- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Digital Labor Market Size, Share & Forecast | CAGR of 17.05%

Global Digital Labor Market Size, Share, Analysis Report By Platform (Online Platforms, Location-based Platforms); Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

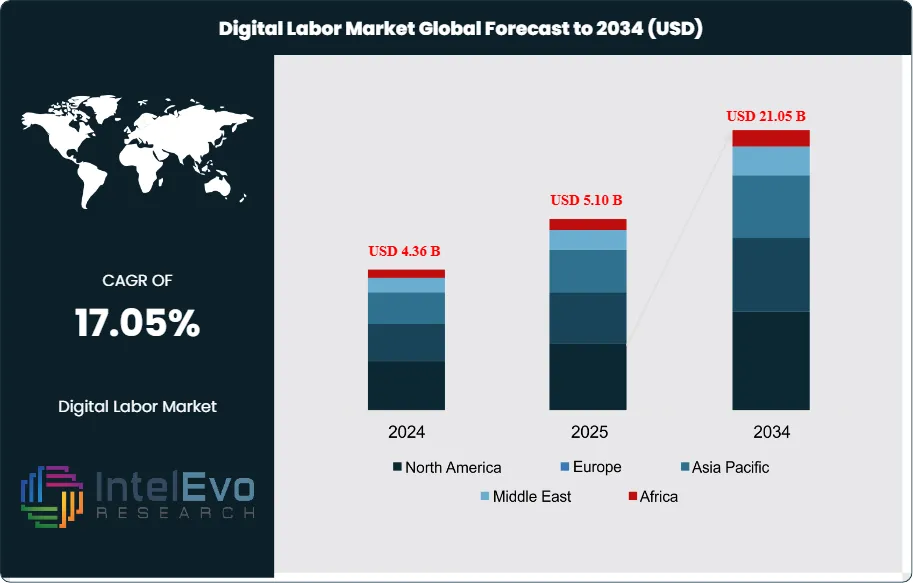

The Digital Labor Market size is expected to be worth around USD 21.05 Billion by 2034, from USD 4.36 Billion in 2024, growing at a CAGR of 17.05% during the forecast period from 2024 to 2034. The Digital Labor Market encompasses software robots, AI-powered agents, and intelligent automation platforms that perform human-like work activities across various business processes. This market includes robotic process automation (RPA), artificial intelligence workers, intelligent process automation (IPA), and cognitive automation solutions that can execute rule-based tasks, make decisions, and interact with digital systems to augment or replace human labor in specific workflows.

The market is experiencing explosive growth driven by the urgent need for operational efficiency, cost reduction, and business process optimization across industries. Organizations are rapidly adopting digital labor solutions to address labor shortages, improve accuracy, reduce operational costs, and enable 24/7 business operations. The acceleration of digital transformation initiatives, combined with advances in AI and machine learning capabilities, is creating unprecedented opportunities for digital workers to handle increasingly complex tasks that were previously exclusive to human workers.

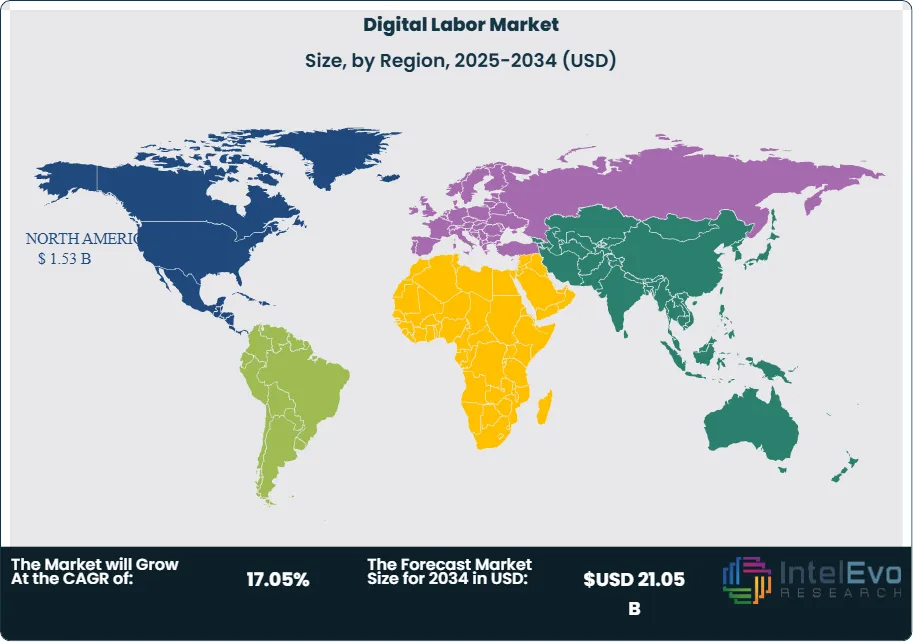

North America leads the global digital labor market, driven by early technology adoption, extensive enterprise digitization, and significant investments in automation technologies. The region benefits from a mature technology ecosystem, strong vendor presence, and enterprise demand for operational efficiency. Asia-Pacific represents the fastest-growing market, fueled by manufacturing automation needs, cost optimization pressures, and government initiatives promoting digital transformation across emerging economies.

The pandemic dramatically accelerated digital labor adoption as organizations sought to maintain business continuity during lockdowns, reduce dependence on physical workforces, and adapt to remote work environments. Companies accelerated automation timelines to address workforce disruptions, ensure operational resilience, and manage increased digital transaction volumes. This trend established digital labor as a strategic necessity rather than an optional efficiency tool, fundamentally changing enterprise automation strategies.

Recent geopolitical tensions and data sovereignty concerns are influencing digital labor deployment strategies, with organizations increasingly focusing on local or regional automation solutions to mitigate compliance risks and ensure data security. Trade restrictions on certain AI technologies and concerns about intellectual property protection are driving demand for domestically developed digital labor solutions and creating opportunities for regional automation vendors.

Get More Information about this report -

Request Free Sample Report; Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The Digital Labor Market is expected to reach USD 21.05 Billion by 2034, fueled by organizations' critical needs for enhanced operational efficiency, cost optimization, and streamlined business processes across various sectors.

- Platform Dominance: Online platforms leads the segment due to their scalability, global access, and ability to efficiently connect businesses with remote talent.

- Application Dominance: Customer support dominates as organizations increasingly utilize digital labor for scalable, cost-efficient, and high-availability service operations.

- Drivers: Key drivers accelerating growth include workforce shortage mitigation and operational efficiency demands, which boost market expansion through cost reduction and productivity improvements.

- Restraints: Growth is hindered by implementation complexity and security concerns, which create challenges such as technical integration difficulties and data protection requirements.

- Opportunities: The market is poised for expansion due to opportunities like AI-powered automation advancement and industry-specific solutions, which enable sophisticated cognitive tasks and specialized applications.

- Trends: Emerging trends including hyperautomation adoption and no-code/low-code platforms are reshaping the market by enabling comprehensive process automation and democratizing automation development.

- Regional Analysis: North America leads owing to technology maturity and enterprise adoption rates. Asia-Pacific and Latin America show high promise due to cost optimization needs and digital transformation initiatives.

Platform Analysis:

Online platforms dominate the digital labor market by leveraging advanced technological infrastructure that enables seamless workforce scalability and global talent accessibility. These platforms utilize sophisticated matching algorithms and automated workflows to efficiently pair businesses with qualified remote workers across diverse skill sets and geographic locations. Their cloud-based architecture supports real-time collaboration, secure payment processing, and comprehensive project management tools that streamline the entire digital work lifecycle. Unlike traditional employment models, online platforms offer instant access to specialized expertise without geographical constraints, allowing organizations to rapidly scale their workforce up or down based on project demands. The platforms' ability to maintain quality standards through rating systems, skill verification, and performance analytics further enhances their appeal to enterprises seeking reliable, cost-effective solutions for various business functions while maintaining operational flexibility.

Application Analysis:

Customer Support Leads With nearly 30% Market Share In Digital Labor Market: Customer support leads the digital labor market as enterprises recognize the strategic advantages of leveraging remote workforce capabilities for service delivery. Organizations are increasingly adopting digital labor solutions to achieve round-the-clock customer assistance across multiple time zones without the overhead costs associated with traditional call centers. This approach enables businesses to rapidly scale their support operations during peak periods while maintaining consistent service quality through trained digital workers who can handle diverse customer inquiries via chat, email, and voice channels. The cost-effectiveness of digital labor allows companies to offer multilingual support and specialized technical assistance without significant infrastructure investments. Additionally, digital workers can be quickly deployed to manage seasonal fluctuations, product launches, or crisis situations, providing the operational agility that modern businesses require to maintain competitive customer service standards while optimizing resource allocation.

Regional Analysis:

North America Leads With more than 35% Market Share In Digital Labor Market: North America maintains its leadership position in the global digital labor market through early technology adoption, extensive enterprise digitization initiatives, and the presence of major automation vendors and technology companies. The region benefits from a mature business process outsourcing industry, strong consulting services ecosystem, and enterprise demand for operational efficiency that drives digital labor adoption. The United States leads regional consumption through its advanced services sector, technology leadership, and aggressive corporate automation strategies across finance, healthcare, and telecommunications industries.

Asia-Pacific represents the fastest-growing regional market, driven by manufacturing automation needs, cost optimization pressures, and government initiatives promoting Industry 4.0 and digital transformation across emerging economies. Countries like India, China, and Singapore are investing heavily in automation technologies to maintain manufacturing competitiveness, improve service delivery, and address labor cost pressures. The region's growth is supported by a large business process outsourcing industry, expanding middle-class consumer markets, and increasing enterprise sophistication in process automation.

Europe maintains a stable market position with steady growth supported by regulatory compliance automation needs, sustainability initiatives, and digital transformation programs across manufacturing and services sectors. The region's emphasis on data privacy, worker protection, and ethical automation creates unique market dynamics that favor sophisticated digital labor solutions with strong governance capabilities. Germany, France, and the United Kingdom lead regional adoption through their strong industrial bases, advanced services sectors, and commitment to digital innovation and process optimization.

Get More Information about this report -

Request Free Sample ReportMarket Key Segment

Platform

- Online Platforms

- Location-based Platforms

Application

- Content Moderation

- Customer Support

- Data Annotation and Labeling

- Others

Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.10 B |

| Forecast Revenue (2034) | USD 21.05 B |

| CAGR (2025-2034) | 17.05% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Platform (Online Platforms, Location-based Platforms); Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Upwork, Toptal, Microsoft Corporation, Fiverr, Deel, Amazon Mechanical Turk, Andela, WorkMarket, OneForma, Appen, Workforce.com, Field Nation, Teemwork.AI, LiveOps, Clickworker |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

; Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

; Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

; Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Frequently Asked Questions

How big is the Digital Labor Market?

Global Digital Labor Market set to hit USD 21.05 Bn by 2034 at 17.05% CAGR. Uncover key technologies, industry demand, and future strategies for businesses.

Who are the major players in the Digital Labor Market?

Upwork, Toptal, Microsoft Corporation, Fiverr, Deel, Amazon Mechanical Turk, Andela, WorkMarket, OneForma, Appen, Workforce.com, Field Nation, Teemwork.AI, LiveOps, Clickworker

Which segments covered the Digital Labor Market?

Platform (Online Platforms, Location-based Platforms); Application (Content Moderation, Customer Support, Data Annotation and Labeling, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date