Deep Observability Market Size USD 16.1B & 38.9% CAGR

Global Deep Observability Market Size, Share & IT Operations Intelligence Analysis By Component (APM, Logs, Traces, Metrics), By Deployment (Cloud-Native, Hybrid), By End User (Enterprises, SaaS, Telecom), DevOps Adoption Trends, Key Vendors & Forecast 2025–2034

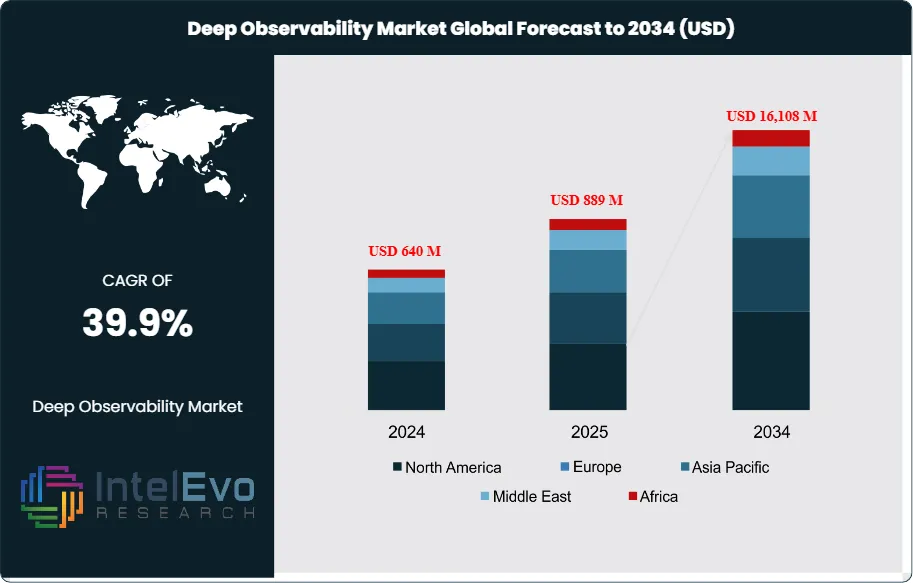

The Deep Observability Market is estimated at USD 640 million in 2024 and is projected to reach approximately USD 16,108 million by 2034, registering a CAGR of about 38.9% during 2025–2034. This exceptional growth trajectory reflects rising enterprise reliance on deep, packet-level visibility as IT environments become more distributed, encrypted, and cloud-native. Organizations are increasingly adopting deep observability to maintain performance, security, and compliance across hybrid and multicloud architectures.

Near-term momentum reinforces this outlook. Several analyses place the market at roughly USD 0.57 billion in 2024, with expectations to exceed USD 2.1 billion by 2028, tracking a CAGR near 39%. Adoption is accelerating as enterprises struggle to manage complex traffic flows created by containerization, microservices, and SaaS interconnections. As workloads shift beyond traditional perimeters, teams require visibility into lateral (East–West) traffic to prevent blind spots that can undermine application reliability and security.

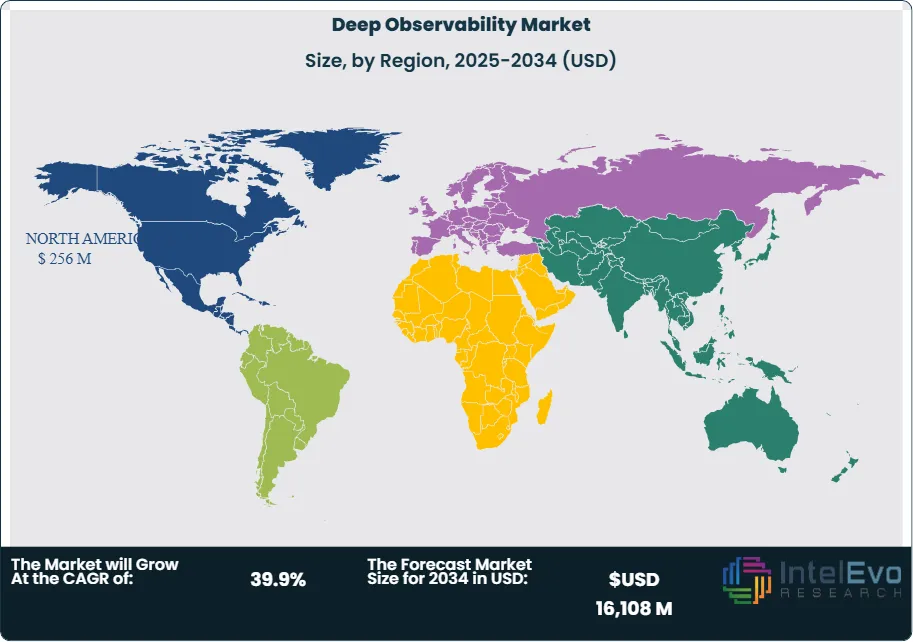

Regional demand is led by North America, which accounts for more than 40% of global revenue, supported by large enterprise and government adoption. The U.S. market alone generated approximately USD 186.4 million in 2024 and is forecast to expand at nearly 38% CAGR through 2034, driven by Zero Trust mandates and federal cybersecurity programs. Cloud-delivered deep observability solutions are gaining traction, with cloud deployments expected to represent over 50% of market revenue by 2027, signaling a decisive shift in investment priorities.

Security imperatives are a central adoption driver. Industry surveys indicate that 83% of leaders view visibility into data in motion as critical, 73% prioritize East–West traffic monitoring, and 87% consider encrypted traffic inspection essential for cloud security. Yet gaps remain: 60% of organizations lack sufficient East–West visibility, one in three could not detect a breach in the past year, and 62% report encrypted traffic is less likely to be inspected, exposing material operational and security risk. These deficiencies are pushing enterprises to invest in deeper, network-derived telemetry.

On the supply side, vendor concentration remains high. Gigamon accounted for roughly 63% market share in 2023, supported by rapid deployment of its Deep Observability Pipeline across thousands of organizations. Buyers are increasingly standardizing on platforms that fuse packet-level telemetry with logs and traces, enabling faster root-cause analysis and threat detection. AI- and machine-learning–driven analytics now enhance anomaly detection and predictive insights, while real-time processing supports high-volume telemetry across cloud and on-premises estates. For enterprise roadmaps, prioritizing encrypted traffic visibility, East–West monitoring, and Zero Trust alignment will be critical to reducing downtime, strengthening security posture, and sustaining scalable operations.

Key Takeaways

Market Growth: The market stands at USD 640 million in 2024 and is projected to reach USD 16,108 million by 2034, a 38.9% CAGR. You should plan around sustained expansion driven by hybrid and multicloud complexity and the growth of encrypted traffic inspection needs.

Component: Software accounted for about 70% of 2024 revenue as buyers’ prioritized platforms that unify network-derived telemetry with logs and traces for faster detection and root-cause analysis.

Deployment: Cloud-based solutions captured more than 61% of 2024 spend due to hybrid cloud adoption and the need to inspect data in motion at scale.

End Use: IT & Telecom held 27% share in 2024 given large East-West traffic volumes and stringent uptime requirements across carrier and enterprise networks.

Driver: 83% of leaders rate full visibility into data in motion as critical; 73% prioritize East-West over North-South monitoring; and 87% deem encrypted traffic monitoring essential, directly boosting deep observability adoption.

Restraint: Visibility gaps persist as 60% lack adequate East-West insight, one in three missed a recent breach, and 62% say encrypted traffic often bypasses inspection, which slows adoption and undermines security ROI.

Opportunity: The total addressable market is projected at USD 880 million in 2025, rising to USD 2.7 billion by 2029 at a 33% CAGR; focus on encrypted traffic analysis and lateral movement detection to capture high-growth budgets.

Trend: Vendor concentration remains high; Gigamon held 63% share in 2023 and 52% in 2025 as the segment scaled, while H1 2024 revenue exceeded USD 200 million on pace for about USD 500 million for the year.

Regional Analysis: North America led with over 40% share and USD 252 million revenue in 2024; the US reached USD 186.4 million and is set to grow at 37.7% through 2034, making it your primary near-term target market.

Component Analysis

Software remained the core of deep observability in 2024, generating over 70% of revenue as enterprises prioritized platforms that fuse network-derived telemetry with logs, metrics, and traces for faster detection and resolution across hybrid estates. This tilt toward software reflects operational needs to analyze data in motion at scale and to surface encrypted traffic blind spots that traditional tools miss.

From 2025 onward, demand concentrates in software subscriptions and pipeline capabilities as the total addressable market expands from USD 0.88 billion in 2025 to USD 2.71 billion by 2029 at a 33% CAGR, driven by hybrid cloud growth and AI-enabled analytics embedded in detection workflows. You should expect steady services pull-through for architecture design, run-state tuning, and use-case rollout as security and platform teams operationalize encrypted traffic inspection and East-West visibility.

Vendor concentration remains high, with leading providers scaling platform adoption and integrations that channel network-derived telemetry to existing cloud, security, and observability stacks to improve time to value. The model aligns with buyer goals to reduce missed breaches and instrument critical paths without ballooning log ingestion costs.

Deployment Analysis

Cloud-based deployments captured more than 61% of spend in 2024 as teams instrument multicloud services and containerized workloads and require continuous insight into data in motion across regions and accounts. The shift ties directly to risk priorities: 83% of leaders call full visibility into data in motion critical, and 87% say monitoring encrypted traffic is essential for cloud security.

The 2025 outlook favors cloud delivery as buyers seek faster rollout, elastic scale, and centralized policy for decryption and traffic brokering, reinforced by research showing deep observability has become foundational to hybrid cloud security for nearly 89% of leaders. You will see attach rates rise for managed pipeline features that filter, deduplicate, and route telemetry to control cost and enhance tool efficacy.

Hybrid remains material for firms balancing data sovereignty, east-west monitoring inside data centers, and staged migrations that demand consistent policy across on-prem and cloud endpoints. On-premise persists for sensitive segments that require local processing and selective forwarding of decrypted signals into downstream tools.

End-User Industry Analysis

IT & Telecom led with about 27% of revenue in 2024, reflecting large east-west traffic volumes, low tolerance for downtime, and complex service chains that demand packet-level visibility to assure performance and security. Operators use deep observability to detect anomalies and lateral movement earlier, reducing mean time to detect and remediate incidents across distributed networks.

BFSI, Government, and Healthcare accelerate investment where encrypted flows dominate and regulatory scrutiny is high, aligning budgets to encrypted traffic inspection and zero-trust-aligned controls that reduce blind spots. One in three organizations failed to identify a recent breach and 62% say encrypted traffic often bypasses inspection, sharpening urgency in these verticals.

Manufacturing and Others adopt for telemetry consolidation across plants and remote sites, aiming to cut tool sprawl and improve incident response with prioritized, filtered network-derived signals. Your roadmap should map to high-value use cases such as east-west segmentation validation, encrypted traffic analytics, and workload-level risk scoring.

Regional Analysis

North America held over 40% share and USD 252 million revenue in 2024; the United States reached USD 186.4 million with a projected 37.7% CAGR through 2034, sustained by large enterprise and public sector programs that require encrypted traffic visibility and lateral movement detection. The segment’s revenue pace was evident in 2024, with first-half sales exceeding USD 200 million and on track toward roughly USD 500 million for the year.

Europe and Asia Pacific expand from 2025 as cloud-first initiatives, sovereignty mandates, and compliance-driven inspection needs converge, steering buyers to deep observability to cover data in motion across regions. You should expect faster adoption where multicloud modernization and container platforms scale, requiring consistent policy enforcement and encrypted flow analytics.

Latin America and the Middle East & Africa see growing pilots around critical infrastructure, finance, and government workloads, often anchored by hybrid deployments that align with local data controls while feeding cloud analytics for detection and performance optimization. Vendor investments in partner ecosystems and packaged integrations will shape market entry and time to production across these regions.

By Component (Software, Services), By Deployment (On-Premise, Cloud-Based, Hybrid), By End-User Industry (IT & Telecom, Healthcare, BFSI, Manufacturing, Government, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Netscout, Cribl, Elastic, Honeycomb.io, Keysight Technologies, Arista Networks, Datadog, Inc., New Relic, Inc., Gigamon Inc., Kentik Inc.

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA DEEP OBSERVABILITY CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA DEEP OBSERVABILITY CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA DEEP OBSERVABILITY CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL DEEP OBSERVABILITY CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

This section profiles Datadog, New Relic, Elastic, and Gigamon against 2025 deep observability priorities including AI adoption, hybrid cloud expansion, and encrypted traffic visibility.

Datadog: Positioning: challenger with platform scale in observability and security analytics focused on AI-driven incident response and automation across hybrid estates. Core products include APM, logs, metrics, and Cloud SIEM, now extended by Bits AI agents that investigate alerts, generate code fixes, and triage security signals natively in the platform. In 2025, Datadog introduced Bits AI SRE, Dev Agent, and Security Analyst to coordinate incidents, open production-ready pull requests, and automate SIEM investigations, reflecting a strategy to compress mean time to detect and resolve with agentic workflows at scale. The company processes trillions of telemetry points and positions applied AI as a differentiator by acting within existing customer workflows rather than only summarizing data, which you should weigh when comparing operational impact and tool consolidation.

Datadog’s roadmap aligns with buyer focus on cost control and speed by using agents to filter noise, pinpoint root cause, and propose remediations that integrate with GitHub, Slack, and runbooks, reducing context switching for on-call teams. For 2025 budgets, this positions Datadog to capture expansions tied to AIOps, Cloud SIEM automation, and developer productivity improvements inside a single telemetry plane.

New Relic: Positioning: platform provider and category reporter, anchoring buyer education through the 2025 Observability Forecast that surveyed 1,700 leaders across 23 countries to quantify adoption patterns and investment priorities. The report highlights rising AI use in observability programs and continued pressure to consolidate tools and manage data costs, which shapes how you set KPI targets for uptime, risk, and spend in 2025. New Relic’s strategy emphasizes end-to-end telemetry with AI-assisted workflows and benchmarking based on the forecast, guiding customers on where to invest for the next planning cycle.

Differentiation comes from evidence-backed guidance on budget shifts, benefits realized, and capability gaps, which helps you justify spend on AI monitoring, incident response, and tool rationalization without overextending ingestion pipelines. The Forecast’s breadth and comparatives make New Relic a reference point for executives calibrating adoption roadmaps and expected ROI from observability expansions in 2025.

Elastic: Positioning: innovator with search-led observability that embeds an AI Assistant to interpret logs, traces, and errors while generating ES|QL queries, visualizations, and runbook actions inside the product. The assistant integrates with OpenAI, Azure OpenAI, and Amazon Bedrock, enabling contextual analysis and function calling that turns telemetry into guided investigations for SRE and platform teams. Elastic’s approach centers on unifying signals in Elasticsearch with an AI layer that explains issues and proposes remediation, which can reduce analysis time and improve consistency across incidents.

Strategically, Elastic targets 2025 demand for explainable AI in operations by keeping analysis close to indexed data and exposing natural-language workflows that fit existing teams and processes. You should consider Elastic where search performance, ES|QL-driven insights, and private LLM integration requirements dominate selection criteria for regulated and large-scale environments.

Gigamon: Positioning: market leader in deep observability pipelines focused on data-in-motion, encrypted traffic visibility, and East-West monitoring across hybrid cloud and data center environments. Gigamon held 63% share in 2023 and is projected around 52% in 2025 as the category scales, supported by deployments across more than 4,000 organizations and expanded integrations with security and cloud tools. Revenue cadence underscores adoption, with the segment surpassing USD 200 million in the first half of 2024 and pacing toward about USD 500 million for the year, indicating resilient demand going into 2025. Frost & Sullivan’s 2025 view of the total addressable market supports continued growth as hybrid cloud and encrypted traffic inspection budgets expand through the decade.

Gigamon differentiates on encrypted traffic analytics and East-West visibility, where 83% of leaders cite full data-in-motion visibility as critical, 73% prioritize East-West monitoring, and 87% deem encrypted traffic inspection essential for cloud security, yet 60% still lack adequate East-West insight and 62% report encrypted flows bypass inspection. This gap positions Gigamon as a priority vendor for risk reduction and Zero Trust alignment, particularly in North America where adoption and budget concentration remain highest in 2025.

Market Key Players:

Netscout

Cribl

Elastic

Honeycomb.io

Keysight Technologies

Arista Networks

Datadog, Inc.

New Relic, Inc.

Gigamon Inc.

Kentik Inc.

Driver

Hybrid and Multicloud Complexity Elevates Deep Observability Priority

In 2025, hybrid and multicloud estates are shaping enterprise IT agendas as teams manage encrypted traffic, container sprawl, and lateral movement across regions and accounts. Decision-makers increasingly recognize the limits of traditional monitoring, with a large majority calling for deeper visibility into data in motion. Full packet-level insight is now viewed as foundational for securing distributed applications and maintaining service reliability across complex cloud topologies.

Security Mandates Translate Into Sustained Budget Allocation

Security imperatives are directly influencing platform selection and spending. Enterprise leaders prioritize East–West traffic monitoring and encrypted traffic inspection as essential components of cloud security programs, particularly under Zero Trust architectures. This urgency is reflected in market expansion, with adoption accelerating as organizations standardize network-derived telemetry alongside logs, metrics, and traces to support unified security and observability strategies.

Despite rising awareness, many enterprises continue to operate with material blind spots. Inadequate East–West visibility, limited inspection of encrypted traffic, and delayed breach detection remain common, reducing confidence in early deployments. These gaps can slow rollouts and weaken the perceived return on investment, especially when teams lack the operational maturity to translate deeper telemetry into actionable outcomes.

Telemetry Cost Inflation Pressures ROI at Scale

Rising telemetry volumes present a second constraint. Storage, processing, and ingestion costs for high-fidelity network data can outpace primary infrastructure spending, forcing organizations to reassess scope and deployment models. To sustain adoption, enterprises increasingly rely on sampling, selective packet capture, and intelligent pipeline filtering, adding architectural complexity that can delay time-to-value if not carefully planned.

Opportunity

Encrypted Traffic and East–West Analytics Create High-Value Use Cases

Near-term growth opportunities center on high-impact applications such as encrypted traffic analytics and lateral threat detection in hybrid environments. Regulated sectors—including finance, government, and healthcare—are driving adoption as compliance and breach-prevention requirements intensify. These use cases deliver measurable risk reduction and performance gains, strengthening the business case for broader deep observability deployments.

Revenue Momentum Signals Durable Demand Into 2025

Market momentum is visible in accelerating revenue cadence, reflecting enterprise willingness to fund deep observability as a core capability rather than an optional add-on. Organizations are prioritizing platforms that combine security impact with cost control, using intelligent filtering and targeted telemetry routing to maximize insight while containing operational expense. This balance positions the segment for sustained growth through upcoming planning cycles.

Vendor dynamics are consolidating as buyers gravitate toward platforms that efficiently deliver network-derived telemetry into security, cloud, and observability stacks. Integrated pipelines that reduce noise and expose lateral movement at scale are increasingly favored over point tools. This shift reflects enterprise demand for operational simplicity and faster detection across hybrid environments.

AI-Driven Monitoring and Cloud Delivery Become the Default

AI-enabled monitoring is rapidly becoming standard, enhancing anomaly detection, triage, and forecasting across observability programs. At the same time, cloud-delivered deep observability continues to gain share as organizations favor elastic, policy-driven instrumentation that scales across regions. Together, AI adoption and cloud delivery are reshaping deployment architectures and setting new expectations for performance, governance, and agility in 2025 and beyond.

Recent Developments

Dec 2024 – Gigamon: Released the 2024 Hybrid Cloud Security Survey showing 83% of leaders require full visibility into data in motion, 73% prioritize East-West monitoring, and 87% view encrypted traffic inspection as essential; gaps persist as 60% lack East-West insight, 62% say encrypted traffic bypasses inspection, and one in three missed a recent breach. The findings intensify demand for deep observability pipelines and strengthen Gigamon’s position in encrypted traffic and lateral movement visibility across hybrid cloud.

Feb 2025 – New Relic: Announced 20+ AI-led platform upgrades at New Relic Now+, integrating RAG with customer and third‑party data and opening an ecosystem with partners such as ServiceNow, Google Gemini, Amazon Q Business, and GitHub Copilot. The rollout broadens New Relic’s AI footprint in observability and supports your 2025 plans to compress MTTR and manage data costs at scale.

Apr 2025 – Gigamon: Reported by 650 Group to have maintained leadership with 55% market share in 2024 as deep observability adoption accelerated across global enterprises. The validation consolidates Gigamon’s share in data‑in‑motion visibility and signals continued budget allocation to East‑West and encrypted traffic inspection use cases in 2025.

Jul 2025 – Datadog: Unveiled Bits AI SRE, Dev Agent, and Security Analyst agents that investigate incidents, propose code fixes, and automate SIEM triage, extending agentic workflows across APM, logs, and Cloud SIEM. The additions differentiate Datadog on actionability and position your teams to reduce noise and accelerate remediation within existing DevSecOps pipelines.

Sep 2025 – New Relic: Published the 2025 Observability Forecast surveying 1,700+ leaders across 20+ countries, highlighting rising AI adoption, tool consolidation, and cost governance as top priorities for the next budget cycle. The study shapes 2025 vendor selection and helps you benchmark adoption roadmaps, KPI targets, and ROI expectations for observability expansion.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Deployment (Cloud-Native, Hybrid), By End User (Enterprises, SaaS, Telecom), DevOps Adoption Trends, Key Vendors & Forecast 2025–2034")

, By Deployment (Cloud-Native, Hybrid), By End User (Enterprises, SaaS, Telecom), DevOps Adoption Trends, Key Vendors & Forecast 2025–2034")

, By Deployment (Cloud-Native, Hybrid), By End User (Enterprises, SaaS, Telecom), DevOps Adoption Trends, Key Vendors & Forecast 2025–2034")

, By Deployment (Cloud-Native, Hybrid), By End User (Enterprises, SaaS, Telecom), DevOps Adoption Trends, Key Vendors & Forecast 2025–2034")