- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Decal Paper Market Size Growth, Trends & Forecast | 7.9% CAGR

Global Decal Paper Market Size, Share & Analysis By Type (Laser, Inkjet, Candle, Tattoo, Wood), By End-user (Textile, Construction, Automotive, Others), Printing Technology Trends, Cost Analysis, Regional Outlook & Forecast 2025–2034

Report Overview

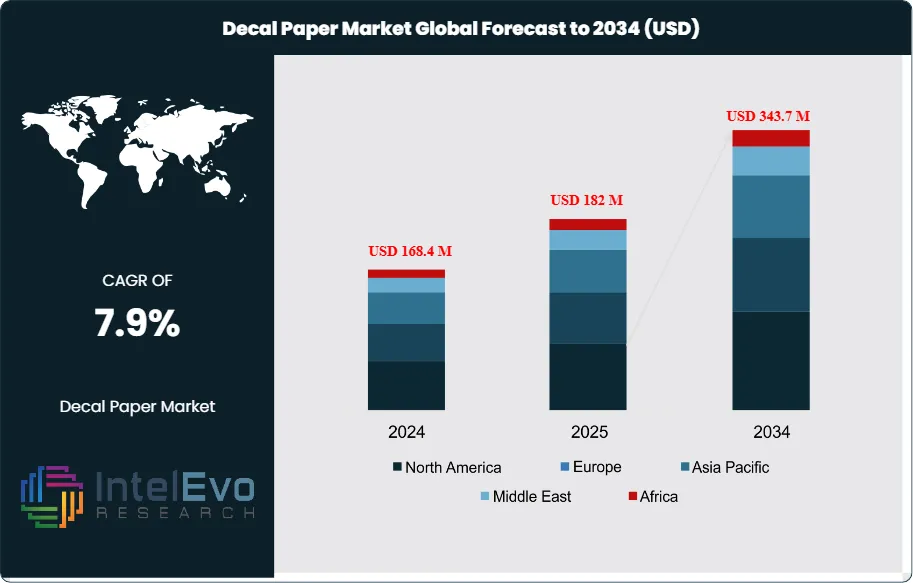

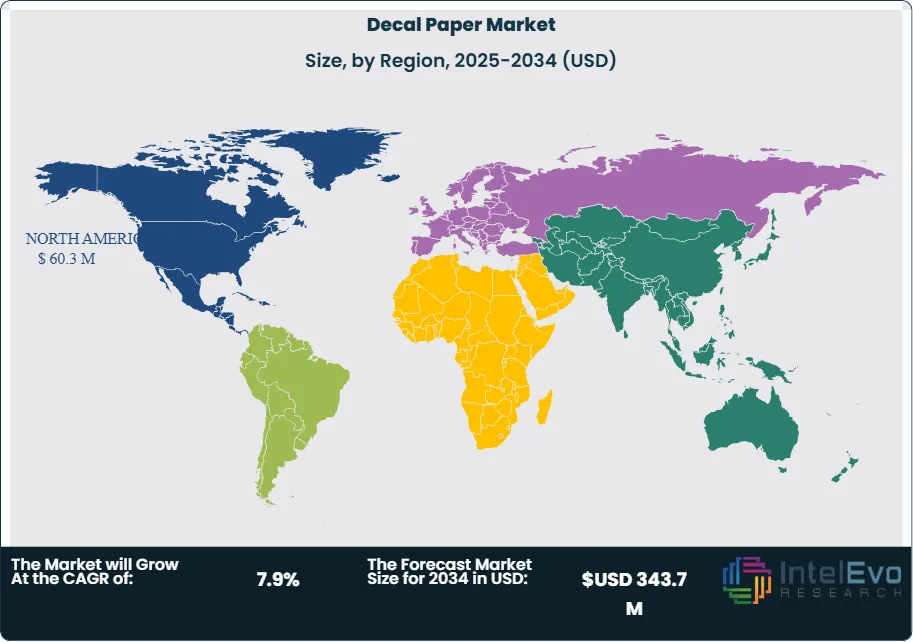

The Decal Paper Market is valued at USD 168.4 million in 2024 and is projected to reach nearly USD 343.7 million by 2034, expanding at an estimated CAGR of around 7.9% from 2025 to 2034. Growth is being driven by rising personalization trends, booming craft and DIY culture, and expanding applications across ceramics, textiles, automotive detailing, and branded merchandise. Modern printing technologies—laser, inkjet, and eco-solvent—are accelerating adoption as businesses and creators seek cost-effective customization solutions. With the surge of online craft marketplaces and small-scale manufacturers, decal paper is entering a high-visibility growth phase worldwide.

Get More Information about this report -

Request Free Sample ReportThis steady expansion underscores the growing relevance of decal paper as a versatile medium for design transfer across multiple industries. Historically, the market was niche, catering mainly to specialty crafts and limited commercial applications. However, in recent years, demand has accelerated due to rising consumer interest in personalization, do-it-yourself (DIY) projects, and decorative applications spanning ceramics, textiles, glass, and home décor. This shift has expanded decal paper’s role from an artisan tool to a mainstream input for creative, industrial, and small-business uses.

A number of demand-side and supply-side factors are shaping market momentum. On the demand front, the surge in social media–driven aesthetics and influencer culture has amplified the appeal of customized and handmade goods, driving higher consumption of decal paper products. From the supply side, advancements in printing technologies—particularly inkjet and laser printing—have enhanced the quality, durability, and usability of decal papers. Their water-resistant and UV-tolerant properties add functional advantages, making them suitable for both indoor and outdoor applications. Nevertheless, challenges such as fluctuating raw material prices and the need for quality consistency across substrates could temper growth, particularly for smaller producers facing cost pressures.

Technology adoption is also reshaping competitive dynamics. Emerging innovations include digitalized design software, AI-enabled customization platforms, and the integration of eco-friendly paper substrates that align with sustainability imperatives. Automation in printing processes and e-commerce–driven distribution models are further widening market accessibility. These technological advances are expected to lower entry barriers for small enterprises while creating new premium categories for advanced design transfer solutions.

Regionally, North America and Europe continue to lead in market share, driven by strong craft, home décor, and design-oriented consumer bases. However, Asia-Pacific is rapidly emerging as a growth hotspot, fueled by expanding middle-class consumption, rising urbanization, and increasing demand for affordable decorative solutions. Countries such as China and India are particularly attractive for investors, offering both manufacturing scale and high-volume consumer markets. Collectively, these dynamics position the decal paper market as a steadily expanding sector with clear opportunities for both incumbents and new entrants seeking exposure to the personalization and design economy.

, By End-user (Textile, Construction, Automotive, Others), Printing Technology Trends, Cost Analysis, Regional Outlook & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Decal Paper Market was valued at USD 168.4 million in 2024 and is projected to reach USD 343.7 million by 2034, registering a CAGR of 7.9% over 2025–2034. Growth is fueled by rising consumer demand for customization, DIY crafts, and decorative applications in home décor and lifestyle products.

- Product Type: Inkjet decal paper accounted for the largest revenue share of over 40% in 2024, supported by its compatibility with consumer-grade printers and widespread use in personalized crafts. Its lower cost and high accessibility continue to make it the preferred choice across small businesses and hobbyists.

- Application: The ceramics and glass segment held more than 35% of global revenue in 2024, driven by strong adoption in decorative kitchenware, tableware, and interior design. The durability of decal prints on non-porous surfaces has reinforced growth in this application segment.

- Driver: The surge in social media–driven consumer trends has significantly boosted demand for customized merchandise, with over 65% of millennial consumers reporting willingness to pay a premium for personalized products, directly supporting decal paper adoption.

- Restraint: Fluctuations in raw material costs and the dependency on quality paper substrates pose supply chain challenges, with smaller producers experiencing up to 10–15% margin pressure in periods of volatility.

- Opportunity: Asia-Pacific is expected to witness the fastest growth at a CAGR exceeding 6.5% through 2034, supported by rising middle-class consumption, e-commerce expansion, and low-cost manufacturing hubs in China and India.

- Trend: Digitalization and eco-friendly product development are reshaping the market. Manufacturers are investing in sustainable decal substrates and AI-enabled design tools, with early adopters gaining competitive advantage in premium and environmentally conscious consumer segments.

- Regional Analysis: North America and Europe collectively accounted for over 55% of global revenue in 2024, supported by established DIY and craft cultures. Meanwhile, Asia-Pacific is emerging as the next investment hotspot, projected to contribute an additional USD 40–45 million to market revenues by 2034.

Type Analysis

The decal paper market is broadly categorized into inkjet decal paper, laser decal paper, and tattoo decal paper, each catering to distinct user needs and industries. As of 2025, the laser decal paper segment is poised for the fastest expansion, supported by its superior precision, durability, and compatibility with professional-grade printers. Its ability to deliver high-resolution prints suitable for commercial applications in ceramics, automotive trims, and branded merchandise makes it increasingly attractive for industrial buyers. Analysts project this segment to capture a larger share of new installations, growing at a CAGR above 6% through 2032.

Inkjet decal paper continues to hold significant adoption among hobbyists, designers, and small-scale craft businesses. Favored for its affordability and accessibility, it remains a dominant choice for indoor decorative purposes, miniature modeling, and DIY personalization. Despite slower growth compared to laser paper, the segment maintains steady demand as inkjet printers remain widely used in households and small enterprises. Tattoo decal paper, meanwhile, serves niche demand across temporary body art and cosmetic applications, finding traction in fashion-driven markets and event-based retail promotions.

Application Analysis

Decal paper is utilized across multiple applications, with textiles, ceramics, and construction emerging as key growth arenas. The textile segment is expected to witness robust expansion as customization becomes central to consumer fashion and interior design. Rising demand for personalized clothing, luxury fabrics, and specialty apparel has fueled adoption, with textile applications expected to represent a significant revenue share by 2032. Ceramics follow closely, driven by the continued popularity of customized tableware, kitchenware, and ornamental products enhanced with high-quality decal prints.

The construction sector is anticipated to grow at a healthy pace, supported by the use of decal paper in decorative tiles, architectural glass, and interior panels. As design aesthetics play a greater role in urban development, the integration of decals into construction materials is increasingly viewed as a cost-effective solution for differentiation. Automotive applications also contribute meaningfully, with decals applied for both aesthetic customization and branding, further expanding the market scope.

End-Use Analysis

Residential applications dominate end-use demand, fueled by consumer interest in home décor, craft projects, and DIY customization. The increasing affordability of advanced printing techniques has widened access to personalized décor items such as glassware, ceramics, and furniture accents. Commercial buildings also represent a rising opportunity, particularly in hospitality and retail, where decals are used to create branded interiors and customer experiences. This segment is expected to grow steadily as businesses seek differentiation through design-led strategies.

Industrial applications, though smaller in scale, are expanding with the adoption of decals in packaging, automotive detailing, and specialty product labeling. As industries continue to integrate customization into product offerings, decal paper provides a flexible medium for low-cost, high-quality design transfer, enhancing brand visibility and consumer engagement.

Regional Analysis

North America accounted for approximately 35.8% of the global decal paper market in 2024 and continues to lead, underpinned by advanced printing infrastructure, a strong DIY culture, and widespread adoption in home décor and automotive industries. Growth is further supported by demand for temporary tattoos and nail art, reflecting evolving lifestyle trends.

Europe remains a significant market, particularly in cutlery, ceramics, and household décor. Manufacturers in Germany, Italy, and France are integrating decals into high-end consumer goods, reinforcing the region’s position as a premium design hub. Asia Pacific, however, is forecasted to be the fastest-growing region through 2032, with a CAGR surpassing 7%. Rapid industrialization, expanding middle-class consumption, and government initiatives promoting manufacturing and creative industries in China and India are fueling demand. Latin America and the Middle East & Africa are emerging markets, where rising disposable incomes and urbanization are gradually driving uptake of decorative and functional decal applications.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Laser

- Inkjet

- Candle

- Tattoo

- Wood

By End-user

- Textile

- Construction

- Automotive

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 168.4 M |

| Forecast Revenue (2034) | USD 343.7 M |

| CAGR (2024-2034) | 7.9% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Laser, Inkjet, Candle, Tattoo, Wood), By End-user (Textile, Construction, Automotive, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Hemmi Papilio Supplies LLC., Chengdu Jitian Decal Print, Bel Inc., Lazertran Ltd., Tullis Russell Coaters, Stechcol Ceramic Crafts Development, One Step Papers, LLC., Image Transfers Inc., Glitters Ltd., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-user (Textile, Construction, Automotive, Others), Printing Technology Trends, Cost Analysis, Regional Outlook & Forecast 2025–2034")

, By End-user (Textile, Construction, Automotive, Others), Printing Technology Trends, Cost Analysis, Regional Outlook & Forecast 2025–2034")

, By End-user (Textile, Construction, Automotive, Others), Printing Technology Trends, Cost Analysis, Regional Outlook & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date