center segment led the market with a 37.2% share in 2023, as organizations prioritize securing sensitive information housed in centralized systems vulnerable to breaches and insider threats.

- Enterprise Size: Large enterprises represented 58.4% of global demand in 2023, supported by higher security budgets, complex IT ecosystems, and stricter compliance obligations compared to SMEs.

- Solution Type: Encryption solutions captured 24.3% of the market share in 2023, underscoring the growing reliance on encryption technologies to protect data integrity and confidentiality across regulated sectors.

- Industry Vertical: The BFSI sector accounted for over 22% of market revenue in 2023, driven by stringent regulatory requirements, financial data sensitivity, and high vulnerability to cyberattacks.

- Driver: The expansion of remote work environments and the proliferation of cloud services have significantly increased the attack surface, fueling the adoption of DLP solutions to mitigate data exfiltration risks.

- Restraint: High implementation costs and integration challenges with legacy IT systems remain major barriers, particularly for small and medium-sized enterprises with limited cybersecurity budgets.

- Opportunity: Emerging markets in Asia-Pacific present strong growth potential, with rapid digital transformation, rising cybercrime incidents, and new government-backed data protection initiatives creating favorable conditions for DLP adoption.

- Trend: Integration of artificial intelligence (AI) and machine learning (ML) into DLP systems is enabling predictive analytics and adaptive security, positioning next-generation solutions as proactive defense tools.

- Regional Analysis: North America led the global market with a 36.9% share in 2023, supported by advanced cybersecurity infrastructure and regulatory enforcement, while Asia-Pacific is expected to register the fastest growth rate through 2033 due to escalating cloud adoption and heightened regulatory scrutiny.

Solution Analysis

In 2025, the Storage/Data Centre DLP segment continues to hold a commanding position, accounting for more than one-third of global revenues. This strength reflects the growing importance of securing vast volumes of structured and unstructured data stored across physical data centers and cloud repositories. As organizations migrate mission-critical workloads to digital platforms, data centers have become prime targets for increasingly sophisticated cyberattacks, driving heightened demand for advanced monitoring and prevention tools.

The dominance of this segment is also shaped by regulatory compliance requirements, with frameworks such as the EU’s GDPR, the U.S. CCPA, and sector-specific mandates enforcing strict safeguards for stored data. Enterprises are investing heavily in DLP systems that deliver visibility, real-time monitoring, and layered defense to mitigate unauthorized access risks. Looking ahead, the Storage/Data Centre DLP market is set to expand further as enterprises embrace digital-first operations, cloud-native ecosystems, and AI-enabled data protection strategies.

Deployment Mode Analysis

Cloud-based DLP solutions remain the fastest-growing deployment mode in 2025, holding more than 60% of market share. Their growth is fueled by the global shift toward cloud computing, SaaS adoption, and distributed workforces, where sensitive data is frequently accessed from multiple endpoints and networks. The scalability, cost-efficiency, and rapid deployment of cloud-native DLP systems give them a competitive advantage over traditional on-premise solutions.

Organizations are increasingly favoring cloud-based models because they provide continuous updates, vendor-managed compliance features, and seamless integration with collaboration tools such as Microsoft 365, Google Workspace, and Salesforce. With hybrid and remote work models now mainstream, the reliance on centralized, cloud-managed security solutions will intensify. This trajectory suggests cloud-based deployments will continue to dominate, especially as AI-driven and zero-trust architectures become integral to enterprise cybersecurity frameworks.

Organization Size Analysis

Large enterprises remain the primary consumers of DLP solutions in 2025, accounting for nearly 60% of global revenues. Their leadership stems from both scale and complexity: multinational corporations generate and process vast amounts of sensitive information across diverse geographies, business units, and digital infrastructures. With regulatory scrutiny intensifying across jurisdictions, large enterprises are compelled to invest in advanced, multi-layered DLP platforms that provide proactive threat detection, incident response, and compliance assurance.

The financial resources available to larger organizations further strengthen their ability to adopt end-to-end DLP systems. In contrast, while small and mid-sized enterprises (SMEs) represent a growing market, their adoption is constrained by budgetary pressures and limited in-house expertise. However, the rise of affordable, cloud-delivered DLP solutions tailored for SMEs indicates a growing opportunity in this segment over the medium term.

Application Analysis

Among DLP applications, Encryption leads with more than 23% market share in 2025. Its primacy reflects encryption’s critical role as a frontline defense against unauthorized data access in both storage and transmission environments. Regulatory frameworks such as HIPAA in the U.S. and GDPR in Europe mandate encryption for sensitive personal and financial information, cementing its importance in enterprise data protection strategies.

Encryption demand is also rising in tandem with the expansion of remote work, mobile business operations, and cloud adoption, where data is frequently transmitted across unsecured channels. Beyond encryption, applications such as email and web protection, incident response, and policy enforcement are gaining traction, with enterprises increasingly seeking integrated DLP suites that deliver comprehensive security and policy management across diverse digital ecosystems.

Industry Vertical Analysis

In 2025, the Banking, Financial Services, and Insurance (BFSI) sector remains the largest industry vertical for DLP solutions, representing over one-fifth of total revenues. The sector’s reliance on sensitive data—ranging from personal identification details to transaction records—makes it a frequent target for cybercriminals. Regulatory regimes such as PCI DSS, SOX, and evolving open banking frameworks further compel financial institutions to adopt stringent DLP measures.

The rapid digitization of financial services, the rise of mobile payments, and fintech innovation are amplifying the sector’s exposure to data risks. Consequently, BFSI institutions are prioritizing real-time monitoring, transaction-level protection, and compliance-driven security investments. Other high-growth verticals include healthcare, where electronic health records demand strong encryption, and government, where safeguarding sensitive national data is paramount.

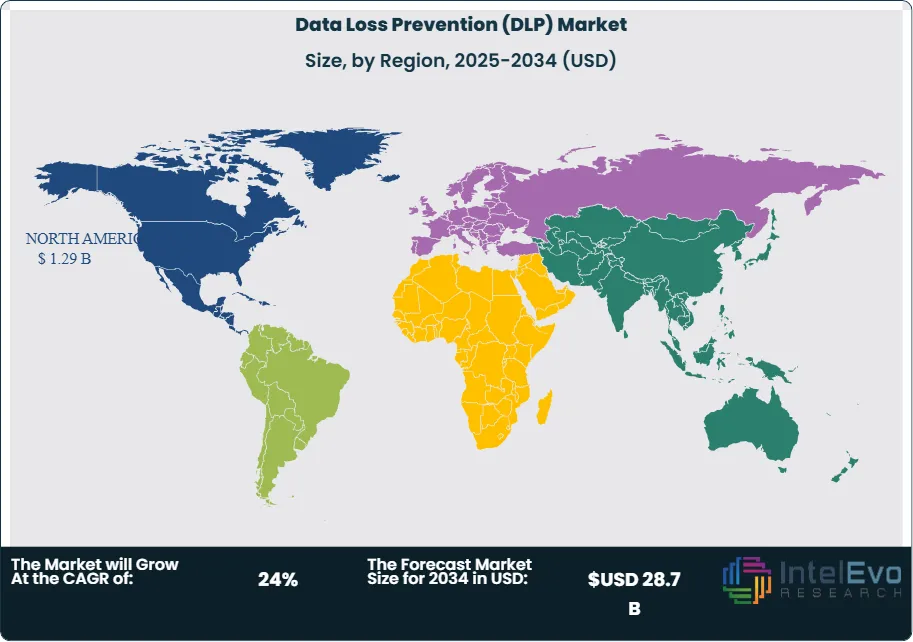

Regional Outlook Analysis

North America continues to dominate the global Data Loss Prevention market in 2025, holding more than 36.9% of revenues. This leadership is supported by a mature cybersecurity landscape, stringent regulations such as HIPAA and CCPA, and the presence of leading technology firms like Broadcom, IBM, and Forcepoint. Enterprises in the U.S. and Canada are also early adopters of AI and machine learning-enhanced DLP tools, which further strengthens regional growth.

Europe remains the second-largest market, driven by GDPR compliance and strong adoption across banking, healthcare, and government sectors. Meanwhile, Asia-Pacific is emerging as the fastest-growing region, propelled by rapid digital transformation, rising cybercrime rates, and new regulatory frameworks in countries like India, Singapore, and Japan. With organizations across APAC increasingly prioritizing cybersecurity, the region is expected to significantly expand its share of the global DLP market over the coming decade.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Solution

- Storage/Data Centre DLP

- Network DLP

- Endpoint DLP

By Deployment Mode

- Cloud-Based

- On-Premise

By Organization Size

- Small and Medium-Sized Enterprises

- Large Enterprises

By Application

- Encryption

- Email and Web Protection

- Cloud Storage

- Centralized Management

- Policy, Standards, and Procedures

- Workflow Management and Incident Response

By Industry Vertical

- IT and Telecommunications

- BFSI

- Manufacturing

- Healthcare

- Retail and Logistics

- Government and Public Sector

- Other Industry Verticals

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 3.5 B |

| Forecast Revenue (2034) | USD 28.7 B |

| CAGR (2024-2034) | 24% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector, Other Industry Verticals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Cisco Systems, Inc., Proofpoint, Inc., Forcepoint, Sophos Ltd., GTB Technologies, Microsoft Corporation, Varonis, Zscaler, Inc., Check Point Software Technologies Ltd., Broadcom Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Market Size, Share & Analysis By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector) Industry Regions & Key Players – Cybersecurity Threat Landscape & Forecast 2025–2034")

Market Size, Share & Analysis By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector) Industry Regions & Key Players – Cybersecurity Threat Landscape & Forecast 2025–2034")

Market Size, Share & Analysis By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector) Industry Regions & Key Players – Cybersecurity Threat Landscape & Forecast 2025–2034")

Frequently Asked Questions

How big is the Data Loss Prevention (DLP) Market?

The Data Loss Prevention (DLP) Market is expected to grow from USD 3.5 Billion in 2024 to USD 28.7 Billion by 2034, at a CAGR of 24%. Rising cyber threats, stricter compliance regulations, and enterprise security modernization are driving strong market adoption.

Who are the major players in the Data Loss Prevention (DLP) Market?

Cisco Systems, Inc., Proofpoint, Inc., Forcepoint, Sophos Ltd., GTB Technologies, Microsoft Corporation, Varonis, Zscaler, Inc., Check Point Software Technologies Ltd., Broadcom Inc., Other Key Players

Which segments covered the Data Loss Prevention (DLP) Market?

By Solution (Storage/Data Centre DLP, Network DLP, Endpoint DLP), By Deployment Mode (Cloud-Based, On-Premise), By Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), By Application (Encryption, Email and Web Protection, Cloud Storage, Centralized Management, Policy, Standards, and Procedures, Workflow Management and Incident Response), By Industry Vertical (IT and Telecommunications, BFSI, Manufacturing, Healthcare, Retail and Logistics, Government and Public Sector, Other Industry Verticals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Data Loss Prevention (DLP) Market

Published Date : 10 Nov 2025 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date