- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Continuous Glucose Monitor Market Size, Share | CAGR 14.8%

Global Digital Biomarker Market Size, Share, Analysis By Biomarker Type (Physiological, Behavioral, Cognitive, Vocal, Idiosyncratic), By Component & Platform (Data Collection Tools, Wearable Sensors, Mobile Apps, Implantables, Data Integration Software, Analytics Platforms), By Therapeutic Area (Cardiovascular, Neurology, Oncology, Metabolic Disorders), By End-User (Pharma & Biotech Companies, Healthcare Providers, CROs, Payers) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 5.04 Billion | USD 31.82 Billion | 22.7% | North America, ~59.0% |

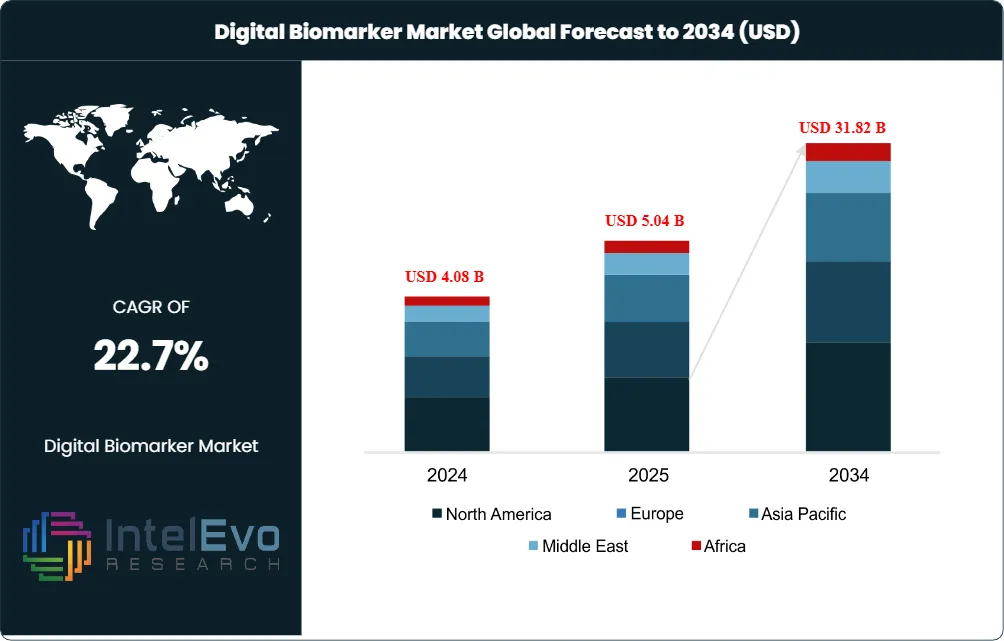

The Digital Biomarker Market was valued at USD 4.08 Billion in 2024 and USD 5.04 Billion in 2025. The market is projected to reach USD 31.82 Billion by 2034, expanding at a CAGR of 22.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 26.78 billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe digital biomarker market is expanding because clinical trials, remote patient monitoring, decentralized research, neurology studies, cardiology trials, and chronic disease programs need objective patient data outside hospitals. FDA guidance on digital health technologies confirms that wearable, implanted, ingested, and environmental technologies can collect clinical trial data remotely, which directly supports digital biomarker adoption in drug development.

Growth is also linked to disease burden. In the United States, CDC data identifies chronic diseases such as heart disease, cancer, and diabetes as leading drivers of disability and USD 4.9 trillion in annual healthcare costs. Alzheimer’s disease adds another demand layer, with 7.2 million Americans aged 65 and older living with Alzheimer’s dementia in 2025 and care costs projected at USD 384 billion.

Regulation is shifting from uncertainty to structured validation. The FDA’s final guidance on digital health technologies for remote data acquisition in clinical investigations was issued in December 2023, while the FDA Biomarker Qualification Program continues to support biomarkers as drug development tools. In May 2024, the FDA qualified Apple’s AFib History Feature as a biomarker test for secondary effectiveness endpoints in cardiac ablation device studies, creating a reference case for wearable-derived digital biomarkers.

North America leads because FDA pathways, payer interest in remote monitoring, Apple Watch adoption, Empatica’s FDA-cleared health monitoring platform, Medidata clinical trial infrastructure, and IQVIA analytics capacity cluster in the United States. Europe follows through EMA qualification advice, EU MDR clinical evidence requirements, GDPR data controls, and digital endpoint work in neurology and rare disease trials. Asia Pacific is the fastest-growth region because Japan, China, South Korea, India, and Singapore are expanding digital health infrastructure and clinical trial participation.

Market Definition & Scope

The digital biomarker market is defined as the commercial market for objective, quantifiable physiological and behavioral measures collected through digital health technologies and analyzed for disease detection, monitoring, drug development, or clinical decision support. The market includes wearable sensors, smartphone-based assessments, connected medical devices, cloud analytics, algorithmic endpoints, digital clinical outcome assessments, remote monitoring platforms, and software used to process sensor-derived health signals.

The digital biomarker market includes validated digital measures used in cardiology, neurology, respiratory disease, sleep medicine, oncology, psychiatry, metabolic disease, and decentralized clinical trials. It excludes traditional molecular biomarkers, laboratory assays, radiographic biomarkers, generic wellness wearables without clinical validation, and consumer fitness analytics not used for healthcare, regulatory, or research decisions. The parent market is digital health technology, while digital biomarkers represent the clinical evidence layer inside that larger market.

, By Component & Platform (Data Collection Tools, Wearable Sensors, Mobile Apps, Implantables, Data Integration Software, Analytics Platforms), By Therapeutic Area (Cardiovascular, Neurology, Oncology, Metabolic Disorders), By End-User (Pharma & Biotech Companies, Healthcare Providers, CROs, Payers) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

Key Takeaways

- Market Growth: The digital biomarker market increased to USD 5.04 billion in 2025 and is projected to reach USD 31.82 billion by 2034, reflecting a verified 22.7% CAGR.

- Segment Dominance: Data collection tools held approximately 68.0% share in 2025, equal to USD 3.43 billion, because wearables and smartphones remain the main capture layer for continuous patient signals.

- Segment Dominance: Clinical trials represented approximately 46.0% share in 2025, equal to USD 2.32 billion, because sponsors use digital endpoints to reduce site dependence and capture real-world functional outcomes.

- Driver: Chronic disease monitoring is the primary demand driver, supported by CDC’s USD 4.9 trillion annual U.S. healthcare cost figure for chronic conditions.

- Restraint: Validation cost and regulatory evidence requirements slow procurement because sponsors must prove analytical validity, clinical validity, usability, data integrity, and cybersecurity before deployment.

- Opportunity: Neurology and aging-related disorders represent the largest white-space opportunity, with Alzheimer’s care costs projected at USD 384 billion in the United States in 2025.

- Trend: Digital endpoints are moving from pilot studies to formal trial use, with DiMe-referenced data showing 505 digital endpoints in its library as of 2024.

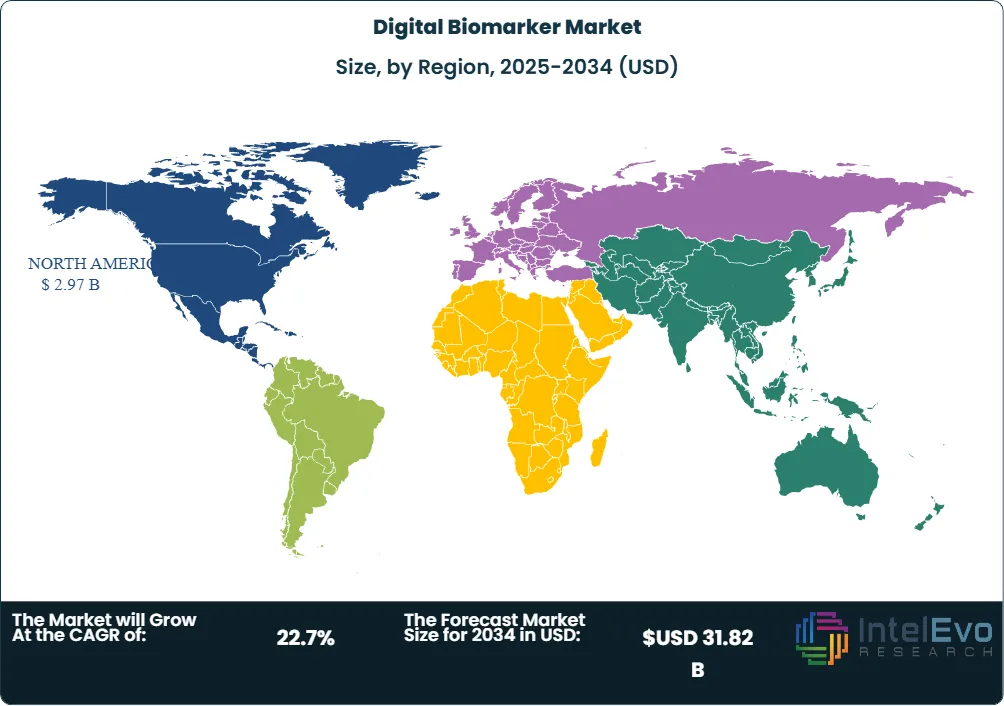

- Regional: North America led the digital biomarker market with approximately 59.0% share in 2025, equal to USD 2.97 billion.

Key Insights Summary

- The FDA’s December 2023 final guidance positioned digital health technologies as acceptable tools for remote clinical investigation data acquisition when sponsors address verification, validation, usability, and participant risk.

- Apple’s AFib History Feature became an FDA-qualified Medical Device Development Tool in May 2024 for estimating AFib burden as a secondary endpoint in cardiac ablation studies.

- DiMe’s digital endpoint resource listed 505 digital endpoints as of 2024, indicating a tenfold expansion from earlier industry-sponsored trial use.

- EMA-linked analysis covering 2013-2022 procedures found accelerometers were the most proposed digital health technologies for endpoint measurement, followed by glucose monitors and smartphones.

- Empatica received an FDA 510(k) clearance in June 2025 covering a Predetermined Change Control Plan for its SpO2 algorithm within the Empatica Health Monitoring Platform.

- On November 6, 2025, the FDA Digital Health Advisory Committee reviewed generative AI-enabled digital mental health medical devices, including evidence and postmarket monitoring questions.

Competitive Landscape Overview

The digital biomarker market is moderately fragmented, with the top four commercial platforms estimated to control approximately 31.0% of 2025 revenue. Competition is based on regulatory credibility, sensor validation, therapeutic-area depth, trial operations, cloud analytics, and pharma relationships. Dassault Systèmes’ Medidata, IQVIA, Clario, and Empatica hold high visibility because they combine trial infrastructure, endpoint data, wearable evidence, and enterprise relationships.

The competitive structure is shifting toward platform bundling. Thermo Fisher Scientific’s October 2025 agreement to buy Clario for USD 8.875 billion upfront shows that clinical research service providers want endpoint data, software, imaging, and digital measures under one operating model.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Medidata Solutions | United States | Leader | Medidata platform, patient experience, sensor-connected trial tools | North America, Europe, Japan | Expanded AI-enabled clinical trial functions through Dassault Systèmes platform activity in 2025 |

| IQVIA Holdings Inc. | United States | Leader | Technology & Analytics Solutions, clinical analytics, R&D data systems | North America, Europe, Asia Pacific | Reported USD 1.821 billion Q4 2025 TAS revenue, up 9.8% year over year. |

| Clario Holdings, Inc. | United States | Leader | Endpoint data, eCOA, imaging, respiratory and digital endpoint systems | North America, Europe | Entered Thermo Fisher acquisition agreement in October 2025. |

| Empatica S.r.l. | Italy | Leader | EmbracePlus, EmbraceMini, Empatica Health Monitoring Platform | United States, Europe | Secured FDA clearance for EmbraceMini sleep monitoring in January 2026. |

| Ametris | United States | Challenger | Wearable DHT platform and trial analytics | United States, Europe | Repositioned from ActiGraph to Ametris with clinical DHT focus. |

| Koneksa Health | United States | Challenger | Digital measures, sensor analytics, disease-specific endpoints | United States, Europe | Advanced Parkinson’s digital biomarker work through 2025 scientific activity. |

| Medable Inc. | United States | Challenger | Digital clinical trial platform, eCOA, AI agents | North America, Europe | Released oncology trial offering and AI trial operations tools in 2025. |

| Huma Therapeutics | United Kingdom | Challenger | Remote monitoring and disease management platforms | Europe, Middle East, Asia | Continued regulated digital health platform expansion across disease programs |

| Evidation Health | United States | Niche Player | Real-world digital health data and patient-generated evidence | United States | Continued consumer-linked evidence generation for life sciences research |

| Altoida | United States | Niche Player | Cognitive digital biomarkers | United States, Europe | Continued neurodegenerative disease assessment activity |

By Offering

The digital biomarker market by offering is led by data collection tools, which held approximately 68.0% share in 2025, equal to USD 3.43 billion. Wearables, smartphones, connected spirometers, smart rings, ECG patches, glucose monitors, and actigraphy devices dominate because the algorithm layer cannot operate without reliable longitudinal signals. Empatica, Apple, Ametris, and Garmin-linked research workflows benefit from this structure because procurement teams often start with devices before buying analytics.

Software analytics represented approximately 22.0% share in 2025, equal to USD 1.11 billion. This segment includes signal processing, endpoint calculation, anomaly detection, disease progression modeling, dashboards, and trial data integration. Medidata, IQVIA, Koneksa, and Clario compete here because sponsors need auditable pipelines that convert raw movement, sleep, heart rhythm, and respiratory signals into usable trial variables.

Services represented approximately 10.0% share in 2025, equal to USD 0.50 billion. Services include protocol design, endpoint selection, validation strategy, statistical analysis plans, patient support, regulatory submissions, and data monitoring. This share is smaller than device revenue, but margins are attractive because digital biomarker implementation requires clinical science, biostatistics, and regulatory documentation.

By Application

The digital biomarker market by application is led by clinical trials, which held approximately 46.0% share in 2025, equal to USD 2.32 billion. Clinical trials dominate because pharmaceutical sponsors use digital endpoints to capture mobility, sleep, tremor, heart rhythm, activity, and symptom variation between site visits. FDA and EMA guidance has reduced uncertainty, while Medidata, Clario, IQVIA, Koneksa, and Ametris benefit from sponsor demand for validated workflows.

Remote patient monitoring held approximately 27.0% share in 2025, equal to USD 1.36 billion. This segment grows because health systems need earlier deterioration signals for cardiometabolic disease, COPD, epilepsy, Parkinson’s disease, and sleep disorders. Empatica, Huma, Biofourmis-linked care models, and hospital-at-home platforms compete by converting continuous signals into escalation logic.

Diagnostics and screening held approximately 15.0% share in 2025, equal to USD 0.76 billion. This segment remains smaller because diagnostic claims require stricter evidence than monitoring or exploratory endpoints. Apple’s AFib History qualification and Empatica’s regulated platform show how digital biomarkers can move toward medical-grade use, but broad reimbursement remains uneven.

Personalized treatment and drug response monitoring held approximately 12.0% share in 2025, equal to USD 0.60 billion. This segment is attractive in oncology, neurology, psychiatry, and metabolic disease because it connects therapy response with daily function. Adoption is slower than clinical trials because treatment adjustment requires physician workflow integration and payer alignment.

By Therapeutic Area

The digital biomarker market by therapeutic area is led by cardiology and metabolic disease, which held approximately 30.0% share in 2025, equal to USD 1.51 billion. Cardiovascular monitoring benefits from mature sensors for heart rate, rhythm, activity, blood oxygen, and sleep. Apple, Empatica, iRhythm-style cardiac monitoring platforms, IQVIA, and Medidata support this segment through device-derived evidence and trial analytics.

Neurology held approximately 26.0% share in 2025, equal to USD 1.31 billion. Parkinson’s disease, Alzheimer’s disease, epilepsy, multiple sclerosis, Huntington’s disease, and movement disorders need continuous measurement because clinic assessments miss daily variability. Koneksa, Empatica, Altoida, Roche-linked research programs, and academic neurology groups are active because gait, tremor, cognition, sleep, and medication response can be measured digitally.

Respiratory and sleep disorders held approximately 18.0% share in 2025, equal to USD 0.91 billion. This segment includes COPD, asthma, sleep apnea, insomnia, circadian rhythm disturbance, and actigraphy-based assessment. Empatica’s EmbraceMini FDA clearance for sleep monitoring in January 2026 strengthened the regulated device pathway for actigraphy-based digital biomarkers.

Psychiatry, oncology, and other areas held approximately 26.0% share in 2025, equal to USD 1.31 billion. Mental health demand is rising because passive smartphone signals, sleep, activity, speech, and digital behavior may support depression, anxiety, and relapse monitoring. The FDA’s November 2025 advisory discussion on generative AI-enabled digital mental health devices shows that oversight is intensifying as software moves closer to clinical decisions.

By End-User

The digital biomarker market by end-user is led by pharmaceutical and biotechnology companies, which held approximately 52.0% share in 2025, equal to USD 2.62 billion. This end-user group buys digital biomarkers to support clinical trials, patient stratification, endpoint enrichment, and post-approval evidence. Roche, Novartis, Pfizer, Sanofi, Takeda, and other sponsors use vendors such as Medidata, Clario, IQVIA, Koneksa, and Ametris when trial protocols require sensor-derived endpoints.

Healthcare providers held approximately 24.0% share in 2025, equal to USD 1.21 billion. Hospitals and specialty clinics adopt digital biomarkers for epilepsy monitoring, cardiology follow-up, sleep evaluation, and chronic disease management. Empatica, Huma, Apple-linked clinical workflows, and remote monitoring platforms compete because providers need patient-facing tools and clinician-facing triage dashboards.

Payers, research institutes, and digital therapeutics companies held approximately 24.0% share in 2025, equal to USD 1.21 billion. Payers evaluate digital biomarkers when they can reduce admissions, improve adherence, or support risk scoring. Academic centers and research networks use them for neurology, aging, psychiatry, and rare disease studies where traditional site-based assessments are slow and expensive.

Regional Analysis

The digital biomarker market in North America held approximately 59.0% share in 2025, equal to USD 2.97 billion. The United States accounts for most regional revenue because FDA guidance, Apple’s MDDT qualification, Empatica clearances, IQVIA analytics, Medidata infrastructure, Clario endpoint data, and decentralized trial investment are concentrated there. Canada contributes through academic digital health research and remote care programs. North America’s share is larger than Europe’s because U.S. sponsors spend more on regulated trial technology.

The digital biomarker market in Europe held approximately 23.0% share in 2025, equal to USD 1.16 billion. Germany, the United Kingdom, France, Italy, Switzerland, and the Nordics are the main contributors because EMA qualification advice, EU MDR 2017/745, GDPR, and university-led neurology programs encourage evidence-based digital health. EMA’s qualification process for novel methodologies supports digital endpoint discussions in medicine development.

The digital biomarker market in Asia Pacific held approximately 13.0% share in 2025, equal to USD 0.66 billion. Japan, China, South Korea, India, Singapore, and Australia drive adoption through aging populations, connected device penetration, and clinical trial digitization. Japan and South Korea lead in regulated medtech sophistication, while India and China offer scale for remote monitoring and smartphone-based health data capture.

The digital biomarker market in Latin America held approximately 3.0% share in 2025, equal to USD 0.15 billion. Brazil, Mexico, Argentina, Chile, and Colombia are the main demand centers. Adoption is slower because reimbursement, trial infrastructure, and device access remain uneven. Growth is expected through multinational clinical trials and cardiometabolic disease monitoring.

The digital biomarker market in the Middle East & Africa held approximately 2.0% share in 2025, equal to USD 0.10 billion. Saudi Arabia, the United Arab Emirates, Israel, South Africa, and Qatar lead because digital health infrastructure and specialty-care investment are higher than regional averages. The region’s opportunity is strongest in remote chronic disease monitoring, hospital-at-home programs, and trial recruitment for multinational sponsors.

Country Analysis

The digital biomarker market in the United States was valued at approximately USD 2.65 billion in 2025 and is forecast to grow at a 22.4% CAGR through 2034. FDA guidance, the Biomarker Qualification Program, the MDDT pathway, and the Digital Health Advisory Committee shape procurement decisions. CDC’s USD 4.9 trillion chronic disease cost estimate gives providers and payers a financial reason to evaluate remote physiological monitoring.

The digital biomarker market in Germany was valued at approximately USD 0.28 billion in 2025 and is forecast to grow at a 20.8% CAGR through 2034. Germany benefits from EU MDR compliance infrastructure, university hospitals, decentralized trial participation, and digital health reimbursement experience. Demand concentrates in neurology, cardiology, sleep, and metabolic disease because German sponsors and providers require strong clinical evidence before broad adoption.

The digital biomarker market in Japan was valued at approximately USD 0.24 billion in 2025 and is forecast to grow at a 24.0% CAGR through 2034. Japan’s aging population, pharmaceutical R&D base, robotics culture, and connected device adoption support demand. Neurology, dementia, sleep, and mobility assessment are attractive use cases because functional decline can be measured continuously.

The digital biomarker market in China was valued at approximately USD 0.22 billion in 2025 and is forecast to grow at a 25.5% CAGR through 2034. China’s smartphone scale, hospital digitization, local wearable manufacturing, and clinical trial expansion support adoption. Regulatory scrutiny over health data and algorithmic claims remains the main restraint because digital biomarkers require trust in data integrity and model performance.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Offering

- Software

- Wearable Devices

- Mobile Applications

- Data Analytics Platforms

- Cloud-Based Digital Biomarker Solutions

- Services

- Artificial Intelligence (AI)-Enabled Platforms

- Others

By Application

- Disease Diagnosis

- Disease Monitoring

- Drug Discovery and Development

- Clinical Trials

- Remote Patient Monitoring

- Personalized Medicine

- Preventive Healthcare

- Health and Wellness Monitoring

- Others

By Therapeutic Area

- Neurological Disorders

- Cardiovascular Diseases

- Respiratory Diseases

- Oncology

- Diabetes and Metabolic Disorders

- Mental Health Disorders

- Musculoskeletal Disorders

- Infectious Diseases

- Rare Diseases

- Others

By End-User

- Pharmaceutical and Biotechnology Companies

- Healthcare Providers

- Hospitals and Clinics

- Contract Research Organizations (CROs)

- Academic and Research Institutes

- Health Insurance Companies

- Digital Health Companies

- Government and Public Health Organizations

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.04 B |

| Forecast Revenue (2034) | USD 31.82 B |

| CAGR (2025-2034) | 22.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software, Wearable Devices, Mobile Applications, Data Analytics Platforms, Cloud-Based Digital Biomarker Solutions, Services, Artificial Intelligence (AI)-Enabled Platforms, Others), By Application, (Disease Diagnosis, Disease Monitoring, Drug Discovery and Development, Clinical Trials, Remote Patient Monitoring, Personalized Medicine, Preventive Healthcare, Health and Wellness Monitoring, Others), By Therapeutic Area, (Neurological Disorders, Cardiovascular Diseases, Respiratory Diseases, Oncology, Diabetes and Metabolic Disorders, Mental Health Disorders, Musculoskeletal Disorders, Infectious Diseases, Rare Diseases, Others), By End-User, (Pharmaceutical and Biotechnology Companies, Healthcare Providers, Hospitals and Clinics, Contract Research Organizations (CROs), Academic and Research Institutes, Health Insurance Companies, Digital Health Companies, Government and Public Health Organizations, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MEDIDATA SOLUTIONS, IQVIA HOLDINGS INC., CLARIO HOLDINGS, INC., EMPATICA S.R.L., AMETRIS, KONEKSA HEALTH, MEDABLE INC., HUMA THERAPEUTICS, EVIDATION HEALTH, ALTOIDA, APPLE INC., FITBIT HEALTH SOLUTIONS, GARMIN HEALTH, BIOFOURMIS, IXLAYER, NEURALIGHT, ROCHE DIGITAL HEALTH PROGRAMS, TAKEDA DIGITAL HEALTH PROGRAMS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Component & Platform (Data Collection Tools, Wearable Sensors, Mobile Apps, Implantables, Data Integration Software, Analytics Platforms), By Therapeutic Area (Cardiovascular, Neurology, Oncology, Metabolic Disorders), By End-User (Pharma & Biotech Companies, Healthcare Providers, CROs, Payers) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

, By Component & Platform (Data Collection Tools, Wearable Sensors, Mobile Apps, Implantables, Data Integration Software, Analytics Platforms), By Therapeutic Area (Cardiovascular, Neurology, Oncology, Metabolic Disorders), By End-User (Pharma & Biotech Companies, Healthcare Providers, CROs, Payers) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

, By Component & Platform (Data Collection Tools, Wearable Sensors, Mobile Apps, Implantables, Data Integration Software, Analytics Platforms), By Therapeutic Area (Cardiovascular, Neurology, Oncology, Metabolic Disorders), By End-User (Pharma & Biotech Companies, Healthcare Providers, CROs, Payers) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

Frequently Asked Questions

How big is the Digital Biomarker Market?

The Global Continuous Glucose Monitor Market was valued at USD 12.10 Billion in 2024 and USD 13.80 Billion in 2025, and is projected to reach USD 47.74 Billion by 2034, growing at a CAGR of 14.8% from 2026 to 2034. Market growth is driven by wearable glucose monitoring, diabetes management, and digital healthcare technologies.

Who are the major players in the Digital Biomarker Market?

MEDIDATA SOLUTIONS, IQVIA HOLDINGS INC., CLARIO HOLDINGS, INC., EMPATICA S.R.L., AMETRIS, KONEKSA HEALTH, MEDABLE INC., HUMA THERAPEUTICS, EVIDATION HEALTH, ALTOIDA, APPLE INC., FITBIT HEALTH SOLUTIONS, GARMIN HEALTH, BIOFOURMIS, IXLAYER, NEURALIGHT, ROCHE DIGITAL HEALTH PROGRAMS, TAKEDA DIGITAL HEALTH PROGRAMS, Others

Which segments covered the Digital Biomarker Market?

By Offering, (Software, Wearable Devices, Mobile Applications, Data Analytics Platforms, Cloud-Based Digital Biomarker Solutions, Services, Artificial Intelligence (AI)-Enabled Platforms, Others), By Application, (Disease Diagnosis, Disease Monitoring, Drug Discovery and Development, Clinical Trials, Remote Patient Monitoring, Personalized Medicine, Preventive Healthcare, Health and Wellness Monitoring, Others), By Therapeutic Area, (Neurological Disorders, Cardiovascular Diseases, Respiratory Diseases, Oncology, Diabetes and Metabolic Disorders, Mental Health Disorders, Musculoskeletal Disorders, Infectious Diseases, Rare Diseases, Others), By End-User, (Pharmaceutical and Biotechnology Companies, Healthcare Providers, Hospitals and Clinics, Contract Research Organizations (CROs), Academic and Research Institutes, Health Insurance Companies, Digital Health Companies, Government and Public Health Organizations, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date