Democratization of AI Market Outlook 2024–2034 | Growth & Trends

Global Democratization of AI Market Size, Share & Analysis By Technology (AI-as-a-Service (AIaaS), No-code Tools, Others), By Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, IT & Telecom, Others), By Deployment Model Industry Outlook, Workforce Transformation Trends & Forecast 2025–2034

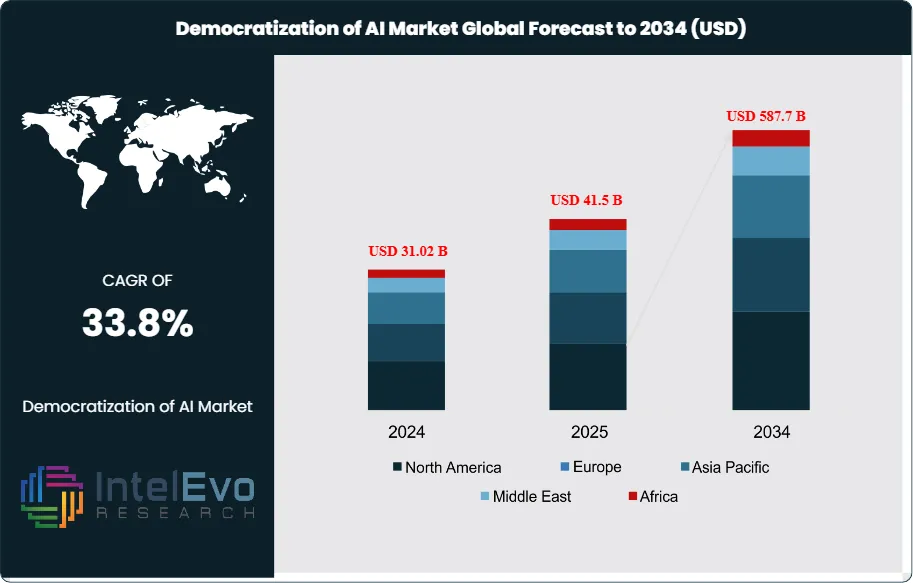

The Democratization of AI market is estimated at USD 31.02 billion in 2024 and is projected to reach approximately USD 587.7 billion by 2034, reflecting an exceptional CAGR of about 33.8% during 2025–2034. The rapid integration of low-code/no-code AI platforms, expanding access to generative AI tools, and enterprise-wide automation initiatives are accelerating adoption at an unprecedented scale. Small and mid-sized businesses are emerging as key contributors as AI becomes more affordable, intuitive, and cloud-native. With AI capabilities increasingly shifting from tech giants to everyday users, the market is poised to reshape global productivity and innovation across every sector.

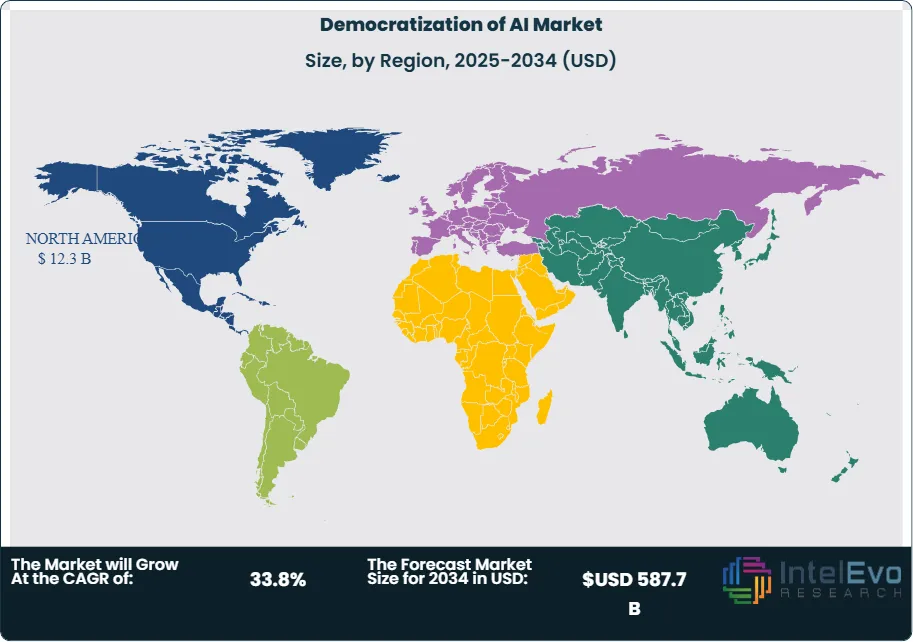

Adoption of artificial intelligence is shifting from specialized technical teams to a wider user base across industries. This expansion is being driven by tools and platforms designed for non-experts, enabling broader participation in AI development and application. In 2024, North America captured 42.7% of total market revenue, or approximately USD 12.3 billion, reflecting strong enterprise investment and a mature cloud services ecosystem that supports AI integration at scale.

Small and medium-sized enterprises (SMEs) are key contributors to market growth. These businesses are leveraging cloud-based AI tools, automated analytics platforms, and no-code interfaces to compete in data-driven environments without the need for large IT teams. The ability to deploy AI with minimal technical expertise is accelerating adoption in areas such as customer engagement, supply chain optimization, fraud detection, and sales forecasting.

The market is being shaped by demand-side pressures for faster decision-making and scalable intelligence solutions, as well as supply-side innovations in AI infrastructure and open-source platforms. Tools like AutoML and explainable AI frameworks are simplifying model training, reducing development cycles, and increasing accessibility. This is helping organizations embed AI into daily workflows without compromising reliability or transparency.

Key sectors leading adoption include healthcare, financial services, and retail. These industries require real-time data insights and personalization, both of which benefit from simplified AI deployment. In healthcare, for instance, democratized AI is being used to support clinical decision-making and patient engagement. In finance, it underpins risk assessment and customer service automation.

Ethical and regulatory considerations remain a critical focus. As AI reaches a broader base of users, concerns around bias, model accountability, and data privacy are growing. Solutions that include built-in compliance tools and bias-detection mechanisms are gaining traction, particularly among firms operating in regulated sectors.

With low-code platforms, accessible APIs, and cloud-native infrastructure accelerating uptake, the democratization of AI is transitioning from a technology trend to a core business enabler. As organizations seek to decentralize AI capabilities across functions, demand for intuitive, cost-effective, and transparent solutions is expected to grow sharply through 2034.

Key Takeaways

Market Growth: The global Democratization of AI market is projected to grow from USD 31.02 billion in 2024 to USD 587.7 billion by 2034, registering a robust CAGR of 33.8%. Growth is fueled by rising demand for accessible AI tools across non-technical user segments, particularly in small and mid-sized enterprises.

Product Type: AI-as-a-Service (AIaaS) led the market in 2024 with a 72.5% share, driven by the growing adoption of pre-built AI models, APIs, and low-code platforms by organizations lacking in-house AI expertise.

Deployment Mode: Cloud-based AI platforms accounted for 56.7% of market share in 2024, reflecting enterprise preference for scalable, cost-efficient, and remotely accessible AI solutions with minimal infrastructure requirements.

End Use: The Banking, Financial Services, and Insurance (BFSI) sector captured over 21.3% of the market in 2024. This is attributed to high demand for AI in fraud detection, credit risk analysis, and personalized financial services.

Driver: The increasing availability of no-code and low-code AI platforms is accelerating adoption across non-technical users. These tools reduce development time and enable faster deployment of AI-driven analytics, customer service, and process automation.

Restraint: Data privacy and regulatory compliance challenges remain a significant constraint, particularly in healthcare and finance. Varying global data governance laws complicate deployment and increase the cost of compliance.

Opportunity: Asia Pacific presents a strong growth opportunity, supported by government-led digital transformation initiatives and a rising SME base. The region is expected to grow at a CAGR exceeding 35% through 2034.

Trend: AutoML and explainable AI tools are gaining traction among enterprises aiming to balance ease of use with transparency. Vendors offering pre-built, auditable AI pipelines are increasingly favored in regulated industries.

Regional Analysis: North America led the market in 2024 with a 42.7% share, equivalent to USD 12.3 billion in revenue. The region’s dominance is supported by a mature cloud infrastructure, strong enterprise AI adoption, and favorable investment activity.

Technology Analysis

AI-as-a-Service (AIaaS) remains the leading segment in the democratization of AI market, accounting for over 72.5% of global revenue in 2024. The model offers on-demand access to advanced AI capabilities such as natural language processing, predictive analytics, and computer vision without the need for in-house infrastructure. For small and medium-sized enterprises, this structure significantly reduces the upfront costs and technical complexity associated with AI deployment.

Adoption is being driven by the flexibility and scalability of AIaaS platforms, which allow users to adjust capacity based on operational needs. Enterprises across sectors—including healthcare, retail, and logistics—are embedding AIaaS into workflows to streamline processes and enhance decision-making. Providers offering vertical-specific solutions, integrated APIs, and transparent pricing models are gaining traction among users looking for low-risk AI adoption paths.

Deployment Mode Analysis

Cloud-based deployment led the market in 2024, capturing 56.7% of total share, reflecting strong preference for accessible, scalable, and cost-efficient AI infrastructure. Organizations favor cloud-based AI platforms for their ease of integration, frequent updates, and reduced maintenance burden. These platforms eliminate the need for dedicated IT infrastructure, enabling faster adoption in resource-constrained environments.

As industries accelerate digital transformation, the shift toward cloud-native applications has intensified. Cloud providers are also investing heavily in cybersecurity, offering enterprise-grade protections that often exceed the capabilities of on-premises systems. This has become a critical factor for sectors such as BFSI and healthcare, where data protection is a regulatory and operational priority.

Industry Vertical Analysis

The BFSI sector led adoption of democratized AI in 2024, with over 21.3% market share. Financial institutions are using AI to drive real-time decision-making in areas such as credit scoring, fraud detection, and portfolio management. AI is also being used to automate regulatory compliance checks and reduce manual processing costs.

Increased regulatory scrutiny and competition from fintechs are accelerating AI deployment within the sector. Institutions are using AI to interpret complex data sets, detect anomalies, and deliver personalized customer experiences. This transformation supports both cost reduction and improved service levels in a highly competitive and regulated market environment.

Regional Analysis

North America dominated the global market in 2024, accounting for 42.7% of total revenue, or USD 12.3 billion. The region benefits from a mature digital ecosystem, advanced cloud infrastructure, and a concentration of AI leaders including platform providers, system integrators, and enterprise users.

The U.S. leads in both venture capital activity and enterprise AI implementation, supported by a large base of AI talent and STEM education. AI democratization is further advanced by strong public-private collaboration and a supportive policy environment. In contrast, Asia Pacific is emerging as a high-growth region, driven by SME digitalization, rising tech adoption, and government-backed AI initiatives.

By Technology (AI-as-a-Service (AIaaS), No-code Tools, Others), By Deployment Mode (Cloud-Based, On-Premises), By Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, IT & Telecom, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Pega Systems, Amazon Web Services (AWS), DataRobot, SAP, UiPath, Alteryx, IBM Corporation, Salesforce, H2O.ai, Microsoft Azure, OpenAI, Google Cloud, Other Key Players

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA DEMOCRATIZATION OF AI CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA DEMOCRATIZATION OF AI CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL DEMOCRATIZATION OF AI CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

IBM Corporation: IBM is positioned as a long-standing leader in enterprise AI and continues to play a key role in democratizing artificial intelligence through its Watson platform. The company’s focus in 2025 is on embedding AI into enterprise workflows with a strong emphasis on explainability, governance, and compliance. Watsonx, IBM’s AI and data platform, enables business users to train, tune, and deploy foundation models at scale. Its appeal lies in robust support for regulated industries such as healthcare, finance, and government.

IBM differentiates itself through AI model transparency and built-in risk mitigation tools. The company is investing in industry-specific AI solutions and hybrid cloud deployments, allowing clients to manage sensitive data on-premises while leveraging cloud-based AI services. IBM’s partnerships with SAP, Salesforce, and Red Hat also support its cross-platform integration capabilities. This ecosystem-centric strategy helps IBM maintain its position in complex, compliance-driven markets.

Google Cloud: Google Cloud is a market leader in AI democratization, with a strong focus on no-code/low-code tools, model efficiency, and open-source adoption. Its Vertex AI platform streamlines the AI lifecycle, from data preparation to model deployment, offering access to Google's pre-trained models and custom training environments. In 2025, Google continues to scale its offerings across sectors such as retail, healthcare, and logistics, where businesses seek fast, flexible AI integration.

A key differentiator for Google is its deep alignment with the open-source community. Tools such as TensorFlow and TFX remain widely adopted in both academic and commercial AI projects. The company also supports AutoML features for non-technical users and provides seamless integration with Google Workspace and BigQuery. This positions Google Cloud as a preferred choice for businesses seeking ease of use, speed to market, and developer support.

Microsoft Azure: Microsoft Azure holds a leading position in the democratization of AI through its Azure AI portfolio and close integration with Office 365 and Dynamics 365. Azure OpenAI Service provides enterprise-grade access to large language models, including GPT-4, while Azure Machine Learning supports both code-first and low-code development. As of 2025, Microsoft continues to expand its customer base in financial services, manufacturing, and the public sector.

The company's competitive edge lies in its scale, security, and enterprise familiarity. Microsoft’s strength in identity management, compliance tools, and global cloud infrastructure makes it a go-to provider for large organizations deploying AI at scale. Strategic investments in responsible AI and AI ethics frameworks also support Microsoft’s positioning as a trusted vendor for AI governance and regulatory readiness.

Amazon Web Services (AWS): AWS is a dominant player in AI democratization, offering a broad suite of AI services through Amazon SageMaker and Bedrock. SageMaker enables developers and data scientists to build, train, and deploy machine learning models efficiently, while Bedrock provides access to foundational models from third parties, including Anthropic, AI21, and Stability AI. In 2025, AWS is emphasizing accessibility for SMEs and extending its reach through regional infrastructure expansion in Asia and Latin America.

AWS differentiates itself through its scalable pricing models, deep customization options, and wide service ecosystem. Its AI services integrate seamlessly with AWS data lakes, IoT solutions, and cloud-native apps, making it highly adaptable to different enterprise architectures. AWS also continues to invest in AI skills development through its training programs, helping close the capability gap among users across industries.

Market Key Players

Pega Systems

Amazon Web Services (AWS)

DataRobot

SAP

UiPath

Alteryx

IBM Corporation

Salesforce

H2O.ai

Microsoft Azure

OpenAI

Google Cloud

Other Key Players

Driver:

Open-Source AI Frameworks Expanding Market Accessibility

As of 2025, the growing availability of open-source AI frameworks is a core enabler of market expansion. Platforms like TensorFlow, PyTorch, and Hugging Face are removing traditional cost and access barriers, allowing individuals, startups, and smaller enterprises to experiment with and deploy AI tools without proprietary licensing fees. This has significantly expanded the base of AI contributors and users across academic, commercial, and government sectors.

Collaborative Ecosystems Accelerating Innovation and Adoption

Open-source ecosystems accelerate innovation by promoting transparency, peer review, and rapid iteration. They also encourage global collaboration, which helps uncover bias, improve security, and increase the pace of AI development. For vendors and investors, this broad participation base is expanding use cases, unlocking new business models, and driving higher demand for AI infrastructure, support services, and integrations.

Restraint:

Ethical and Security Risks Rising with Wider AI Access

The expanded access to AI technologies has intensified concerns around ethical misuse and security vulnerabilities. With open tools widely available, the risk of unintended outcomes—including algorithmic bias, unauthorized surveillance, and malicious automation—has grown. In many regions, regulatory frameworks remain underdeveloped, leaving organizations exposed to reputational and compliance risks.

Governance Gaps Creating Compliance Challenges for Enterprises

Without strong governance and enforcement mechanisms, democratized AI may amplify systemic inequalities or result in data privacy breaches. For companies deploying AI at scale, balancing accessibility with responsible use requires robust internal safeguards, risk assessment protocols, and alignment with emerging global standards such as the EU AI Act and U.S. AI Bill of Rights.

Opportunity:

Low-Code and No-Code AI Unlocking Growth in Emerging Markets

The democratization of AI is creating substantial opportunities for economic expansion, especially in underserved and emerging markets. Lower technical barriers and the rise of no-code platforms are enabling a broader range of users to integrate AI into daily operations. This is fueling productivity gains, reducing time-to-market for digital services, and enabling innovation in sectors that previously lacked access to advanced analytics.

SMEs Leveraging AI for Productivity, Automation, and Value Creation

Small and mid-sized enterprises are using AI to optimize workflows, automate customer interactions, and improve decision-making at scale. With global AI spending projected to exceed USD 500 billion by 2034, inclusive access to AI tools could unlock widespread value creation and serve as a catalyst for new job categories, digital entrepreneurship, and regional development.

Trend:

Simplified AI Interfaces Driving Cross-Functional Adoption

As adoption widens in 2025, two trends are reshaping the democratization landscape: interface simplification and ethical AI integration. Tools with intuitive, drag-and-drop features—such as no-code AI platforms—are gaining popularity among non-technical professionals in marketing, HR, and logistics. This usability shift is increasing cross-functional AI implementation beyond traditional IT and data teams.

Ethical and Transparent AI Becoming a Core Enterprise Imperative

Simultaneously, companies are embedding fairness, explainability, and privacy protections directly into AI models. Enterprise buyers are prioritizing compliance-ready solutions with built-in bias detection and audit trails. As regulators move to enforce transparency and accountability, vendors that align with ethical standards and offer user-centric tools are capturing increased enterprise demand and long-term strategic relevance.

Recent Developments

Dec 2024 – Microsoft Azure: Microsoft launched new generative AI features within Azure AI Studio, including a custom prompt tuning module for enterprise users. The update is expected to support over 5,000 enterprise clients globally by Q2 2025. This move enhances Azure’s enterprise value proposition and expands its footprint in regulated industries.

Feb 2025 – Amazon Web Services (AWS): AWS announced the addition of Cohere and Mistral models to its Bedrock platform, expanding its foundational model ecosystem. The update aims to improve flexibility for developers using multiple model providers. This strengthens AWS’s position as a multi-model hub for democratized AI deployment.

Apr 2025 – Google Cloud: Google Cloud partnered with the European Commission to launch a sovereign AI initiative, backed by an investment of over USD 250 million. The program aims to improve AI accessibility for public institutions across the EU. The partnership deepens Google’s public sector engagement and aligns with evolving digital sovereignty policies.

Jul 2025 – IBM Corporation: IBM introduced new AI governance tools within its Watsonx platform, including auditability features designed for financial and healthcare sectors. These tools help companies manage compliance with AI risk management frameworks such as the EU AI Act and NIST RMF. The update reinforces IBM’s differentiation in regulated markets.

Sep 2025 – Salesforce: Salesforce unveiled AI Studio for CRM, a no-code tool enabling sales and marketing teams to build AI workflows using enterprise data. Over 3,000 customers signed up in the first month, with pilot deployments showing a 22% increase in campaign efficiency. This product broadens Salesforce’s influence in the democratized AI space, targeting business users without technical backgrounds.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, No-code Tools, Others), By Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, IT & Telecom, Others), By Deployment Model Industry Outlook, Workforce Transformation Trends & Forecast 2025–2034")

, No-code Tools, Others), By Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, IT & Telecom, Others), By Deployment Model Industry Outlook, Workforce Transformation Trends & Forecast 2025–2034")

, No-code Tools, Others), By Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, IT & Telecom, Others), By Deployment Model Industry Outlook, Workforce Transformation Trends & Forecast 2025–2034")

, No-code Tools, Others), By Industry Vertical (BFSI, Healthcare, Retail, Manufacturing, IT & Telecom, Others), By Deployment Model Industry Outlook, Workforce Transformation Trends & Forecast 2025–2034")