- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Dental Biomaterial Market Size & Forecast | CAGR 7.3%

Global Dental Biomaterial Market Size, Share, Growth & Industry Analysis By Material Type (Dental Ceramics Zirconia, Lithium Disilicate, Feldspathic, Composite Resins Nano-Filled & Bulk-Fill, Dental Cements, Dental Alloys, Bone Grafts), By Application (Restorative, Prosthodontics, Implantology, Endodontics, Orthodontics), By End-User (Clinics, Labs, Hospitals) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

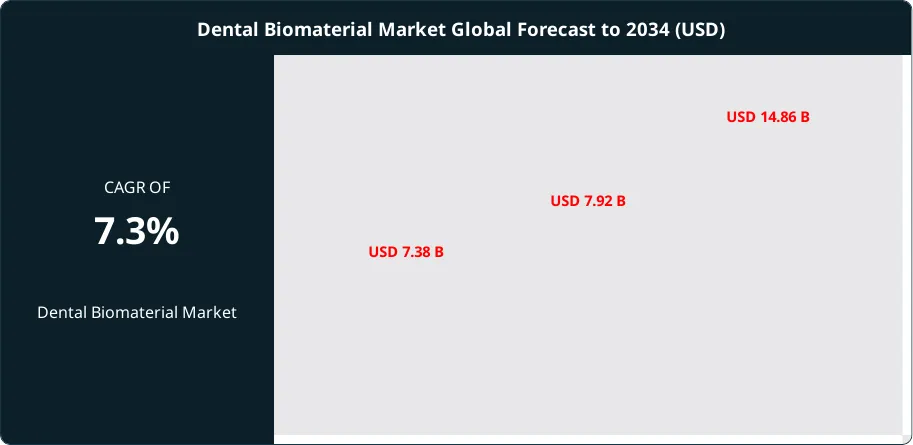

| USD 7.92 Billion | USD 14.86 Billion | 7.3% | North America, 38.4% |

The Dental Biomaterial Market was valued at approximately USD 7.38 Billion in 2024 and reached USD 7.92 Billion in 2025. The market is projected to grow to USD 14.86 Billion by 2034, expanding at a CAGR of 7.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.94 Billion over the analysis period, underpinned by rising global dental care utilization, accelerating adoption of digital dentistry workflows, and the sustained expansion of implantology and cosmetic dental procedures across both developed and emerging economies.

Get More Information about this report -

Request Free Sample ReportDental biomaterials encompass a broad and technically sophisticated product category spanning dental ceramics, composite resins, dental cements, dental alloys, bone graft substitutes, and regenerative membrane materials used in restorative, prosthodontic, endodontic, and periodontal applications. The dental biomaterial market sits at the intersection of materials science and clinical dentistry, where performance requirements including biocompatibility per ISO 10993 standards, mechanical durability meeting ISO 6872 flexural strength criteria, and esthetic translucency comparable to natural enamel drive continuous product development cycles. Regulatory oversight from the U.S. Food and Drug Administration under the 510(k) premarket notification pathway and the European Medical Device Regulation (EU MDR 2017/745) governs market entry for dental biomaterial products in the two largest end markets globally.

Digital dentistry is fundamentally restructuring demand patterns within the dental biomaterial market. Computer-aided design and computer-aided manufacturing (CAD/CAM) milling systems now account for an estimated 31.4% of all crown and bridge restorations produced globally in 2025, up from 18.6% in 2020, creating direct demand for high-strength zirconia blocks, lithium disilicate ceramic blanks, and PMMA resin discs compatible with milling workflows. The World Health Organization’s Global Oral Health Action Plan 2023–2030 has prioritized access to restorative dental care, with member states committing to reduce untreated dental caries prevalence, directly expanding the addressable market for restorative dental biomaterials in lower- and middle-income countries.

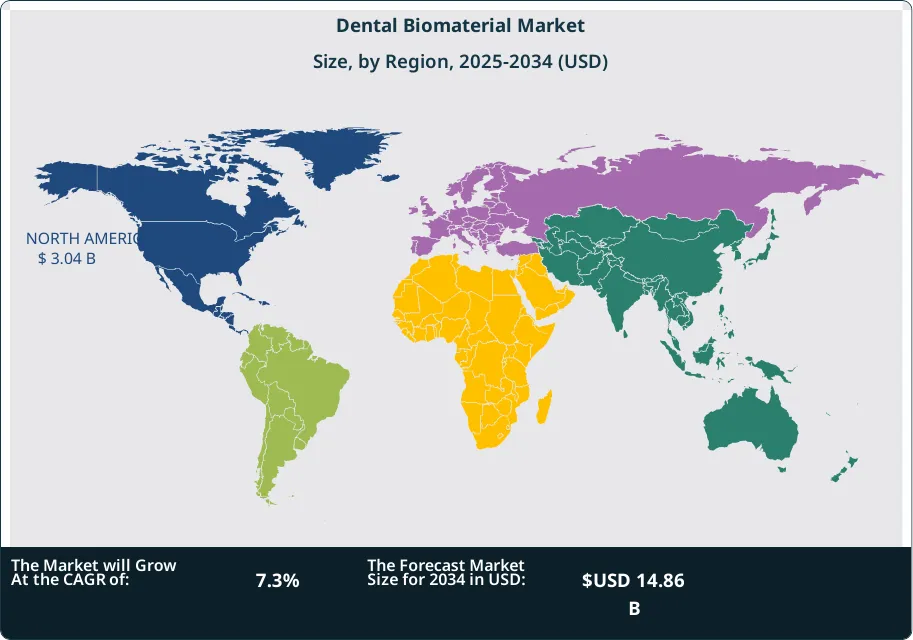

From a supply-side perspective, the dental biomaterial market benefits from strong vertical integration among major manufacturers, with leading companies investing in proprietary ceramic formulation, surface chemistry modification, and clinical bonding system development. North America leads the market with a 38.4% share in 2025, anchored by high dental insurance penetration, strong cosmetic dentistry demand, and a mature implant-supported restoration sector. Asia Pacific is the fastest-growing region at 9.2% CAGR through 2034, driven by expanding dental care access in China, India, and Southeast Asia, increasing medical tourism activity, and government oral health programs that are broadening the patient base for dental materials consumption.

, By Application (Restorative, Prosthodontics, Implantology, Endodontics, Orthodontics), By End-User (Clinics, Labs, Hospitals) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global dental biomaterial market was valued at USD 7.92 Billion in 2025 and is projected to reach USD 14.86 Billion by 2034, registering a CAGR of 7.3% over the forecast period 2026–2034.

- Segment Dominance: By material type, dental ceramics represent the leading sub-segment with 34.6% of the dental biomaterial market in 2025, driven by the widespread transition to all-ceramic and zirconia-based restorations replacing metal-ceramic alternatives in cosmetic and functional dental applications.

- Segment Dominance: By application, restorative dentistry accounts for 42.8% of total dental biomaterial spending in 2025, anchored by high-volume demand for composite resin, dental cement, and ceramic inlay and crown materials across private dental practices and hospital-based dental departments.

- Driver: Rising global prevalence of dental caries and tooth loss is the primary demand driver; the WHO estimates 3.5 Billion people are affected by oral diseases globally in 2025, with dental caries in permanent teeth representing the most prevalent condition and directly expanding the market for restorative and regenerative biomaterials.

- Restraint: High product cost and limited dental insurance reimbursement in emerging markets restrict access to premium dental biomaterials; all-ceramic and zirconia restorations cost USD 800–2,500 per unit in the U.S., limiting adoption among cost-sensitive patient populations and reducing total procedure volumes in price-sensitive markets.

- Opportunity: Bioactive and regenerative dental biomaterials represent an estimated USD 2.1 Billion addressable opportunity within the dental biomaterial market by 2034, driven by demand for calcium silicate cements, growth factor-enhanced bone grafts, and resorbable guided tissue regeneration membranes in implantology and periodontal surgery.

- Trend: CAD/CAM-compatible dental biomaterials are the dominant technology trend; zirconia block and ceramic blank unit sales grew 18.3% year-over-year in 2025 as dental laboratories and chairside milling systems displaced traditional feldspathic ceramic fabrication in crown and bridge workflows.

- Regional Analysis: North America leads the dental biomaterial market with 38.4% share and USD 3.04 Billion in revenue in 2025, driven by high per-capita dental expenditure, a dense network of specialty dental practices, and strong adoption of premium biomaterial systems by implant prosthodontists and cosmetic dentists.

Competitive Landscape Overview

The dental biomaterial market is moderately consolidated, with the top four companies accounting for approximately 46% of global revenue in 2025. Competition is technology-driven, with leaders differentiating through proprietary ceramic and composite formulations, integrated bonding system portfolios, and compatibility with major CAD/CAM milling platforms. Strategic acquisitions have defined competitive dynamics over the past three years, with large dental conglomerates acquiring specialty biomaterial firms to broaden their restorative and regenerative portfolios. Two significant new entrants from the broader medical devices sector entered the dental biomaterial space in 2024–2025, intensifying competition in the premium ceramic and bone regeneration sub-segments.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Dentsply Sirona | USA | Leader | CEREC Zirconia CAD/CAM Blocks | North America / Europe | Launched next-gen CEREC Zirconia ML multilayer blocks for chairside milling in Jan 2025 |

| Ivoclar Vivadent | Liechtenstein | Leader | IPS e.max CAD Lithium Disilicate | Europe / Global | Expanded IPS e.max production capacity by 40% at its Schaan facility in Feb 2025 |

| 3M (Solventum) | USA | Leader | Filtek Supreme Ultra Composite | North America / Global | Spun out dental product line under Solventum brand in 2024 with USD 2.0B revenue commitment |

| Straumann Group | Switzerland | Leader | DEDICAM Zirconia Milling Blanks | Europe / North America | Acquired a bone regeneration biomaterial startup for USD 320M in Mar 2025 |

| Kuraray Noritake | Japan | Challenger | Panavia V5 Resin Cement | Asia Pacific / Global | Launched Clearfil Universal Bond Quick 2 for universal adhesive applications in Dec 2024 |

| GC Corporation | Japan | Challenger | G-aenial Composite Resin System | Asia Pacific / Europe | Opened a new European distribution hub in the Netherlands in Apr 2025 |

| Envista Holdings (Danaher) | USA | Challenger | KaVo Kerr Dental Cements | North America | Completed integration of Nobel Biocare bone graft product line in Jan 2025 |

| Shofu Dental | Japan | Niche Player | Ceramage Up Nano-Ceramic Composite | Asia Pacific | Introduced a new bioactive glass-ionomer cement line for paediatric dentistry in Mar 2025 |

| DENTSPLY GAC | USA | Niche Player | ProRoot MTA Endodontic Cement | North America / Europe | Received FDA 510(k) clearance for next-generation bioceramic root repair cement in Jun 2025 |

| Geistlich Pharma | Switzerland | Niche Player | Geistlich Bio-Oss Bone Substitute | Europe / North America | Launched Bio-Oss Collagen+ enhanced bone graft matrix in Feb 2025 |

By Material Type

The dental biomaterial market by material type is led by dental ceramics, which account for 34.6% of total market revenue in 2025 at approximately USD 2.74 Billion. The dominance of ceramics reflects the ongoing industry transition from metal-ceramic and amalgam-based restorations toward all-ceramic solutions that offer superior esthetic results, bioinertness, and compatibility with CAD/CAM fabrication systems. Zirconia ceramics, including monolithic and multilayer formulations, represent the fastest-growing ceramic sub-category due to their high flexural strength exceeding 800 MPa in tetragonal zirconia polycrystal (TZP) grades and their ability to meet the esthetic demands of anterior and posterior restorations simultaneously. Composite resins represent the second-largest material type at 26.8% of the market in 2025, driven by their wide application in Class I through Class V direct restorations and their continued evolution toward nano-filled and nano-hybrid formulations that improve wear resistance and color stability. Dental cements, encompassing resin cements, glass ionomer cements, and resin-modified glass ionomers, hold 14.3% of the dental biomaterial market and are experiencing demand growth from the expanding volume of adhesively bonded all-ceramic restorations. Dental alloys, primarily cobalt-chromium and titanium-based, account for 12.7% of revenue and remain essential for implant prosthetics and partial denture frameworks. Bone graft substitutes and regenerative membranes together represent 11.6% of the market, a segment expanding rapidly as implant placement volumes and guided bone regeneration procedures increase globally.

By Application

Dental biomaterial market segmentation by application places restorative dentistry as the dominant application with 42.8% market share in 2025 at approximately USD 3.39 Billion. The restorative segment encompasses direct and indirect restorations including composite resin fillings, ceramic inlays, onlays, and full-coverage crowns, supported by high procedure volumes across private dental practices and hospital-based dental units globally. Dental caries is the primary clinical driver for restorative material consumption, with an estimated 2.3 Billion people affected by untreated caries in permanent teeth in 2025 according to WHO data. Prosthodontics represents the second-largest application with 24.3% of market revenue, driven by the growing demand for fixed partial dentures, complete denture acrylic materials, and implant-supported crown and bridge restorations. Implantology and bone regeneration applications account for 17.6% of total dental biomaterial spending in 2025, growing at an above-market CAGR of 9.4% through 2034 as dental implant placement volumes expand globally. Endodontics holds 9.2% of the market, supported by demand for root canal sealers, bioceramic root repair cements, and obturation materials. Periodontics and orthodontics together account for the remaining 6.1%, encompassing guided tissue regeneration membranes, bone grafts, and tooth-colored bracket bonding materials.

By End-User

The dental biomaterial market by end-user is dominated by dental clinics and private practices, which account for 58.4% of total revenue in 2025 at USD 4.62 Billion. This segment reflects the high frequency of direct-placed restorations, impression materials, and bonding agents consumed in the outpatient dental setting, where chair-side material consumption constitutes a recurring operating cost for practitioners. Dental laboratories represent the second-largest end-user segment at 22.7% of market revenue, encompassing the fabrication of indirect restorations including ceramic crowns, zirconia bridges, and metal-ceramic prostheses. The laboratory segment is undergoing structural change as in-house CAD/CAM milling systems in dental practices reduce referrals to external laboratories for single-unit restorations. Hospitals and academic dental institutions account for 12.4% of the dental biomaterial market, primarily consuming surgical biomaterials including bone substitutes, barrier membranes, and bioceramic endodontic cements for specialty procedures. Research and educational institutions hold the remaining 6.5% and serve as critical early adoption channels for novel biomaterial formulations including bioactive composites, self-adhesive cements, and calcium silicate-based systems prior to broader commercial distribution.

By Technology

The dental biomaterial market by technology segments products into conventional analog systems and digital/CAD-CAM compatible materials. Analog dental biomaterials, including hand-mixed and auto-mixed composite resins, glass ionomer cements, and traditional feldspathic ceramic powders for manual layering, retain 54.2% of market revenue in 2025 due to the large installed base of traditional dental practices and the continued use of direct restorative techniques for Class I and Class II carious lesions. However, digital and CAD-CAM compatible dental biomaterials hold 45.8% of market revenue in 2025 and are growing at an estimated 10.6% CAGR through 2034, more than twice the growth rate of the analog segment. This category includes pre-sintered zirconia blanks, lithium disilicate CAD blocks, PMMA and composite resin discs for temporary and definitive restorations, and 3D printing resins for surgical guides and model fabrication. The rapid expansion of intraoral scanning and same-day dentistry workflows is the principal driver of digital material adoption, with chairside CAD/CAM systems such as CEREC, Planmeca FIT, and Carestream CS 3600 now present in an estimated 22% of U.S. dental practices and 18% of European practices as of 2025.

Regional Analysis

North America

North America leads the global dental biomaterial market with a 38.4% share and USD 3.04 Billion in revenue in 2025. The United States is the dominant country market, accounting for approximately 88% of North American revenue. High per-capita dental expenditure, estimated at USD 450 per capita annually in the U.S. in 2025, and strong private dental insurance penetration covering approximately 61% of the adult population drive consistent demand for premium restorative and implant-prosthetic biomaterials. The ADA Health Policy Institute reports that over 200 Million dental restoration procedures are performed annually in the U.S., creating a large and stable demand base for composite resin, dental ceramic, and cement materials. CAD/CAM dentistry adoption rates in the U.S. are among the highest globally, with same-day crown procedures now representing over 12% of all single-unit crown deliveries. Canada is the second-largest North American market, with a publicly funded dental care program expanding adult access to restorative dentistry since 2023, creating incremental demand for composite and glass ionomer materials in underserved populations. Mexico is an emerging market within the region, benefiting significantly from dental tourism demand from U.S. patients seeking cost-effective implant and ceramic crown procedures.

Europe

Europe accounts for 27.8% of the global dental biomaterial market in 2025 at USD 2.20 Billion. Germany is the leading European country market, home to major dental material manufacturers including Ivoclar Vivadent’s European operations, Shofu, and Voco GmbH, as well as a high-density network of dental laboratories consuming significant volumes of ceramic and alloy materials. The German statutory health insurance system provides partial reimbursement for dental restorations, with patients co-paying for ceramic upgrades over amalgam or composite base rates, creating a tiered demand structure for biomaterial quality levels. France is the second-largest European market, where Carte Vitale reimbursement reforms in 2023 expanded coverage for tooth-colored resin restorations, generating measurable incremental composite resin demand. The United Kingdom represents a significant market where NHS dentistry and private sector growth coexist; the shift toward private practice in cosmetic and implant dentistry is driving premium biomaterial consumption. Switzerland is a globally disproportionate market due to its concentration of leading dental biomaterial headquarters including Straumann Group, Geistlich Pharma, and Ivoclar, which conduct significant clinical research and product launch activities domestically. The EU MDR 2017/745 transition has increased regulatory compliance costs for dental biomaterial manufacturers, consolidating the European competitive base around larger, better-resourced firms.

Asia Pacific

Asia Pacific holds a 23.6% share of the global dental biomaterial market in 2025 with USD 1.87 Billion in revenue and represents the fastest-growing region, projected to expand at a 9.2% CAGR through 2034. Japan is the leading Asia Pacific dental biomaterial market, supported by its universal health insurance system covering basic restorative materials and a sophisticated dental laboratory network consuming advanced ceramic and resin materials. Japan is also home to major dental biomaterial manufacturers including GC Corporation, Shofu, and Kuraray Noritake, which are globally competitive in composite resins, glass ionomers, and resin cements. China is the fastest-growing individual country market, with dental service demand expanding rapidly as urbanization, rising disposable incomes, and government oral health initiatives under the Healthy China 2030 program increase access to restorative care. China’s National Medical Products Administration (NMPA) regulatory approval reforms have improved market entry timelines for international dental biomaterial brands. India is an emerging high-growth market, where a large underserved dental population and expanding private dental chain networks are driving demand for cost-competitive composite and glass ionomer materials. South Korea’s advanced dental industry, including major dental implant manufacturers such as Osstem Implant and Dentium, creates associated demand for bone regeneration biomaterials and implant prosthetic ceramics.

Latin America

Latin America accounts for 6.2% of the global dental biomaterial market in 2025 with USD 0.49 Billion in revenue. Brazil is by far the dominant Latin American market, representing approximately 58% of regional spending. Brazil has the largest dentist-to-population ratio globally, with an estimated 340,000 registered dentists providing dental services to a market where public sector dental care coexists with a large and growing private dental chain sector. The Brazilian National Health Surveillance Agency (ANVISA) regulates dental biomaterials, and domestic manufacturers including FGM Dental Products and Biodinamic compete with international brands on cost grounds in the public sector supply chain. Argentina is the second-largest Latin American market for dental biomaterials, though economic volatility has constrained premium material adoption and investment in digital dentistry infrastructure. Mexico benefits from dental tourism demand driving higher-grade ceramic and implant-prosthetic material consumption in border cities. Colombia and Chile represent smaller but consistently growing markets as urban middle-class populations increase dental care spending. Regional distribution infrastructure limitations and import tariff structures have historically favored global brands that maintain local distribution partnerships over direct import models.

Middle East & Africa

The Middle East and Africa region holds a 4.0% share of the global dental biomaterial market in 2025 with USD 0.32 Billion in revenue. The UAE is the leading Middle Eastern market, with Dubai and Abu Dhabi hosting a concentration of high-end dental clinics serving expatriate populations and medical tourists who demand premium ceramic and implant-prosthetic biomaterials. Saudi Arabia is the second-largest market in the region, with Vision 2030 healthcare reforms expanding dental service coverage under the national insurance system and increasing government procurement of dental materials for public health facilities. South Africa leads the African market segment, with a formal private dental sector in Johannesburg and Cape Town consuming internationally branded composite resin and ceramic materials. The Gulf Cooperation Council (GCC) countries collectively represent the highest per-capita dental biomaterial consumption in the region, driven by high disposable incomes and a strong preference for esthetic dentistry including all-ceramic veneers and implant-supported restorations. Infrastructure investment in dental schools and hospital-based dental departments across North Africa, Kenya, and Nigeria is creating incremental demand for foundational biomaterials including glass ionomer cements and basic composite resins in these emerging country markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Dental Ceramics (Zirconia, Lithium Disilicate, Feldspathic)

- Composite Resins (Nano-filled, Nano-hybrid, Bulk-fill)

- Dental Cements (Resin Cement, Glass Ionomer, RMGI)

- Dental Alloys (Cobalt-Chromium, Titanium, Precious Metal)

- Bone Graft Substitutes & Regenerative Membranes

By Application

- Restorative Dentistry

- Prosthodontics

- Implantology & Bone Regeneration

- Endodontics

- Periodontics & Orthodontics

By End-User

- Dental Clinics & Private Practices

- Dental Laboratories

- Hospitals & Academic Dental Institutions

- Research & Educational Institutions

By Technology

- Analog Dental Biomaterials

- Digital / CAD-CAM Compatible Dental Biomaterials

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.92 B |

| Forecast Revenue (2034) | USD 14.86 B |

| CAGR (2025-2034) | 7.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type, (Dental Ceramics (Zirconia, Lithium Disilicate, Feldspathic), Composite Resins (Nano-filled, Nano-hybrid, Bulk-fill), Dental Cements (Resin Cement, Glass Ionomer, RMGI), Dental Alloys (Cobalt-Chromium, Titanium, Precious Metal), Bone Graft Substitutes & Regenerative Membranes), By Application, (Restorative Dentistry, Prosthodontics, Implantology & Bone Regeneration, Endodontics, Periodontics & Orthodontics), By End-User, (Dental Clinics & Private Practices, Dental Laboratories, Hospitals & Academic Dental Institutions, Research & Educational Institutions), By Technology, (Analog Dental Biomaterials, Digital / CAD-CAM Compatible Dental Biomaterials) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | DENTSPLY SIRONA, IVOCLAR VIVADENT AG, 3M (SOLVENTUM DENTAL SOLUTIONS), STRAUMANN GROUP, KURARAY NORITAKE DENTAL INC., GC CORPORATION, ENVISTA HOLDINGS (DANAHER CORPORATION), SHOFU DENTAL CORPORATION, GEISTLICH PHARMA AG, VOCO GMBH, COLTENE HOLDING AG, OSSTEM IMPLANT CO., LTD., BISCO DENTAL PRODUCTS, SDI LIMITED, KERR CORPORATION (ENVISTA), VITA ZAHNFABRIK, FGM DENTAL PRODUCTS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Restorative, Prosthodontics, Implantology, Endodontics, Orthodontics), By End-User (Clinics, Labs, Hospitals) Industry Trends & Forecast 2026–2034")

, By Application (Restorative, Prosthodontics, Implantology, Endodontics, Orthodontics), By End-User (Clinics, Labs, Hospitals) Industry Trends & Forecast 2026–2034")

, By Application (Restorative, Prosthodontics, Implantology, Endodontics, Orthodontics), By End-User (Clinics, Labs, Hospitals) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Dental Biomaterial Market?

Global Dental biomaterial market valued at USD 7.38B in 2024, reaching USD 14.86B by 2034, growing at a CAGR of 7.3% from 2026–2034.

Who are the major players in the Dental Biomaterial Market?

DENTSPLY SIRONA, IVOCLAR VIVADENT AG, 3M (SOLVENTUM DENTAL SOLUTIONS), STRAUMANN GROUP, KURARAY NORITAKE DENTAL INC., GC CORPORATION, ENVISTA HOLDINGS (DANAHER CORPORATION), SHOFU DENTAL CORPORATION, GEISTLICH PHARMA AG, VOCO GMBH, COLTENE HOLDING AG, OSSTEM IMPLANT CO., LTD., BISCO DENTAL PRODUCTS, SDI LIMITED, KERR CORPORATION (ENVISTA), VITA ZAHNFABRIK, FGM DENTAL PRODUCTS, Others

Which segments covered the Dental Biomaterial Market?

By Material Type, (Dental Ceramics (Zirconia, Lithium Disilicate, Feldspathic), Composite Resins (Nano-filled, Nano-hybrid, Bulk-fill), Dental Cements (Resin Cement, Glass Ionomer, RMGI), Dental Alloys (Cobalt-Chromium, Titanium, Precious Metal), Bone Graft Substitutes & Regenerative Membranes), By Application, (Restorative Dentistry, Prosthodontics, Implantology & Bone Regeneration, Endodontics, Periodontics & Orthodontics), By End-User, (Dental Clinics & Private Practices, Dental Laboratories, Hospitals & Academic Dental Institutions, Research & Educational Institutions), By Technology, (Analog Dental Biomaterials, Digital / CAD-CAM Compatible Dental Biomaterials)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date