- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Future of Digital Twin Simulation Market $97.2B by 2034 | CAGR 21.5%

Global Digital Twin Market Size, Share, Analysis Report By Type (Product Digital Twin, Process Digital Twin, System Digital Twin), Technology (IoT, Artificial Intelligence, Big Data Analytics, Augmented Reality, Virtual Reality), Application (Predictive Maintenance, Product Design and Development, Performance Monitoring, Fleet Management), Industry Vertical(Manufacturing, Automotive, Aerospace and Defense, Energy and Utilities, Healthcare), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview

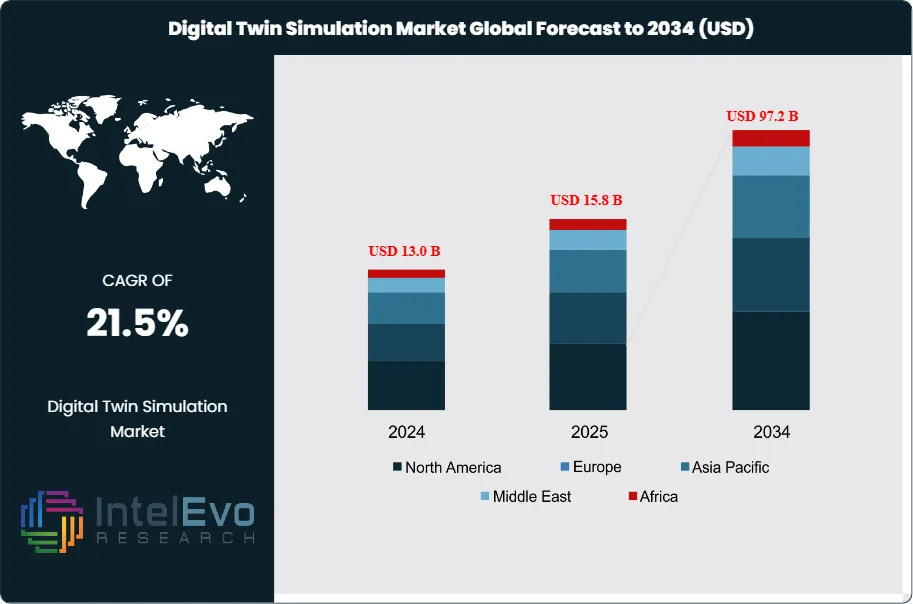

The Digital Twin Simulation Market is projected to reach approximately USD 97.2 Billion by 2034, up from USD 13.0 Billion in 2024, growing at a CAGR of 21.5% during the forecast period from 2024 to 2034. The market outlook reflects strong demand for real-time monitoring and advanced simulation capabilities. With expanding applications across industries, digital twins are set to become a critical enabler of Industry 4.0 transformation.

Get More Information about this report -

Request Free Sample ReportDigital twin simulation refers to the creation of virtual replicas of physical assets, processes, or systems, enabling real-time monitoring, predictive analytics, and scenario testing. This market encompasses software platforms, integration services, and IoT-enabled devices that collectively allow organizations to optimize operations, reduce downtime, and accelerate innovation. Digital twin simulation is widely adopted across industries such as manufacturing, automotive, energy, healthcare, aerospace, and smart cities, supporting use cases from product design and predictive maintenance to supply chain optimization and urban planning.

The market’s rapid growth is driven by the increasing adoption of Industry 4.0 practices, the proliferation of IoT sensors, and the need for data-driven decision-making. Key growth catalysts include advancements in AI and machine learning, which enhance simulation accuracy and enable autonomous optimization. The integration of cloud computing and edge analytics further accelerates deployment and scalability, while the growing complexity of industrial systems makes digital twins essential for risk mitigation and operational efficiency.

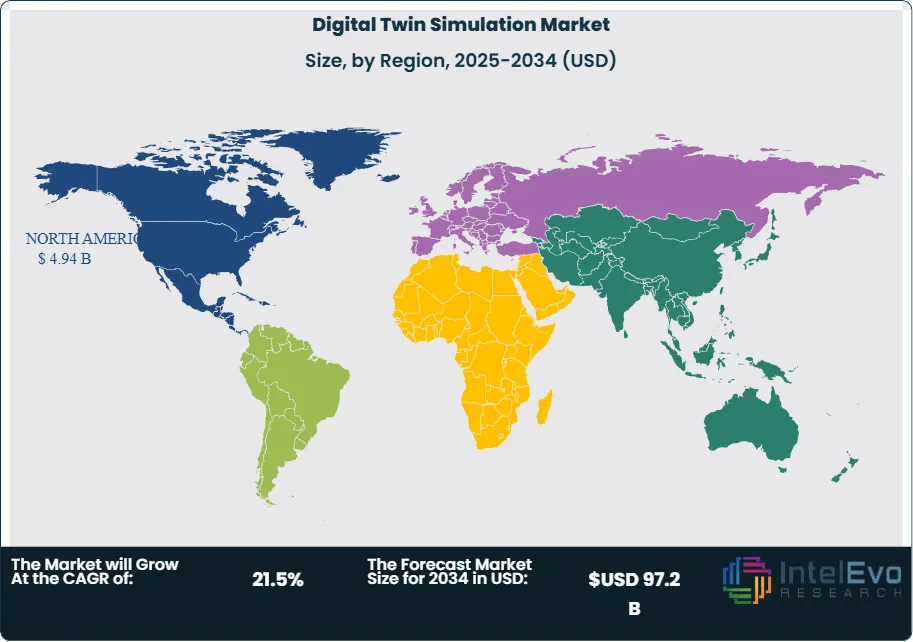

North America leads the global digital twin simulation market, supported by strong investments in R&D, a mature industrial base, and early adoption of advanced technologies. The Asia-Pacific region is the fastest-growing market, fueled by rapid industrialization, smart city initiatives, and government support for digital transformation. Europe maintains a significant presence due to its focus on sustainability, automotive innovation, and regulatory compliance.

The COVID-19 pandemic accelerated digital transformation, highlighting the value of remote monitoring, virtual commissioning, and scenario planning. Organizations increasingly rely on digital twins to ensure business continuity, optimize resource allocation, and enhance resilience against future disruptions.

Rising demand for predictive maintenance, asset optimization, and real-time process control is reshaping market dynamics. The convergence of digital twins with AR/VR, blockchain, and 5G connectivity is unlocking new opportunities for immersive simulation, secure data sharing, and ultra-low-latency applications.

, Technology (IoT, Artificial Intelligence, Big Data Analytics, Augmented Reality, Virtual Reality), Application (Predictive Maintenance, Product Design and Development, Performance Monitoring, Fleet Management), Industry Vertical(Manufacturing, Automotive, Aerospace and Defense, Energy and Utilities, Healthcare), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways

- Market Growth: The Digital Twin Simulation Market is expected to reach USD 97.2 Billion by 2034, driven by Industry 4.0 adoption, IoT proliferation, and the need for operational efficiency.

- Type Dominance: System Digital Twins lead the segment, enabling end-to-end simulation of complex industrial processes and infrastructure.

- Application Dominance: Predictive Maintenance and Asset Management are the largest application areas, as organizations seek to minimize downtime and extend asset lifecycles.

- Driver: Growth is propelled by the need for real-time monitoring, cost reduction, and accelerated product development cycles.

- Restraint: High implementation costs, data integration challenges, and cybersecurity risks hinder widespread adoption.

- Opportunity: The market is poised for expansion through AI-driven autonomous twins, integration with AR/VR for immersive simulation, and adoption in emerging sectors like healthcare and smart cities.

- Trend: The rise of cloud-native digital twins, edge analytics, and blockchain-enabled data integrity is transforming simulation capabilities and business models.

- Regional Analysis: North America leads due to advanced industrial infrastructure, while Asia-Pacific is the fastest-growing region, and Europe maintains a strong focus on sustainability and compliance.

Type Analysis

System Digital Twins represent the leading segment, providing comprehensive simulation of entire production lines, energy grids, or transportation networks. These digital twins enable organizations to model complex interactions, optimize workflows, and test scenarios before implementation. Their dominance is driven by the need for holistic visibility and control in large-scale operations. Component and Process Digital Twins are also significant, focusing on individual assets or specific processes. These are widely used in manufacturing, automotive, and aerospace for design validation, quality assurance, and process optimization.

Application Analysis

Predictive Maintenance and Asset Management Lead With Over 35% Market Share. Predictive maintenance is the largest application, leveraging digital twins to monitor equipment health, predict failures, and schedule maintenance proactively. This reduces unplanned downtime, lowers maintenance costs, and extends asset lifespans. Asset management applications use digital twins for real-time tracking, performance optimization, and lifecycle management. Other key applications include product design and development, supply chain optimization, energy management, and urban planning.

Region Analysis

North America dominates the global digital twin simulation market, supported by a robust industrial sector, high R&D investment, and early adoption of digital transformation initiatives. The region benefits from a strong presence of leading technology providers and a culture of innovation. The Asia-Pacific region is the fastest-growing market, driven by rapid industrialization, government-led smart city projects, and increasing adoption of IoT and AI technologies. China, Japan, and South Korea are key contributors. Europe maintains a significant market share, focusing on sustainability, automotive innovation, and regulatory compliance, particularly in Germany, France, and the UK.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type

- Product/Component Digital Twin

- Process Digital Twin

- System Digital Twin

By Technology

- IoT & IIoT

- Artificial Intelligence (AI) & Machine Learning (ML)

- Cloud Computing & Big Data Analytics

- Augmented Reality (AR) & Virtual Reality (VR)

By End-User Industry

- Manufacturing

- Healthcare

- Automotive & Transportation

- Aerospace & Defense

- Energy & Utilities

- Oil & Gas

- Retail & Consumer Goods

- Others

By Application

- Predictive Maintenance

- Business Optimization

- Asset Performance Management

- Real-Time Monitoring

- Simulation & Design

- Others

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 15.8 B |

| Forecast Revenue (2034) | USD 97.2 B |

| CAGR (2025-2034) | 21.5% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Product/Component Digital Twin, Process Digital Twin, System Digital Twin), By Technology (IoT & IIoT, Artificial Intelligence (AI) & Machine Learning (ML), Cloud Computing & Big Data Analytics, Augmented Reality (AR) & Virtual Reality (VR)), By End-User Industry (Manufacturing, Healthcare, Automotive & Transportation, Aerospace & Defense, Energy & Utilities, Oil & Gas, Retail & Consumer Goods, Others), By Application (Predictive Maintenance, Business Optimization, Asset Performance Management, Real-Time Monitoring, Simulation & Design, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Siemens AG, General Electric (GE), IBM Corporation, Microsoft Corporation, PTC Inc., SAP SE, Oracle Corporation, Ansys, Inc., Dassault Systèmes, Robert Bosch GmbH, AVEVA Group plc, Bentley Systems, Incorporated, Altair Engineering, Inc., Hexagon AB, Rockwell Automation, Inc., Autodesk, Inc., Emerson Electric Co., Schneider Electric SE, Huawei Technologies Co., Ltd., ABB Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Technology (IoT, Artificial Intelligence, Big Data Analytics, Augmented Reality, Virtual Reality), Application (Predictive Maintenance, Product Design and Development, Performance Monitoring, Fleet Management), Industry Vertical(Manufacturing, Automotive, Aerospace and Defense, Energy and Utilities, Healthcare), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Technology (IoT, Artificial Intelligence, Big Data Analytics, Augmented Reality, Virtual Reality), Application (Predictive Maintenance, Product Design and Development, Performance Monitoring, Fleet Management), Industry Vertical(Manufacturing, Automotive, Aerospace and Defense, Energy and Utilities, Healthcare), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Technology (IoT, Artificial Intelligence, Big Data Analytics, Augmented Reality, Virtual Reality), Application (Predictive Maintenance, Product Design and Development, Performance Monitoring, Fleet Management), Industry Vertical(Manufacturing, Automotive, Aerospace and Defense, Energy and Utilities, Healthcare), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Digital Twin Simulation Market?

The Global Digital Twin Simulation Market is set to grow from USD 12.7B in 2024 to USD 95.8B by 2034, driven by IoT, AI, and Industry 4.0 adoption.

Who are the major players in the Digital Twin Simulation Market?

Siemens AG, General Electric (GE), IBM Corporation, Microsoft Corporation, PTC Inc., SAP SE, Oracle Corporation, Ansys, Inc., Dassault Systèmes, Robert Bosch GmbH, AVEVA Group plc, Bentley Systems, Incorporated, Altair Engineering, Inc., Hexagon AB, Rockwell Automation, Inc., Autodesk, Inc., Emerson Electric Co., Schneider Electric SE, Huawei Technologies Co., Ltd., ABB Ltd.

Which segments covered the Digital Twin Simulation Market?

By Type (Product/Component Digital Twin, Process Digital Twin, System Digital Twin), By Technology (IoT & IIoT, Artificial Intelligence (AI) & Machine Learning (ML), Cloud Computing & Big Data Analytics, Augmented Reality (AR) & Virtual Reality (VR)), By End-User Industry (Manufacturing, Healthcare, Automotive & Transportation, Aerospace & Defense, Energy & Utilities, Oil & Gas, Retail & Consumer Goods, Others), By Application (Predictive Maintenance, Business Optimization, Asset Performance Management, Real-Time Monitoring, Simulation & Design, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date