- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

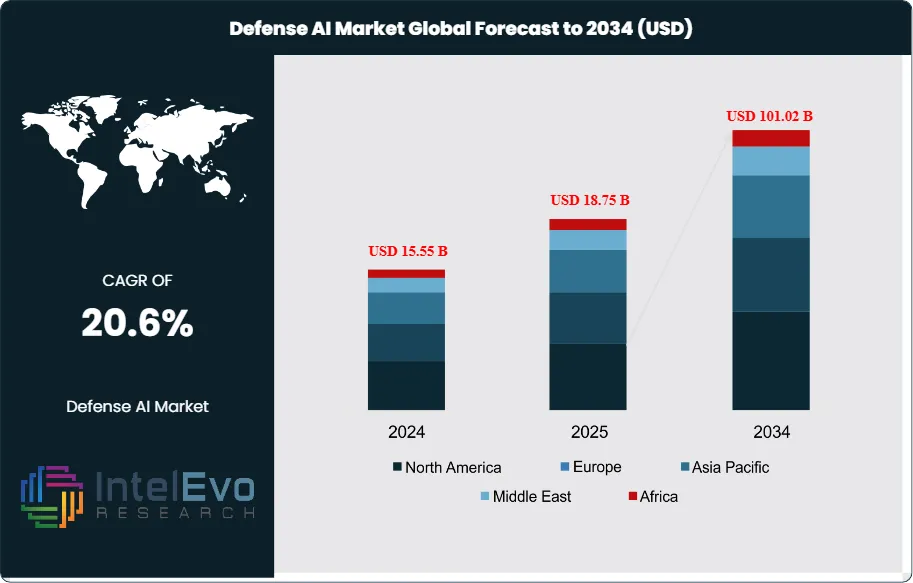

Global Defense AI Market Size, Share & Forecast 2034 | CAGR 20.6%

Global Defense AI Market Size, Share, Analysis By Component (Hardware, Software, Services), By Technology (Machine Learning, Deep Learning, Computer Vision, Natural Language Processing, Generative AI, Edge AI, Reinforcement Learning), By Application (ISR, Cybersecurity, Command & Control, Autonomous Combat Systems, Predictive Maintenance, Electronic Warfare), By Platform (Land, Naval, Airborne, Space, Unmanned Systems) Industry Trends, Competitive Landscape & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 18.75 Billion | USD 101.02 Billion | 20.6% | North America, 40.4% |

The Defense AI Market was valued at approximately USD 15.55 Billion in 2024 and reached USD 18.75 Billion in 2025. The market is projected to grow to USD 101.02 Billion by 2034, expanding at a CAGR of 20.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 82.27 Billion over the analysis period. The Defense AI Market covers the commercial space for artificial intelligence software, autonomous systems, computer vision, natural language processing, machine learning, and decision-support platforms procured by defense ministries, armed forces, intelligence agencies, and defense contractors for military applications.

Get More Information about this report -

Request Free Sample ReportDemand growth is anchored in sharply rising defense expenditure and geopolitical tensions. Global military spending reached USD 2.44 trillion in 2023 per the Stockholm International Peace Research Institute (SIPRI), rising 6.8% year-over-year. U.S. Department of War (formerly Department of Defense) FY2025 base budget reached USD 849.8 billion, with the Chief Digital and Artificial Intelligence Office (CDAO) accelerating AI procurement cycles. NATO allies committed to 2% of GDP defense spending targets at the Vilnius Summit of July 2023, with several European states moving toward 3% GDP targets through 2026 under the Hague Declaration framework. Ukraine's use of AI-enabled drones, Shield AI V-BAT, Anduril Altius, and Palantir Maven platforms demonstrated battlefield validation that shifted global procurement behavior through 2024-2025.

Capital deployment into the Defense AI Market accelerated sharply through 2024-2025. Defense tech startups raised USD 49.1 billion in 2025, nearly double the USD 27.2 billion raised in 2024. Anduril Industries reached a USD 30.5 billion valuation in 2025 and is raising up to USD 8 billion at an estimated USD 60 billion valuation. Shield AI reached a USD 5.6 billion valuation in 2025 following a USD 300 million extension round, with USD 300 million in 2025 revenue. Helsing reached a EUR 12 billion valuation. Palantir Technologies' market capitalization exceeded USD 370 billion through 2025, surpassing Lockheed Martin. The U.S. Department of War increased Palantir's Maven Smart System contract ceiling to USD 1.3 billion through 2029 in May 2025, up from the initial USD 480 million five-year IDIQ of May 2024.

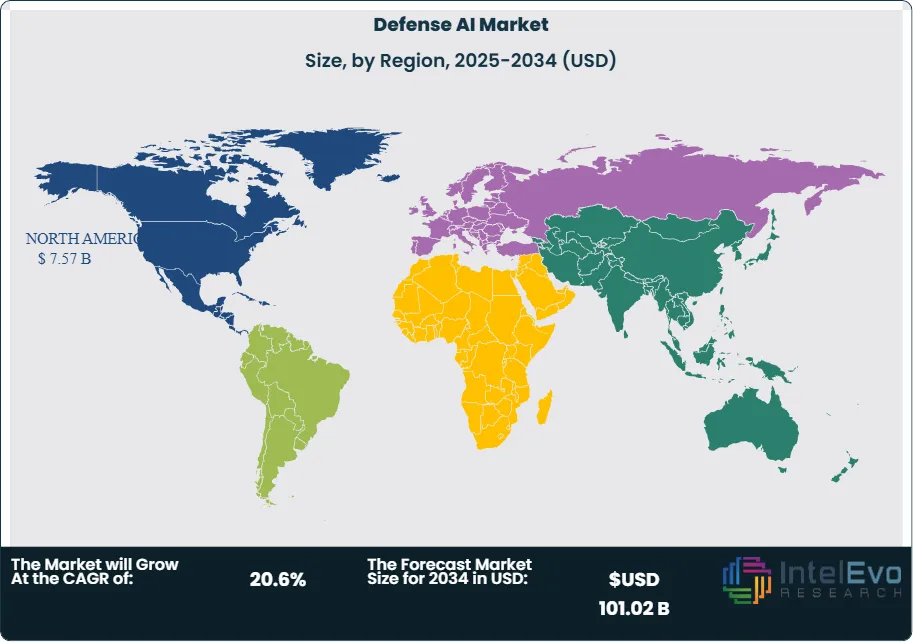

North America held 40.4% of global Defense AI Market revenue in 2025, equivalent to USD 7.57 Billion, with the United States contributing 94% of the regional share. The U.S. Department of War has become the largest single Defense AI buyer globally through programs including Maven Smart System, the Joint All-Domain Command and Control (JADC2) initiative, the Replicator autonomous drone program, and the Golden Dome USD 185 billion missile defense shield. Europe captured approximately 27% share, driven by the NATO DIANA innovation accelerator, European Defence Fund (EDF) investments, and national AI defense strategies from France (AMIAD), Germany, and the United Kingdom. Asia Pacific held 20% share and is projected to grow fastest at approximately 24% CAGR through 2034.

Forward visibility through 2034 rests on three catalysts. First, the U.S. Golden Dome missile defense initiative of May 2025 committed USD 185 billion to a space-based AI-driven integrated air and missile defense system, with Anduril, Palantir, SpaceX, and RTX among the initial contractors. Second, Palantir's Maven Smart System was designated an official program of record in 2025, providing stable long-term funding and streamlined adoption across all military branches, with more than 20,000 active users across 35+ tools by mid-2025. Third, the NATO Maven Smart System NATO deployment extends U.S. defense AI software into the Allied Command Operations strategic command. These forces together support the 20.6% forecast CAGR in the Defense AI Market through 2034.

Market Definition & Scope

The Defense AI Market is defined as the commercial space for artificial intelligence and machine learning software, hardware, and services procured for military, defense, and national security applications. The market encompasses seven core technology categories: machine learning and deep learning platforms, computer vision for intelligence-surveillance-reconnaissance (ISR), natural language processing for signals intelligence, autonomous systems and autonomous weapons, predictive maintenance, logistics and supply chain AI, and AI-enabled cybersecurity for defense networks.

This analysis includes AI software licenses, AI-enabled hardware platforms procured as modernized weapons systems, autonomous unmanned aerial, ground, surface, and underwater vehicles with embedded AI pilots, integrated AI modules within sixth-generation fighter programs (NGAD, GCAP, FCAS), and associated AI consulting and integration services. The scope explicitly excludes generic enterprise IT spending without AI capability, legacy non-AI weapons systems, training simulators without adaptive AI, and commercial cloud services procured for non-AI workloads. The parent global defense market reached approximately USD 2.44 trillion in 2023 per SIPRI, with the Defense AI segment representing approximately 0.8% of total defense spending in 2025, projected to reach 3% of parent spending by 2034.

, By Technology (Machine Learning, Deep Learning, Computer Vision, Natural Language Processing, Generative AI, Edge AI, Reinforcement Learning), By Application (ISR, Cybersecurity, Command & Control, Autonomous Combat Systems, Predictive Maintenance, Electronic Warfare), By Platform (Land, Naval, Airborne, Space, Unmanned Systems) Industry Trends, Competitive Landscape & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Defense AI Market grew from USD 18.75 Billion in 2025 to a projected USD 101.02 Billion in 2034, expanding at a 20.6% CAGR.

- Segment Dominance (By Component): Hardware held the largest share in 2025 at approximately 48% revenue share, anchored by AI-enabled sensor platforms, autonomous drones, and edge AI compute on tactical systems.

- Segment Dominance (By Application): Warfare applications including targeting, autonomous weapons, and battlefield command and control led revenue share in 2025 at approximately 32%.

- Driver: Global military spending rose 6.8% to USD 2.44 trillion in 2023 per SIPRI, with defense tech startups raising USD 49.1 billion in 2025, nearly double the USD 27.2 billion raised in 2024.

- Restraint: Algorithmic accountability, ethical AI concerns, and U.S. Department of War Directive 3000.09 on Autonomy in Weapon Systems (updated January 2023) constrain fully autonomous lethal AI deployment.

- Opportunity: The U.S. Golden Dome missile defense initiative announced in May 2025 committed USD 185 billion to an AI-driven space-based integrated air and missile defense system.

- Trend: Palantir's Maven Smart System was designated an official program of record in 2025, with active users exceeding 20,000 across 35+ military tools by mid-2025, more than doubling since January 2025.

- Regional: North America held 40.4% revenue share in 2025 at USD 7.57 Billion, with the United States contributing approximately 94% of the regional share.

Key Insights Summary

- The U.S. Department of War increased Palantir's Maven Smart System contract ceiling to USD 1.3 billion through 2029 in May 2025, up from the initial USD 480 million five-year IDIQ signed in May 2024, reflecting more than doubling of active users in the first half of 2025.

- Anduril Industries won a contract worth up to USD 20 billion from the U.S. Army in 2025 to integrate commercial technologies into a unified AI-driven operational system, and is raising up to USD 8 billion at an estimated USD 60 billion valuation.

- The Trump Administration announced the Golden Dome missile defense initiative in May 2025, committing USD 185 billion to a space-based AI-driven integrated air and missile defense system with Anduril, Palantir, SpaceX, and RTX among initial contractors.

- Shield AI reached a USD 5.6 billion valuation in 2025 following a USD 300 million extension round, with USD 300 million in 2025 revenue, backed by Palantir, Airbus, Lockheed Martin, L3Harris, Andreessen Horowitz, and Point72.

- Defense tech startups raised USD 49.1 billion in 2025, nearly double the USD 27.2 billion raised in 2024, with Anduril at USD 30.5 billion valuation and Helsing at EUR 12 billion leading the neoprime cohort.

- Palantir signed a deal with NATO in 2025 for Maven Smart System NATO, supporting the Allied Command Operations strategic command and extending U.S. defense AI software into allied operational environments.

- Global military spending reached USD 2.44 trillion in 2023 per SIPRI, rising 6.8% year-over-year, with NATO allies committing to 2% of GDP defense spending targets and several European states moving toward 3% GDP targets through 2026.

Competitive Landscape Overview

The Defense AI Market is moderately concentrated with the top 10 players accounting for approximately 28.5% of the market in 2023 per The Business Research Company. Competition is structured across three tiers: legacy defense primes including Lockheed Martin, Northrop Grumman, RTX, BAE Systems, Boeing, and General Dynamics which collectively hold 35 to 45% of AI-enabled hardware and mission-system awards across NATO markets per SIPRI procurement data; software-first specialists led by Palantir (20-25% of identifiable U.S. AI software obligations in FY2023-FY2024) and Booz Allen Hamilton (10-12%); and neoprime autonomy specialists led by Anduril Industries, Shield AI, Helsing, Saronic Technologies, and Chaos Industries.

Competitive dynamics shifted sharply through 2024-2025 as primes and neoprimes moved from competition to collaboration. Palantir and Anduril announced a strategic partnership in December 2024 combining Palantir's Maven data processing platform with Anduril's Lattice mesh networking for drone swarming and battlefield data fusion. Shield AI, Palantir, and Anduril formed a consortium pitching jointly for defense contracts including Golden Dome. Anduril partnered with Oracle for cloud infrastructure, with Archer for hybrid-propulsion aircraft, and with SpaceX for space-layer integration. Safran acquired Preligens (rebranded Safran.AI) for USD 244 million in September 2023 to build European AI defense capability. Hensoldt, Helsing, and Thales anchor European defense AI sovereignty under the European Defence Fund framework.

Competitive Landscape Matrix

| Company | HQ | Position | Key Platform | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Palantir Technologies Inc. | Denver, CO, USA | Leader (Software) | Maven Smart System; Gotham; AIP (AI Platform) | Global (NATO) | DoD increased Maven Smart System contract ceiling to USD 1.3B in May 2025; USD 10B Army enterprise agreement 2025 |

| Anduril Industries, Inc. | Costa Mesa, CA, USA | Leader (Neoprime) | Lattice AI command and control; autonomous systems | United States, Allies | Won up to USD 20B U.S. Army contract in 2025; raising USD 8B at USD 60B valuation |

| Lockheed Martin Corporation | Bethesda, MD, USA | Leader (Prime) | AI-enabled platforms; Skunk Works autonomy; F-35 data fusion | Global | Continued AI integration across F-35 and hypersonic programs through FY2025 |

| Northrop Grumman Corporation | Falls Church, VA, USA | Leader (Prime) | Autonomous mission systems; MQ-4C Triton AI; B-21 Raider | Global | Continued B-21 Raider AI integration and IBCS command system expansion 2025 |

| RTX Corporation (Raytheon) | Arlington, VA, USA | Leader (Prime) | AI-enabled missile defense; Collins Aerospace autonomy | Global | Continued Golden Dome missile defense integration alongside Anduril and Palantir 2025 |

| BAE Systems plc | London, United Kingdom | Leader (Prime) | AI mission systems; Typhoon/F-35 data fusion | Europe, Global | Continued Tempest/GCAP AI integration and UK defense AI program expansion 2025 |

| Shield AI, Inc. | San Diego, CA, USA | Challenger (Neoprime) | Hivemind autonomy; V-BAT drone; X-BAT fighter | United States, Allies | Raised USD 300M extension reaching USD 5.6B valuation in 2025; USD 300M revenue 2025 |

| Thales Group | Paris, France | Challenger (Prime) | cortAIx AI factory; Syracuse 4 AI; sensor fusion | Europe, Global | Continued cortAIx AI factory expansion and European defense AI program participation 2025 |

| Helsing GmbH | Munich, Germany | Challenger (Neoprime) | Altra AI; Saab Gripen integration; HX-2 munition | Europe (NATO) | Reached EUR 12B valuation in 2025 with continued Ukraine deployment and European contracts |

| International Business Machines Corp. | Armonk, NY, USA | Niche (Software) | Watsonx for defense; AI infrastructure | Global | Continued expansion of Watsonx enterprise AI for defense intelligence workflows 2025 |

Segmentation Analysis

The Defense AI Market segments across component, technology, application, platform, and end-user. Procurement leaders building a defense AI procurement checklist should benchmark vendors on model assurance and MLOps maturity, classified cloud and edge deployment options, Five Eyes intelligence sharing compatibility, adversarial robustness testing, and Authority to Operate (ATO) readiness across each segmentation dimension.

By Component

Hardware held the largest revenue share at 48% in 2025, equivalent to approximately USD 9.00 Billion, anchored by AI-enabled sensors, autonomous drones, edge AI compute modules including NVIDIA Jetson and AMD EPYC Embedded, GPU-accelerated servers for classified cloud environments, and ruggedized AI inference appliances. Software held 38% share at USD 7.13 Billion, led by Palantir Gotham, Palantir AIP, Anduril Lattice, Shield AI Hivemind, Helsing Altra AI, and IBM Watsonx for defense intelligence workflows. Services captured 14% share at USD 2.63 Billion, including integration, training, model assurance, and managed AI operations services provided by Booz Allen Hamilton, Accenture Federal Services, Leidos, and defense prime service arms. Per Grand View Research 2024 data, software leads revenue mix at 42.5% in specific defense AI sub-categories.

By Technology

Machine learning and deep learning held the largest technology share at 43% in 2025, providing the underlying framework for computer vision, predictive analytics, and autonomous decision-making. Computer vision captured 22% share, dominated by ISR applications, automated target recognition, and drone-based surveillance. Natural language processing held 17.6% share in 2024 per Global Market Insights, enabling communications monitoring, intelligence triage, and multilingual document analysis for coalition operations. Autonomous systems and robotics captured 10%, context-aware computing 4%, and other technologies including quantum-resilient cryptography and advanced simulation 3% per GMI segment splits. The machine learning segment is expected to maintain the largest share through 2034 as foundation model techniques extend into multi-domain operations.

By Application

Warfare applications including targeting, autonomous weapons, and battlefield command and control led revenue share at 32% in 2025, equivalent to approximately USD 6.00 Billion. Intelligence, surveillance, and reconnaissance (ISR) captured 24% share, supported by Maven Smart System, MQ-4C Triton, and commercial satellite AI fusion. Cybersecurity held 16% share and is projected to grow fastest, driven by AI-enabled SIEM, zero-trust architecture for classified networks, and offensive cyber operations. Logistics and supply chain AI captured 11%, training and simulation 8%, and predictive maintenance 6%. Other applications including battlefield healthcare and soldier monitoring held 3%. The cybersecurity application segment is expected to grow at the fastest CAGR over the forecast period per Precedence Research.

By Platform

Land platforms led platform revenue share at 34% in 2025, reflecting AI integration across the U.S. Army's Next Generation Combat Vehicle, the UK's Ajax, France's Scorpion, Germany's Puma, and Israel's Merkava programs. Airborne platforms captured 28% share, including AI copilots on the F-35 Lightning II, B-21 Raider, MQ-9 Reaper, and Shield AI V-BAT and forthcoming X-BAT platforms. Naval platforms held 19%, anchored by autonomous surface vessels from Saronic Technologies, AI-enabled combat management systems on Aegis and Type 26 platforms, and unmanned underwater vehicles. Space platforms captured 13% and are expected to grow fastest under the Golden Dome program and Space Development Agency Proliferated Warfighter Space Architecture. Cyber platform AI captured 6% reflecting dedicated AI cyber defense workload placement.

Regional Analysis

The Defense AI Market divides across North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, with North America leading in 2025 and Asia Pacific growing fastest through 2034.

North America

North America held 40.4% of global Defense AI Market revenue in 2025, equivalent to USD 7.57 Billion, per Fortune Business Insights. The United States contributed approximately 94% of the regional share at USD 7.12 Billion. U.S. Department of War FY2025 base budget reached USD 849.8 billion, and the Chief Digital and Artificial Intelligence Office (CDAO) has accelerated AI procurement cycles. Palantir's Maven Smart System contract ceiling was increased to USD 1.3 billion in May 2025, and Anduril won a USD 20 billion Army contract in 2025. The Replicator autonomous drone initiative targeted USD 500 million in its first tranche. Canada's Department of National Defence committed CAD 8.1 billion to AI and cyber in the 2024 Our North, Strong and Free policy update.

Europe

Europe held 27.0% share in 2025 at approximately USD 5.06 Billion. The European Defence Fund (EDF) committed EUR 8 billion for the 2021-2027 period, with AI as a priority investment area. NATO DIANA launched in 2023 as a deep-tech accelerator across 23 sites in 22 allied countries. France's Ministry of the Armed Forces established AMIAD (Agence Ministerielle pour l'Intelligence Artificielle de Defense) in March 2024 with EUR 2 billion committed through 2030. Germany's Bundeswehr Cyber Innovation Hub and the BAAINBw procurement agency drive Helsing, Quantum Systems, and Hensoldt adoption. The UK Ministry of Defence's Defence Artificial Intelligence Strategy of June 2022 directs investment through the Defence AI Centre. PESCO projects and the Permanent Structured Cooperation framework coordinate Dutch, Italian, Spanish, and Polish AI defense investment.

Asia Pacific

Asia Pacific captured 20.0% share in 2025 at approximately USD 3.75 Billion and is projected to grow fastest at 24% CAGR through 2034. China leads regional adoption, with the People's Liberation Army pursuing algorithmic warfare doctrine and intelligentized warfare concept per the 2019 Defense White Paper. Chinese domestic vendors including SenseTime, Megvii, iFlytek, and state defense conglomerates including NORINCO and CASIC anchor the domestic ecosystem. Japan's Ministry of Defense adopted its first AI policy in 2024 focusing on target detection, logistics support, and cyber defense. South Korea's Defense Acquisition Program Administration (DAPA) committed KRW 3.4 trillion to AI-enabled systems through 2027 under the Defense Innovation 4.0 initiative. Australia's AUKUS Pillar II framework accelerates AI collaboration with the U.S. and UK.

Latin America

Latin America held 5.5% share in 2025 at approximately USD 1.03 Billion, led by Brazil, Mexico, Colombia, and Chile. Brazil's Ministry of Defense SISFRON border monitoring program integrates AI-enabled surveillance, and Embraer's defense and security division deploys AI in Super Tucano and C-390 Millennium programs. Mexico's Secretaria de la Defensa Nacional (SEDENA) procurement supports AI-enabled border surveillance. Colombia's continued counter-narcotics operations drive AI-enabled ISR procurement. Regional growth is constrained by foreign exchange volatility and competing fiscal priorities, though multinational defense contractor subsidiaries and Israeli vendor partnerships sustain baseline procurement.

Middle East & Africa

The Middle East & Africa region held 7.1% share in 2025 at approximately USD 1.33 Billion, anchored by Saudi Arabia, the United Arab Emirates, Israel, Turkey, and Egypt. Saudi Arabia's Vision 2030 includes USD 75 billion Public Investment Fund commitments to SAMI (Saudi Arabian Military Industries) and AI defense capability. The UAE's Edge Group consolidates AI defense capability through subsidiaries including ADSB, SIGN4L, and Halcon. Israeli vendors Elbit Systems, Israel Aerospace Industries (IAI), and Rafael Advanced Defense Systems supply global markets with AI-enabled air defense (Iron Dome, David's Sling), loitering munitions, and C4ISR. Turkey's Aselsan and Baykar lead TB2 and Kizilelma autonomous platform development. The region is projected to grow at approximately 23% CAGR through 2034.

Country Analysis

The Defense AI Market concentrates in four national markets that together contribute more than 70% of 2025 global revenue: the United States, China, the United Kingdom, and France.

United States

The United States generated approximately USD 7.12 Billion in Defense AI Market revenue in 2025 and is projected to grow at a country CAGR of 21.0% through 2034. The U.S. Department of War FY2025 base budget reached USD 849.8 billion, with approximately USD 1.5 billion allocated specifically to AI and machine learning investment per DoD historical allocation. Major programs include Palantir's Maven Smart System (USD 1.3 billion ceiling through 2029), Anduril's USD 20 billion Army operational system contract, the Replicator initiative, JADC2, and the Golden Dome USD 185 billion missile defense shield. The Chief Digital and Artificial Intelligence Office (CDAO) and the Defense Innovation Unit (DIU) accelerate procurement. Major buyers include the U.S. Army, Navy, Air Force, Space Force, Marine Corps, National Geospatial-Intelligence Agency (NGA), and combatant commands including INDOPACOM and EUCOM.

China

China contributed approximately USD 2.25 Billion in Defense AI Market revenue in 2025, with a country CAGR of 24.5% through 2034. The People's Liberation Army (PLA) pursues intelligentized warfare doctrine articulated in the 2019 Defense White Paper. The 14th Five-Year Plan committed significant funding to military-civil fusion (MCF) AI development under the Central Military Commission Science and Technology Committee. Domestic defense AI vendors include state conglomerates NORINCO, CASIC, and AVIC, alongside tech firms SenseTime, Megvii, and iFlytek under varying degrees of U.S. Entity List designation. The PLA Strategic Support Force integrates AI across cyber, space, and electronic warfare operations. Regional territorial disputes drive sustained AI-enabled ISR, maritime surveillance, and counter-stealth investment.

United Kingdom

The United Kingdom accounted for approximately USD 1.48 Billion in Defense AI Market revenue in 2025, with a projected country CAGR of 20.8% through 2034. The UK Ministry of Defence Defence Artificial Intelligence Strategy of June 2022 commits investment through the Defence AI Centre. The Defence Science and Technology Laboratory (Dstl) and Defence Equipment and Support (DE&S) anchor procurement. The Global Combat Air Programme (GCAP) partnership with Italy and Japan integrates AI across the sixth-generation fighter. BAE Systems, QinetiQ, Babcock International, and Leonardo UK lead domestic integration, while U.S. vendors Palantir, Anduril, and Shield AI serve UK forces through Five Eyes and Defence Technology Exploitation Programme (DTEP) pathways. Major UK buyers include the Royal Navy, British Army, Royal Air Force, and GCHQ.

France

France generated approximately USD 1.12 Billion in Defense AI Market revenue in 2025, with a country CAGR of 21.5% through 2034. The French Ministry of the Armed Forces established AMIAD in March 2024, committing EUR 2 billion to defense AI through 2030 under the Military Programming Law (LPM) 2024-2030 totaling EUR 413 billion. Thales Group's cortAIx AI factory, Dassault Aviation's Rafale AI integration, Safran.AI (formerly Preligens acquired for USD 244 million in September 2023), MBDA, Airbus Defence and Space, and Naval Group anchor domestic capability. The Future Combat Air System (FCAS) partnership with Germany and Spain integrates AI as a core pillar of the sixth-generation fighter. Major French buyers include the Armee de l'Air et de l'Espace, Armee de Terre, and Marine Nationale.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Component

- Hardware

- AI Processors & Accelerators

- Sensors & Imaging Systems

- Edge Computing Devices

- Communication & Networking Equipment

- Software

- AI Platforms & Frameworks

- Decision Support Systems

- Intelligence Analysis Software

- Autonomous Mission Software

- Cyber Defense Solutions

- Services

- Consulting & Strategy Services

- System Integration Services

- Training & Simulation Services

- Maintenance & Support Services

By Technology

- Machine Learning (ML)

- Deep Learning & Neural Networks

- Natural Language Processing (NLP)

- Computer Vision

- Autonomous Systems & Robotics

- Predictive Analytics

- Edge AI

- Generative AI & Large Language Models (LLMs)

- Reinforcement Learning

- Explainable AI (XAI)

By Application

- Intelligence, Surveillance & Reconnaissance (ISR)

- Autonomous Weapons & Combat Systems

- Cybersecurity & Threat Detection

- Command & Control (C2)

- Logistics & Supply Chain Optimization

- Predictive Maintenance

- Battlefield Healthcare & Medical Support

- Training & Simulation

- Target Recognition & Identification

- Electronic Warfare

By Platform

- Land-Based Defense Systems

- Naval Defense Systems

- Airborne Defense Systems

- Space-Based Defense Systems

- Unmanned Systems

- Unmanned Aerial Vehicles (UAVs)

- Unmanned Ground Vehicles (UGVs)

- Unmanned Surface Vehicles (USVs)

- Unmanned Underwater Vehicles (UUVs)

- Soldier-Borne & Wearable Systems

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 18.75 B |

| Forecast Revenue (2034) | USD 101.02 B |

| CAGR (2025-2034) | 20.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Hardware, Software, Services), By Technology, (Machine Learning (ML), Deep Learning & Neural Networks, Natural Language Processing (NLP), Computer Vision, Autonomous Systems & Robotics, Predictive Analytics, Edge AI, Generative AI & Large Language Models (LLMs), Reinforcement Learning, Explainable AI (XAI)), By Application, (Intelligence, Surveillance & Reconnaissance (ISR), Autonomous Weapons & Combat Systems, Cybersecurity & Threat Detection, Command & Control (C2), Logistics & Supply Chain Optimization, Predictive Maintenance, Battlefield Healthcare & Medical Support, Training & Simulation, Target Recognition & Identification, Electronic Warfare), By Platform, (Land-Based Defense Systems, Naval Defense Systems, Airborne Defense Systems, Space-Based Defense Systems, Unmanned Systems, Soldier-Borne & Wearable Systems) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PALANTIR TECHNOLOGIES INC., ANDURIL INDUSTRIES, INC., LOCKHEED MARTIN CORPORATION, NORTHROP GRUMMAN CORPORATION, RTX CORPORATION (RAYTHEON), BAE SYSTEMS PLC, SHIELD AI, INC., THALES GROUP, HELSING GMBH, INTERNATIONAL BUSINESS MACHINES CORP., THE BOEING COMPANY, GENERAL DYNAMICS CORPORATION, L3HARRIS TECHNOLOGIES, INC., LEONARDO S.P.A., AIRBUS DEFENCE AND SPACE, ISRAEL AEROSPACE INDUSTRIES LTD., RAFAEL ADVANCED DEFENSE SYSTEMS LTD., ELBIT SYSTEMS LTD., SAAB AB, SAFRAN ELECTRONICS & DEFENSE (SAFRAN.AI), HENSOLDT AG, SARONIC TECHNOLOGIES, INC., BOOZ ALLEN HAMILTON HOLDING CORPORATION, CHARLES RIVER ANALYTICS INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Machine Learning, Deep Learning, Computer Vision, Natural Language Processing, Generative AI, Edge AI, Reinforcement Learning), By Application (ISR, Cybersecurity, Command & Control, Autonomous Combat Systems, Predictive Maintenance, Electronic Warfare), By Platform (Land, Naval, Airborne, Space, Unmanned Systems) Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Technology (Machine Learning, Deep Learning, Computer Vision, Natural Language Processing, Generative AI, Edge AI, Reinforcement Learning), By Application (ISR, Cybersecurity, Command & Control, Autonomous Combat Systems, Predictive Maintenance, Electronic Warfare), By Platform (Land, Naval, Airborne, Space, Unmanned Systems) Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Technology (Machine Learning, Deep Learning, Computer Vision, Natural Language Processing, Generative AI, Edge AI, Reinforcement Learning), By Application (ISR, Cybersecurity, Command & Control, Autonomous Combat Systems, Predictive Maintenance, Electronic Warfare), By Platform (Land, Naval, Airborne, Space, Unmanned Systems) Industry Trends, Competitive Landscape & Forecast 2026-2034")

Frequently Asked Questions

How big is the Defense AI Market?

The Global Defense AI Market was valued at USD 15.55 Billion in 2024 and is projected to reach USD 101.02 Billion by 2034, growing at a CAGR of 20.6% from 2026 to 2034. Growth is driven by rising defense modernization initiatives, increasing adoption of autonomous military systems, AI-powered intelligence and surveillance capabilities, cybersecurity advancements, predictive maintenance solutions, and the integration of generative AI across land, air, naval, space, and multi-domain defense operations worldwide.

Who are the major players in the Defense AI Market?

PALANTIR TECHNOLOGIES INC., ANDURIL INDUSTRIES, INC., LOCKHEED MARTIN CORPORATION, NORTHROP GRUMMAN CORPORATION, RTX CORPORATION (RAYTHEON), BAE SYSTEMS PLC, SHIELD AI, INC., THALES GROUP, HELSING GMBH, INTERNATIONAL BUSINESS MACHINES CORP., THE BOEING COMPANY, GENERAL DYNAMICS CORPORATION, L3HARRIS TECHNOLOGIES, INC., LEONARDO S.P.A., AIRBUS DEFENCE AND SPACE, ISRAEL AEROSPACE INDUSTRIES LTD., RAFAEL ADVANCED DEFENSE SYSTEMS LTD., ELBIT SYSTEMS LTD., SAAB AB, SAFRAN ELECTRONICS & DEFENSE (SAFRAN.AI), HENSOLDT AG, SARONIC TECHNOLOGIES, INC., BOOZ ALLEN HAMILTON HOLDING CORPORATION, CHARLES RIVER ANALYTICS INC., Others

Which segments covered the Defense AI Market?

By Component, (Hardware, Software, Services), By Technology, (Machine Learning (ML), Deep Learning & Neural Networks, Natural Language Processing (NLP), Computer Vision, Autonomous Systems & Robotics, Predictive Analytics, Edge AI, Generative AI & Large Language Models (LLMs), Reinforcement Learning, Explainable AI (XAI)), By Application, (Intelligence, Surveillance & Reconnaissance (ISR), Autonomous Weapons & Combat Systems, Cybersecurity & Threat Detection, Command & Control (C2), Logistics & Supply Chain Optimization, Predictive Maintenance, Battlefield Healthcare & Medical Support, Training & Simulation, Target Recognition & Identification, Electronic Warfare), By Platform, (Land-Based Defense Systems, Naval Defense Systems, Airborne Defense Systems, Space-Based Defense Systems, Unmanned Systems, Soldier-Borne & Wearable Systems)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date