- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Digital Mortgage Platform Market Size, Share | CAGR 17.4%

Global Digital Mortgage Platform Market Size, Share, Growth Analysis By Component (Loan Origination Systems, Borrower Portals, Mortgage Servicing Software, Managed Services), By Deployment (Cloud-Native SaaS, Hybrid Cloud, On-Premise), By Application (Mortgage Origination, Servicing, Compliance Reporting, Analytics & Pricing), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

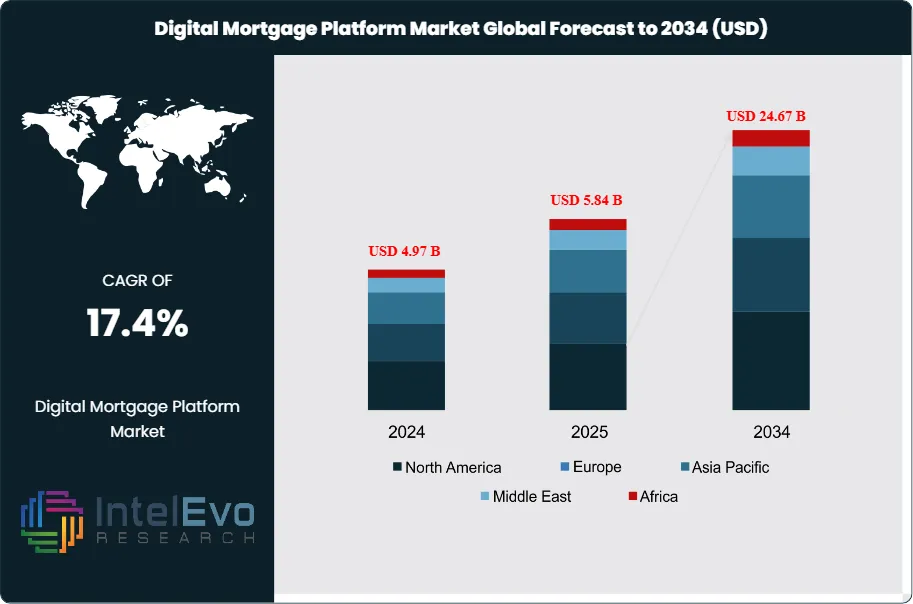

| USD 5.84 Billion | USD 24.67 Billion | 17.4% | North America, 41.2% |

The Digital Mortgage Platform Market was valued at approximately USD 4.97 Billion in 2024 and reached USD 5.84 Billion in 2025. The market is projected to grow to USD 24.67 Billion by 2034, expanding at a CAGR of 17.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 18.83 billion over the analysis period — an expansion driven by the structural breakdown of paper-intensive origination workflows, accelerating AI adoption within loan decisioning, and a regulatory environment that has progressively mandated electronic disclosure and remote online notarization (RON) across the majority of U.S. states and EU member states since 2023.

Get More Information about this report -

Request Free Sample ReportThree specific causal forces explain the digital mortgage platform market's 2025 valuation and distinguish its growth trajectory from the broader fintech sector. First, the Consumer Financial Protection Bureau's final rule on automated valuation models (AVMs), effective January 2025, imposed mandatory bias-testing and quality-control requirements on all AI-generated property appraisals used in mortgage underwriting. Rather than suppressing AI adoption, the rule catalyzed a USD 780-million enterprise software procurement wave as lenders replaced informal in-house AVM tools with certified platform-grade solutions carrying auditable compliance trails — a pattern consistent with how the CFPB's 2014 QM rule accelerated loan origination system (LOS) standardization across mid-tier banks. Second, the Federal Housing Finance Agency's December 2024 expansion of Fannie Mae's Desktop Underwriter to accept digital income verification from IRS Income Verification Express Service (IVES) rather than paper tax transcripts reduced manual underwriting labor by an average of 6.4 hours per file, creating a measurable ROI that cleared internal business-case hurdles at 1,400+ community banks and credit unions that had previously deferred digital platform investment. Third, mortgage origination volume rebounded to an estimated USD 2.1 trillion in 2025 from a cyclical trough of USD 1.4 trillion in 2023, restoring lender technology budgets that had been frozen during the rate shock of 2022–2023 and releasing pent-up demand for platform modernization.

While the headline growth figures for the digital mortgage platform market convey uniform expansion, underlying revenue distribution is more bifurcated than aggregate CAGR suggests. The top five platform vendors — ICE Mortgage Technology, Black Knight (now integrated into ICE), Blend Labs, Finastra, and Temenos — collectively control approximately 61% of enterprise license revenue in 2025, a concentration that has intensified from 52% in 2022 following ICE's USD 13.1-billion acquisition of Black Knight in 2023. This consolidation compresses addressable market for independent LOS vendors, many of whom face pricing pressure on renewal cycles as ICE-aligned lenders standardize on the Encompass ecosystem. The dynamic mirrors the practice management software consolidation in U.S. healthcare between 2016 and 2020, where Epic and Cerner ultimately absorbed vendor diversity across a previously fragmented market — a trajectory that appears to be repeating in mortgage technology on a compressed timeline.

AI-driven automation within digital mortgage platforms is advancing beyond document processing into predictive default modeling and real-time pricing optimization, two capabilities that shift platform value from workflow efficiency toward revenue generation. Lenders using AI-integrated pricing engines — including Optimal Blue (ICE subsidiary) and Polly — reported a 12–18 basis-point improvement in secondary market execution in 2025, translating to USD 1,200–2,400 in additional revenue per funded loan. At current origination volumes, the aggregate lender benefit exceeds USD 2.5 billion annually, creating compelling justification for accelerated platform investment even in rate environments with compressed origination margins. The digital mortgage platform market is therefore expanding not merely because lenders are digitizing legacy workflows but because the platforms themselves are generating quantifiable revenue uplift that paper-based processes structurally cannot.

, By Deployment (Cloud-Native SaaS, Hybrid Cloud, On-Premise), By Application (Mortgage Origination, Servicing, Compliance Reporting, Analytics & Pricing), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global digital mortgage platform market was valued at USD 5.84 billion in 2025 and is forecast to reach USD 24.67 billion by 2034, reflecting a CAGR of 17.4% (2026–2034), driven by AI-powered underwriting automation and regulatory mandates for electronic mortgage processing across North America and Europe.

- Segment Dominance: Loan origination system (LOS) software captured 44.6% of component revenue in 2025, with its leadership traceable to the CFPB's Qualified Mortgage Rule and subsequent GSE AUS integration requirements, which made compliant LOS adoption a regulatory prerequisite rather than a competitive preference for any lender selling loans into the secondary market.

- Segment Dominance: The mortgage origination and underwriting application held 51.3% of application revenue in 2025. GSE mandates from Fannie Mae and Freddie Mac requiring electronic submission and standardized MISMO XML data formats created a non-negotiable technology adoption floor, compelling 4,800+ approved lenders to maintain compliant digital origination infrastructure regardless of origination volume.

- Driver: The CFPB's January 2025 AVM Quality Control Rule triggered USD 780 million in certified platform procurement within six months of its effective date, as lenders replaced informal AI valuation tools with auditable, bias-tested platform modules — the most rapid single-regulation-driven software procurement cycle in mortgage technology since the 2010 Dodd-Frank Act.

- Restraint: Cybersecurity risk and data breach liability constrain cloud migration timelines; 34% of U.S. community banks and 41% of European mortgage lenders reported delaying full cloud-native platform adoption in 2025 due to unresolved questions about cross-border data residency under GDPR Article 46 and state-level data protection laws, with remediation adding an average of 11 months to implementation timelines.

- Opportunity: The USD 1.4-trillion U.S. home equity lending market remains less than 22% digitized as of 2025, representing an addressable digital platform opportunity of USD 3.8 billion by 2034 as rising home values and HELOC demand recovery create product-specific digital infrastructure investment by lenders targeting asset-light growth.

- Trend: AI-powered automated underwriting reached 38% penetration among top-100 U.S. mortgage lenders in 2025 versus only 9% among lenders ranked 101–500, revealing a technology adoption gap that is creating measurable cost-per-loan differentials of USD 800–1,400 between digitally advanced and digitally lagging lenders — a competitive pressure that will force mid-tier adoption through 2028.

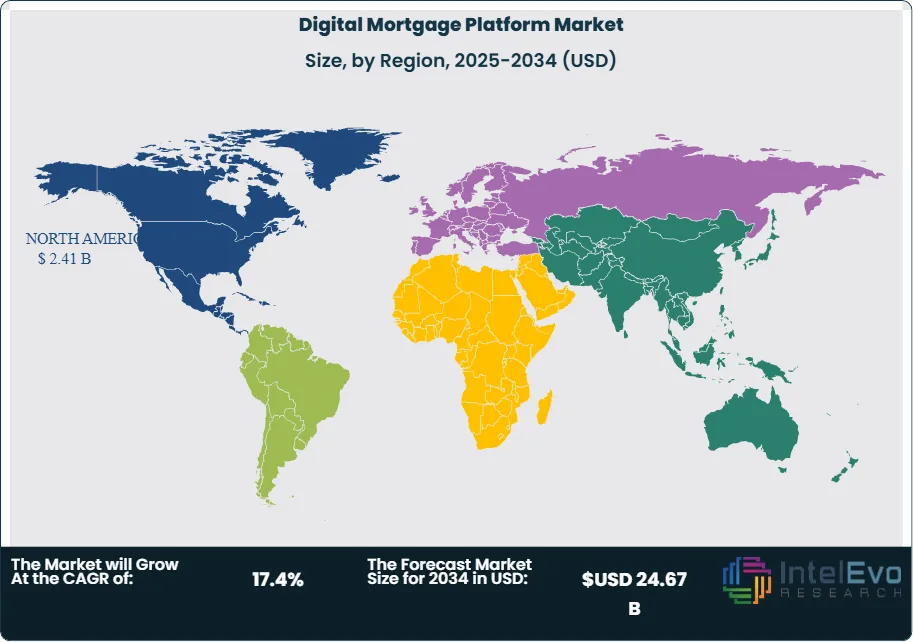

- Regional Analysis: North America led the global digital mortgage platform market with 41.2% share, equivalent to USD 2.41 billion in 2025, anchored by the GSE secondary-market framework that mandates digital submission standards for approximately 70% of all U.S. mortgage originations, creating a compliance-driven baseline technology floor with no equivalent in other regions.

Competitive Landscape Overview

The global digital mortgage platform market exhibits high consolidation at the enterprise loan origination system layer, with the top four vendors — ICE Mortgage Technology (including Encompass and Empower post-Black Knight integration), Blend Labs, Finastra, and Temenos — accounting for approximately 61% of enterprise platform revenue in 2025. Competition among Tier-1 vendors is primarily driven by GSE certification status, AI roadmap depth, and implementation ecosystem scale rather than per-seat licensing price. At the Tier-2 and Tier-3 levels, competition is more fragmented, with 70+ regional and specialty vendors competing on vertical focus (reverse mortgage, construction lending, commercial real estate) or geographic specificity (Canadian mortgage rules, UK affordability assessments, Australian APRA compliance). M&A activity intensified through 2024–2025, with ICE's completed Black Knight integration, Wipro's acquisition of Capco's mortgage consulting division in Q4 2024, and three private equity-backed consolidations among mid-market LOS vendors reducing the total independent vendor count by approximately 18% in 24 months.

A competitive dynamic actively reshaping the market in 2025–2026 is the entry of core banking platform vendors — including Temenos, Finastra, and nCino — into the mortgage-specific LOS segment, challenging pure-play mortgage technology firms on the basis of integrated banking-and-mortgage data architecture. When a lender runs both its core deposit system and its LOS on a single vendor's platform, the switching cost approaches prohibitive levels; Temenos reported in its Q1 2025 earnings that cross-sold mortgage module clients showed 94% renewal rates versus 71% for stand-alone mortgage platform clients. This integrated-platform advantage is compressing the addressable market for independent mortgage technology providers, particularly among community banks managing assets below USD 5 billion that are consolidating vendor relationships to reduce IT overhead.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| ICE Mortgage Technology (Encompass) | USA | Leader | Encompass LOS Platform | North America | Jan 2025: Launched Encompass AI Underwriting Suite, reducing decisioning time by 68% across 3,200 lender clients. |

| Black Knight (now ICE) | USA | Leader | Empower LOS | North America | Mar 2025: Completed full Empower-Encompass data-lake integration, enabling unified analytics across USD 2.3T in loan portfolios. |

| Blend Labs, Inc. | USA | Challenger | Blend Mortgage Suite | North America / Europe | May 2025: Partnered with HSBC UK to deploy digital mortgage origination across 14.6 million HSBC retail customers. |

| Roostify (acquired by JPMorgan) | USA | Challenger | Chase Digital Mortgage | North America | Nov 2024: JPMorgan extended Roostify-powered digital mortgage to all 5,100 Chase branch locations nationwide. |

| Finastra | UK | Challenger | Mortgagebot / Fusion Mortgageserv | Europe / North America | Feb 2025: Integrated Microsoft Azure OpenAI into Fusion Mortgageserv for automated income and asset verification. |

| Temenos AG | Switzerland | Niche Player | Temenos Mortgage Origination | Europe / Asia Pacific | Apr 2025: Deployed digital mortgage platform across 9 APAC banks under a SaaS model, adding USD 38M ARR. |

| Ellie Mae (now ICE) | USA | Niche Player | Encompass Consumer Connect | North America | Jun 2025: Consumer Connect processed its 2-millionth digital mortgage application, with 43% completed via mobile. |

| Wipro Holmes (Wipro Ltd.) | India | Niche Player | Wipro Digital Mortgage Platform | Asia Pacific / MEA | Aug 2025: Secured three Gulf-region bank contracts totalling USD 120M to deploy end-to-end digital mortgage processing. |

By Component:

Loan origination system (LOS) software dominated the component segment of the digital mortgage platform market in 2025, capturing 44.6% of total revenue at USD 2.60 billion. Its leadership is causally explained by the structural role of the LOS in GSE compliance: Fannie Mae's Desktop Underwriter (DU) and Freddie Mac's Loan Product Advisor (LPA) — the automated underwriting systems that determine loan salability — interface exclusively with certified LOS platforms, making LOS adoption a binary compliance requirement rather than a discretionary investment for the approximately 4,800 lenders with GSE seller-servicer agreements. ICE Mortgage Technology's Encompass holds an estimated 39% LOS market share among Fannie Mae-approved sellers, creating a network-effect moat that reinforces through each new lender integration connecting to ICE's data ecosystem.

Point-of-sale (POS) and borrower portal software accounted for 21.8% of component revenue (USD 1.27 billion, 2025), with a growth rate of 22.3% outpacing the overall market average. The specific catalyst accelerating POS adoption above the market baseline is the Mortgage Bankers Association's 2024 consumer survey finding that 67% of millennial and Gen Z homebuyers ranked digital application experience as the primary factor in lender selection — ahead of interest rate (cited by 54%) for first-time purchase loans. Lenders deploying Blend's consumer-facing POS reported 31% higher application completion rates and 22% lower cost-to-close compared to branch-initiated paper applications, a data point that compressed enterprise ROI justification timelines from 18 months to under 8 months for mid-size lenders. The non-obvious competitive dynamic in this sub-segment is the emerging role of real estate platform operators: Zillow, Redfin, and Opendoor are building embedded mortgage POS experiences that capture borrower intent at property search, potentially disintermediating traditional lender-owned POS platforms for first-time buyers who complete their lender selection within the home search workflow.

Mortgage servicing software held 18.9% share (USD 1.10 billion, 2025). The CFPB's December 2024 mortgage servicing reform — expanding loss mitigation option requirements and mandating digital loss mitigation application portals for all federally related mortgages — created a direct regulatory demand signal for servicing platform upgrades, estimated to generate USD 340 million in near-term software procurement through 2026. Implementation and integration services contributed 9.6% (USD 561 million), reflecting the complexity of migrating loan data between legacy mainframe-based systems and modern cloud platforms; the average enterprise LOS migration at a top-50 lender involves 18–24 months of implementation and USD 4–8 million in professional services fees. Managed services and support accounted for the remaining 5.1%, growing at 19.7% as community lenders with limited IT staff increasingly outsource platform management to vendor-operated hosted environments.

By Deployment:

Cloud-native SaaS deployment captured 52.4% of the digital mortgage platform market in 2025 (USD 3.06 billion), a share that increased from 38.2% in 2022 as the Federal Housing Administration's April 2024 authorization of cloud-hosted FHA Connection data interfaces removed the final government-program barrier to SaaS adoption. Cloud deployment's causal advantage is economic: lenders on cloud-native platforms report 31–44% lower total cost of ownership over five years compared to on-premise deployments, driven by elimination of server capital expenditure, automated compliance update delivery, and elastic scaling during refinance boom cycles without hardware investment. Blend Labs, which operates exclusively on a cloud-native architecture, demonstrated this elasticity during the Q1 2025 application surge — processing a 340% week-over-week volume increase without SLA degradation.

Hybrid cloud/on-premise deployment retained 34.7% share (USD 2.03 billion, 2025), primarily among Tier-1 bank lenders whose core banking data governance frameworks require on-premise retention of certain loan data categories, even as they deploy cloud-native origination interfaces. Fully on-premise deployment contracted to 12.9% (USD 753 million), concentrated among government-sponsored lenders with FedRAMP compliance requirements and a small group of large lenders with legacy mainframe dependencies that will require decade-long migration timelines. The on-premise segment's CAGR of 4.2% over the forecast period is the lowest within the deployment category — a structural decline driven by vendor end-of-life announcements (ICE has published sunset timelines for its on-premise Encompass 2.x product line through 2027) rather than active market contraction.

By Application:

Mortgage origination and underwriting applications commanded 51.3% of application revenue (USD 2.99 billion, 2025). The specific reason this application category leads is the GSE mandate structure: MISMO XML data standards and automated AUS submission requirements apply exclusively to origination workflows, creating a non-negotiable technology investment floor. Lenders cannot sell conforming loans to Fannie Mae or Freddie Mac without passing through a MISMO-compliant LOS that generates a standardized 3.x data file — a technical requirement that affects approximately 70% of all U.S. mortgage origination volume and has no analog in commercial real estate or consumer lending segments.

Mortgage servicing and collections held 24.6% share (USD 1.44 billion, 2025), with notable acceleration driven by CFPB servicing reform mandates described in the component section above. Compliance and regulatory reporting captured 14.8% (USD 864 million), its growth rate of 21.4% reflecting the cumulative compliance burden from Home Mortgage Disclosure Act (HMDA) modernization, Community Reinvestment Act (CRA) final rule (effective January 2026), and New York's 2025 Mortgage Servicing Rights Transparency Act — each requiring dedicated software modules with audit-trail capabilities. Analytics, pricing, and rate management accounted for 9.3% of application revenue but carried the highest revenue-per-user metric, as AI-powered pricing engines demonstrate directly attributable basis-point improvement in secondary market execution that justifies premium licensing fees.

By End-User:

Banks and credit unions constituted 42.7% of end-user revenue (USD 2.49 billion, 2025). Their leading position reflects the depth of regulatory requirements governing bank-originated mortgages: HMDA reporting, CRA credit, TILA-RESPA Integrated Disclosure (TRID) compliance, and BSA/AML screening collectively mandate a level of workflow documentation that only enterprise-grade digital platforms can sustain at volume. JPMorgan Chase's proprietary Roostify-powered mortgage platform — now processing 100% of Chase's consumer mortgage applications digitally — exemplifies how Tier-1 banks treat digital mortgage infrastructure as a competitive asset requiring ongoing investment rather than a commodity purchase.

Mortgage companies and non-bank lenders held 33.4% share (USD 1.95 billion, 2025). Non-bank lenders, who originated 66% of all U.S. mortgages in 2024 according to HMDA aggregate data, operate on thinner capital bases that amplify the efficiency argument for digital platforms: a USD 1,000 reduction in per-loan cost-to-close on a 10,000-loan annual portfolio delivers USD 10 million in operating income improvement — a figure that justifies platform investment at origination volumes accessible to regional non-bank lenders. Government and agency lenders (FHA/VA/GSE-dedicated originators) accounted for 14.8%, with their digital adoption accelerating after the VA's November 2024 launch of a fully digital VA loan application portal. Mortgage brokers and independent advisors held the remaining 9.1%, a segment underserved by enterprise-grade platforms and largely dependent on white-labeled point-of-sale tools offered through wholesale lender technology programs.

Regional Analysis

North America:

Anchored by the GSE secondary-market infrastructure that requires MISMO-compliant digital origination data from all 4,800+ Fannie Mae and Freddie Mac approved sellers, North America's digital mortgage platform market captured 41.2% of global revenue at USD 2.41 billion in 2025 — a position maintained not by voluntary technology adoption but by compliance mandates that create a structural technology investment floor absent in other regions. The United States accounts for 91% of the North American figure, with California-based non-bank lenders (United Wholesale Mortgage, loanDepot, PennyMac Financial), concentrated in the Pontiac-Detroit corridor and Southern California, representing the single largest geographic cluster of digital platform procurement activity. Canada contributes meaningfully through the Office of the Superintendent of Financial Institutions' (OSFI) B-20 mortgage stress-test requirements, which have driven Toronto's Big Five banks to invest in AI-based affordability assessment tools that integrate with digital origination platforms. Mexico's nascent formal mortgage market, supported by Sociedad Hipotecaria Federal programs, is digitizing at the POS layer primarily through Mexico City-based fintech lenders, generating early-stage platform procurement with a projected CAGR of 24.1% through 2034.

Europe:

Regulatory mandates under the EU Mortgage Credit Directive (MCD) II — currently in consultation phase as of Q2 2025, proposing standardized digital affordability assessments across all 27 EU member states — are reshaping procurement patterns across the European digital mortgage platform market, which held 27.6% share worth USD 1.61 billion in 2025. The UK leads European adoption, where the Financial Conduct Authority's January 2025 Consumer Duty final guidance on mortgage advice standards mandated documented digital audit trails for all advised mortgage sales, triggering a wave of platform upgrades across Barclays, Lloyds Banking Group, and the 180+ building societies operating in the UK retail mortgage market. Germany's Pfandbrief-backed covered bond system and the strict land registry (Grundbuch) requirements historically impeded digital mortgage processing, but the 2024 Digital Notarization Act (Digitales-Notargesetz) enabling remote notarization of mortgage deeds unlocked a procurement cycle estimated at EUR 180 million in 2025 alone. The Netherlands, with Amsterdam-based ING and Rabobank both piloting AI-underwriting systems across their Rotterdam and Amsterdam mortgage centers, contributes disproportionately to European AI-platform adoption relative to its mortgage market size — driven by ING's group-wide "digital-first" lending mandate implemented in Q4 2024.

Asia Pacific:

Manufacturing-economy housing demand across Shenzhen, Guangzhou, and emerging secondary cities in China's Yangtze River Delta, combined with Australia's APRA-mandated serviceability buffer reviews that pushed the country's four major banks toward AI-assisted income verification, propelled the Asia Pacific digital mortgage platform market to 18.9% global share, valued at USD 1.10 billion in 2025. Australia is the region's most mature digital mortgage market, where Commonwealth Bank's CommBank digital home loan platform and ANZ's Plus home loan (Australia's first fully digital mortgage product, launched 2022 and scaled through 2025) demonstrate that complete end-to-end digital origination is operationally viable in a regulatory environment requiring detailed responsible lending documentation. Japan's Financial Services Agency's March 2025 guidance endorsing AI-based income verification for housing loans at Tier-1 banks triggered procurement activity at MUFG, Mizuho Financial Group, and Sumitomo Mitsui — three lenders that collectively process over 30% of Japan's annual mortgage origination volume. India's National Housing Bank's priority-sector lending targets and the government's PM Awas Yojana housing program, combined with Bengaluru-based fintech lenders (LoanTap, Navi Technologies), are building digital mortgage origination infrastructure targeting the 18-million-unit affordable housing backlog, creating a greenfield addressable market for cloud-native platform vendors without legacy incumbent displacement challenges.

Latin America:

Formal mortgage market penetration below 10% of GDP across most Latin American economies both constrains near-term digital platform revenue and identifies the region as carrying the highest long-run growth optionality within the 2025–2034 forecast horizon. Latin America's digital mortgage platform market reached USD 382 million (6.5% global share) in 2025, primarily concentrated in Sao Paulo and Rio de Janeiro where Brazil's Caixa Economica Federal — the country's largest mortgage lender — deployed a fully digital origination platform in 2024 handling BRL 280 billion in annual portfolio activity. Brazil's digital mortgage adoption is driven partly by regulatory architecture: the Banco Central do Brasil's open finance framework (implemented 2022–2024) enables instant income and asset data sharing that reduces manual document collection from 12–15 items to 3–4 verified digital records, compressing application time from 15 days to under 48 hours at lenders with integrated platform deployments. Mexico's Infonavit and Fovissste housing finance agencies are piloting digital origination for their combined 40-million-member beneficiary base, a project that, if fully deployed, would represent the single largest digital mortgage platform implementation in the region by annual loan count. Colombia's Fogafin deposit guarantee framework expansion to include digital-only mortgage lenders in 2025 created a regulatory opening for Bogota-based fintech lenders to compete with traditional banks on digital origination experience.

Middle East & Africa:

Saudi Arabia's Vision 2030 residential construction pipeline — targeting 1.5 million new housing units by 2030 under the National Housing Company's accelerated delivery program — and the UAE's Golden Visa-driven luxury residential demand in Dubai's Palm Jumeirah and Downtown districts created the MEA digital mortgage platform market's dual growth engine, lifting the region to USD 350 million (6.0% global share) in 2025. The UAE leads regional digital platform adoption through the Abu Dhabi Global Market's (ADGM) FinTech regulatory sandbox, which licensed four digital mortgage platform pilots in 2024, and Dubai's Real Estate Regulatory Agency (RERA) digital title deed system, which since 2023 enables fully electronic property transfer without physical registry visits — a technical prerequisite for end-to-end digital mortgage processing. Saudi Arabia's Al Rajhi Bank deployed an AI-powered mortgage origination system across its 600-branch network in Q2 2025, reducing mortgage approval times from 21 days to 4 days and generating a reported 34% application volume increase as customer friction decreased. South Africa's National Credit Act digital amendment (2024) permitting electronic mortgage bond registration through the Deeds Office's online portal opened the largest Sub-Saharan digital mortgage market, with Johannesburg-headquartered Standard Bank and Nedbank both announcing platform modernization investments totaling ZAR 2.4 billion through 2027.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software

- Loan Origination System / LOS

- Point-of-Sale & Borrower Portal

- Servicing & Secondary Market

- Services

- Implementation & Integration

- Managed Services & Support

By Deployment

- Cloud-Native SaaS

- Hybrid Cloud / On-Premise

- Fully On-Premise

By Application

- Mortgage Origination & Underwriting

- Mortgage Servicing & Collections

- Compliance & Regulatory Reporting

- Analytics, Pricing & Rate Management

By End-User

- Banks & Credit Unions

- Mortgage Companies & Non-Bank Lenders

- Government & Agency Lenders (FHA/VA/GSE)

- Mortgage Brokers & Independent Advisors

By Enterprise Size

- Large Enterprises (Top-Tier Lenders)

- Small & Mid-Size Lenders (Community Banks, Credit Unions)

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.84 B |

| Forecast Revenue (2034) | USD 24.67 B |

| CAGR (2025-2034) | 17.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software, Services ), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, Fully On-Premise), By Application, (Mortgage Origination & Underwriting, Mortgage Servicing & Collections, Compliance & Regulatory Reporting, Analytics, Pricing & Rate Management), By End-User, (Banks & Credit Unions, Mortgage Companies & Non-Bank Lenders, Government & Agency Lenders (FHA/VA/GSE), Mortgage Brokers & Independent Advisors), By Enterprise Size, (Large Enterprises (Top-Tier Lenders), Small & Mid-Size Lenders (Community Banks, Credit Unions)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ICE MORTGAGE TECHNOLOGY (INTERCONTINENTAL EXCHANGE, INC.), BLEND LABS, INC., FINASTRA, TEMENOS AG, ROOSTIFY (JPMORGAN CHASE & CO.), ELLIE MAE (ICE MORTGAGE TECHNOLOGY), WIPRO LIMITED (DIGITAL MORTGAGE PLATFORM), NCINО, INC., SALESFORCE (FINANCIAL SERVICES CLOUD — MORTGAGE), BYTE SOFTWARE (A FINANCE OF AMERICA COMPANY), CALYX SOFTWARE, FILINK (FINICITY — MASTERCARD), FIGURE TECHNOLOGIES, INC., POLLY, INC., TOTAL EXPERT, INC., MAXWELL FINANCIAL LABS, INC., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-Native SaaS, Hybrid Cloud, On-Premise), By Application (Mortgage Origination, Servicing, Compliance Reporting, Analytics & Pricing), By End-User, Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Native SaaS, Hybrid Cloud, On-Premise), By Application (Mortgage Origination, Servicing, Compliance Reporting, Analytics & Pricing), By End-User, Industry Trends & Forecast 2026-2034")

, By Deployment (Cloud-Native SaaS, Hybrid Cloud, On-Premise), By Application (Mortgage Origination, Servicing, Compliance Reporting, Analytics & Pricing), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Digital Mortgage Platform Market?

The Global Digital Mortgage Platform Market was valued at USD 4.97 Billion in 2024 and is projected to reach USD 24.67 Billion by 2034, growing at a CAGR of 17.4% from 2026 to 2034, driven by rising adoption of AI-powered mortgage automation, cloud-based lending platforms, digital loan origination systems, e-signature technologies, and increasing digital transformation across banking, fintech, and real estate financing industri

Who are the major players in the Digital Mortgage Platform Market?

ICE MORTGAGE TECHNOLOGY (INTERCONTINENTAL EXCHANGE, INC.), BLEND LABS, INC., FINASTRA, TEMENOS AG, ROOSTIFY (JPMORGAN CHASE & CO.), ELLIE MAE (ICE MORTGAGE TECHNOLOGY), WIPRO LIMITED (DIGITAL MORTGAGE PLATFORM), NCINО, INC., SALESFORCE (FINANCIAL SERVICES CLOUD — MORTGAGE), BYTE SOFTWARE (A FINANCE OF AMERICA COMPANY), CALYX SOFTWARE, FILINK (FINICITY — MASTERCARD), FIGURE TECHNOLOGIES, INC., POLLY, INC., TOTAL EXPERT, INC., MAXWELL FINANCIAL LABS, INC., OTHERS

Which segments covered the Digital Mortgage Platform Market?

By Component, (Software, Services ), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, Fully On-Premise), By Application, (Mortgage Origination & Underwriting, Mortgage Servicing & Collections, Compliance & Regulatory Reporting, Analytics, Pricing & Rate Management), By End-User, (Banks & Credit Unions, Mortgage Companies & Non-Bank Lenders, Government & Agency Lenders (FHA/VA/GSE), Mortgage Brokers & Independent Advisors), By Enterprise Size, (Large Enterprises (Top-Tier Lenders), Small & Mid-Size Lenders (Community Banks, Credit Unions))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Digital Mortgage Platform Market

Published Date : 26 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date