- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Digital Therapeutics Market Forecast 2034 | CAGR 15.3%

Global Digital Therapeutics Platform Market Size, Share, Growth & Industry Analysis By Offering (Software/Standalone SaMD, Platform-as-a-Service/SaaS Infrastructure, Wearable-Integrated Therapeutics), By Application (Mental Health, Cardiometabolic, MSK Rehabilitation, Respiratory, Oncology Support), By Deployment Mode (B2B2C, Prescription DTx, Direct-to-Consumer), By End-User (Hospitals, Payers, Pharma, Employers) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

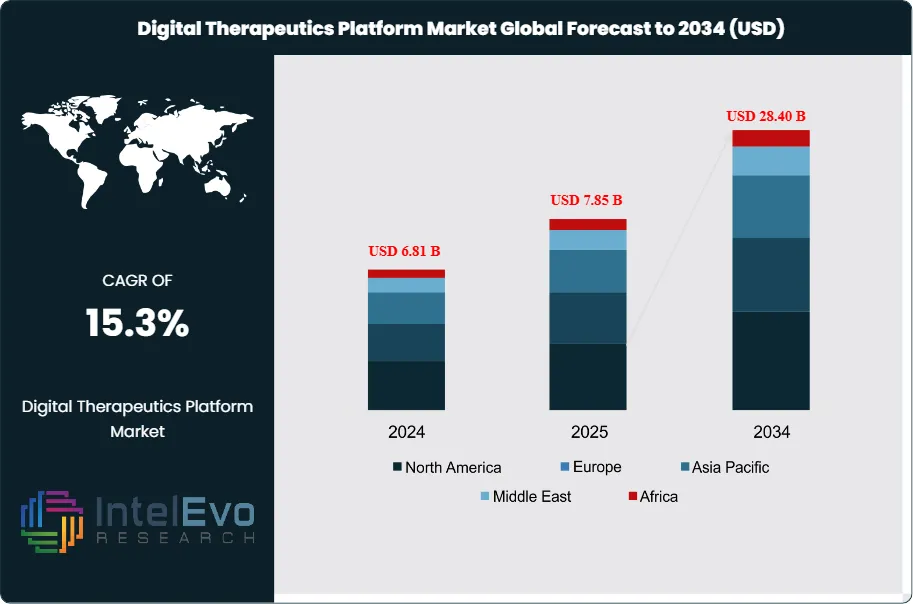

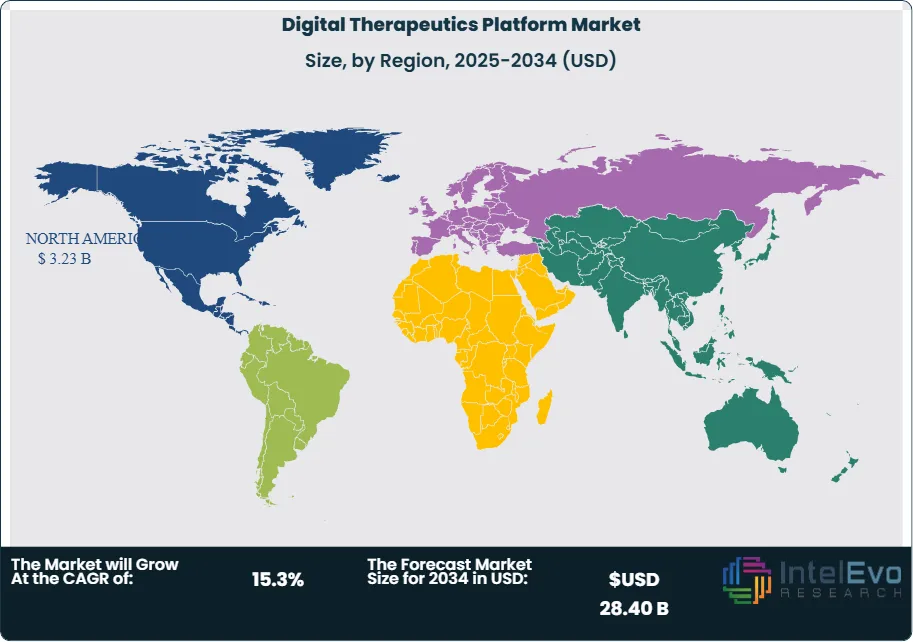

| USD 7.85 Billion | USD 28.40 Billion | 15.3% | North America, 41.2% |

The Digital Therapeutics Platform Market was valued at approximately USD 6.81 Billion in 2024 and reached USD 7.85 Billion in 2025. The market is projected to grow to USD 28.40 Billion by 2034, expanding at a CAGR of 15.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 20.55 Billion over the analysis period, reflecting intensifying clinical adoption of software-based interventions that deliver evidence-based therapeutic outcomes across a wide range of chronic and behavioral health conditions.

Get More Information about this report -

Request Free Sample ReportThe digital therapeutics platform market has entered a period of structural acceleration driven by mounting chronic disease burden, rising behavioral health demand, and the broader integration of prescription digital therapeutics (PDTs) into standard clinical pathways. Industry analysis indicates that more than 60% of adults in high-income economies live with at least one chronic condition amenable to behavioral intervention, creating a substantial addressable patient population that conventional pharmacotherapy alone cannot efficiently manage. Digital therapeutics platforms fill this gap by delivering cognitive behavioral therapy (CBT), disease self-management modules, medication adherence tracking, and real-world data generation through regulated software applications. The U.S. Food and Drug Administration (FDA) has played a defining role in shaping market structure through its De Novo and 510(k) clearance pathways for software as a medical device (SaMD), while the EU's Medical Device Regulation (EU MDR 2017/745) has similarly imposed mandatory clinical evidence requirements that have elevated quality standards and created a compliance-differentiated competitive tier.

North America held the largest share of the digital therapeutics platform market at 41.2% in 2025, supported by robust payer engagement, established FDA regulatory pathways, and concentrated enterprise health system partnerships. Asia Pacific is emerging as the fastest-growing regional market, with government-backed digital health initiatives in Japan, South Korea, and China accelerating clinical deployment. The competitive environment remains moderately fragmented, with a combination of dedicated digital therapeutics companies and large technology platforms competing for health system contracts and formulary inclusion. Supply-side investment has intensified, with venture capital deployment into digital therapeutics platform development exceeding USD 3.1 Billion in 2024 alone, according to publicly reported funding data. Reimbursement expansion represents the single most important market-enabling force: as national payers in Germany (under DIGA reimbursement), the United States (through Medicare Advantage and commercial insurers), and Japan extend coverage to FDA-cleared and MDR-compliant digital therapeutics, the total reimbursable patient base is growing at an accelerating pace through the forecast period.

, By Application (Mental Health, Cardiometabolic, MSK Rehabilitation, Respiratory, Oncology Support), By Deployment Mode (B2B2C, Prescription DTx, Direct-to-Consumer), By End-User (Hospitals, Payers, Pharma, Employers) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global Digital Therapeutics Platform Market was valued at USD 7.85 Billion in 2025 and is projected to reach USD 28.40 Billion by 2034, expanding at a CAGR of 15.3% during 2025-2034.

- Segment Dominance: The Software/Application segment led by offering type, capturing 68.4% of the digital therapeutics platform market in 2025, driven by broad SaMD deployability across iOS and Android ecosystems without hardware dependencies.

- Segment Dominance: The Mental Health and Behavioral Health application segment held the largest share at 34.7% in 2025, reflecting the structural shortage of mental health professionals and growing clinical validation for CBT-based digital interventions.

- Driver: Expanded reimbursement coverage is the primary growth driver; Germany's DIGA framework had approved 54 digital health applications by early 2025, while U.S. commercial payer coverage of PDTs grew by 28% between 2023 and 2025.

- Restraint: Low clinician awareness and engagement remain a significant constraint; survey data from healthcare provider networks indicate that fewer than 22% of primary care physicians actively prescribe or recommend digital therapeutics platforms as of 2025.

- Opportunity: Oncology-integrated digital therapeutics represent the largest near-term untapped segment, with an addressable market of USD 4.8 Billion by 2034 as cancer centers seek scalable supportive care and treatment adherence tools.

- Trend: Artificial intelligence-driven personalization is the dominant trend reshaping the digital therapeutics platform market; AI-adaptive content delivery has demonstrated 31% higher patient engagement versus static protocol apps in clinical studies through 2025.

- Regional Analysis: North America led the digital therapeutics platform market with a 41.2% share, generating USD 3.23 Billion in revenue in 2025, supported by FDA regulatory clarity, established health system procurement, and payer reimbursement infrastructure.

Competitive Landscape Overview

The Digital Therapeutics Platform Market operates in a moderately consolidated structure, with the top four players collectively accounting for approximately 38.5% of global market share in 2025. Competition is primarily technology-driven, with clinical evidence depth, FDA/MDR regulatory status, and electronic health record (EHR) integration capability serving as the principal differentiating axes. Platform interoperability, payer contract penetration, and the breadth of therapeutic indication coverage are increasingly decisive in large health system procurement decisions. M&A activity accelerated in 2024-2025, with several traditional pharmaceutical companies acquiring digital therapeutics assets to create hybrid drug-plus-software care bundles, signaling a structural shift in how the market is organized around therapeutic verticals.

Competitive Landscape Matrix

| Company Name | HQ | Position | Key Product/Solution | Geo Strength | Recent Strategic Move |

| Pear Therapeutics | USA | Leader | reSET-O (SUD PDT) | North America | Expanded SUD platform licensing to 12 additional state Medicaid programs (Q1 2025) |

| Voluntis | France | Leader | Oleena (Oncology DTx) | Europe | Signed co-development agreement with a major EU oncology network for GI cancer module (Mar 2025) |

| Noom | USA | Leader | Noom Health Platform | North America | Launched enterprise B2B2C cardiometabolic program covering 4.2 million covered lives (Feb 2025) |

| Biofourmis | USA/Singapore | Leader | Biovitals Analytics | Asia Pacific | Secured USD 100M Series D to expand AI biosignal analytics into chronic pain management (Jan 2025) |

| Big Health | UK/USA | Challenger | Sleepio (CBT-i DTx) | North America, Europe | Obtained FDA De Novo clearance for Sleepio as a prescription digital therapeutic (Dec 2024) |

| Kaia Health | Germany/USA | Challenger | Kaia MSK Platform | Europe | DIGA-listed; expanded into Japan via partnership with a national health insurer (Jun 2025) |

| DarioHealth | USA | Challenger | Dario Cardiometabolic | North America | Acquired Twill (formerly Happify Health) to add behavioral health to cardiometabolic suite (Q2 2025) |

| Sword Health | USA/Portugal | Niche Player | SWORD Phoenix (MSK AI) | North America | Launched AI-physical therapist generative tool with 6 U.S. employer health plan contracts (Apr 2025) |

| Limbix | USA | Niche Player | Limbix Spark (Adolescent DTx) | North America | Completed pediatric depression RCT with results submitted to FDA for De Novo clearance (Sep 2025) |

Segmentation Analysis

By Offering

The Software/Application segment dominated the digital therapeutics platform market with a 68.4% share in 2025, generating approximately USD 5.37 Billion in revenue. This segment encompasses standalone mobile and web-based SaMD applications that deliver structured therapeutic protocols without requiring an associated hardware device. The dominance of the software segment reflects the scalability economics of app-based delivery: marginal cost of patient onboarding approaches zero once development and regulatory clearance costs are absorbed, making software-based platforms far more attractive to payers and health systems operating under capitated or value-based contracts. Clinical evidence generation has become a core competitive activity in this segment, with leading players investing heavily in randomized controlled trial infrastructure to achieve FDA clearance and payer formulary placement. Sub-categories include standalone prescription digital therapeutics (PDTs), over-the-counter wellness applications with clinical evidence, and hybrid apps that serve as digital companions to pharmaceutical regimens.

The Platform-as-a-Service (PaaS) / Software-as-a-Service (SaaS) Infrastructure segment held a 19.8% share of the digital therapeutics platform market in 2025, valued at approximately USD 1.55 Billion. This segment addresses the needs of pharmaceutical companies, health systems, and condition management organizations seeking to rapidly develop and deploy their own digital therapeutics using pre-validated technology frameworks. PaaS providers offer regulatory-grade development environments, real-world data collection modules, patient engagement toolkits, and compliance-ready data architectures aligned with HIPAA, GDPR, and EU MDR requirements. Demand for this segment is accelerating as large pharmaceutical companies pursue digital-drug combination strategies rather than building proprietary platforms from scratch.

The Wearable-Integrated and Hardware-Enabled Therapeutics segment accounted for the remaining 11.8% of digital therapeutics platform market share in 2025, representing approximately USD 0.93 Billion. This segment involves platforms where therapeutic delivery is contingent on physiological data streams from FDA-cleared wearable biosensors, including continuous glucose monitors, ECG patches, accelerometers, and photoplethysmography-based wearables. Clinical applications span cardiac rehabilitation, neurological condition management, chronic pain modulation via biofeedback, and precision sleep intervention. The integration of continuous biosignal data enables closed-loop therapeutic adaptation, improving clinical outcomes relative to static software interventions but at higher per-patient cost.

By Application/Therapeutic Area

Mental Health and Behavioral Health applications held the largest share of the digital therapeutics platform market at 34.7% in 2025, generating approximately USD 2.72 Billion in revenue. This dominance reflects the acute global mental health workforce shortage: the World Health Organization (WHO) estimates a deficit of over 1.8 million mental health professionals globally, creating demand for scalable, regulated software-based interventions. FDA-cleared and DIGA-listed CBT applications for depression, anxiety disorders, insomnia (CBT-i), and substance use disorder (SUD) have achieved meaningful clinical adoption in both direct-to-consumer and prescription channels. The integration of AI-driven natural language processing for personalized CBT delivery is improving completion rates and expanding the addressable patient population in this segment.

The Cardiometabolic and Metabolic Disease segment captured 26.3% of the digital therapeutics platform market in 2025, valued at approximately USD 2.07 Billion. This segment addresses type 2 diabetes prevention and management, hypertension, obesity, and dyslipidemia through structured lifestyle intervention platforms, medication adherence tools, and connected monitoring integrations. The American Diabetes Association (ADA) has incorporated evidence-based digital intervention pathways into its standards of care, providing clinical legitimacy that has accelerated payer coverage expansion. Programs validated under the National Diabetes Prevention Program (NDPP) framework have achieved broad reimbursement in U.S. Medicare, creating a template for commercial payer adoption.

The Musculoskeletal (MSK) and Physical Rehabilitation segment held 18.4% of digital therapeutics platform market share in 2025, representing approximately USD 1.44 Billion. Employer self-insured health plans have been the primary demand driver, motivated by the high cost of MSK-related disability claims and the shortage of physical therapists available for in-person care. AI-guided motion analysis via smartphone cameras, combined with personalized exercise protocol generation and remote monitoring by licensed physical therapists, defines the current state-of-the-art in this segment. Responders demonstrate 40-50% improvements in functional pain scores compared to untreated controls in employer-sponsored MSK platform trials.

Respiratory Disease, Oncology Supportive Care, and Other Therapeutic Areas collectively accounted for the remaining 20.6% of the digital therapeutics platform market in 2025. Respiratory platforms focus primarily on asthma self-management, COPD exacerbation prevention, and smoking cessation, with several FDA-cleared applications operating under payer coverage agreements. Oncology-integrated digital therapeutics represent an emerging high-value segment; platforms designed to manage chemotherapy side effects, improve treatment adherence, and support psychological well-being during cancer treatment are gaining traction as cancer centers seek scalable supportive care solutions. Other therapeutic areas including neurology, women's health, and pediatric chronic disease management are at earlier stages of clinical validation and market development.

By Deployment Mode

The Business-to-Business-to-Consumer (B2B2C) deployment mode dominated with 58.6% of digital therapeutics platform market share in 2025, generating approximately USD 4.60 Billion. Under this model, digital therapeutics are procured by health systems, employer groups, or payers and made available to their covered patient or employee populations. B2B2C deployment benefits from concentrated distribution economics: a single enterprise contract can onboard tens of thousands of eligible patients, dramatically reducing customer acquisition cost per patient relative to direct-to-consumer channels. Integration with employer health benefit administration platforms and EHR prescription workflows are key enablers of this deployment mode.

The Direct-to-Consumer (DTC) and Prescription Digital Therapeutics (PDT) segments together accounted for 41.4% of digital therapeutics platform market share in 2025. The PDT channel, where physicians prescribe FDA-cleared digital therapeutics directly to patients in a manner analogous to pharmaceutical prescriptions, is growing faster than DTC due to payer reimbursement alignment and clinical credibility. DTC wellness-positioned platforms operate in a less regulated environment but face increasing scrutiny as regulatory bodies globally move toward requiring clinical evidence for health claims.

Regional Analysis

North America

North America led the digital therapeutics platform market with a 41.2% share in 2025, generating USD 3.23 Billion in revenue. The United States drives the overwhelming majority of regional demand, supported by an established FDA regulatory framework for SaMD, active clinical adoption in large integrated delivery networks, and a growing payer reimbursement footprint. The Veterans Health Administration (VHA) has been an early institutional adopter, deploying mental health digital therapeutics across more than 170 medical centers. Commercial insurers including Cigna, Aetna, and several Blue Cross Blue Shield regional affiliates expanded digital therapeutics coverage during 2024-2025, adding approximately 28 million covered lives eligible for PDT access. Canada is emerging as a secondary growth market, with Health Canada's progressive regulatory posture on SaMD and increasing provincial payer engagement supporting adoption. Mexico presents nascent opportunity in the chronic disease management segment, though reimbursement infrastructure remains underdeveloped as of 2025.

Europe

Europe held a 28.6% share of the digital therapeutics platform market in 2025, representing approximately USD 2.25 Billion in revenue. Germany functions as the world's most advanced regulatory market for digital therapeutics through its Digitale Gesundheitsanwendungen (DIGA) fast-track approval and statutory reimbursement framework, which had approved 54 applications across mental health, cardiometabolic, and musculoskeletal indications by early 2025. France has adopted a comparable approach through its Agence Nationale de Securite du Medicament (ANSM) digital health pathway, while the UK's NHS App Library and NICE evidence framework provide a structured route to NHS commissioning. The EU's Medical Device Regulation (MDR 2017/745) applies to Class I and Class IIa SaMD, establishing a rigorous clinical evidence standard that has simultaneously raised market entry barriers and created credibility signals favoring established players. Scandinavian countries demonstrate particularly high digital health infrastructure readiness, supporting faster deployment cycles relative to Southern and Eastern European markets.

Asia Pacific

Asia Pacific captured 18.9% of the digital therapeutics platform market in 2025, generating approximately USD 1.48 Billion in revenue, and is projected to be the fastest-growing regional market through 2034. Japan has established a dedicated SaMD approval pathway through the Pharmaceuticals and Medical Devices Agency (PMDA) and has approved digital therapeutics for hypertension and nicotine dependence, with national health insurance reimbursement in place. South Korea's Ministry of Food and Drug Safety (MFDS) operates a dedicated digital therapeutic approval track, and the country's extensive 5G infrastructure supports high-fidelity remote patient monitoring integrations. China represents the largest national market in the region by addressable patient population, with the National Medical Products Administration (NMPA) progressively developing SaMD regulatory standards. India's digital health ecosystem is expanding rapidly under the Ayushman Bharat Digital Mission (ABDM) framework, though commercial digital therapeutics adoption remains concentrated in urban tier-1 markets. Australia is an established secondary market with the Therapeutic Goods Administration (TGA) providing SaMD regulatory oversight.

Latin America

Latin America represented 6.8% of the digital therapeutics platform market in 2025, generating approximately USD 0.53 Billion in revenue. Brazil is the dominant national market, driven by a large and growing chronic disease population, increasing smartphone penetration exceeding 82% among adults, and active health technology investment from ANVISA-regulated health systems. The Brazilian supplemental health system (Saude Suplementar), regulated by ANS, is beginning to incorporate digital therapeutic platforms into chronic disease management programs for covered beneficiaries. Mexico and Colombia represent secondary growth markets; Mexico's IMSS and ISSSTE public health systems are evaluating scalable digital health deployments to address diabetes and hypertension burden, which together affect more than 40 million Mexicans. Reimbursement formalization and clinical evidence requirements from regional regulatory agencies remain the primary constraint on faster adoption across Latin American markets.

Middle East and Africa

The Middle East and Africa region accounted for 4.5% of the digital therapeutics platform market in 2025, generating approximately USD 0.35 Billion in revenue. The Gulf Cooperation Council (GCC) states, particularly the United Arab Emirates and Saudi Arabia, represent the most commercially active markets in the region, driven by national digital health transformation agendas embedded in UAE Vision 2031 and Saudi Vision 2030. The UAE's Dubai Health Authority and Abu Dhabi Department of Health have each established digital health regulatory frameworks and are piloting digital therapeutics programs for diabetes and cardiovascular risk management. Saudi Arabia's Sehhaty national health platform integration creates a scalable distribution channel for digital therapeutics reaching the country's unified health record population. South Africa leads sub-Saharan African adoption, with digital therapeutics platforms targeting HIV adherence support and tuberculosis treatment completion achieving notable public health impact through NGO and government partnerships. Infrastructure limitations, variable smartphone penetration, and nascent reimbursement structures constrain broader regional market development.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software/Application (Standalone SaMD)

- Platform-as-a-Service (PaaS) / SaaS Infrastructure

- Wearable-Integrated and Hardware-Enabled Therapeutics

By Application/Therapeutic Area

- Mental Health and Behavioral Health

- Cardiometabolic and Metabolic Disease

- Musculoskeletal (MSK) and Physical Rehabilitation

- Respiratory Disease

- Oncology Supportive Care

- Other Therapeutic Areas

By Deployment Mode

- Business-to-Business-to-Consumer (B2B2C)

- Prescription Digital Therapeutics (PDT) Channel

- Direct-to-Consumer (DTC)

By End-User

- Health Systems and Hospitals

- Employer Self-Insured Plans

- Health Insurance Payers

- Pharmaceutical Companies

- Individual Consumers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.85 B |

| Forecast Revenue (2034) | USD 28.40 B |

| CAGR (2025-2034) | 15.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Software/Application (Standalone SaMD), Platform-as-a-Service (PaaS) / SaaS Infrastructure, Wearable-Integrated and Hardware-Enabled Therapeutics), By Application/Therapeutic Area, (Mental Health and Behavioral Health, Cardiometabolic and Metabolic Disease, Musculoskeletal (MSK) and Physical Rehabilitation, Respiratory Disease, Oncology Supportive Care, Other Therapeutic Areas), By Deployment Mode, (Business-to-Business-to-Consumer (B2B2C), Prescription Digital Therapeutics (PDT) Channel, Direct-to-Consumer (DTC)), By End-User, (Health Systems and Hospitals, Employer Self-Insured Plans, Health Insurance Payers, Pharmaceutical Companies, Individual Consumers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PEAR THERAPEUTICS, NOOM INC., BIOFOURMIS, BIG HEALTH, VOLUNTIS, KAIA HEALTH, DARIOHEALTH CORP., SWORD HEALTH, LIMBIX, WELLTH, VIRTA HEALTH, OMADA HEALTH, PROPELLER HEALTH (RESMED), COGNOA, FREESPIRA, CLICK THERAPEUTICS, TWILL (ACQUIRED BY DARIOHEALTH), OTSUKA DIGITAL HEALTH (ABILIFY MYCITE), MAHANA THERAPEUTICS, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Mental Health, Cardiometabolic, MSK Rehabilitation, Respiratory, Oncology Support), By Deployment Mode (B2B2C, Prescription DTx, Direct-to-Consumer), By End-User (Hospitals, Payers, Pharma, Employers) Industry Trends & Forecast 2026–2034")

, By Application (Mental Health, Cardiometabolic, MSK Rehabilitation, Respiratory, Oncology Support), By Deployment Mode (B2B2C, Prescription DTx, Direct-to-Consumer), By End-User (Hospitals, Payers, Pharma, Employers) Industry Trends & Forecast 2026–2034")

, By Application (Mental Health, Cardiometabolic, MSK Rehabilitation, Respiratory, Oncology Support), By Deployment Mode (B2B2C, Prescription DTx, Direct-to-Consumer), By End-User (Hospitals, Payers, Pharma, Employers) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Digital Therapeutics Platform Market?

Global Digital therapeutics market valued at USD 6.81B in 2024, reaching USD 28.40B by 2034, growing at a CAGR of 15.3% from 2026–2034.

Who are the major players in the Digital Therapeutics Platform Market?

PEAR THERAPEUTICS, NOOM INC., BIOFOURMIS, BIG HEALTH, VOLUNTIS, KAIA HEALTH, DARIOHEALTH CORP., SWORD HEALTH, LIMBIX, WELLTH, VIRTA HEALTH, OMADA HEALTH, PROPELLER HEALTH (RESMED), COGNOA, FREESPIRA, CLICK THERAPEUTICS, TWILL (ACQUIRED BY DARIOHEALTH), OTSUKA DIGITAL HEALTH (ABILIFY MYCITE), MAHANA THERAPEUTICS, OTHERS

Which segments covered the Digital Therapeutics Platform Market?

By Offering, (Software/Application (Standalone SaMD), Platform-as-a-Service (PaaS) / SaaS Infrastructure, Wearable-Integrated and Hardware-Enabled Therapeutics), By Application/Therapeutic Area, (Mental Health and Behavioral Health, Cardiometabolic and Metabolic Disease, Musculoskeletal (MSK) and Physical Rehabilitation, Respiratory Disease, Oncology Supportive Care, Other Therapeutic Areas), By Deployment Mode, (Business-to-Business-to-Consumer (B2B2C), Prescription Digital Therapeutics (PDT) Channel, Direct-to-Consumer (DTC)), By End-User, (Health Systems and Hospitals, Employer Self-Insured Plans, Health Insurance Payers, Pharmaceutical Companies, Individual Consumers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Digital Therapeutics Platform Market

Published Date : 16 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date