- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Deepwater Drilling Services Market Size, Share & Growth Analysis | CAGR 5.9%

Global Deepwater Drilling Services Market Size, Share & Industry Analysis By Service Type (Well Construction and Drilling Management Services, Subsea Production Systems & SURF Services, Completion Stimulation and Intervention Services, ROV Inspection and Vessel-Based Support Services), By Water Depth, By End Use (Development Drilling, Exploration and Appraisal Services, Production Support and Late-Life Well Services), By Contract Model, Industry Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 26.8 Billion, 2025 | USD 44.9 Billion, 2034 | 5.9%, 2026–2034 | Latin America, 28.00%, 2025 |

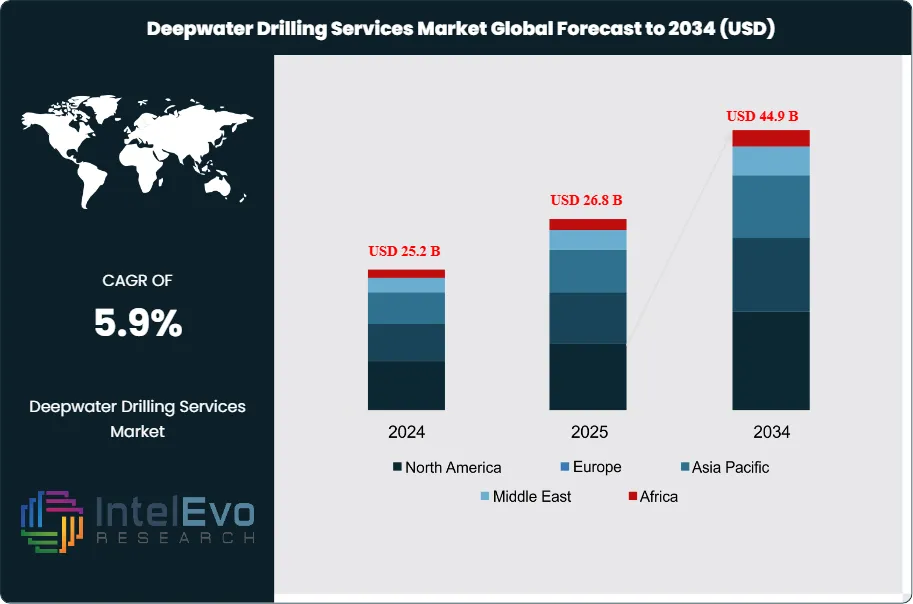

The Deepwater Drilling Services Market was valued at approximately USD 25.2 Billion in 2024 and increased to USD 26.8 Billion in 2025. The market is projected to reach nearly USD 44.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.9% during the forecast period from 2026 to 2034. Market growth is primarily driven by increasing investments in offshore oil and gas exploration, rising demand for deepwater and ultra-deepwater production projects, and technological advancements in drilling rigs, subsea systems, and offshore service capabilities. Additionally, growing energy demand and the development of new offshore fields in regions such as Brazil, West Africa, and the Gulf of Mexico are expected to further support market expansion.

Get More Information about this report -

Request Free Sample ReportThis market size is a modeled estimate built from 2025 public disclosures on offshore well construction, drilling and evaluation, subsea EPC, completion services, and deepwater contract awards across the leading service providers. The CAGR is mathematically consistent with the 2025 base and 2034 forecast.

The Deepwater Drilling Services Market in 2025 was supported by a firmer offshore development cycle than most short-cycle land service segments. Deepwater demand was led by Brazil, the U.S. Gulf of America, West Africa, and selected Southeast Asian gas projects. The U.S. Gulf remained one of the most active basins, while Brazil and Nigeria supported large field development and completion demand.

Supply in the Deepwater Drilling Services Market is no longer defined only by offshore rigs. It is increasingly shaped by well construction capacity, subsea system execution, completion intensity, digital subsea control, intervention support, and offshore vessel availability. SLB, Halliburton, Baker Hughes, and TechnipFMC all expanded or reinforced positions in one or more of these service layers during 2025 and early 2026.

Technology is changing the Deepwater Drilling Services Market through automation, AI-assisted maintenance, real-time well control support, digital completions, and subsea production intelligence. Operators now favor larger service bundles tied to recovery improvement, uptime, and lower intervention risk. AI is tightening execution, reducing unplanned downtime, and improving reservoir control in complex wells.

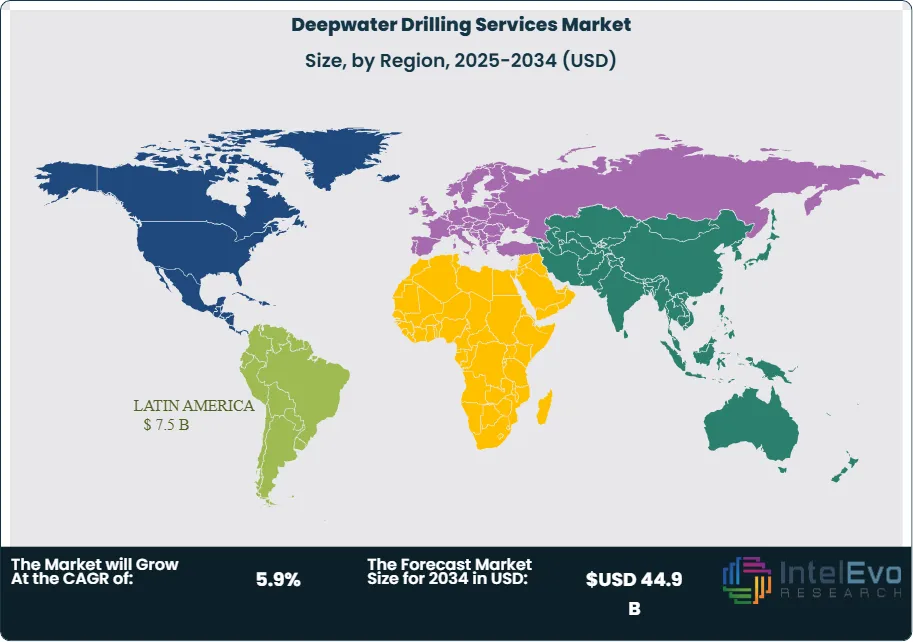

Regionally, Latin America held 28.0% of the Deepwater Drilling Services Market in 2025, equal to USD 7.5 Billion, supported by Brazil’s pre-salt and post-salt programs. North America held 24.0%, or USD 6.4 Billion, backed by the U.S. Gulf. Middle East and Africa accounted for 20.0%, or USD 5.4 Billion, driven by Nigeria, Angola, Namibia, Saudi Arabia, and the UAE. Asia Pacific represented 16.0%, or USD 4.3 Billion, while Europe held 12.0%, or USD 3.2 Billion. Regulatory pressure now centers on local content, emissions, subsea integrity, and offshore safety. Risk remains tied to oil price swings, project delays, and contractor concentration, but the 2025 demand base was strong enough to support a constructive long-range outlook.

, By Water Depth, By End Use (Development Drilling, Exploration and Appraisal Services, Production Support and Late-Life Well Services), By Contract Model, Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Deepwater Drilling Services Market stood at USD 26.8 Billion in 2025 and is projected to reach USD 44.9 Billion by 2034 at a 5.9% CAGR during 2025-2034. The growth path reflects deeper offshore development pipelines, broader subsea service scope, and stronger completion intensity in Brazil, the U.S. Gulf, and West Africa.

- Segment Dominance: By service type, well construction and drilling management services led with 32.0% share in 2025, equal to USD 8.6 Billion. The segment stayed ahead because every deepwater development requires drilling engineering, directional tools, drilling fluids support, cementing, and wellbore execution before subsea tieback and production work begins.

- Segment Dominance: By end use, development drilling held the largest share at 57.0% in 2025, or USD 15.3 Billion. The market favored development programs over frontier exploration because reserve risk is lower and project economics are clearer.

- Driver: The main driver is multi-year offshore project sanctioning and expansion. Strong Gulf of America momentum into 2026 and large planned deepwater investment in Nigeria lifted multi-year service demand.

- Restraint: The key restraint is service pricing pressure when operators delay awards or rebid scopes. Offshore contractors continued to respond to uneven utilization and pricing by consolidating fleets and service exposure.

- Opportunity: The largest opportunity sits in Brazil, Guyana, Namibia, Malaysia, and the eastern Mediterranean. These basins can add more than USD 7.0 Billion of incremental addressable deepwater drilling services demand between 2025 and 2034.

- Trend: Integrated subsea and completion packages form the clearest trend. Back-to-back Petrobras, ExxonMobil Guyana, and PTTEP awards show a shift toward bundled offshore execution and stronger digital control.

- Regional Analysis: Latin America led the Deepwater Drilling Services Market with 28.0% share and USD 7.5 Billion revenue in 2025. Brazil remained the core revenue engine due to its dense pipeline of pre-salt deepwater developments and related completion, subsea, and drilling service demand.

Competitive Landscape

The Deepwater Drilling Services Market is moderately consolidated. The top four companies controlled an estimated 41.0% of 2025 market revenue. Competition is technology-driven and platform-based, with scale in well construction, subsea production systems, intelligent completions, and integrated project execution shaping share more than pure pricing. Competitive intensity rose in 2025 and early 2026 as operators favored larger service bundles, while Saipem and Subsea7 agreed to combine and Transocean moved to acquire Valaris, confirming broader offshore consolidation pressure.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| SLB | US | Leader | OneSubsea integrated subsea production systems | North America, Middle East, Southeast Asia | Won PTTEP EPC contracts offshore Malaysia in Oct 2025 and bp Tiber subsea boosting work in Nov 2025. |

| HALLIBURTON | US | Leader | SmartWell and deepwater completion services | Latin America, North America, West Africa | Won Petrobras deepwater completion and stimulation contracts in Brazil in Oct 2025. |

| BAKER HUGHES | US | Leader | Subsea tree systems and integrated well construction services | Brazil, North America, Africa | Won Petrobras subsea tree systems and associated services award in Sep 2025. |

| TECHNIPFMC | UK | Leader | iEPCI and subsea production systems | Latin America, Guyana, global deepwater | Won Petrobras and ExxonMobil Guyana subsea contracts in Sep 2025. |

| SUBSEA7 | Luxembourg | Challenger | Subsea installation and SURF services | Europe, Middle East, Africa | Agreed merger with Saipem in Feb 2025 and extended Sakarya work in Mar 2026. |

| SAIPEM | Italy | Challenger | Deepwater SURF and offshore EPC | Middle East, Mediterranean, Africa | Won offshore Qatar contract worth about USD 4 Billion in Dec 2025. |

| OCEANEERING INTERNATIONAL | US | Challenger | ROV, intervention, and vessel-based offshore projects | North America, global deepwater support | Announced vessel services agreement for Harvey Deep Sea in Jun 2025. |

| TRANSOCEAN | Switzerland | Niche Player | Ultra-deepwater rig services | U.S. Gulf, Brazil, West Africa | Announced Valaris acquisition in Feb 2026 to expand offshore capability. |

| SEADRILL | Bermuda | Niche Player | Premium drillship services | Brazil, Southeast Asia | Added USD 0.5 Billion of backlog across seven rigs in Feb 2026. |

| VALARIS | Bermuda | Niche Player | Deepwater drillship services | Brazil, Australia, U.S. Gulf | Added around USD 900 Million of backlog by Feb 2026. |

By Service Type

Well construction and drilling management services accounted for 32.0% of the Deepwater Drilling Services Market in 2025, or USD 8.6 Billion. This segment includes drilling engineering, directional drilling, drilling fluids support, cementing, wireline support tied to drilling, and well execution management. It leads because it sits at the front of every deepwater well cycle and anchors project control. The segment performs best in Brazil, the U.S. Gulf, and multi-well deepwater developments where service continuity and execution quality matter more than single-line pricing.

Subsea production systems and SURF services held 29.0%, or USD 7.8 Billion, driven by TechnipFMC, SLB OneSubsea, Baker Hughes, Subsea7, and Saipem. Completion, stimulation, and intervention services represented 23.0%, or USD 6.2 Billion, supported by Petrobras awards and rising intelligent completion adoption. ROV, inspection, and vessel-based support services held the remaining 16.0%, or USD 4.3 Billion, with Oceaneering and other specialists strongest in this layer.

By Water Depth

Deepwater services led with 54.0% share in 2025, equal to USD 14.5 Billion. This segment covers water depths below ultra-deepwater thresholds but still requires premium offshore execution, subsea tieback capability, and advanced completions. It stayed ahead because a large portion of Brazil, West Africa, and Gulf work remains in the deepwater band even when headline attention shifts to ultra-deepwater discoveries.

Ultra-deepwater services held 34.0%, or USD 9.1 Billion, and carry the fastest structural growth rate because discoveries and seismic campaigns are pushing farther offshore. Harsh-environment deepwater services represented 12.0%, or USD 3.2 Billion, centered on Norway and other demanding offshore basins where weather, emissions performance, and safety requirements create higher technical barriers.

By End Use

Development drilling dominated with 57.0% share in 2025, or USD 15.3 Billion. The market now favors reserve development, infill wells, and production optimization over pure frontier exploration. Development work sustains multi-well service packages that combine drilling management, subsea systems, completions, and intervention planning.

Exploration and appraisal services held 26.0%, equal to USD 7.0 Billion. This segment remains strategically important because Namibia, Guyana-adjacent acreage, Trinidad and Tobago, and selected African basins can create the next wave of long-cycle awards. Production support, intervention, and late-life well services represented 17.0%, or USD 4.6 Billion, and are gaining ground as offshore fields mature and operators focus on uptime, recovery improvement, and subsea integrity.

By Contract Model

Integrated service contracts accounted for 46.0% of the Deepwater Drilling Services Market in 2025, or USD 12.3 Billion. Operators increasingly bundle well construction, subsea hardware, completions, stimulation, installation, and digital control under broader contract structures. This is the most important commercial shift in the market.

Standalone service contracts held 31.0%, or USD 8.3 Billion, and remain important where operators split scopes for procurement or technical reasons. Performance-linked and digital-enhanced contracts represented 23.0%, or USD 6.2 Billion, and should grow fastest through 2034 as offshore operators demand stronger alignment around uptime, intervention avoidance, and recovery performance.

Regional Analysis

North America Deepwater Drilling Services Market

North America held 24.0% of the Deepwater Drilling Services Market in 2025, equal to USD 6.4 Billion. The United States led the region, followed by Mexico and Canada. The U.S. Gulf of America remained the anchor and supported a dense pipeline of drilling, completion, subsea, and intervention services. SLB, Halliburton, Baker Hughes, TechnipFMC, Oceaneering, and leading rig contractors all have strong regional exposure.

North America is one of the most technically mature deepwater service markets. It combines strong infrastructure, advanced service fleets, digital offshore operations, and high operator familiarity with integrated contracting. Regulatory risk remains present, but the basin’s economics remain attractive enough to sustain premium service activity through 2034.

Europe Deepwater Drilling Services Market

Europe accounted for 12.0% of the Deepwater Drilling Services Market in 2025, or USD 3.2 Billion. Norway led the region, followed by the UK, Germany, and the Netherlands. Norway is the main profit center because harsh-environment deepwater and subsea work require premium engineering and stronger emissions performance.

Europe is the most regulation-heavy regional market. Emissions scrutiny, offshore integrity standards, and safety rules shape contract awards and favor suppliers with strong documentation, subsea engineering depth, and harsh-environment operating records. Growth stays moderate, but Europe remains an important premium market for subsea compression, tieback upgrades, brownfield deepwater support, and digitally monitored offshore operations.

Asia Pacific Deepwater Drilling Services Market

Asia Pacific held 16.0% of the Deepwater Drilling Services Market in 2025, equal to USD 4.3 Billion. China, India, Malaysia, and Australia formed the most relevant country set. Malaysia stood out in late 2025 after SLB OneSubsea won EPC contracts from PTTEP, while offshore gas service momentum also strengthened elsewhere in the region.

Asia Pacific combines shallow-water scale with selective deepwater growth. The region’s advantage is gas demand. Offshore gas developments create long-duration service opportunities across subsea systems, installation, completions, and intervention support. Asia Pacific should be one of the fastest-growing regional markets through 2034.

Latin America Deepwater Drilling Services Market

Latin America represented 28.0% of the Deepwater Drilling Services Market in 2025, or USD 7.5 Billion. Brazil dominated the region, followed by Mexico, Guyana, and Argentina. Brazil is the market’s single most important deepwater service center and remained active across completions, subsea systems, and deepwater development awards in 2025.

The region benefits from large reserve bases, strong multi-year project visibility, and high service intensity per well. Guyana remains smaller today in absolute revenue, but recent awards confirm its rapid strategic rise. Latin America should remain the top regional market through much of the forecast period because the service stack in Brazil is both broad and high value.

Middle East & Africa Deepwater Drilling Services Market

Middle East and Africa held 20.0% of the Deepwater Drilling Services Market in 2025, equal to USD 5.4 Billion. Saudi Arabia, the UAE, South Africa, and Namibia were the most relevant strategic countries, while Nigeria and Angola remained major service centers inside the broader region. The region mixes stable national oil company demand with high-upside frontier work.

Political and tender risk remain real, but the long-term direction is positive because reserve replacement needs are high and offshore discoveries continue to expand the addressable service base. Middle East and Africa should post one of the strongest growth rates through 2034, especially if Namibia and additional West African deepwater programs convert into development-scale work.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Well Construction and Drilling Management Services

- Subsea Production Systems and SURF Services

- Completion, Stimulation, and Intervention Services

- ROV, Inspection, and Vessel-Based Support Services

By Water Depth

- Deepwater Services

- Ultra-Deepwater Services

- Harsh-Environment Deepwater Services

By End Use

- Development Drilling

- Exploration and Appraisal Services

- Production Support, Intervention, and Late-Life Well Services

By Contract Model

- Integrated Service Contracts

- Standalone Service Contracts

- Performance-Linked and Digital-Enhanced Contracts

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 26.8 B |

| Forecast Revenue (2034) | USD 44.9 B |

| CAGR (2025-2034) | 5.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type (Well Construction and Drilling Management Services, Subsea Production Systems and SURF Services, Completion, Stimulation, and Intervention Services, ROV, Inspection, and Vessel-Based Support Services), By Water Depth (Deepwater Services, Ultra-Deepwater Services, Harsh-Environment Deepwater Services), By End Use (Development Drilling, Exploration and Appraisal Services, Production Support, Intervention, and Late-Life Well Services), By Contract Model (Integrated Service Contracts, Standalone Service Contracts, Performance-Linked and Digital-Enhanced Contracts) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, TECHNIPFMC, SUBSEA7, SAIPEM, OCEANEERING INTERNATIONAL, TRANSOCEAN, SEADRILL, VALARIS, AKER SOLUTIONS, ONE SUBSEA, DRIL-QUIP, WEATHERFORD, HELIX ENERGY SOLUTIONS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Water Depth, By End Use (Development Drilling, Exploration and Appraisal Services, Production Support and Late-Life Well Services), By Contract Model, Industry Trends & Forecast 2026–2034")

, By Water Depth, By End Use (Development Drilling, Exploration and Appraisal Services, Production Support and Late-Life Well Services), By Contract Model, Industry Trends & Forecast 2026–2034")

, By Water Depth, By End Use (Development Drilling, Exploration and Appraisal Services, Production Support and Late-Life Well Services), By Contract Model, Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Deepwater Drilling Services Market?

The Global Deepwater Drilling Services Market was valued at USD 25.2 Billion in 2024 and USD 26.8 Billion in 2025, projected to reach USD 44.9 Billion by 2034 at a CAGR of 5.9% from 2026–2034. Market growth is driven by rising offshore exploration investments, increasing deepwater and ultra-deepwater drilling projects, and advancements in offshore drilling technologies.

Who are the major players in the Deepwater Drilling Services Market?

SLB, HALLIBURTON, BAKER HUGHES, TECHNIPFMC, SUBSEA7, SAIPEM, OCEANEERING INTERNATIONAL, TRANSOCEAN, SEADRILL, VALARIS, AKER SOLUTIONS, ONE SUBSEA, DRIL-QUIP, WEATHERFORD, HELIX ENERGY SOLUTIONS, Others

Which segments covered the Deepwater Drilling Services Market?

By Service Type (Well Construction and Drilling Management Services, Subsea Production Systems and SURF Services, Completion, Stimulation, and Intervention Services, ROV, Inspection, and Vessel-Based Support Services), By Water Depth (Deepwater Services, Ultra-Deepwater Services, Harsh-Environment Deepwater Services), By End Use (Development Drilling, Exploration and Appraisal Services, Production Support, Intervention, and Late-Life Well Services), By Contract Model (Integrated Service Contracts, Standalone Service Contracts, Performance-Linked and Digital-Enhanced Contracts)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Deepwater Drilling Services Market

Published Date : 13 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date