- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Death Care Services Market Size, Share & Forecast 2025–2034 | 4.5% CAGR

Global Death Care Services Market Size, Share, Growth & Industry Analysis By Service Type (Funeral Services, Cremation Services, Burial Services, Memorial Services, Pre-Need Planning), By Arrangement Type (At-Need, Pre-Need), By Disposition (Burial, Cremation, Green/Natural Burial), By End-User (Funeral Homes, Crematories, Cemeteries, Online Memorial Platforms), By Region & Key Players – Industry Trends, Competitive Landscape, Investment Outlook & Forecast 2025–2034

Report Overview

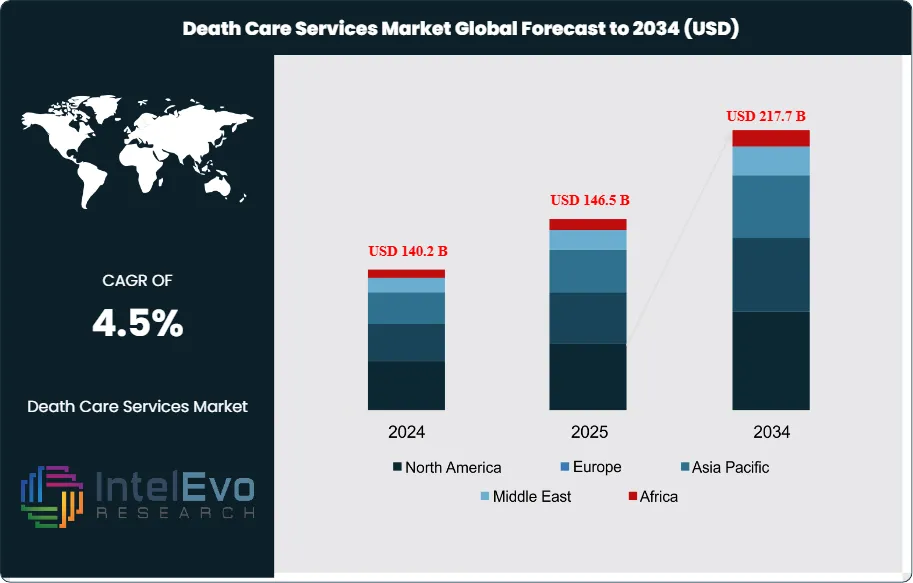

The Death Care Services Market was valued at approximately USD 140.2 billion in 2024 and is projected to reach nearly USD 217.7 billion by 2034, reflecting steady expansion supported by demographic aging trends, rising funeral service costs, and increasing demand for personalized memorial solutions. Based on the established growth trajectory, the market size for 2025 is estimated at approximately USD 146.5 billion. From 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 4.5% during 2026–2034, ultimately reaching around USD 217.7 billion by 2034.

Get More Information about this report -

Request Free Sample ReportThis growth is primarily driven by increasing mortality volumes in aging populations across North America, Europe, and parts of Asia Pacific. Additionally, changing consumer preferences toward pre-need funeral planning, eco-friendly burial options, and digital memorial services are reshaping the service portfolio of providers. Consolidation among funeral home operators and cemetery management companies is further strengthening pricing power and operational efficiency, supporting long-term revenue stability across the industry.

Death care services encompass the coordinated set of activities required after a death, including body preparation, transportation, visitation and ceremony management, cremation or interment, and administration of the final disposition. The sector also captures revenue from essential merchandise such as caskets, urns, and memorial products, alongside preneed planning and aftercare support. Demand remains structurally resilient because utilization tracks mortality trends rather than discretionary consumption, yet spending patterns continue to shift toward simpler formats and transparent pricing.

Consumer choice is moving decisively toward cremation and lower-total-cost arrangements. The NFDA cites a 61.9% cremation rate in 2024, with long-range projections reaching 82.1% by 2045, which strengthens volume visibility for cremation operators and suppliers of urns and memorialization services. Price sensitivity reinforces this pivot: a funeral with burial averaged USD 8,300 in 2023 versus USD 6,280 for cremation services. Environmental preference also reshapes product design and service mix. Interest in green options reached 68%, up from 55.7% in 2021, supporting differentiated offerings such as natural burial grounds, biodegradable containers, and lower-emission disposition methods where permitted.

Supply conditions reflect a fragmented provider base with ongoing consolidation. Large multi-location operators and metro-area funeral homes benefit from scale in facilities, fleet utilization, and procurement, while independents gain share in local, faith-based, and eco-focused niches. A reasonable global estimate places the top 10 providers at roughly 30–35% of revenue, leaving ample room for tuck-in acquisitions. Regulatory oversight influences operating models through consumer-protection rules on disclosures and pricing, licensing requirements, zoning constraints, and tightening environmental standards for crematoria emissions and waste handling. Key risks include energy and labor cost inflation, land scarcity for burial, compliance failures, and reputational exposure from service disruptions.

Digitalization is accelerating operational and commercial change. Online arrangement platforms, remote conferencing for services, and digital memorial ecosystems expand reach and improve conversion. AI-enabled scheduling, demand forecasting, and automated documentation reduce cycle times, while sensor-driven maintenance and workflow automation improve facility uptime. Regionally, North America remains the largest profit pool at an estimated 35–40% of 2024 revenue, while Asia-Pacific posts the fastest growth at a projected 5.5–6.5% CAGR, led by urbanizing corridors in India, Southeast Asia, and coastal China where cremation capacity and premium memorial parks attract capital. Europe advances in regulated green burial, and select Gulf and Latin American cities emerge as smaller but investable hubs tied to modern cemetery infrastructure and private crematoria development.

, By Arrangement Type (At-Need, Pre-Need), By Disposition (Burial, Cremation, Green/Natural Burial), By End-User (Funeral Homes, Crematories, Cemeteries, Online Memorial Platforms), By Region & Key Players – Industry Trends, Competitive Landscape, Investment Outlook & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market grows from 140.2 billion USD, 2024 to 217.7 billion USD, 2034 at 4.5% CAGR, 2024-2034.

- Segment Dominance : Cremation Services lead the service type mix at 40.3%, 2024 as consumers shift away from traditional burial.

- Segment Dominance: Individual Consumers account for 53.1%, 2024, keeping demand concentrated in personalized, direct-to-consumer offerings.

- Driver: Providers capture demand for lower-cost disposition, supported by estimated: 6.3 thousand USD, 2024 average cremation spending in comparable markets.

- Restraint: Operators face cost pressure from labor, energy, and compliance, reflected in estimated: 3.0% YoY operating cost inflation, 2024 in mature markets.

- Opportunity: Firms scale preneed plans and value-added memorial products to lift revenue per case, targeting estimated: 1.2 thousand USD, 2024 incremental add-on spend per service.

- Trend: Digital arrangements and automated back-office workflows accelerate adoption, with estimated: 35.0% of bookings initiated online, 2024 across large urban providers.

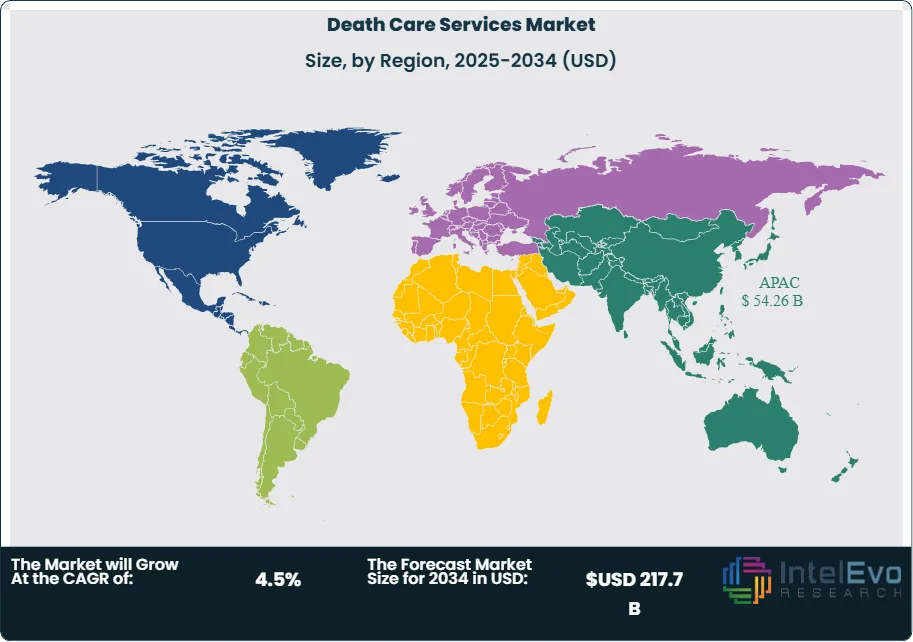

- Regional Analysis: Asia Pacific leads at 38.7%, 2024, generating 54.26 billion USD, 2024, backed by population scale and modernization of death care infrastructure.

By Type

Cremation Services enter 2025 as the largest revenue line, holding 40.3% share in 2024. Cost discipline drives that position. NFDA pricing data puts the median funeral with burial at USD 8,300 in 2023, versus USD 6,280 for a funeral with cremation. Families also choose cremation for its logistics. It supports later ceremonies, ash scattering, and keepsake products without the time and land constraints of burial.

Funeral Services and Burial Services remain core, but they shift toward smaller, simpler packages. Younger households show higher price sensitivity and higher acceptance of direct cremation, which compresses merchandise revenue from caskets while increasing demand for urns and memorial add-ons. Embalming Services hold a smaller share because many cremation pathways bypass embalming unless viewing requirements or transport rules apply. Memorial Services expand as a standalone option, especially when families separate the disposition from the gathering.

Pre-Planning Services gain weight in the mix as providers push predictable cash flow and better capacity planning. Large operators continue to professionalize sales and aftercare programs. Service Corporation International reported USD 977 million in adjusted operating cash flow for 2024 and deployed USD 181 million to acquire 26 funeral homes and 6 cemeteries, signaling continued consolidation and disciplined capital allocation going into 2025.

By Application

Service demand increasingly splits between disposition-only transactions and experience-led memorialization. Direct cremation and streamlined burial packages win volume because they reduce total spend and shorten decision cycles. At the same time, families still pay for personalization. They shift budgets toward venues, catering, tribute media, and commemorative products when they avoid high-cost traditional bundles.

Digital channels now shape how families evaluate options. Many providers route first contact through websites and call centers, then confirm arrangements in person or by video. Automation reduces paperwork time in permits, death certificates, and scheduling. AI supports pricing consistency, staffing plans, and case load forecasting. These tools matter because service quality depends on on-time coordination across transport, preparation, and ceremony logistics.

Environmental considerations influence application choices beyond cremation. Interest in green options remains high. NFDA reports 61.4% of consumers show interest in exploring green funeral options in 2025, up from 55.7% in 2021. Regulatory pathways also widen the menu. Alkaline hydrolysis, also called water cremation, continues to expand across US states, which supports investment in alternative disposition capacity where rules and local acceptance align.

By End-Use

Individual Consumers drive the market because decisions sit with households at the point of need. This segment accounted for 53.1% share in 2024 and stays central through 2025 as families demand transparent pricing, fast coordination, and personalization. When you compare providers, you increasingly expect clear itemized packages, online price access, and simple scheduling.

Funeral Homes remain the operational backbone even when they do not appear as the primary payer. They control facilities, staff, fleet, and supplier relationships. They also carry compliance risk. In the United States, the FTC Funeral Rule sets disclosure expectations around price lists and consumer choice, and the agency has signaled active scrutiny of how providers share pricing information. That pressure rewards firms that standardize scripts, train staff, and keep digital price information consistent.

Religious Institutions influence ceremony format in faith-led communities, but they rarely control the full spend. Hospitals and healthcare providers also shape the flow through mortuary services, referrals, and documentation, especially in urban centers. Government and military channels add steady volume tied to benefits administration and protocol requirements, and they often demand strict process control and auditability.

By Region

Asia Pacific leads on scale. The region held 38.7% share in 2024, equal to USD 54.26 billion, supported by population size, aging demographics, and rapid urbanization. Demand varies sharply by country due to faith practices and land availability. Urban corridors in China, Japan, and Southeast Asia support higher utilization of cremation infrastructure and formal memorial parks, while parts of South Asia maintain strong burial traditions that sustain cemetery and funeral ceremony spending.

North America remains a high-margin market because of established preneed penetration, corporate consolidation, and mature cemetery operations. The US cremation rate reached 61.9% in 2024 and points higher over the next decade, which keeps investment focused on crematories, merchandise mix changes, and alternative disposition approvals. Europe shows steady demand with strong regulatory oversight and accelerating interest in natural burial and lower-emission practices, particularly in Western and Northern markets.

Latin America and the Middle East and Africa offer selective growth tied to urban middle-class expansion, insurance development, and private facility build-out. In these regions, you see opportunity where operators modernize cold storage, transport fleets, and compliant cremation capacity, while adapting service design to local religious requirements and municipal permitting constraints.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Funeral Services

- Cremation Services

- Burial Services

- Memorial Services

- Pre-Planning Services

- Embalming Services

By End-User

- Individual Consumers

- Funeral Homes

- Religious Institutions

- Hospitals & Healthcare Providers

- Government & Military

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 146.5 B |

| Forecast Revenue (2034) | USD 217.7 B |

| CAGR (2025-2034) | 4.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type (Funeral Services, Cremation Services, Burial Services, Memorial Services, Pre-Planning Services, Embalming Services), By End-User (Individual Consumers, Funeral Homes, Religious Institutions, Hospitals & Healthcare Providers, Government & Military) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | InvoCare, Matthews International Corporation, Kaashimukthi, Service Corporation International (SCI), Banyan Funeral Services, Arbor Memorial Services, FUJIFILM Holdings Corporation (Fujifilm Memorial Services), Sukhant Funeral, Carriage Services, Nirvana Funeral Services, Indian Funeral Services, Dignity Memorial, Last Journey, Anthyesti Funeral Services, StoneMor Inc., Amedisys Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Arrangement Type (At-Need, Pre-Need), By Disposition (Burial, Cremation, Green/Natural Burial), By End-User (Funeral Homes, Crematories, Cemeteries, Online Memorial Platforms), By Region & Key Players – Industry Trends, Competitive Landscape, Investment Outlook & Forecast 2025–2034")

, By Arrangement Type (At-Need, Pre-Need), By Disposition (Burial, Cremation, Green/Natural Burial), By End-User (Funeral Homes, Crematories, Cemeteries, Online Memorial Platforms), By Region & Key Players – Industry Trends, Competitive Landscape, Investment Outlook & Forecast 2025–2034")

, By Arrangement Type (At-Need, Pre-Need), By Disposition (Burial, Cremation, Green/Natural Burial), By End-User (Funeral Homes, Crematories, Cemeteries, Online Memorial Platforms), By Region & Key Players – Industry Trends, Competitive Landscape, Investment Outlook & Forecast 2025–2034")

Frequently Asked Questions

How big is the Death Care Services Market?

The Global Death Care Services Market was valued at USD 140.2 Billion in 2024 and is projected to reach USD 217.7 Billion by 2034, growing at a CAGR of 4.5% from 2026–2034. Explore market trends, funeral and cremation services demand, personalized memorial solutions, key drivers, and future industry opportunities.

Who are the major players in the Death Care Services Market?

InvoCare, Matthews International Corporation, Kaashimukthi, Service Corporation International (SCI), Banyan Funeral Services, Arbor Memorial Services, FUJIFILM Holdings Corporation (Fujifilm Memorial Services), Sukhant Funeral, Carriage Services, Nirvana Funeral Services, Indian Funeral Services, Dignity Memorial, Last Journey, Anthyesti Funeral Services, StoneMor Inc., Amedisys Inc.

Which segments covered the Death Care Services Market?

By Service Type (Funeral Services, Cremation Services, Burial Services, Memorial Services, Pre-Planning Services, Embalming Services), By End-User (Individual Consumers, Funeral Homes, Religious Institutions, Hospitals & Healthcare Providers, Government & Military)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date