- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Demineralized Bone Matrix Market Size, Growth & Forecast | CAGR 7.1%

Global Demineralized Bone Matrix Market Size, Share & Industry Analysis By Product Type (Putty, Paste, Gel, Strips/Sheets, Others), By Tissue Source (Allograft, Xenograft), By Application (Spinal Fusion, Trauma, Dental, Foot & Ankle, Others), By End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Academic & Research Institutes) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034

Report Overview

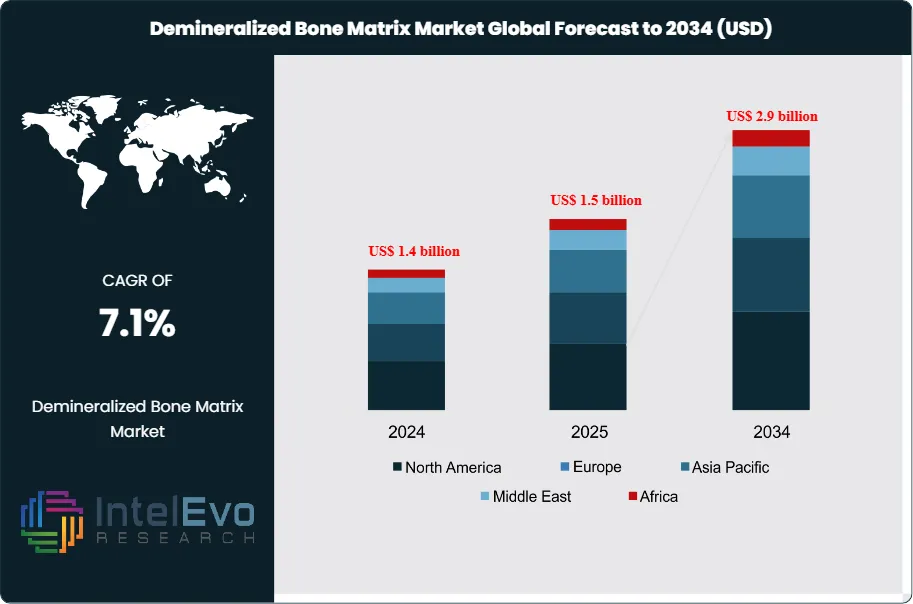

The Demineralized Bone Matrix (DBM) Market is valued at approximately US$ 1.5 billion in 2025 and is projected to reach around US$ 2.9 billion by 2034, expanding at a compound annual growth rate (CAGR) of about 7.1% during the forecast period from 2026 to 2034. Market growth is supported by rising orthopedic trauma cases, increasing spinal fusion procedures, and broader adoption of biologic graft substitutes across hospitals and specialty clinics. In addition, advancements in DBM formulations, growing preference for minimally invasive surgeries, and expanding use in sports medicine and reconstructive procedures are strengthening demand, positioning the market for sustained global expansion.

Get More Information about this report -

Request Free Sample ReportDemand for demineralized bone matrix continues to rise as orthopedic, spinal, and trauma procedures increase worldwide. Surgeons use DBM as a versatile graft substitute in spinal fusion, fracture repair, and reconstructive surgery, supported by its osteoinductive profile and handling characteristics. Growing incidence of musculoskeletal disorders, more road traffic injuries, and greater participation in high-impact sports expand procedure volumes and sustain DBM utilization.

The market shows a tightening supply landscape. Human donor tissue banks and specialized processing firms supply about 70% of DBM volumes, while vertically integrated medtech companies provide the remainder through proprietary lines. Stringent biocompatibility, sterility, and traceability standards in the United States, Europe, and key Asian markets raise barriers to entry but reinforce clinical confidence. Reliance on donor availability, variable tissue quality, and complex cold-chain logistics introduces cost pressure and periodic supply constraints.

Technology-driven differentiation is increasing. Manufacturers apply advanced decontamination, 3D-printed carriers, and nano-structured formulations to improve consistency and graft incorporation. Digitalization and AI-based surgical planning tools support more precise case selection and sizing, which can enhance DBM use per procedure and sharpen inventory management. Automation in processing plants limits batch-to-batch variability and supports scale, though capital intensity and validation requirements extend development timelines.

Risk factors remain material. Competition from synthetic bone grafts, cellular allografts, and growth factor–based biologics may limit price expansion and compress margins, particularly in cost-sensitive health systems. Reimbursement scrutiny, evolving rules on tissue-based products, and any adverse event related to disease transmission or graft failure could slow adoption. Even so, the underlying demand outlook remains positive.

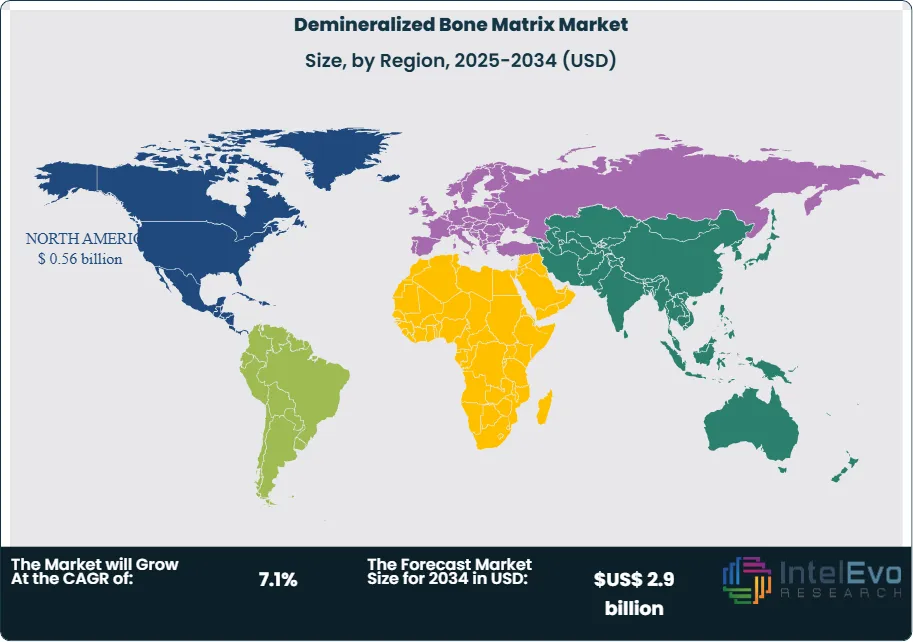

Regionally, North America accounts for an estimated 38% of global revenue in 2024, supported by high surgical volumes and established reimbursement pathways. Europe represents roughly 30%, shaped by large hospital networks and strict tissue governance frameworks. Asia Pacific is the fastest growing region, with a projected CAGR above 8% through 2034 driven by large trauma burdens, expanding private healthcare, and rising investments in local tissue banking and DBM processing capacity. These dynamics position DBM as a core element of future orthopedic and spine care portfolios.

, By Tissue Source (Allograft, Xenograft), By Application (Spinal Fusion, Trauma, Dental, Foot & Ankle, Others), By End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Academic & Research Institutes) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Demineralized Bone Matrix market records revenue of 1.4 billion USD, 2024, US$ 1.5 billion in 2025 and is projected to reach US$ 2.9 billion by 2034, reflecting a CAGR of 7.1%, 2026-2034. This steady expansion indicates resilient procedure demand across orthopedic, spinal, and trauma indications.

- Segment Dominance: Within product types, putty leads the portfolio with a 40.9% share, 2023, as clinicians favor its handling characteristics and versatility in complex cases. Other formats such as paste, gel, and strips/sheets collectively account for the remaining 59.1%, 2023, and continue to serve niche indications.

- Segment Dominance: By tissue source, allograft dominates with a 64.7% share, 2023, while xenograft solutions capture the remaining 35.3%, 2023. In applications, spinal fusion stands as the primary revenue engine with a 45.2% share, 2024, supported by rising procedure volumes.

- Driver: Growing adoption in hospitals, which hold a 52.3% revenue share, 2024, and in high-volume spinal fusion and trauma cases acts as the core demand catalyst. Procedure intensity and rising case complexity in orthopedic centers contribute an additional estimated: 5.0%, 2024 uplift in annual DBM consumption.

- Restraint: Reliance on donor-derived tissue and stringent processing requirements can elevate production and compliance costs by an estimated: 10.0%, 2024 premium versus synthetic substitutes. Fragmented sourcing and regulatory scrutiny on human tissue use may also slow approvals and limit rapid scale-up.

- Opportunity: Underpenetrated indications such as dental, foot and ankle, and outpatient trauma represent a significant expansion pool, with these non-spine segments positioned for an estimated: 7.5%, 2024-2034 CAGR. Targeted portfolio extensions and indication-specific formulations can unlock incremental revenue above the core spine market baseline of 1.4 billion USD, 2024.

- Trend: Clinicians increasingly favor ready-to-use formats, with putty and paste together expected to reach an estimated: 55.0%, 2024 share as workflow optimization gains importance. Hospitals and ambulatory surgical centers shift toward standardized DBM protocols, reinforcing evidence-based product selection and volume purchasing.

- Regional Analysis: North America leads with a 40.2% market share, 2024, driven by high procedure rates and favorable reimbursement. Emerging regions in Asia and Latin America collectively contribute an estimated: 25.0%, 2024 share and are poised to outpace the global CAGR of 6.3%, 2024-2034 as surgical infrastructure expands.

By Type

The product mix in the demineralized bone matrix market continues to shift in 2025 as surgeons increase their use of putty formats. Putty accounted for more than 40 percent of global revenue in the last assessment period and retains its lead due to its moldability and consistent performance in orthopedic, dental, and spine procedures. You see greater demand for putty in cases where irregular defects require a material that conforms easily and supports stable placement.

Growth in this segment aligns closely with the rise in minimally invasive surgery. Surgeons prefer graft materials that they can position accurately with limited exposure, and putty formulations meet this need. Advancements in osteoinductive additives and carrier systems strengthen clinical outcomes, particularly in spinal fusion and dental reconstruction. Paste, gel, and strip formats remain relevant, yet putty is expected to maintain its dominant position as procedure volumes increase across major care settings.

By Application

Spinal fusion continues to anchor overall demand in 2025. The segment represents more than 45 percent of DBM revenue, driven by rising surgical volumes for degenerative disc disease, scoliosis, and age-related instability. DBM plays a central role because it supports bone formation and provides a biologically active environment needed for fusion success. You see stronger adoption in both open and minimally invasive approaches as device makers integrate DBM with new instrumentation systems.

Growth in trauma and foot and ankle applications is also gaining momentum. Higher incidence of fractures in aging populations and a steady rise in sports-related injuries expand the pool of cases requiring grafting solutions. Dental applications remain steady, supported by the global increase in implant procedures. Across all segments, continued refinement of formulations and improved delivery systems strengthen DBM’s position as a preferred biologic option.

By End-Use

Hospitals remain the primary users of DBM products in 2025 with more than half of global revenue attributed to this channel. Complex orthopedic and spine procedures continue to concentrate in hospital settings due to specialized equipment, trained surgical teams, and reimbursement structures that support biologic use. You also see rising procurement volumes as hospitals standardize bone grafting protocols across surgical departments.

Ambulatory surgical centers and orthopedic clinics represent growing end-use environments. As minimally invasive techniques expand, more spine and trauma cases shift into outpatient settings. These facilities prioritize DBM types that offer predictable handling and efficient application. Academic and research institutes maintain consistent demand for developing and validating new formulations, contributing to innovation across the broader market.

By Region

North America leads the global market in 2025 with a share above 40 percent. The region reports a high rate of orthopedic injuries, including more than 3 million sports-related cases annually, which strengthens the need for reliable graft substitutes. Aging demographics further influence demand as osteoporosis and degenerative spinal disorders rise. You also see strong adoption driven by reimbursement support, extensive surgical infrastructure, and active collaboration between device manufacturers and clinical networks.

Europe follows with steady growth supported by large procedural volumes, strong regulatory oversight, and widespread acceptance of biologics in spinal fusion. Asia Pacific shows the fastest trajectory with a double-digit CAGR expected through the next decade. Countries such as China and India expand healthcare capacity, accelerate approvals for biologic materials, and increase investment in orthopedic care. A rapidly growing elderly population and rising medical tourism also contribute to adoption. Latin America and the Middle East and Africa advance at a moderate pace as healthcare modernization and private sector investment improve access to DBM solutions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Product Type

- Putty

- Paste

- Gel

- Strips/Sheets

- Others

Tissue Source

- Xenograft

- Allograft

Application

- Spinal Fusion

- Foot & Ankle

- Trauma

- Dental

- Others

End User

- Hospitals

- Academic & Research Institutes

- Orthopedic Clinics

- Ambulatory Surgical Centers

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | US$ 1.5 billion |

| Forecast Revenue (2034) | US$ 2.9 billion |

| CAGR (2025-2034) | 7.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product Type (Putty, Paste, Gel, Strips/Sheets, Others), Tissue Source (Xenograft, Allograft, Application, Spinal Fusion, Foot & Ankle, Trauma, Dental, Others), End User (Hospitals, Academic & Research Institutes, Orthopedic Clinics, Ambulatory Surgical Centers, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Arthrex Inc, Medtronic Plc, Essent Biologics, Zimmer Biomet, Globus Medical, Ossifix Orthopedics, DePuy Synthes, SeaSpine Holdings Corporation, Stryker |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Tissue Source (Allograft, Xenograft), By Application (Spinal Fusion, Trauma, Dental, Foot & Ankle, Others), By End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Academic & Research Institutes) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

, By Tissue Source (Allograft, Xenograft), By Application (Spinal Fusion, Trauma, Dental, Foot & Ankle, Others), By End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Academic & Research Institutes) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

, By Tissue Source (Allograft, Xenograft), By Application (Spinal Fusion, Trauma, Dental, Foot & Ankle, Others), By End User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Academic & Research Institutes) Industry Region & Key Players – Segment Overview, Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Demineralized Bone Matrix Market?

The global demineralized bone matrix (DBM) market was valued at US$ 1.5 billion in 2025 and is projected to reach US$ 2.9 billion by 2034, growing at a CAGR of 7.1% from 2026 to 2034, driven by rising orthopedic trauma cases, spinal fusion procedures, minimally invasive surgeries, and advances in biologic graft technologies.

Who are the major players in the Demineralized Bone Matrix Market?

Arthrex Inc, Medtronic Plc, Essent Biologics, Zimmer Biomet, Globus Medical, Ossifix Orthopedics, DePuy Synthes, SeaSpine Holdings Corporation, Stryker

Which segments covered the Demineralized Bone Matrix Market?

Product Type (Putty, Paste, Gel, Strips/Sheets, Others), Tissue Source (Xenograft, Allograft, Application, Spinal Fusion, Foot & Ankle, Trauma, Dental, Others), End User (Hospitals, Academic & Research Institutes, Orthopedic Clinics, Ambulatory Surgical Centers, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Demineralized Bone Matrix Market

Published Date : 04 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date