- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Decentralized Clinical Trial Platform Market Size, Share & Forecast | CAGR 14.6%

Global Decentralized Clinical Trial Platform Market Size, Share, Growth Analysis By Offering (Solutions, Managed DCT Services, Professional Services), By Trial Phase (Phase I, Phase II, Phase III, Phase IV/Post-Marketing), By Therapeutic Area (Oncology, Cardiovascular, CNS & Neurology, Rare Diseases, Immunology), By End-User (Pharma & Biotech Companies, CROs, Research Institutions, Medical Device Companies), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

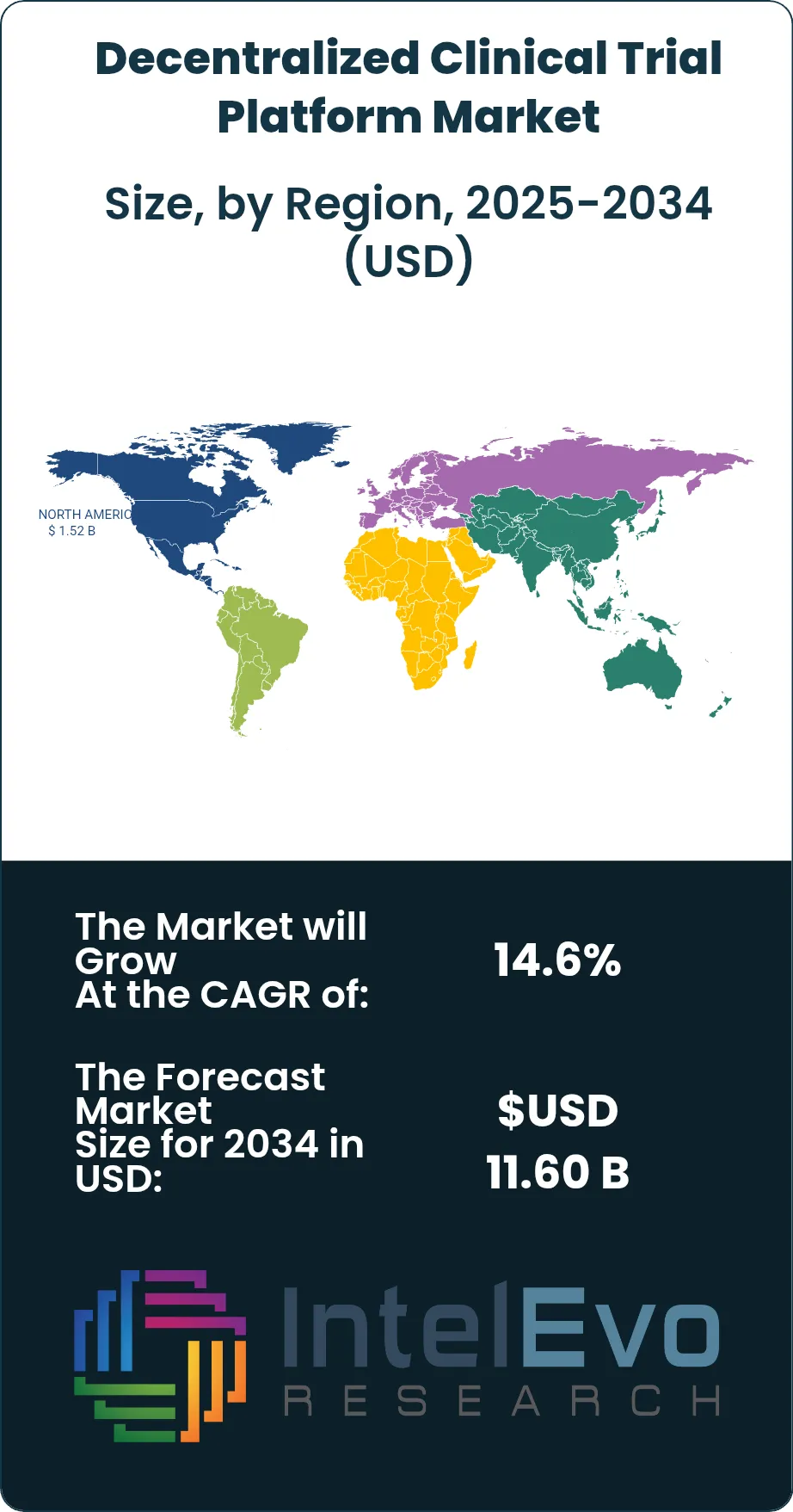

| USD 3.40 Billion | USD 11.60 Billion | 14.6% | North America, 44.6% |

The Decentralized Clinical Trial Platform Market was valued at approximately USD 2.97 Billion in 2024 and reached USD 3.40 Billion in 2025. The market is projected to grow to USD 11.60 Billion by 2034, expanding at a CAGR of 14.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 8.20 Billion over the analysis period, driven by pharmaceutical sponsors' accelerating adoption of remote and hybrid trial execution models, regulatory support from the FDA and EMA for virtual trial designs, and the maturation of digital health technologies enabling home-based clinical data collection at clinical-grade quality.

Get More Information about this report -

Request Free Sample ReportDecentralized clinical trial platforms encompass the software, services, and technology infrastructure that enable clinical trials to be conducted partly or fully outside traditional site settings, using eConsent, electronic patient-reported outcomes, remote monitoring, telemedicine visits, home health nurse networks, and connected wearable devices. The market spans solutions sold to pharmaceutical and biotech sponsors, contract research organizations, academic medical centers, and medical device manufacturers. Industry analysis indicates that fully decentralized and hybrid decentralized trials now represent approximately 38% of all newly initiated Phase II and Phase III programs globally as of 2025, compared to 11% in 2020 — a structural shift catalyzed by COVID-19 operational necessity and cemented by the demonstrated patient recruitment and retention advantages of decentralized designs.

Regulatory frameworks have been instrumental in shaping the decentralized clinical trial platform market's current structure. The FDA's 2023 guidance on decentralized clinical trials for drugs, biological products, and devices established a formal framework for remote visits, digital biomarkers, and home health professional use in regulated studies, resolving the ambiguity that had slowed pharma adoption. The EMA's reflection paper on decentralized elements in clinical trials, updated in 2023, aligned European practice with U.S. expectations while adding specific requirements for electronic consent validity under EU GDPR. The ICH E6(R3) Good Clinical Practice revision, finalized in 2023 and implemented progressively through 2025, explicitly accommodates decentralized trial conduct, providing the GCP compliance framework needed for global multi-regional DCT studies. These regulatory developments collectively removed the primary compliance uncertainty that had held back widespread adoption.

North America commands 44.6% of 2025 global market revenue, approximately USD 1.52 Billion, anchored by the high concentration of pharmaceutical and biotech sponsors, FDA regulatory clarity, and the dense CRO infrastructure based in Research Triangle, Pennsylvania, and New Jersey. Europe holds 28.2% of 2025 share, driven by EMA alignment and active multi-country DCT programs among European pharma majors. Asia Pacific accounts for 17.8% and is the fastest-growing region as Japanese, Australian, and Indian sponsors expand DCT capabilities. The decentralized clinical trial platform market is moderately consolidated, with Medidata Solutions, ICON, Science 37, and Veeva Systems collectively holding approximately 49% of 2025 global revenue.

, By Trial Phase (Phase I, Phase II, Phase III, Phase IV/Post-Marketing), By Therapeutic Area (Oncology, Cardiovascular, CNS & Neurology, Rare Diseases, Immunology), By End-User (Pharma & Biotech Companies, CROs, Research Institutions, Medical Device Companies), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global decentralized clinical trial platform market was valued at USD 3.40 Billion in 2025 and is projected to reach USD 11.60 Billion by 2034, at a CAGR of 14.6% for 2026–2034.

- Segment Dominance: Solutions (software and platform licenses) account for 54.2% of 2025 market revenue, as pharmaceutical sponsors prioritize platform-based DCT infrastructure over managed service contracts to maintain greater control over data sovereignty and regulatory audit trail management.

- Segment Dominance: Oncology is the leading therapeutic area at 31.8% of 2025 market share, driven by the high unmet need for patient-centric cancer trial designs, the geographic dispersion of oncology patient populations away from major academic medical centers, and FDA Oncology Center of Excellence endorsement of decentralized elements in cancer studies.

- Driver: FDA's 2023 DCT guidance and ICH E6(R3) GCP revision have resolved compliance uncertainty; decentralized and hybrid trial initiation grew from 11% of Phase II/III programs in 2020 to 38% in 2025, a 245% increase that demonstrates regulatory-driven demand acceleration across the pharmaceutical industry.

- Restraint: Fragmented digital health technology integration is the primary operational constraint; 62% of DCT program delays in 2024 were attributed to data interoperability failures between wearable devices, ePRO systems, and central EDC platforms, adding an average of 3.4 months to study timelines and USD 1.2 Million in unplanned technology costs per Phase III program.

- Opportunity: Rare disease and orphan drug trial programs represent an estimated USD 1.6 Billion incremental DCT platform opportunity by 2030, as the extreme geographic dispersion of rare disease patient populations makes fully decentralized trial execution the only practically viable clinical development model for sponsors targeting ultra-rare indications.

- Trend: AI-powered patient recruitment and retention automation is the dominant trend; platforms deploying AI eligibility screening report a 68% reduction in patient identification timelines — from 62 days to 20 days on average — and a 42% improvement in protocol deviation rates compared to conventional site-based recruitment, fundamentally improving trial quality economics.

- Regional Analysis: North America leads the decentralized clinical trial platform market with 44.6% of 2025 global revenue, equivalent to approximately USD 1.52 Billion, underpinned by FDA regulatory clarity, the highest concentration of pharmaceutical and biotech DCT sponsor activity, and the most developed home health and telemedicine infrastructure globally.

Competitive Landscape Overview

The decentralized clinical trial platform market is moderately consolidated, with the top four vendors — Medidata Solutions, ICON, Science 37, and Veeva Systems — collectively accounting for approximately 49% of 2025 global revenue. Competition is platform-driven, with vendors differentiating on breadth of integrated capabilities, regulatory compliance documentation depth, patient-facing app quality, and home health network geographic coverage. M&A activity was significant between 2021 and 2024, including Dassault Systèmes' embedding of Medidata into its life sciences cloud and ICON's acquisition of PRA Health Sciences. New AI-native patient recruitment and ePRO vendors are entering as point-solution challengers, pressuring incumbent platforms to accelerate AI feature integration or risk module-by-module displacement.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Medidata Solutions (Dassault Systèmes) | USA | Leader | Medidata Rave DCT / Patient Cloud | North America | Integrated Patient Cloud with Rave EDC for fully unified DCT; secured 14 new Phase III DCT sponsor agreements (Jan 2025) |

| ICON plc | Ireland | Leader | ICON DCT Platform (Symphony) | Europe | Launched Symphony 3.0 with AI-driven patient eligibility screening and real-time ePRO integration; 22 active DCT studies (Mar 2025) |

| Science 37 | USA | Challenger | Network Orchestrated Trials (NOT) Platform | North America | Expanded virtual care network to 47 states; launched AI-powered site-less oncology protocol module (Feb 2025) |

| Veeva Systems | USA | Challenger | Veeva Vault eTMF / Veeva SiteVault | Global | Launched Veeva DCT Suite connecting eTMF, SiteVault, and CTMS with integrated eConsent and home health workflows (Apr 2025) |

| Oracle Health Sciences | USA | Challenger | Oracle Clinical One (DCT Module) | North America | Released Clinical One DCT 5.0 with wearable data ingestion for 40+ device types and automated safety signal detection (Jun 2025) |

| Parexel International | USA | Niche Player | Parexel DCT-as-a-Service | North America | Partnered with Best Buy Health to deploy home health nurse networks across 38 states for hybrid DCT visits (Sep 2025) |

| Labcorp Drug Development | USA | Niche Player | Covance DCT Solutions | North America | Expanded home phlebotomy network to 12 new European markets through Labcorp partnership with LabConnect (Jan 2026) |

| PRA Health Sciences (ICON) | Ireland | Niche Player | PRA Hybrid DCT Framework | Europe | Integrated PRA wearable data collection toolkit into ICON Symphony; added continuous glucose monitoring support (Oct 2025) |

| TransCelerate BioPharma | USA | Niche Player | eClinical Integration Toolkit (DCT) | Global | Released DCT Principles v2.0 framework adopted by 16 sponsor companies for hybrid trial design standardization (May 2025) |

| Advarra | USA | Niche Player | Advarra eConsent / IRB DCT Services | North America | Launched centralized IRB review package specifically for multi-site DCT protocols; reduced review turnaround to 5 days (Aug 2025) |

By Offering

Solutions — encompassing DCT software platforms, eConsent modules, electronic patient-reported outcome systems, remote monitoring dashboards, and wearable data ingestion platforms — command 54.2% of 2025 global decentralized clinical trial platform market revenue, equivalent to approximately USD 1.84 Billion. Enterprise pharmaceutical sponsors and large CROs prioritize platform-based deployments that consolidate the full DCT technology stack — from patient recruitment and consent through data collection, safety monitoring, and regulatory submission — within a validated, 21 CFR Part 11 and EU Annex 11 compliant environment. Average enterprise DCT platform contract values have risen materially over the 2022 to 2025 period, from approximately USD 350,000 per study to USD 680,000 per Phase III study, reflecting the expanded scope of integrated capabilities sponsors now expect from a single vendor relationship. The platform segment is being reshaped by the integration of AI patient eligibility screening, automated ePRO reminder systems, and real-time safety signal detection, all of which are migrating from optional add-ons to standard platform inclusions. Services — encompassing managed DCT execution, home health professional coordination, telemedicine visit facilitation, and DCT program design consulting — hold the remaining 45.8% of 2025 market revenue. Managed DCT services are particularly important for sponsors running their first decentralized program, who lack in-house operational expertise in home health logistics, virtual visit scheduling, and remote specimen collection chain-of-custody management.

By Trial Phase

Phase II trials account for 38.4% of 2025 global decentralized clinical trial platform market revenue and represent the largest single phase by adoption rate. Phase II DCT programs benefit most directly from the recruitment speed advantages of decentralized designs; proof-of-concept and dose-ranging studies targeting specific patient phenotypes can access geographically dispersed populations that conventional site networks miss entirely. Phase II DCT adoption grew 52% between 2022 and 2025, as sponsors recognized that faster Phase II recruitment translates directly to accelerated go/no-go decisions and reduced capital tied to uncertain clinical programs. Phase III trials hold 31.6% of 2025 market revenue and are growing fastest in absolute dollar terms, as high Phase III study budgets — averaging USD 40 Million to USD 300 Million per program — generate the largest software and services contract values in the DCT market. Hybrid Phase III designs, which combine traditional investigative sites with decentralized remote visits and home health support, now represent the dominant execution model for late-phase programs. Phase I accounts for 22.7% of 2025 revenue, primarily for first-in-human studies at academic medical centers that use DCT tools for remote follow-up between in-clinic visits. Phase IV and post-marketing surveillance programs hold the remaining 7.3% and are a growing segment as FDA and EMA increasingly accept decentralized designs for real-world evidence generation supporting label expansions.

By Therapeutic Area

Oncology is the dominant therapeutic area in the decentralized clinical trial platform market, capturing 31.8% of 2025 market revenue. Cancer patients, who frequently experience treatment-related fatigue, immune compromise, and geographic treatment center constraints, are disproportionately burdened by conventional site visit requirements. Decentralized and hybrid oncology trials reduce the patient site visit burden by an average of 47%, improving enrollment rates and reducing dropout caused by visit logistics. The FDA Oncology Center of Excellence has issued specific guidance supporting decentralized elements in oncology trials, including remote safety monitoring, digital biomarker endpoints for performance status assessment, and home health nurse administration of subcutaneous oncology agents. Central nervous system and neurology indications hold 24.6% of 2025 market share, where remote cognitive assessment tools, wearable neurological monitoring, and telemedicine neurologist visits create a natural fit with decentralized execution. Cardiovascular trials account for 19.2%, with continuous cardiac monitoring wearables enabling endpoint collection outside hospital settings. Rare diseases and orphan drug programs hold 14.7% of 2025 share and are the fastest-growing therapeutic area by percentage, as patient population geography makes full decentralization the only practical execution model for many ultra-rare indications. Immunology and inflammation accounts for the remaining 9.7%.

By End-User

Pharmaceutical and biotech companies are the dominant end-user cohort in the decentralized clinical trial platform market, generating 42.3% of 2025 global revenue. Large pharmaceutical sponsors — including those operating 50 or more concurrent clinical studies — have invested most aggressively in enterprise DCT platform licensing, building internal decentralized trial centers of excellence that drive standardized platform adoption across their global development portfolios. Biotech companies, particularly clinical-stage organizations with limited internal clinical operations infrastructure, represent the fastest-growing sub-segment within this cohort, as DCT platforms allow lean clinical teams to execute Phase II programs without large site management organizations. Contract research organizations account for 29.8% of 2025 market share and are the primary commercial channel for DCT platform technology reaching mid-market pharma and biotech sponsors. CROs that have built proprietary DCT capabilities — including Science 37's Network Orchestrated Trials model and Parexel's DCT-as-a-Service offering — compete directly with platform vendors for the same sponsor budgets. Academic and research institutions hold 18.6% of 2025 revenue, driven by NIH-funded programs that have adopted decentralized methodologies for population health and chronic disease outcome studies. Medical device companies account for the remaining 9.3%, using DCT platforms primarily for FDA 510(k) and PMA post-market clinical follow-up studies.

Regional Analysis

North America

North America leads the global decentralized clinical trial platform market with 44.6% of 2025 revenue, approximately USD 1.52 Billion. The United States is overwhelmingly dominant, driven by the FDA's detailed 2023 DCT guidance that provided the specific compliance framework pharmaceutical sponsors needed to commit institutional capital to decentralized program infrastructure. The U.S. maintains the world's largest pharmaceutical R&D investment base — with the PhRMA member companies collectively investing more than USD 100 Billion annually in clinical development — and even a marginal shift toward decentralized trial designs generates disproportionate absolute platform revenue growth. The concentration of CRO headquarters in Research Triangle (ICON, Parexel), Philadelphia, and New Jersey creates a dense operational infrastructure for DCT execution that smaller markets cannot match. The U.S. health system's established telehealth infrastructure, built during the COVID-19 pandemic and sustained through permanent CMS and state-level reimbursement policies, provides the telemedicine backbone that DCT virtual visit workflows require. Canada contributes to the North American market through Health Canada's progressive acceptance of ICH E6(R3) and through the University Health Network and other academic research leaders that have built DCT capabilities for publicly funded clinical programs. Mexico's growing pharmaceutical manufacturing sector is beginning to generate CRO-driven DCT demand for early-phase local studies, though adoption remains nascent compared to the United States.

Europe

Europe holds 28.2% of 2025 global decentralized clinical trial platform market revenue, approximately USD 959 Million. The European market operates under a dual regulatory framework that adds complexity to DCT implementation: trial execution must satisfy both EMA GCP requirements and national competent authority interpretations, while patient consent and data processing must comply with GDPR across member states. Despite this complexity, major European pharma companies — Roche, Novartis, AstraZeneca, Sanofi, and Novo Nordisk — have made DCT adoption a strategic priority, with each maintaining dedicated decentralized trial programs across multiple indications. Germany is the continent's largest single DCT market, driven by the BfArM's progressive regulatory stance and the pharmaceutical industry cluster centered on Frankfurt and Munich. The United Kingdom, operating under MHRA regulations since Brexit, has become a leading DCT innovation hub, with NHS Digital's infrastructure and the NIHR's clinical research network supporting nationwide decentralized study execution across NHS primary care settings. Switzerland contributes through the Roche and Novartis global clinical trial headquarters, both of which have invested substantially in proprietary DCT capabilities and vendor platform relationships. France's ANSM has approved DCT-specific protocols since 2021, and Sanofi's commitment to 50% hybrid trial designs by 2027 is driving significant platform investment through the French market. The EU Clinical Trials Regulation (EU CTR 536/2014), now fully operational through the CTIS portal, accommodates decentralized elements and is accelerating multi-country EU DCT program initiation timelines.

Asia Pacific

Asia Pacific accounts for 17.8% of 2025 global decentralized clinical trial platform market revenue, approximately USD 605 Million, and is the fastest-growing major region with an estimated regional CAGR exceeding 17% through 2034. Japan is the most technically mature DCT market in Asia Pacific, where the PMDA's 2023 reflection paper on DCT elements provided the regulatory clarity needed for major Japanese pharmaceutical sponsors — Takeda, Astellas, and Daiichi Sankyo — to initiate formal DCT programs. Australia has emerged as a preferred DCT innovation market within the region, combining the TGA's progressive regulatory stance, the NHMRC's funding for decentralized research methodologies, and a well-developed telehealth infrastructure to create a favorable environment for early-phase DCT program execution. Australia's research tax incentive program further reduces the cost of running Phase I and Phase II DCTs for international sponsors. India is the highest-growth single market in Asia Pacific, where the expansion of contract research organization capacity — particularly at Syneos Health India, PRA India, and Lambda Therapeutic Research — and CDSCO's progressive update of clinical trial regulations are creating rapidly scaling demand for DCT platform licenses. China represents a strategically important but distinct market: domestic DCT platform vendors are building capability rapidly, while NMPA's progressive regulatory reform has made China a viable destination for hybrid global trial designs with decentralized elements, subject to specific local data residency requirements under the Personal Information Protection Law.

Latin America

Latin America represents 5.6% of 2025 global decentralized clinical trial platform market revenue, approximately USD 190 Million. Brazil is the dominant national market, anchored by ANVISA's 2022 resolution that formally recognized digital consent, remote monitoring, and electronic patient-reported outcomes as valid clinical trial procedures under Brazilian GCP. Brazil's large patient population, high prevalence of cardiovascular and oncology indications, and the expansion of CRO operations in São Paulo — where ICON, Parexel, and Syneos Health all maintain significant Latin American offices — create the infrastructure for hybrid DCT programs serving both domestic and global sponsors. The Brazilian federal government's Mais Saúde Digital program, investing BRL 3 Billion in digital health infrastructure from 2023 through 2026, is building the telehealth connectivity that DCT virtual visit workflows require across underserved patient populations outside major metropolitan centers. Mexico contributes through COFEPRIS's increasingly progressive approach to digital trial tools and through the growing pharmaceutical contract manufacturing and clinical operations base in Monterrey and Mexico City. Argentina's ANMAT has accepted hybrid DCT elements in regulatory submissions since 2023, and the country's established CRO network and academic medical center infrastructure provide a viable platform for early-phase decentralized programs serving the Southern Cone market.

Middle East & Africa

The Middle East and Africa region accounts for 3.8% of 2025 global decentralized clinical trial platform market revenue, approximately USD 129 Million. The UAE is the most active DCT market in the region, driven by the Dubai Health Authority's digital health strategy and the Abu Dhabi Department of Health's investment in digital clinical research infrastructure at Sheikh Khalifa Medical City and Cleveland Clinic Abu Dhabi. The UAE's Vision 2071 healthcare agenda includes specific commitments to positioning the country as a clinical trial hub for the broader MENA region, creating government-sponsored demand for DCT technology. Saudi Arabia is the second-largest market in the region, with the Saudi Food and Drug Authority's progressive alignment with ICH E6(R3) and Vision 2030 healthcare transformation investments driving early adoption of digital clinical trial tools at major academic medical centers including King Faisal Specialist Hospital. South Africa maintains the most established clinical research infrastructure on the African continent, and its experience with large-scale HIV and tuberculosis trials has made South African CROs and academic medical centers early adopters of remote monitoring and digital data collection tools that form the technical foundation for DCT platforms. The broader African continent represents a nascent but strategically important emerging market, where WHO's Africa Clinical Research Network and international pharmaceutical sponsor interest in high-burden disease populations are driving early investment in DCT capability.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Solutions (Software & Platform)

- Services (Managed DCT, Professional Services)

By Trial Phase

- Phase II

- Phase III

- Phase I

- Phase IV / Post-Marketing

By Therapeutic Area

- Oncology

- CNS & Neurology

- Cardiovascular

- Rare Diseases & Orphan Drugs

- Immunology & Inflammation

By End-User

- Pharmaceutical & Biotech Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutions

- Medical Device Companies

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.40 B |

| Forecast Revenue (2034) | USD 11.60 B |

| CAGR (2025-2034) | 14.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Solutions (Software & Platform), Services (Managed DCT, Professional Services)), By Trial Phase, (Phase II, Phase III, Phase I, Phase IV / Post-Marketing), By Therapeutic Area, (Oncology, CNS & Neurology, Cardiovascular , Rare Diseases & Orphan Drugs, Immunology & Inflammation), By End-User, (Pharmaceutical & Biotech Companies , Contract Research Organizations (CROs), Academic & Research Institutions , Medical Device Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MEDIDATA SOLUTIONS (DASSAULT SYSTÈMES), ICON PLC, SCIENCE 37, VEEVA SYSTEMS, ORACLE HEALTH SCIENCES (CLINICAL ONE), PAREXEL INTERNATIONAL, LABCORP DRUG DEVELOPMENT (COVANCE), PRA HEALTH SCIENCES (ICON), TRANSCELERATE BIOPHARMA, ADVARRA, SYNEOS HEALTH, IQVIA HOLDINGS, MEDABLE INC., DATACUBED HEALTH, THREAD (FORMERLY MOSIO), CASTOR EDC, ILLINGWORTH RESEARCH GROUP, ERT (NATUS MEDICAL), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Trial Phase (Phase I, Phase II, Phase III, Phase IV/Post-Marketing), By Therapeutic Area (Oncology, Cardiovascular, CNS & Neurology, Rare Diseases, Immunology), By End-User (Pharma & Biotech Companies, CROs, Research Institutions, Medical Device Companies), Industry Trends & Forecast 2026-2034")

, By Trial Phase (Phase I, Phase II, Phase III, Phase IV/Post-Marketing), By Therapeutic Area (Oncology, Cardiovascular, CNS & Neurology, Rare Diseases, Immunology), By End-User (Pharma & Biotech Companies, CROs, Research Institutions, Medical Device Companies), Industry Trends & Forecast 2026-2034")

, By Trial Phase (Phase I, Phase II, Phase III, Phase IV/Post-Marketing), By Therapeutic Area (Oncology, Cardiovascular, CNS & Neurology, Rare Diseases, Immunology), By End-User (Pharma & Biotech Companies, CROs, Research Institutions, Medical Device Companies), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Decentralized Clinical Trial Platform Market?

The Global Decentralized Clinical Trial Platform Market was valued at USD 2.97 Billion in 2024 and is projected to reach USD 11.60 Billion by 2034, growing at a CAGR of 14.6% from 2026 to 2034, driven by rising adoption of virtual clinical trials, remote patient monitoring technologies, and digital transformation in clinical research.

Who are the major players in the Decentralized Clinical Trial Platform Market?

MEDIDATA SOLUTIONS (DASSAULT SYSTÈMES), ICON PLC, SCIENCE 37, VEEVA SYSTEMS, ORACLE HEALTH SCIENCES (CLINICAL ONE), PAREXEL INTERNATIONAL, LABCORP DRUG DEVELOPMENT (COVANCE), PRA HEALTH SCIENCES (ICON), TRANSCELERATE BIOPHARMA, ADVARRA, SYNEOS HEALTH, IQVIA HOLDINGS, MEDABLE INC., DATACUBED HEALTH, THREAD (FORMERLY MOSIO), CASTOR EDC, ILLINGWORTH RESEARCH GROUP, ERT (NATUS MEDICAL), Others

Which segments covered the Decentralized Clinical Trial Platform Market?

By Offering, (Solutions (Software & Platform), Services (Managed DCT, Professional Services)), By Trial Phase, (Phase II, Phase III, Phase I, Phase IV / Post-Marketing), By Therapeutic Area, (Oncology, CNS & Neurology, Cardiovascular , Rare Diseases & Orphan Drugs, Immunology & Inflammation), By End-User, (Pharmaceutical & Biotech Companies , Contract Research Organizations (CROs), Academic & Research Institutions , Medical Device Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Decentralized Clinical Trial Platform Market

Published Date : 09 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date