- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Digital Oilfield Solutions Market Size, Share & Growth | CAGR 11.4%

Global Digital Oilfield Solutions Market Size, Share, Analysis By Component (Software, Services, Hardware), By Technology (IIoT, AI & ML, Cloud Computing, Big Data & Advanced Analytics, Digital Twin & Augmented Reality), By Application (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health Safety & Environment Monitoring), By Deployment Mode, By End-User (Upstream Operators, Oilfield Service Companies, Midstream Operators, Downstream Refining & Petrochemical Firms) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 28.6 Billion, 2025 | USD 76.4 Billion, 2034 | 11.4%, 2026–2034 | North America, 36.8%, 2025 |

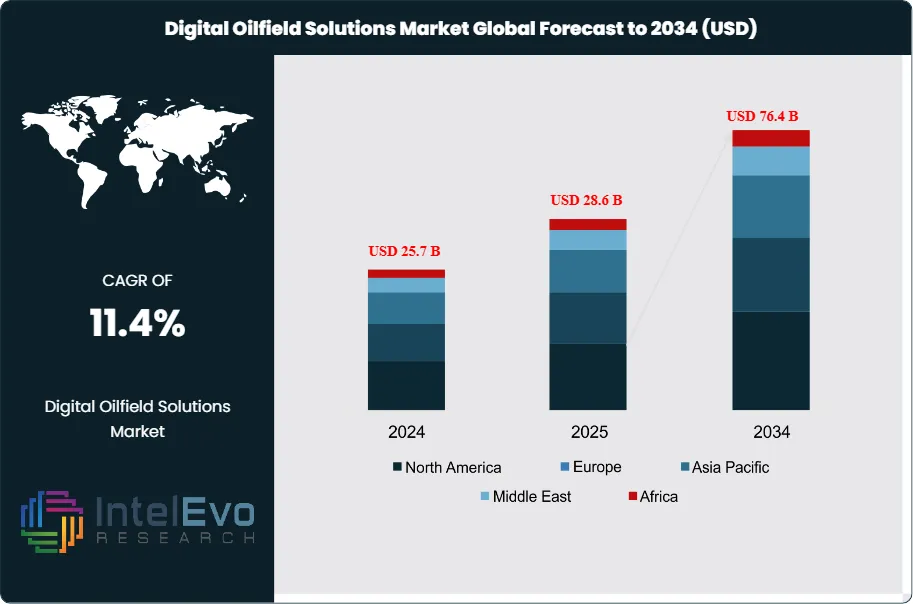

The Digital Oilfield Solutions Market was valued at approximately USD 25.7 Billion in 2024 and increased to USD 28.6 Billion in 2025. The market is projected to reach nearly USD 76.4 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 11.4% during the forecast period from 2026 to 2034. The digital oilfield solutions market is experiencing broad-based adoption across upstream, midstream, and downstream oil and gas operations as energy companies invest heavily in automation, real-time data analytics, and integrated production management platforms to reduce operational costs and improve hydrocarbon recovery efficiency. The convergence of industrial Internet of Things sensors, cloud computing infrastructure, and advanced analytics is transforming how operators monitor and manage oilfield assets across exploration, drilling, production, and reservoir management workflows.

Get More Information about this report -

Request Free Sample ReportDemand forces driving the digital oilfield solutions market include the persistent pressure to reduce lifting costs per barrel, the aging of producing assets that require enhanced surveillance to sustain output, and the industry-wide push toward carbon intensity reduction through operational efficiency gains. Supply-side dynamics reflect increasing competition among oilfield services majors, enterprise software vendors, and specialized technology firms entering the upstream market with purpose-built analytics platforms. The digital oilfield solutions market benefits from the declining cost of cloud computing and sensor hardware, which is making comprehensive digital field programs economically viable for mid-sized and independent operators previously unable to afford enterprise-grade solutions.

Regulatory influences are shaping the digital oilfield solutions market in multiple dimensions. The U.S. Environmental Protection Agency's methane monitoring mandates require continuous sensor-based emissions tracking across producing assets, accelerating the deployment of IoT sensor networks and real-time data platforms. The European Union's energy transition policies are incentivizing operators to demonstrate emissions performance through digital monitoring, while the International Energy Agency's net-zero pathway recommendations have pushed national oil companies to accelerate digital investment as a mechanism for operational decarbonization. These regulatory tailwinds are creating additional demand pull beyond pure productivity motivations.

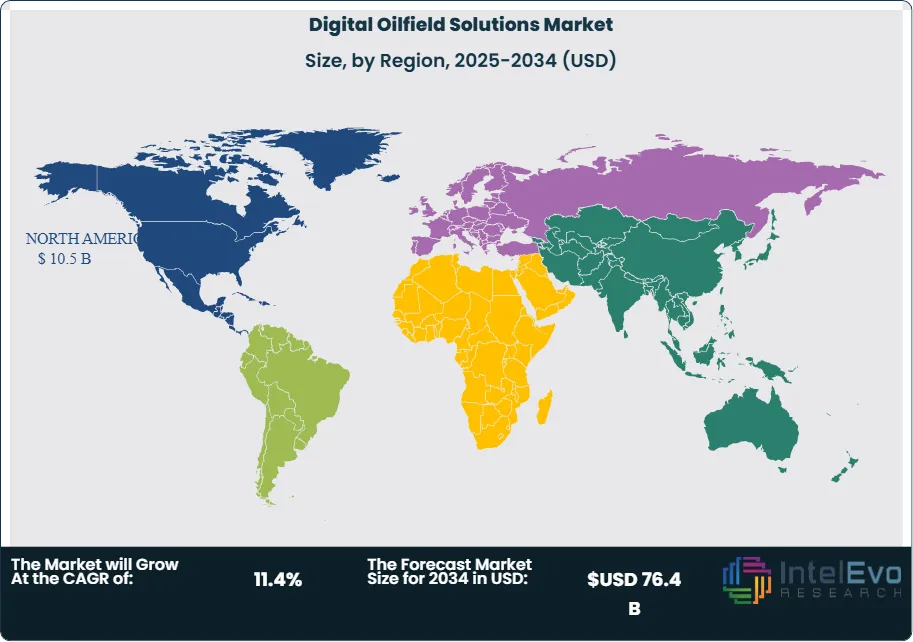

Risk factors include cybersecurity threats associated with connected operational technology environments, the complexity of integrating digital platforms across fragmented legacy information technology systems, and the shortage of petroleum engineers and data scientists who can bridge domain knowledge and digital capabilities. The digital oilfield solutions market is also affected by oil price volatility, which influences capital expenditure budgets and the pace of technology adoption among price-sensitive independent operators. Despite these constraints, North America commands approximately 36.8% of global digital oilfield solutions market revenue in 2025 at USD 10.5 Billion, driven by shale basin digitalization programs. Asia Pacific is the fastest-growing regional market, expanding at approximately 13.2% CAGR through 2034 as national oil companies in China, India, and Southeast Asia accelerate digital transformation investments. By 2034, digital oilfield platforms are projected to underpin the majority of production optimization and reservoir management decisions across global upstream operations, making the digital oilfield solutions market one of the most strategically significant technology segments in the energy sector.

, By Technology (IIoT, AI & ML, Cloud Computing, Big Data & Advanced Analytics, Digital Twin & Augmented Reality), By Application (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health Safety & Environment Monitoring), By Deployment Mode, By End-User (Upstream Operators, Oilfield Service Companies, Midstream Operators, Downstream Refining & Petrochemical Firms) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global digital oilfield solutions market was valued at USD 28.6 Billion in 2025 and is projected to reach USD 76.4 Billion by 2034, registering a CAGR of 11.4% during the forecast period 2026–2034, supported by rising upstream digitalization investment and expanding cloud-native platform adoption.

- Segment Dominance (By Component): The software segment leads the digital oilfield solutions market with a 52.1% share in 2025, equivalent to USD 14.9 Billion, driven by demand for integrated production management platforms, reservoir simulation tools, and real-time field data analytics suites.

- Segment Dominance (By Application): Production optimization is the dominant application segment, commanding 34.2% of digital oilfield solutions market revenue in 2025 at USD 9.8 Billion, as operators prioritize AI-driven production surveillance and automated lift management to maximize recovery from existing wells.

- Driver: The accelerating deployment of industrial IoT sensor networks across producing assets, with global oilfield sensor installations growing at 19.6% annually in 2025, is compelling operators to invest in digital platforms capable of ingesting, processing, and acting on continuous real-time field data streams.

- Restraint: Cybersecurity vulnerabilities in connected operational technology environments constrain adoption, with 38% of upstream operators citing OT security risk as the primary barrier to full-scale digital oilfield deployment. Remediation programs add USD 3–12 Million per operator to total implementation costs.

- Opportunity: Integrated digital twin platforms for full-field reservoir and surface facility modeling represent a USD 9.2 Billion addressable opportunity within the digital oilfield solutions market by 2034. Current penetration covers less than 11% of technically viable field development programs globally as of 2025.

- Trend: Cloud-native digital oilfield platform adoption is growing at 28.3% annually in 2025, replacing on-premise SCADA and historian systems as operators migrate production data management to scalable cloud environments with built-in AI analytics and multi-site collaboration capabilities.

- Regional Analysis: North America leads the global digital oilfield solutions market with a 36.8% share in 2025, equivalent to USD 10.5 Billion, anchored by extensive shale basin digitalization programs, mature cloud infrastructure, and a dense ecosystem of oilfield technology vendors concentrated in Texas and Colorado.

Competitive Landscape

The Digital Oilfield Solutions Market is moderately consolidated, with the top four companies accounting for an estimated 38.0% of global market revenue in 2025. Competition is largely technology-driven, focusing on cloud-based analytics platforms, AI-powered reservoir modeling, digital twins, and integrated production optimization systems rather than purely hardware deployments. Major oilfield service providers and technology firms are strengthening partnerships with operators to deliver end-to-end digital field management solutions. Competitive intensity increased in 2025–2026 as operators accelerated digital transformation programs to improve operational efficiency, reduce downtime, and enhance reservoir recovery using real-time data analytics and automation.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| SLB | US | Leader | DELFI cognitive E&P environment and digital oilfield platforms | North America, Middle East, global offshore | Expanded DELFI cloud platform capabilities and AI reservoir analytics partnerships with major Middle East operators in 2025. |

| HALLIBURTON | US | Leader | DecisionSpace 365 digital subsurface and drilling optimization platform | North America, Latin America, Middle East | Expanded collaboration with Microsoft Azure to scale cloud-based digital oilfield analytics in 2025. |

| BAKER HUGHES | US | Leader | Leucipa automated field production optimization platform | North America, Middle East, Europe | Expanded AI-enabled production optimization programs with ADNOC and other Middle East operators in 2025. |

| WEATHERFORD | US | Leader | ForeSite production optimization and digital well monitoring platform | North America, Middle East, Latin America | Expanded ForeSite Edge remote monitoring deployments across Middle East production assets in 2025. |

| IBM | US | Challenger | AI-driven predictive maintenance and analytics solutions for energy assets | North America, Europe, global enterprise | Expanded hybrid cloud and AI collaboration programs with energy majors for digital operations platforms in 2025. |

| MICROSOFT | US | Challenger | Azure cloud infrastructure and AI-based digital twin solutions | Global enterprise markets | Strengthened Azure energy partnerships with oilfield service providers and operators in 2025. |

| AMAZON WEB SERVICES | US | Challenger | AWS energy data platform and digital oilfield analytics services | North America, Europe, Asia-Pacific | Expanded energy-focused data lake and analytics services supporting upstream digitalization programs in 2025. |

| PALANTIR TECHNOLOGIES | US | Niche Player | Foundry platform for operational data integration and AI analytics | North America, Europe | Expanded energy sector deployments for production analytics and decision support systems in 2025. |

| NVIDIA | US | Niche Player | GPU-accelerated AI computing for seismic processing and reservoir modeling | Global technology markets | Expanded AI infrastructure partnerships with energy companies for high-performance seismic interpretation in 2025. |

| EMERSON ELECTRIC | US | Niche Player | Automation, digital control systems, and asset performance management | North America, Middle East, Asia-Pacific | Expanded industrial automation and digital field monitoring systems for upstream operators in 2025. |

Segmentation Analysis

The digital oilfield solutions market segmentation analysis covers five key dimensions: By Component, By Technology, By Application, By Deployment Mode, and By End-User. Each dimension reveals distinct adoption dynamics, revenue concentrations, and competitive structures that define the market through 2034.

By Component

The software segment dominates the digital oilfield solutions market by component with a 52.1% share in 2025, generating USD 14.9 Billion in annual revenue. Software encompasses integrated production management systems, reservoir simulation platforms, drilling engineering applications, real-time data historians, and analytics dashboards that aggregate and interpret operational data across the oilfield asset base. Leading vendors including SLB, Halliburton, and AspenTech have invested heavily in cloud-native software architectures that enable multi-field portfolio management from centralized operational centers, reducing the need for on-site technical staff at remote producing facilities. Subscription-based pricing models are accelerating software adoption among mid-tier operators who previously relied on legacy desktop applications. The software segment benefits from high switching costs once data pipelines and workflows are embedded in production operations, creating durable recurring revenue streams for established platform vendors.

The services segment holds a 30.4% share of the digital oilfield solutions market in 2025, valued at USD 8.7 Billion. Services encompass digital transformation consulting, system integration, data migration, managed operations services, and ongoing technical support for deployed digital oilfield platforms. Oilfield services majors leverage existing client relationships to bundle digital services with traditional well services contracts, while specialist digital consulting firms target operators seeking vendor-neutral integration expertise. The services segment is growing at above-average rates as operators move from pilot programs to enterprise-scale deployments requiring sustained implementation support. Hardware accounts for 17.5% of the market in 2025 at USD 5.0 Billion, covering IoT sensors, edge computing nodes, industrial gateways, fiber optic networks, and automated control systems deployed across wellsites and pipeline networks. Hardware demand is moderating relative to software and services as sensor costs decline and cloud platforms reduce the need for on-site processing infrastructure.

By Technology

Industrial Internet of Things technology is the foundational layer of the digital oilfield solutions market, accounting for 38.4% of technology segment revenue in 2025 at USD 11.0 Billion. IIoT platforms connect thousands of wellhead sensors, pressure gauges, flow meters, and pump controllers into unified data networks that feed real-time analytics engines. The deployment of wireless sensor networks in remote and offshore environments has been accelerated by the declining cost of low-power wide-area network infrastructure and satellite IoT connectivity services. Major operators report that IIoT sensor networks generate 15–40 terabytes of operational data per day across large producing fields, creating both the opportunity and the imperative for AI-powered analytics platforms to extract actionable insights from continuous data streams.

Artificial intelligence and machine learning technologies hold 27.6% of the digital oilfield solutions market technology segment in 2025 at USD 7.9 Billion. AI applications in the digital oilfield span production decline prediction, equipment failure forecasting, automated well test analysis, and drilling parameter optimization. Cloud computing infrastructure represents 20.8% of the technology segment at USD 5.9 Billion, providing the elastic compute resources required for large-scale production data processing and multi-site operational analytics. Big data and advanced analytics platforms contribute 13.2% at USD 3.8 Billion, encompassing data lake architectures, stream processing engines, and visualization platforms that transform raw operational data into production management intelligence. Other technologies including digital twin simulation and augmented reality field support tools account for the remaining 6.0% of the technology segment in 2025.

By Application

Production optimization is the largest application within the digital oilfield solutions market, representing 34.2% of revenue in 2025 at USD 9.8 Billion. Production optimization applications include automated artificial lift management, real-time well performance surveillance, multiphase flow metering analytics, and integrated production allocation systems. Operators deploying AI-driven production optimization platforms report average production uptime improvements of 8–14% and lifting cost reductions of 12–18% compared to conventional surveillance methods. The application is particularly critical in mature field operations where sustaining production from declining wells requires continuous monitoring and rapid intervention response to maintain economic viability.

Reservoir management applications account for 24.8% of digital oilfield solutions market revenue in 2025 at USD 7.1 Billion, encompassing real-time reservoir surveillance, dynamic model updating, and assisted history matching platforms that integrate production data with subsurface geological models. Drilling management applications hold 18.6% of revenue at USD 5.3 Billion, covering real-time wellbore monitoring, automated drilling parameter adjustment, and well planning optimization tools. Asset performance management applications contribute 13.7% at USD 3.9 Billion, addressing predictive maintenance for surface facilities, compressors, and pipeline networks. Health, safety, and environment monitoring applications represent 8.7% of the market at USD 2.5 Billion in 2025, driven by regulatory emissions monitoring requirements and operational safety surveillance programs.

By Deployment Mode

Cloud-based deployment leads the digital oilfield solutions market with a 54.6% share in 2025 at USD 15.6 Billion. Cloud deployment provides operators with centralized production data management, multi-field analytics consolidation, and real-time collaboration capabilities that are difficult to achieve with site-specific on-premise systems. Major public cloud providers including Microsoft Azure, Amazon Web Services, and Google Cloud have developed oil and gas industry-specific environments with pre-configured connectors for common oilfield SCADA and historian systems. The cloud segment is experiencing the fastest growth within the deployment dimension as operators migrate legacy production data management systems to cloud-native environments with integrated AI analytics.

On-premise deployment retains a 31.2% share in 2025 at USD 8.9 Billion, supported by data sovereignty requirements, real-time control system latency constraints, and cybersecurity policies at national oil companies that restrict transmission of operational data to external cloud environments. Hybrid deployment, combining on-premise edge processing with cloud-based analytics and reporting, accounts for 14.2% of the market at USD 4.1 Billion in 2025 and is the fastest-growing deployment mode as operators seek to balance real-time control requirements with cloud-scale analytics capabilities. The hybrid model is particularly prevalent in offshore platform operations where satellite bandwidth constraints require local data preprocessing before cloud transmission.

By End-User

Upstream oil and gas operators constitute the largest end-user segment of the digital oilfield solutions market, accounting for 62.4% of revenue in 2025 at USD 17.8 Billion. This category spans international oil companies, national oil companies, and independent operators who deploy digital oilfield solutions across exploration, drilling, and production operations. International oil companies lead investment within this group, with entities including ExxonMobil, Shell, BP, TotalEnergies, and Chevron committing multi-billion-dollar digital transformation programs that encompass IoT infrastructure, cloud platforms, and AI analytics across global asset portfolios. Oilfield services companies represent 22.8% of market revenue at USD 6.5 Billion in 2025, embedding digital oilfield solutions within their service delivery models to improve performance guarantees and create data-driven service differentiation.

Midstream operators account for 9.6% of the digital oilfield solutions market in 2025 at USD 2.7 Billion, applying digital pipeline monitoring, leak detection, and throughput optimization platforms across transmission and gathering networks. Downstream refining and petrochemical operators represent the remaining 5.2% at USD 1.5 Billion in 2025, primarily utilizing digital oilfield platform technologies adapted for process optimization, energy management, and predictive maintenance within refinery environments. The downstream segment presents a growing opportunity as refinery operators adopt upstream digital monitoring methodologies to manage feedstock blending optimization and energy efficiency programs.

Regional Analysis

North America Digital Oilfield Solutions Market

North America leads the global digital oilfield solutions market with a 36.8% share in 2025, equivalent to USD 10.5 Billion in revenue. The United States accounts for approximately 85% of North American revenue, driven by the extraordinary density of digital investment across Permian Basin, Eagle Ford, Bakken, and deepwater Gulf of Mexico operations. U.S. shale operators have been among the earliest and most committed adopters of digital oilfield platforms, using production optimization and automated surveillance tools to maintain economic well performance across dense multi-well pad operations. The U.S. market benefits from a mature technology vendor ecosystem, with Houston and Denver serving as primary development centers for oilfield-specific digital solutions. Regulatory drivers including EPA methane monitoring requirements have added a compliance dimension to digital oilfield investment that accelerates deployment timelines beyond purely economic justifications.

Canada contributes approximately 11% of North American digital oilfield solutions market revenue in 2025, with adoption concentrated in Alberta's oil sands operations where process automation and energy management platforms deliver significant operating cost reductions. Mexico's Pemex is accelerating digital investment to arrest production decline across onshore and shallow-water fields, creating opportunities for digital oilfield platform vendors in the Mexican market. The United States Department of Energy's smart oilfield research programs provide institutional support for emerging digital technologies. North America is projected to maintain regional market leadership through 2034, growing at a CAGR of approximately 10.6%, supported by continued shale optimization programs and deepwater asset digitalization initiatives.

Europe Digital Oilfield Solutions Market

Europe holds a 22.4% share of the global digital oilfield solutions market in 2025, generating USD 6.4 Billion in revenue. The United Kingdom leads the European segment, with North Sea operators deploying comprehensive digital oilfield platforms to extend field life and maximize recovery from mature assets operating under sustained production decline. Equinor, Shell, and BP are the largest European digital oilfield investors, with combined annual digital investment estimated at USD 1.8 Billion in 2025 across their North Sea and Norwegian Continental Shelf portfolios. Norway is the second-largest European market, with Equinor's Integrated Operations concept representing one of the most advanced implementations of digital oilfield technology in production operations, integrating real-time reservoir data with drilling and topside facility management.

Germany contributes through its strong industrial automation and software development capabilities, with SAP and Siemens providing enterprise digital oilfield platform components to European operator clients. The Netherlands remains strategically relevant as Shell's global digital technology center in The Hague coordinates digital oilfield R&D programs. European regulatory requirements under the EU Emissions Trading System are incentivizing operators to deploy digital emissions monitoring and energy management platforms that reduce the carbon intensity of extraction operations. Europe is projected to grow at a CAGR of 10.2% through 2034, with digital field management becoming a regulatory compliance requirement rather than a discretionary investment for European offshore operators.

Asia Pacific Digital Oilfield Solutions Market

Asia Pacific represents the fastest-growing regional segment in the digital oilfield solutions market, holding a 24.6% share in 2025 at USD 7.0 Billion and projected to grow at a CAGR of 13.2% through 2034. China is the dominant country market, with PetroChina, SINOPEC, and CNOOC deploying large-scale digital oilfield programs across onshore Sichuan Basin, Tarim Basin, and offshore South China Sea operations. China's government-mandated digital economy strategy includes oilfield digitalization as a priority sector, channeling state investment into domestic digital oilfield platform development and deployment. PetroChina has committed to complete digitalization of its top 50 producing fields by 2027, representing one of the largest digital oilfield deployment programs globally.

India is the second-largest Asia Pacific market, with Oil and Natural Gas Corporation deploying integrated production management and reservoir surveillance platforms across its onshore and offshore producing assets. ONGC's digital transformation program, budgeted at approximately USD 650 Million over 2024–2028, includes comprehensive digital oilfield platform deployment across all major producing basins. Australia's digital oilfield solutions market is driven by LNG sector digitalization, with Woodside Energy and Santos deploying real-time subsea monitoring and topside process optimization platforms across their Carnarvon Basin LNG operations. Indonesia represents a significant growth opportunity as Pertamina accelerates digital adoption to improve recovery rates from its aging Sumatran producing fields through AI-driven production optimization programs.

Latin America Digital Oilfield Solutions Market

Latin America holds an 9.8% share of the global digital oilfield solutions market in 2025, valued at USD 2.8 Billion. Brazil dominates the regional market, accounting for approximately 58% of Latin American revenue, with Petrobras deploying comprehensive digital oilfield platforms across its massive pre-salt Santos and Campos Basin deepwater operations. Petrobras's digital oilfield investment program, valued at approximately USD 1.2 Billion over 2024–2028, focuses on real-time reservoir management, subsea equipment monitoring, and integrated production optimization across its FPSO fleet. The complexity of deepwater pre-salt operations, where subsea tiebacks span distances of 150–300 kilometers from production facilities, makes real-time digital monitoring not merely beneficial but operationally essential.

Mexico represents approximately 24% of Latin American digital oilfield solutions market revenue, with Pemex deploying production optimization and automated surveillance platforms across its Cantarell, Ku-Maloob-Zaap, and onshore Veracruz assets to arrest production decline. Colombia's Ecopetrol is investing in AI-driven enhanced oil recovery optimization for its Llanos Basin fields, deploying digital water injection management and polymer flooding surveillance platforms. Argentina's Vaca Muerta unconventional play is driving digital oilfield adoption at a pace comparable to U.S. shale plays, as operators including YPF and Tecpetrol deploy automated drilling and production management systems across dense well networks. Latin America is projected to grow at a CAGR of 12.4% through 2034.

Middle East & Africa Digital Oilfield Solutions Market

The Middle East and Africa segment accounts for 6.4% of global digital oilfield solutions market revenue in 2025, totaling USD 1.8 Billion. The United Arab Emirates leads the regional market, with ADNOC's comprehensive digital oilfield program representing the most publicly committed national oil company digital transformation initiative globally. ADNOC's Panorama Digital Command Center in Abu Dhabi integrates real-time data from over 100,000 sensors across its onshore and offshore producing assets, processing 8 terabytes of operational data daily to drive production optimization and predictive maintenance decisions. The facility serves as a reference deployment for regional digital oilfield expansion and has attracted significant interest from peer national oil companies across the Gulf Cooperation Council.

Saudi Arabia is the second-largest regional market, with Saudi Aramco's Intelligent Field program integrating digital monitoring, AI analytics, and automated control systems across its Ghawar, Shaybah, and offshore Safaniya producing fields. Saudi Aramco's annual technology and digital investment exceeded USD 2.5 Billion in 2024, with digital oilfield platforms representing a substantial portion of total digital expenditure. South Africa's PetroSA and private sector gas developers contribute to the African market, while frontier producing nations including Nigeria, Angola, and Kenya represent longer-term digital oilfield adoption opportunities as production infrastructure matures. The Middle East and Africa region is projected to grow at a CAGR of 13.8% through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software

- Services

- Hardware

By Technology

- Industrial Internet of Things (IIoT)

- Artificial Intelligence and Machine Learning

- Cloud Computing

- Big Data and Advanced Analytics

- Other Technologies (Digital Twin, Augmented Reality)

By Application

- Production Optimization

- Reservoir Management

- Drilling Management

- Asset Performance Management

- Health, Safety, and Environment Monitoring

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By End-User

- Upstream Oil and Gas Operators

- Oilfield Services Companies

- Midstream Operators

- Downstream Refining and Petrochemical Operators

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 28.6 B |

| Forecast Revenue (2034) | USD 76.4 B |

| CAGR (2025-2034) | 11.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software, Services, Hardware), By Technology, (Industrial Internet of Things (IIoT), Artificial Intelligence and Machine Learning, Cloud Computing, Big Data and Advanced Analytics, Other Technologies (Digital Twin, Augmented Reality)), By Application, (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health, Safety, and Environment Monitoring), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By End-User, (Upstream Oil and Gas Operators, Oilfield Services Companies, Midstream Operators, Downstream Refining and Petrochemical Operators) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB (SCHLUMBERGER LIMITED), HALLIBURTON COMPANY, ASPENTECH (ASPEN TECHNOLOGY), MICROSOFT CORPORATION, BAKER HUGHES COMPANY, WEATHERFORD INTERNATIONAL PLC, IBM CORPORATION, SAP SE, EMERSON ELECTRIC CO., SIEMENS AG, AMAZON WEB SERVICES INC., GOOGLE LLC (ALPHABET INC.), ROCKWELL AUTOMATION INC., HONEYWELL INTERNATIONAL INC., TOTALENERGIES SE, AVEVA GROUP PLC, C3.AI INC., PALANTIR TECHNOLOGIES INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (IIoT, AI & ML, Cloud Computing, Big Data & Advanced Analytics, Digital Twin & Augmented Reality), By Application (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health Safety & Environment Monitoring), By Deployment Mode, By End-User (Upstream Operators, Oilfield Service Companies, Midstream Operators, Downstream Refining & Petrochemical Firms) Industry Trends & Forecast 2026–2034")

, By Technology (IIoT, AI & ML, Cloud Computing, Big Data & Advanced Analytics, Digital Twin & Augmented Reality), By Application (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health Safety & Environment Monitoring), By Deployment Mode, By End-User (Upstream Operators, Oilfield Service Companies, Midstream Operators, Downstream Refining & Petrochemical Firms) Industry Trends & Forecast 2026–2034")

, By Technology (IIoT, AI & ML, Cloud Computing, Big Data & Advanced Analytics, Digital Twin & Augmented Reality), By Application (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health Safety & Environment Monitoring), By Deployment Mode, By End-User (Upstream Operators, Oilfield Service Companies, Midstream Operators, Downstream Refining & Petrochemical Firms) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Digital Oilfield Solutions Market?

The Global Digital Oilfield Solutions Market was valued at USD 25.7 Billion in 2024 and USD 28.6 Billion in 2025, projected to reach USD 76.4 Billion by 2034 at a CAGR of 11.4% from 2026–2034. Growth is driven by AI-powered analytics, digital twins, cloud-based reservoir modeling, predictive maintenance, and increasing adoption of integrated digital oilfield platforms.

Who are the major players in the Digital Oilfield Solutions Market?

SLB (SCHLUMBERGER LIMITED), HALLIBURTON COMPANY, ASPENTECH (ASPEN TECHNOLOGY), MICROSOFT CORPORATION, BAKER HUGHES COMPANY, WEATHERFORD INTERNATIONAL PLC, IBM CORPORATION, SAP SE, EMERSON ELECTRIC CO., SIEMENS AG, AMAZON WEB SERVICES INC., GOOGLE LLC (ALPHABET INC.), ROCKWELL AUTOMATION INC., HONEYWELL INTERNATIONAL INC., TOTALENERGIES SE, AVEVA GROUP PLC, C3.AI INC., PALANTIR TECHNOLOGIES INC., Others

Which segments covered the Digital Oilfield Solutions Market?

By Component, (Software, Services, Hardware), By Technology, (Industrial Internet of Things (IIoT), Artificial Intelligence and Machine Learning, Cloud Computing, Big Data and Advanced Analytics, Other Technologies (Digital Twin, Augmented Reality)), By Application, (Production Optimization, Reservoir Management, Drilling Management, Asset Performance Management, Health, Safety, and Environment Monitoring), By Deployment Mode, (Cloud-Based, On-Premise, Hybrid), By End-User, (Upstream Oil and Gas Operators, Oilfield Services Companies, Midstream Operators, Downstream Refining and Petrochemical Operators)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Digital Oilfield Solutions Market

Published Date : 13 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date