- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Digital Forensics Market Size, Share & Forecast | CAGR 12.1%

Global Digital Forensics Market Size, Share, Analysis By Component (Services, Software & Tooling, Hardware), By Type (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory & Database Forensics), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By End-User (Government & Defense, BFSI, Healthcare, IT & Telecommunications, Retail & E-Commerce, Manufacturing) Industry Trends, Competitive Landscape & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

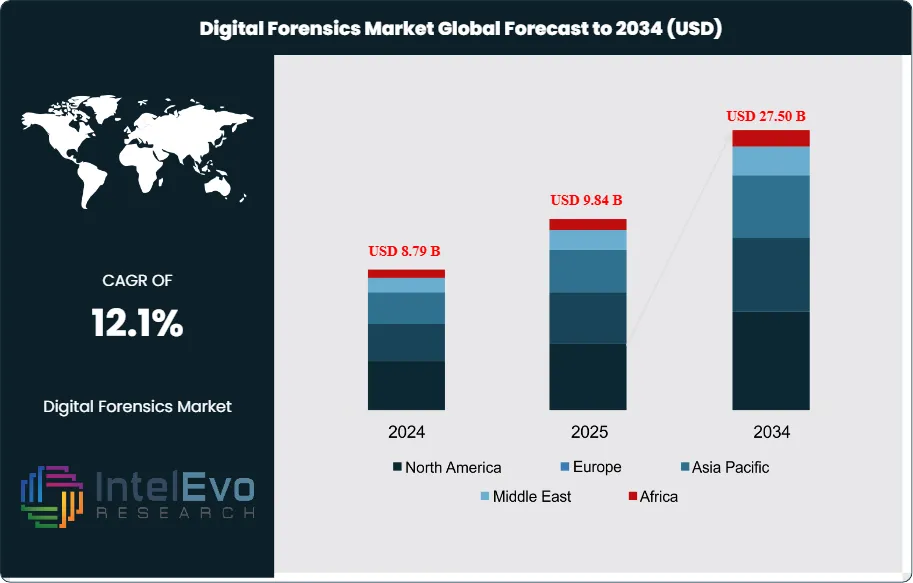

| USD 9.84 Billion | USD 27.50 Billion | 12.1% | North America, 39.6% |

The Digital Forensics Market was valued at approximately USD 8.79 Billion in 2024 and reached USD 9.84 Billion in 2025. The market is projected to grow to USD 27.50 Billion by 2034, expanding at a CAGR of 12.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 17.66 Billion over the analysis period, a trajectory anchored by the SEC Cybersecurity Disclosure Rule (17 CFR Part 229 amendments) effective December 2023 which mandated 8-K disclosure of material cyber incidents within four business days, converting forensic investigation from a discretionary post-breach activity into a compliance-critical process with specific timeline obligations. Enforcement intensified during 2024-2025 with 47 enforcement actions brought under the rule, a frequency that moved digital forensics procurement budgets from cyber insurance claim-driven reimbursement to upfront enterprise security line items at the board-committee level.

Get More Information about this report -

Request Free Sample ReportDemand-side economics shifted fundamentally following the MGM Resorts and Caesars Entertainment breaches of 2023 and the UnitedHealth Change Healthcare incident of February 2024 which cost the payer an estimated USD 2.87 Billion in incident response, ransom, and forensic investigation fees. These incidents converted digital forensics and incident response (DFIR) from a reactive specialty into a standing retainer category. The DORA (Digital Operational Resilience Act) regulation, effective across EU financial institutions from January 2025, imposed mandatory third-party DFIR readiness testing on 1,800+ banks and investment firms, effectively expanding the addressable European market for forensic services by an estimated EUR 340 Million annually. CISA's March 2025 binding operational directive BOD-25-01 required federal civilian executive branch agencies to maintain 24-hour forensic artifact retention capability across cloud and endpoint assets, routing USD 1.1 Billion of federal cybersecurity budget toward forensic tooling and managed services through FY26.

Technology inflection points in the digital forensics market reshaped investigative economics during 2024-2025. AI-assisted artifact correlation reduced average incident triage time from 14.3 days to 5.8 days in deployments at tier-1 enterprises, a productivity improvement that absorbed the effect of the persistent analyst shortage (the sector still operates with an estimated 340,000 unfilled cybersecurity roles globally). Cloud-native forensics platforms capable of acquiring volatile evidence from AWS, Azure, and Google Cloud environments without service disruption reached feature parity with traditional endpoint forensics during Q2 2025, a capability gap closure that opened procurement budgets at cloud-first enterprises who had previously kept forensic retainers minimal. This growth pattern echoes the EDR market's 2018-2021 trajectory, where regulatory and insurance-driven demand preceded genuine product maturity by approximately 24 months before both forces aligned into a compound growth phase.

While headline figures suggest broad expansion, revenue concentration among the top six vendors tightened from 48% in 2022 to 56% in 2025, a consolidation driven by the technical depth required for court-admissible evidence handling under Federal Rules of Evidence 901 and 902 and the European equivalent ENISA forensic evidence guidelines. Preliminary Q1 2025 procurement data suggests managed DFIR services grew at 18.4% year-over-year against 9.7% for standalone forensic software, reflecting customer preference for outcome-based engagements over tooling. Regional investment hotspots include the Washington DC federal contracting corridor, Tel Aviv's cybersecurity startup cluster (which attracted USD 840 Million in DFIR-adjacent Series A and B funding during 2025), and Singapore's Cyber Security Agency-anchored ASEAN DFIR hub. The digital forensics market sits at the intersection of mandatory disclosure regimes, cloud infrastructure complexity, and AI-driven investigative efficiency, a combination that supports the forecast growth path through 2034.

, By Type (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory & Database Forensics), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By End-User (Government & Defense, BFSI, Healthcare, IT & Telecommunications, Retail & E-Commerce, Manufacturing) Industry Trends, Competitive Landscape & Forecast 2026-2034")

Key Takeaways

- Market Growth: The digital forensics market expanded from USD 9.84 Billion in 2025 toward a projected USD 27.50 Billion by 2034, registering a 12.1% CAGR driven by SEC Cybersecurity Disclosure Rule enforcement, DORA regulatory obligations on EU financial institutions, and cloud-native forensic capability maturation.

- Segment Dominance: Services captured 61.4% of 2025 revenue because managed DFIR retainers and incident response engagements command 3-5x higher annual contract value than standalone software licenses, and enterprises increasingly outsource forensic analyst capacity amid the persistent 340,000-role cybersecurity hiring gap.

- Segment Dominance: Computer forensics held 42.8% of type-based segment revenue in 2025 because endpoint evidence acquisition remains the foundational investigative category across all breach types, with court-admissible chain-of-custody procedures tied to Federal Rules of Evidence 901 standards that newer modalities still reference as baseline.

- Driver: The SEC's December 2023 Cybersecurity Disclosure Rule amendments, enforced via 47 actions during 2024-2025, created a USD 1.8 Billion compliance-driven demand inflection as public companies built standing forensic investigation capability to meet four-business-day materiality determination obligations under Item 1.05 of Form 8-K.

- Restraint: The global shortage of 340,000 unfilled cybersecurity roles compressed service provider gross margins by 410 basis points during 2024-2025, with certified GIAC GCFA and EnCE analyst wage inflation reaching 28% year-over-year in major US metropolitan markets.

- Opportunity: Cloud-native forensics and multi-cloud evidence acquisition represent a USD 4.2 Billion addressable opportunity through 2030, unlocked by regulatory acceptance of hypervisor-level memory capture under NIST SP 800-86 Revision 1 updates published in 2024 and the expansion of cloud provider cooperative evidence APIs.

- Trend: AI-assisted artifact correlation reduced incident triage time from 14.3 days to 5.8 days across tier-1 deployments, with adoption reaching 52% of North American DFIR vendors against 19% of Asia Pacific providers, a diffusion gap that is driving USD 720 Million in vendor acquisitions and platform partnerships during 2024-2025.

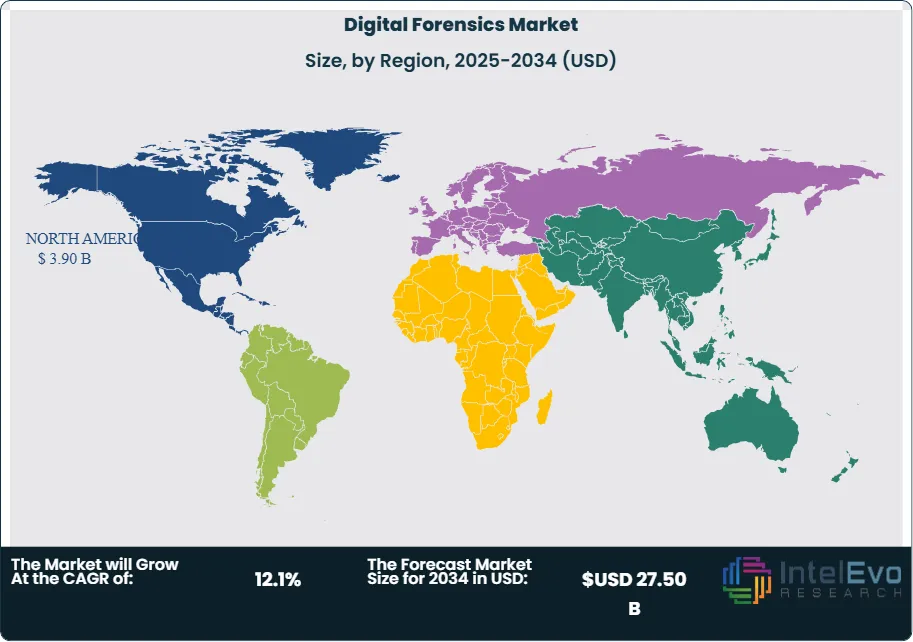

- Regional Analysis: North America led with 39.6% market share worth USD 3.90 Billion in 2025, supported by SEC enforcement density, the concentration of federal DFIR contract vehicles under GSA Schedule 70 and CIO-SP4, and the Washington DC federal cybersecurity contracting corridor anchoring roughly 38% of US federal forensic spend.

Competitive Landscape Overview

Competitive structure in the digital forensics market is moderately consolidated. The top four vendors controlled an estimated 44.6% of 2025 revenue, a concentration that expanded 4 percentage points since 2022 as smaller pure-play vendors exited under the capital intensity of maintaining both endpoint, network, mobile, and cloud forensic capabilities. Competition runs on three axes: depth of court-admissible evidence handling (validated under Federal Rules of Evidence 901 and Daubert precedents), breadth of cloud-native acquisition capability across AWS, Azure, GCP, and SaaS targets, and integration with security operations centers via SOAR and SIEM platforms. Four vertical integration deals valued at a combined USD 3.6 Billion closed during 2025 as managed security service providers acquired boutique DFIR firms to defend margin against commodity-grade tooling from newer entrants.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Regional Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| OpenText Corporation | Canada | Leader | EnCase Forensic and Tableau | North America | Launched EnCase 24.4 with native Microsoft 365 cloud acquisition in Mar 2025, closing key gap vs Magnet Forensics |

| Magnet Forensics (Thoma Bravo) | Canada | Leader | AXIOM Cyber and Verakey | North America, Europe | Acquired Belkasoft in Jan 2025 for USD 180M to extend mobile forensics coverage across 42,000 device models |

| Cellebrite DI Ltd. | Israel | Leader | UFED Premium and Inseyets | Global | Secured USD 240M five-year contract with DHS ICE in May 2025 for nationwide UFED deployment |

| Exterro Inc. | USA | Leader | FTK Forensic Toolkit and Review | North America | Released FTK 9.0 in Sep 2025 with AI artifact correlation cutting triage time by 62% on benchmark cases |

| Paraben Corporation | USA | Challenger | E3 Forensic Platform | North America | Expanded mobile IoT forensic coverage in Jul 2025 to include smart vehicle infotainment systems |

| MSAB (Micro Systemation) | Sweden | Challenger | XRY and XAMN | Europe | Won EU Frontex mobile forensics framework contract valued at EUR 48M in Jun 2025 |

| IBM Corporation | USA | Challenger | X-Force Incident Response | Global | Integrated QRadar SIEM with native forensic artifact acquisition in Feb 2026 under Project Verisense |

| Mandiant (Google Cloud) | USA | Niche Player | Mandiant Consulting | Global | Launched Mandiant Hunt Plus retainer tier in Oct 2025 priced from USD 480K annual minimum commitment |

By Component.

Services captured 61.4% of digital forensics market revenue in 2025, worth USD 6.04 Billion, because managed DFIR retainers and incident response engagements command 3-5x higher annual contract value than standalone software licenses. Enterprises increasingly outsource forensic analyst capacity amid the 340,000-role cybersecurity hiring gap, and cyber insurance carriers progressively required named DFIR retainers as a coverage precondition during 2024-2025 policy renewals. Software and tooling represented 28.6% of revenue at USD 2.81 Billion, growing at 9.8% as the commodification of basic endpoint acquisition capability compressed standalone license pricing by an estimated 15% year-over-year. Hardware (forensic workstations, write-blockers, mobile acquisition devices) held 10.0% share at USD 0.98 Billion, a mature sub-segment where Tableau and CRU write-blocker pricing has remained flat. Within Services, proactive readiness and tabletop exercises grew fastest at 22.1% annually as CISOs shifted spend from incident-only engagements toward standing retainers with breach-simulation components.

By Type.

Computer forensics held 42.8% of type-based segment revenue in 2025 at USD 4.21 Billion because endpoint evidence acquisition remains the foundational investigative category across all breach types, with court-admissible chain-of-custody procedures tied to Federal Rules of Evidence 901 standards that newer modalities still reference as baseline. Mobile device forensics captured 26.2% share, the fastest-accelerating type at 16.4% annual growth, driven by Cellebrite Inseyets and Magnet Forensics Verakey capability expansions that cracked iOS 17 and Android 14 encrypted enclaves during Q3-Q4 2024. Network forensics represented 16.8% of revenue, anchored by Palo Alto Networks Cortex XDR and Corelight network traffic reconstruction adoption at SOC operations. Cloud forensics held 9.4% share but recorded 28.3% annual growth, the highest of any type category, as enterprises remediate the 2023-2024 gap between cloud adoption and cloud-native forensic capability. Memory forensics and database forensics together represented 4.8% of type revenue.

By Deployment Mode.

On-premise deployment captured 54.2% of digital forensics market revenue in 2025 because court-admissibility requirements and evidence chain-of-custody protocols favor air-gapped forensic environments that isolate evidence from production networks. Law enforcement agencies in particular maintain near-exclusive on-premise preference, with the FBI, DEA, and state police forensic labs deploying Cellebrite UFED and Magnet AXIOM on standalone workstations rather than cloud endpoints. Cloud-based deployments held 32.8% share, the fastest-growing mode at 18.2% annual growth as cloud-native forensics platforms achieved feature parity with on-premise offerings during Q2 2025 and regulatory acceptance of hypervisor-level memory capture under NIST SP 800-86 Revision 1 removed prior admissibility concerns. Hybrid deployments accounted for 13.0% share, concentrated at financial services customers subject to DORA operational resilience testing that requires both on-premise and cloud evidence acquisition capability.

By End-User.

Government and defense agencies represented 34.6% of 2025 end-user revenue, the dominant category driven by federal law enforcement (FBI, DEA, ATF), Department of Homeland Security components, and state-level police forensic laboratories. Government procurement volumes rose 14.2% year-over-year supported by CISA BOD-25-01 and the FY2025 National Defense Authorization Act cybersecurity provisions. BFSI (banking, financial services, insurance) captured 24.8% share, accelerated by DORA enforcement in EU institutions and the SEC Cybersecurity Disclosure Rule in US public financial firms. Healthcare and life sciences held 16.2% share with 19.8% year-over-year growth following the Change Healthcare incident and HHS OCR's 2025 HIPAA Security Rule amendments requiring documented forensic readiness. IT and telecommunications captured 12.4%, retail and e-commerce 7.2%, and manufacturing and industrial 4.8%. The healthcare sub-segment's growth inflection followed the first HHS OCR enforcement settlement explicitly citing inadequate forensic investigation capability, a USD 4.75 Million penalty against a regional health system in Q1 2025.

Regional Analysis

North America.

Backed by SEC enforcement density, federal DFIR contract vehicles under GSA Schedule 70 and CIO-SP4, and the Washington DC federal cybersecurity contracting corridor anchoring roughly 38% of US federal forensic spend, North America's digital forensics market captured 39.6% of 2025 revenue at USD 3.90 Billion. The DC-Maryland-Virginia technology corridor hosts Mandiant, CrowdStrike's federal services division, and Booz Allen Hamilton's cyber practice, collectively generating an estimated USD 1.14 Billion in 2025 federal DFIR service revenue. New York's financial district and the San Francisco Bay Area anchor commercial DFIR demand from BFSI and technology sectors respectively. Canada's Communications Security Establishment and the RCMP National Cybercrime Coordination Unit expanded forensic capability procurement under CAD 875 Million allocated in the 2024 federal budget. Mexico's creation of the Guardia Nacional cyber division in late 2024 opened a nascent federal DFIR market, though cross-border sample referrals to US laboratories represented an estimated 42% of Mexican enterprise forensic volume in 2025.

Europe.

Regulatory enforcement under the Digital Operational Resilience Act (DORA Regulation 2022/2554), in force from January 2025, reshaped procurement patterns across the European digital forensics market, which held 27.4% share worth USD 2.70 Billion in 2025. DORA's mandatory threat-led penetration testing (TLPT) and third-party DFIR readiness requirements at 1,800+ EU financial institutions generated an estimated EUR 340 Million in incremental forensic service demand annually. Germany's BSI (Federal Office for Information Security) expanded its CERT-Bund operations with EUR 180 Million in 2025 allocations, concentrating demand at Frankfurt-based DFIR providers. The UK's National Cyber Security Centre continued its Active Cyber Defence programme expansion, and the UK Financial Conduct Authority extended cyber incident reporting thresholds under PS24/3 effective October 2024. France's ANSSI accredited 14 new PRIS forensic service providers during 2024-2025 under the French cybersecurity qualification scheme. Ireland's Data Protection Commission maintained the highest enforcement rate on GDPR breach notification timelines, requiring 72-hour forensic root-cause documentation that drove retainer adoption across Dublin-hubbed tech firms.

Asia Pacific.

Manufacturing capacity for cybersecurity infrastructure across Shenzhen and Hangzhou, combined with Japan's METI-led cybersecurity resilience funding program, propelled Asia Pacific's digital forensics market to 22.8% global share, valued at USD 2.24 Billion in 2025. China's Cybersecurity Law enforcement by the Cyberspace Administration of China drove domestic forensic capability investment at state-owned enterprises and critical information infrastructure operators, though Western DFIR vendor access remained constrained by the Measures for the Security Assessment of Network Products and Services. Japan's cybersecurity market benefited from the 2024 Active Cyber Defense legislation, with Tokyo's NEC, NTT Data, and Fujitsu expanding DFIR service practices. India's digital forensics market grew at 17.6% annually, the fastest in the region, driven by CERT-In reporting obligations, the Digital Personal Data Protection Act of 2023 enforcement beginning in 2025, and Mumbai's financial sector DFIR procurement. Singapore's Cyber Security Agency anchored an ASEAN-wide DFIR hub, with the Infocomm Media Development Authority accrediting 28 CREST-certified providers by Q3 2025. Australia's expanded Cyber Security Strategy 2023-2030 funding flowed through the Australian Signals Directorate and REDSPICE program.

Latin America.

Currency volatility across Argentina and regulatory asymmetry constrained capital equipment procurement, yet Latin America's digital forensics market still reached USD 544 Million (5.5% global share) in 2025, driven primarily by Brazilian public sector demand and financial institution breach response. Brazil's LGPD (General Data Protection Law) enforcement by the Autoridade Nacional de Protecao de Dados issued 34 notifications during 2024-2025 that required documented forensic investigation, concentrated at Sao Paulo and Rio de Janeiro headquartered enterprises. The Federal Police's Instituto Nacional de Criminalistica expanded its Brasilia-based digital forensics lab with BRL 240 Million in 2025 allocations. Mexico's creation of the Guardia Nacional cyber division and Colombia's Ministerio TIC cybersecurity strategy created nascent federal DFIR opportunities. Chile's Ley Marco de Ciberseguridad, enacted March 2024 and effective 2025, established the first binding cyber incident reporting framework in the Southern Cone. Argentina's pure-play DFIR market faced 31% peso depreciation during 2024-2025, pushing enterprises toward regional shared-service DFIR consumption from Brazilian and Uruguayan providers.

Middle East & Africa.

Saudi Arabia's National Cybersecurity Authority mandates and the UAE's Cybersecurity Council strategy opened a new demand corridor, pushing the MEA digital forensics market to USD 464 Million (4.7% share) in 2025. Saudi Arabia's NCA Essential Cybersecurity Controls (ECC-1:2018, updated 2024) mandated forensic readiness at critical national infrastructure operators including Saudi Aramco, SABIC, and the National Water Company. The UAE's 2024 cybersecurity strategy, administered by the Cybersecurity Council and TDRA, accredited 18 DFIR service providers under the Dubai Electronic Security Center framework. Israel remains the region's largest DFIR market despite its geographic ambiguity, with Tel Aviv's cybersecurity cluster generating an estimated USD 140 Million in 2025 domestic DFIR revenue and serving as the R&D origin for Cellebrite, Cybereason, and Claroty platforms. South Africa's POPIA (Protection of Personal Information Act) enforcement by the Information Regulator drove demand at Johannesburg's banking sector and the State Security Agency. Nigeria's 2024 cybersecurity levy funded the National Information Technology Development Agency's forensic capability expansion. The region's shortage of GIAC and EnCE certified analysts remains a structural constraint, with fewer than 3,200 certified practitioners across the entire MEA geography as of 2025.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Services (Managed DFIR, Incident Response, Advisory)

- Software and Tooling

- Hardware (Workstations, Write-Blockers, Acquisition Devices)

By Type

- Computer Forensics

- Mobile Device Forensics

- Network Forensics

- Cloud Forensics

- Memory and Database Forensics

By Deployment Mode

- On-Premise

- Cloud-Based

- Hybrid

By End-User

- Government and Defense

- Banking, Financial Services, and Insurance (BFSI)

- Healthcare and Life Sciences

- IT and Telecommunications

- Retail and E-Commerce

- Manufacturing and Industrial

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 9.84 B |

| Forecast Revenue (2034) | USD 27.50 B |

| CAGR (2025-2034) | 12.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Services (Managed DFIR, Incident Response, Advisory), Software and Tooling, Hardware (Workstations, Write-Blockers, Acquisition Devices)), By Type, (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory and Database Forensics), By Deployment Mode, (On-Premise, Cloud-Based, Hybrid), By End-User, (Government and Defense, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecommunications, Retail and E-Commerce, Manufacturing and Industrial) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | OPENTEXT CORPORATION, MAGNET FORENSICS (THOMA BRAVO), CELLEBRITE DI LTD., EXTERRO INC., PARABEN CORPORATION, MSAB (MICRO SYSTEMATION AB), IBM CORPORATION, MANDIANT (GOOGLE CLOUD), CROWDSTRIKE HOLDINGS, INC., BOOZ ALLEN HAMILTON, DELL TECHNOLOGIES, OXYGEN FORENSICS, INC., BLACKBAG TECHNOLOGIES (CELLEBRITE), NUIX LIMITED, LOGRHYTHM, INC., PALANTIR TECHNOLOGIES, BINALYZE, GROUP-IB, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Type (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory & Database Forensics), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By End-User (Government & Defense, BFSI, Healthcare, IT & Telecommunications, Retail & E-Commerce, Manufacturing) Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Type (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory & Database Forensics), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By End-User (Government & Defense, BFSI, Healthcare, IT & Telecommunications, Retail & E-Commerce, Manufacturing) Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Type (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory & Database Forensics), By Deployment Mode (On-Premise, Cloud-Based, Hybrid), By End-User (Government & Defense, BFSI, Healthcare, IT & Telecommunications, Retail & E-Commerce, Manufacturing) Industry Trends, Competitive Landscape & Forecast 2026-2034")

Frequently Asked Questions

How big is the Digital Forensics Market?

The Global Digital Forensics Market was valued at USD 8.79 Billion in 2024 and is projected to reach USD 27.50 Billion by 2034, growing at a CAGR of 12.1% from 2026 to 2034. Growth is driven by increasing cybercrime incidents, rising demand for digital evidence investigation, cloud and mobile forensics adoption, cybersecurity investments, IoT device proliferation, and advanced forensic analytics across law enforcement, government, defense, and enterprise sectors worldwide.

Who are the major players in the Digital Forensics Market?

OPENTEXT CORPORATION, MAGNET FORENSICS (THOMA BRAVO), CELLEBRITE DI LTD., EXTERRO INC., PARABEN CORPORATION, MSAB (MICRO SYSTEMATION AB), IBM CORPORATION, MANDIANT (GOOGLE CLOUD), CROWDSTRIKE HOLDINGS, INC., BOOZ ALLEN HAMILTON, DELL TECHNOLOGIES, OXYGEN FORENSICS, INC., BLACKBAG TECHNOLOGIES (CELLEBRITE), NUIX LIMITED, LOGRHYTHM, INC., PALANTIR TECHNOLOGIES, BINALYZE, GROUP-IB, OTHERS

Which segments covered the Digital Forensics Market?

By Component, (Services (Managed DFIR, Incident Response, Advisory), Software and Tooling, Hardware (Workstations, Write-Blockers, Acquisition Devices)), By Type, (Computer Forensics, Mobile Device Forensics, Network Forensics, Cloud Forensics, Memory and Database Forensics), By Deployment Mode, (On-Premise, Cloud-Based, Hybrid), By End-User, (Government and Defense, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecommunications, Retail and E-Commerce, Manufacturing and Industrial)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date