- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Directed Evolution Platform Market Forecast 2034 | CAGR 13.0%

Global Directed Evolution Platform Market Size, Share, Growth & Industry Analysis By Platform Type (Software & Computational Tools, Wet-Lab Screening Infrastructure, Integrated Platform Solutions, Contract Directed Evolution Services), By End-Use Application (Pharmaceuticals & Biocatalysis, Industrial Biotechnology, Biofuels, Agriculture, Food & Beverage), By Technology Approach (Error-Prone PCR, DNA Shuffling, Saturation Mutagenesis, AI-Guided Evolution) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

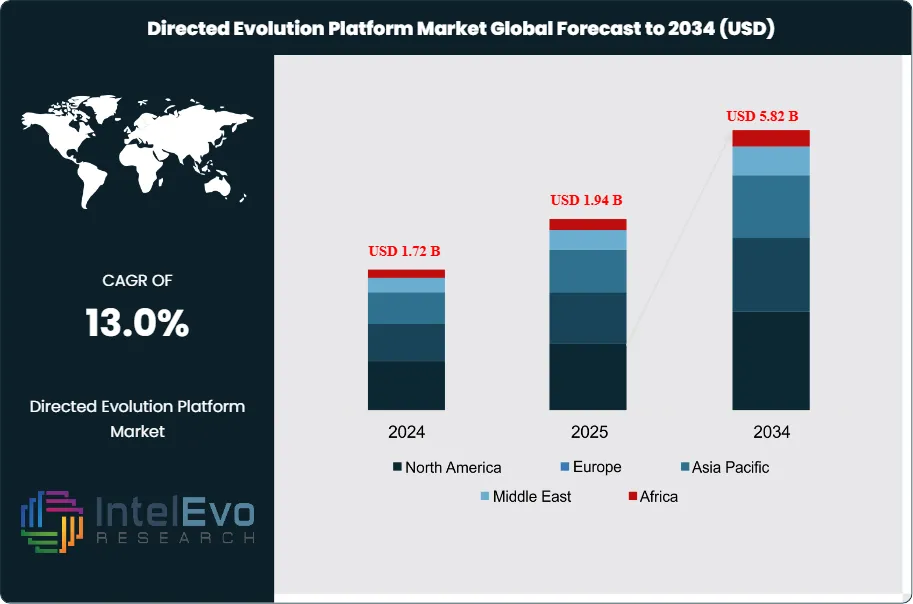

| USD 1.94 Billion | USD 5.82 Billion | 13.0% | North America, 41.2% |

The Directed Evolution Platform Market was valued at approximately USD 1.72 Billion in 2024 and reached USD 1.94 Billion in 2025. The market is projected to grow to USD 5.82 Billion by 2034, expanding at a CAGR of 13.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.88 Billion over the analysis period, driven by surging pharmaceutical biocatalysis demand, rapid integration of machine learning into protein engineering workflows, and the commercial expansion of synthetic biology applications across industrial biotechnology, agriculture, and specialty chemicals.

Get More Information about this report -

Request Free Sample ReportDirected evolution platforms replicate and accelerate natural selection in a laboratory setting, iteratively generating and screening large libraries of protein variants to identify those with superior catalytic activity, stability, substrate specificity, or resistance to industrial process conditions. The commercial directed evolution platform market spans both the computational tools used to design and predict beneficial mutations and the wet-lab infrastructure enabling high-throughput screening of variant libraries. Nobel Prize recognition for directed evolution in 2018 substantially increased academic and commercial awareness of the technology, and the subsequent decade of platform investment has produced a mature commercial ecosystem spanning pharmaceutical biocatalysis, industrial enzyme production, biofuel manufacturing, and agricultural biotechnology.

Several structural forces are accelerating directed evolution platform market growth. Pharmaceutical manufacturers are integrating biocatalytic synthesis routes into an estimated 40% of new chemical entity production workflows as of 2025, creating sustained demand for platforms capable of engineering enantioselective enzymes at commercial scale. The FDA's acceptance of biocatalytic process chemistry in NDA submissions and the ICH Q11 guideline framework for biotechnological drug substance manufacturing have both removed regulatory barriers that previously constrained pharmaceutical adoption. On the technology side, the deployment of deep learning protein fitness prediction tools trained on databases of millions of characterized protein variants has compressed directed evolution campaign timelines from 18-36 months to 6-12 months for well-characterized enzyme families, delivering a 55-65% reduction in per-program R&D cost.

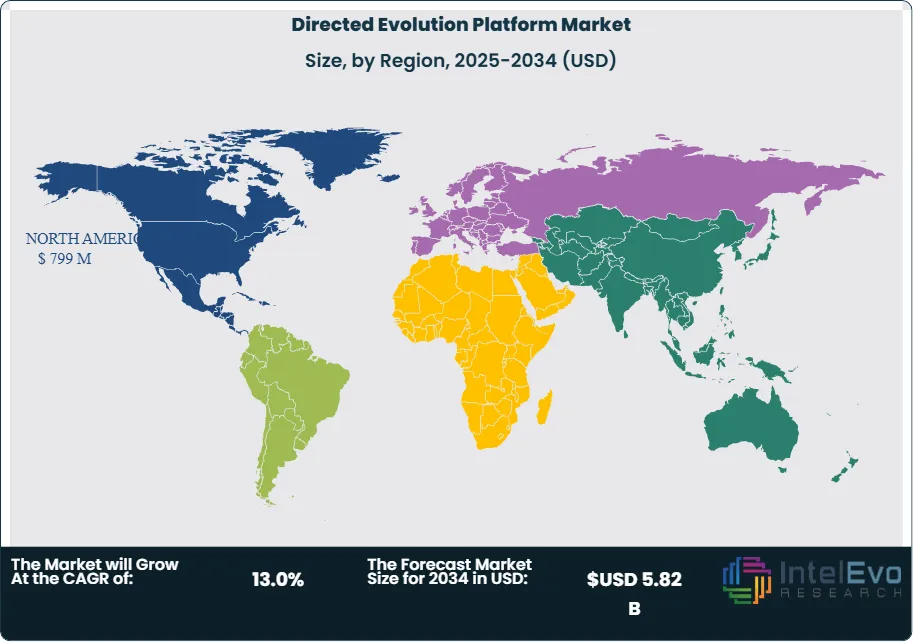

North America dominated the directed evolution platform market with a 41.2% share in 2025, equivalent to USD 799 Million, driven by concentrated venture capital funding for synthetic biology, deep NIH investment in protein engineering research, and a dense cluster of pharmaceutical manufacturing facilities deploying engineered biocatalysts. Europe held a 27.8% share, anchored by industrial biotechnology leaders in Denmark, Germany, and the Netherlands. Asia Pacific is the fastest-growing regional market at a projected CAGR of 15.4% through 2034, as China and India build domestic directed evolution capabilities to support pharmaceutical API manufacturing and industrial enzyme production. The directed evolution platform market remains moderately fragmented, with the top four platform providers holding approximately 46% of combined global revenues in 2025.

, By End-Use Application (Pharmaceuticals & Biocatalysis, Industrial Biotechnology, Biofuels, Agriculture, Food & Beverage), By Technology Approach (Error-Prone PCR, DNA Shuffling, Saturation Mutagenesis, AI-Guided Evolution) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global directed evolution platform market was valued at USD 1.94 Billion in 2025 and is forecast to reach USD 5.82 Billion by 2034, registering a CAGR of 13.0% over the 2026-2034 period.

- Segment Dominance: By platform type, software and computational tools held the largest share at 39.4% of the directed evolution platform market in 2025, reflecting rapid adoption of machine learning-guided protein fitness prediction across pharmaceutical and industrial applications.

- Segment Dominance: By end-use application, pharmaceuticals and biocatalysis accounted for 44.8% of directed evolution platform market revenues in 2025, driven by demand for enantioselective enzymes in API synthesis and ADC bioconjugation workflows.

- Driver: Integration of AI-assisted protein fitness prediction with wet-lab directed evolution has reduced average campaign timelines by 55-65%, enabling pharmaceutical manufacturers to adopt biocatalytic synthesis routes at lower cost and faster cycle times.

- Restraint: High platform access costs, averaging USD 500,000 to USD 3 Million per directed evolution campaign for pharmaceutical applications, constrain adoption among smaller biotech firms and academic spinouts lacking large R&D budgets.

- Opportunity: The global antibody-drug conjugate market, projected to exceed USD 22 Billion by 2034, presents a growing addressable opportunity for directed evolution platforms supplying site-specific conjugation enzymes such as sortases and transglutaminases.

- Trend: Microfluidic high-throughput screening adoption within directed evolution workflows grew at approximately 18.3% annually in 2025, enabling screening of 10 million or more variants per campaign versus 10,000-100,000 in conventional plate-based formats.

- Regional Analysis: North America led the directed evolution platform market with a 41.2% share, equivalent to USD 799 Million in 2025, supported by concentrated pharmaceutical manufacturing, synthetic biology venture funding, and NIH protein engineering research programs.

Competitive Landscape Overview

The directed evolution platform market is moderately fragmented, with the top four providers — Codexis, Ginkgo Bioworks, Twist Bioscience, and Novonesis — collectively accounting for approximately 46% of global revenues in 2025. Competition centers on the breadth and accuracy of machine learning fitness prediction models, high-throughput screening throughput capacity, and the depth of validated enzyme families in proprietary protein databases. M&A activity intensified during 2024-2025, most notably Twist Bioscience's acquisition of Denovium to integrate deep learning protein design, and Evozyne's USD 78 Million Series B to scale its computational platform. New entrants from the AI protein design space are increasing competitive pressure on established wet-lab-centric platform providers.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Codexis Inc. | USA | Leader | CodeEvolver Platform | North America | Secured USD 45M biocatalysis partnership with a top-10 pharma company for stereoselective API synthesis; June 2025. |

| Ginkgo Bioworks | USA | Leader | Foundry DE Platform | North America | Signed multi-year R&D collaboration with BASF for AI-guided enzyme evolution in specialty chemicals; February 2025. |

| Twist Bioscience | USA | Leader | Silicon-Based DNA Synthesis for DE Libraries | North America & Europe | Launched Twist Library Design Suite v3.0 in Q1 2025, enabling higher-diversity mutant libraries for directed evolution screening. |

| Evozyne Inc. | USA | Challenger | ProFACS Computational DE Platform | North America | Raised USD 78M Series B in December 2024 to scale its machine learning-guided protein fitness prediction platform. |

| Protein Evolution Inc. | USA | Challenger | AI-Guided Variant Screening | North America | Partnered with Lonza in March 2025 to integrate directed evolution workflows into cGMP biomanufacturing processes. |

| Arzeda Corp. | USA | Challenger | Computational Protein Design + DE | North America | Expanded enzyme design services to agricultural biotech sector with a new platform launch in Q2 2025. |

| Novonesis (Novozymes) | Denmark | Leader | Proprietary DE Engine (Industrial) | Europe & Global | Completed Novozymes-Chr. Hansen merger in January 2025; combined DE infrastructure now serves 40+ industries globally. |

| Creative Enzymes | USA | Niche Player | Custom Directed Evolution Services | North America | Launched high-throughput microfluidic screening service for SME biopharma clients in September 2025. |

| Alveo Technologies | USA | Niche Player | Optofluidic Screening Platform for DE | North America | Entered partnership with a US academic genome center for directed evolution screening technology co-development; 2025. |

| c-LEcta GmbH | Germany | Niche Player | Pharmaceutical DE & Immobilization | Europe | Raised EUR 22M Series B in January 2026 to scale pharmaceutical-grade directed evolution manufacturing. |

Segmentation Analysis

By Platform Type

The directed evolution platform market by platform type spans software and computational tools, wet-lab screening infrastructure, integrated platform solutions, and contract directed evolution services. Software and computational tools held the largest segment share at 39.4% of the directed evolution platform market in 2025, equivalent to approximately USD 765 Million. This segment covers machine learning fitness prediction models, protein library design software, structural prediction tools derived from AlphaFold architectures, and bioinformatics pipelines for variant characterization. The shift toward AI-driven protein engineering has propelled software tools from an auxiliary role to the primary point of competitive differentiation for platform providers. Ginkgo Bioworks, Evozyne, and Arzeda each center their commercial propositions on proprietary computational models that predict beneficial mutations before any wet-lab screening takes place, reducing the number of experimental variants required and lowering campaign costs substantially.

Wet-lab screening infrastructure, comprising robotic liquid handling systems, microfluidic droplet platforms, and high-throughput spectrophotometric assay equipment, accounted for 28.6% of the directed evolution platform market in 2025. This segment is dominated by instrument manufacturers supplying the enabling hardware, including ultra-high-throughput microfluidic sorters capable of evaluating 10 million variants per experiment. Integrated platform solutions, where computational design and wet-lab screening capabilities are delivered as a bundled service, held 19.7% of the market in 2025. These solutions are most commonly accessed by pharmaceutical companies lacking internal protein engineering infrastructure. Contract directed evolution services, where platform providers conduct full directed evolution campaigns on behalf of clients on a fee-for-service or milestone-based model, captured the remaining 12.3% of the directed evolution platform market in 2025 and are growing fastest among small biotech and agrochemical clients.

By End-Use Application

The directed evolution platform market by end-use application reveals pharmaceuticals and biocatalysis as the clear revenue leader, with a 44.8% share in 2025 equivalent to USD 870 Million. Pharmaceutical manufacturers deploy directed evolution platforms to engineer enantioselective ketoreductases, transaminases, and lipases for active pharmaceutical ingredient synthesis, replacing chemical asymmetric synthesis with enzymatic routes that deliver greater selectivity at ambient conditions. The FDA's regulatory receptiveness to biocatalytic process chemistry, as codified in guidance documents including ICH Q11, has accelerated this shift. In the ADC manufacturing segment, site-specific conjugation enzymes engineered by directed evolution platforms are now central to payload attachment processes for approved therapies such as those developed under BLA filings at major oncology companies.

Industrial biotechnology and specialty chemicals represented 24.6% of the directed evolution platform market in 2025. Enzyme engineering for detergent formulations, textile processing, and paper manufacturing drives steady demand for platforms capable of delivering thermostable and pH-tolerant enzyme variants. The biofuels sector accounted for 13.2% of the market in 2025, with directed evolution platforms supplying optimized cellulase and hemicellulase cocktails for lignocellulosic ethanol production. Agricultural biotechnology held a 9.7% share, driven by demand for evolved enzymes serving crop protection biosynthesis and nitrogen fixation enhancement. Food and beverage applications, research tools supply, and other specialty uses collectively represented the remaining 7.7% of the directed evolution platform market in 2025.

By Technology Approach

Directed evolution platform market segmentation by technology approach covers error-prone PCR and random mutagenesis, DNA shuffling and recombination, saturation mutagenesis, and AI-guided semi-rational directed evolution. Error-prone PCR and random mutagenesis methods, which introduce stochastic mutations across the full gene sequence, represented 33.8% of the directed evolution platform market in 2025. These approaches remain widely used for initial variant generation in both academic and commercial settings because of their technical accessibility and compatibility with most screening infrastructure. DNA shuffling and recombination techniques, which combine beneficial mutations from multiple parent sequences by in vitro recombination, held a 22.4% technology share in 2025 and are particularly effective for complex multi-domain enzyme improvement projects.

Saturation mutagenesis, where every amino acid position or selected active-site positions are systematically substituted, accounted for 19.3% of the directed evolution platform market in 2025 and is the preferred approach for pharmaceutical applications requiring precise active-site optimization. AI-guided semi-rational directed evolution, where machine learning models nominate specific residue positions most likely to yield improvement and saturation mutagenesis is applied only at those positions, held 24.5% of the technology market in 2025 and is the fastest-growing approach, projected to reach 38% of technology revenues by 2034 as model accuracy increases and computational access costs decline.

By End-User

The directed evolution platform market by end-user segments into pharmaceutical and biopharmaceutical companies, industrial biotechnology firms, academic and government research institutions, contract research organizations, and agricultural biotechnology companies. Pharmaceutical and biopharmaceutical companies held the largest end-user share at 42.3% in 2025. These organizations access directed evolution platforms through both in-house deployment of licensed software tools and computational screening infrastructure, and through partnership arrangements with specialist platform providers such as Codexis and Evozyne. Industrial biotechnology firms accounted for 26.8% of the directed evolution platform end-user market in 2025, accessing platforms primarily through industrial enzyme developers such as Novonesis and BASF for in-house enzyme optimization. Academic and government research institutions held 16.4% in 2025, supported by NIH, EU Horizon, and national science foundation grant funding. Contract research organizations and agricultural biotechnology companies together represented the remaining 14.5% of the directed evolution platform end-user market in 2025.

Regional Analysis

North America

North America directed evolution platform market held a 41.2% share in 2025, generating approximately USD 799 Million in revenue. The United States accounts for the vast majority of regional market activity, driven by a concentration of synthetic biology companies, extensive NIH-funded protein engineering programs at institutions including Caltech and MIT, and the presence of global pharmaceutical manufacturers with active biocatalysis programs in New Jersey, Massachusetts, and California. The National Biotechnology and Biomanufacturing Initiative, launched in 2022 and expanded through subsequent executive actions, has directed substantial federal funding toward domestic biocatalysis infrastructure, benefiting directed evolution platform developers. Venture capital investment in synthetic biology companies in the US reached approximately USD 4.1 Billion in 2024, sustaining a pipeline of startups building directed evolution platform capabilities. Canada contributes through academic protein engineering programs at the University of Toronto and industrial bioprocessing facilities in Quebec and Ontario. Mexico represents an emerging market for contract directed evolution services serving its growing pharmaceutical API manufacturing sector.

Europe

Europe directed evolution platform market represented 27.8% of global revenues in 2025, equivalent to USD 540 Million. Denmark is the most significant national market within Europe, anchored by Novonesis, whose industrial directed evolution infrastructure spans 12 research centers globally and serves enzyme engineering clients across food, pharmaceutical, and agriculture sectors. Germany hosts a cluster of specialist directed evolution and biocatalysis firms including c-LEcta and AB Enzymes, supported by Fraunhofer Institute-linked technology transfer programs and BMBF biotechnology funding. The Netherlands is home to DSM-Firmenich's bioprocessing innovation infrastructure, and the UK maintains an active academic-commercial directed evolution ecosystem centered on collaborations between Imperial College London, University of Manchester, and spin-out companies. The EU Horizon Europe program allocated approximately EUR 3.2 Billion to biotechnology and bioeconomy research for 2021-2027, a portion of which directly funds directed evolution platform development. REACH regulation compliance is also driving European chemical manufacturers toward biocatalytic alternatives, creating sustained platform demand.

Asia Pacific

Asia Pacific held approximately 21.6% of the directed evolution platform market in 2025, generating USD 419 Million, and is the fastest-growing region with a projected CAGR of 15.4% through 2034. China is the dominant national market in the region, where the government's 14th Five-Year Plan explicitly targets biomanufacturing as a strategic priority and state-funded biotechnology programs are building domestic directed evolution capabilities at institutions including the Tianjin Institute of Industrial Biotechnology. Chinese pharmaceutical companies are increasingly adopting biocatalytic synthesis for generic API production, creating demand for directed evolution platforms that can deliver cost-effective enzyme optimization. Japan maintains a sophisticated industrial biotechnology sector with Amano Enzyme and Shin Nihon Chemical both operating directed evolution programs for food and pharmaceutical enzyme development. India is emerging as a significant Asia Pacific directed evolution market, driven by the world's largest generic pharmaceutical manufacturing industry and growing investment in domestic biotechnology R&D. South Korea's biosimilar manufacturing sector, producing complex glycoprotein biologics for export, requires glycoengineering enzymes that depend on directed evolution platform capabilities.

Latin America

Latin America represented approximately 5.6% of the directed evolution platform market in 2025, generating USD 109 Million. Brazil is the region's dominant market, where sugarcane bioethanol and agricultural biotechnology sectors drive demand for directed evolution services targeting cellulases and nitrogen fixation enzymes. Brazil's EMBRAPA agricultural research network has piloted directed evolution programs for crop-relevant enzyme optimization, and domestic pharmaceutical companies are beginning to explore biocatalytic synthesis for API production. Argentina represents the second-largest Latin American market for directed evolution platforms, with agricultural biotech applications in soybean and corn processing driving enzyme engineering demand. The region is predominantly a consumer of contract directed evolution services and licensed computational tools rather than a developer of proprietary platforms, reflecting a talent pool and infrastructure base still in early development. Government biotechnology promotion programs in Brazil and Chile are beginning to support academic-commercial directed evolution collaborations.

Middle East & Africa

The Middle East and Africa region held approximately 3.8% of the directed evolution platform market in 2025, generating USD 74 Million. The UAE and Saudi Arabia are the primary demand centers, where government diversification strategies including Saudi Vision 2030 are funding biotechnology and industrial fermentation capacity. Saudi Aramco's downstream diversification program includes exploration of biocatalytic upgrading technologies, creating early-stage directed evolution platform demand in the petrochemical sector. Israel, while a small national market, is a disproportionately significant contributor to the regional directed evolution platform segment through its concentrated deep-tech biotech cluster, with companies such as Evogene applying computational biology tools to directed evolution for agricultural enzyme applications. South Africa leads the African directed evolution market, with mining bioleaching enzyme applications and food processing biotechnology creating commercial interest in platform access. Infrastructure gaps in fermentation capacity and high-throughput screening equipment constrain regional growth, but technology partnerships with European and North American platform developers are beginning to address these barriers.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Platform Type

- Software & Computational Tools

- Wet-Lab Screening Infrastructure

- Integrated Platform Solutions

- Contract Directed Evolution Services

By End-Use Application

- Pharmaceuticals & Biocatalysis

- Industrial Biotechnology & Specialty Chemicals

- Biofuels & Renewable Energy

- Agricultural Biotechnology

- Food & Beverage

- Research Tools & Others

By Technology Approach

- Error-Prone PCR & Random Mutagenesis

- DNA Shuffling & Recombination

- Saturation Mutagenesis

- AI-Guided Semi-Rational Directed Evolution

By End-User

- Pharmaceutical & Biopharmaceutical Companies

- Industrial Biotechnology Firms

- Academic & Government Research Institutions

- Contract Research Organizations

- Agricultural Biotechnology Companies

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.94 B |

| Forecast Revenue (2034) | USD 5.82 B |

| CAGR (2025-2034) | 13.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Platform Type, (Software & Computational Tools, Wet-Lab Screening Infrastructure, Integrated Platform Solutions, Contract Directed Evolution Services), By End-Use Application, (Pharmaceuticals & Biocatalysis, Industrial Biotechnology & Specialty Chemicals, Biofuels & Renewable Energy, Agricultural Biotechnology, Food & Beverage, Research Tools & Others), By Technology Approach, (Error-Prone PCR & Random Mutagenesis, DNA Shuffling & Recombination, Saturation Mutagenesis, AI-Guided Semi-Rational Directed Evolution), By End-User, (Pharmaceutical & Biopharmaceutical Companies, Industrial Biotechnology Firms, Academic & Government Research Institutions, Contract Research Organizations, Agricultural Biotechnology Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CODEXIS INC., GINKGO BIOWORKS, TWIST BIOSCIENCE, NOVONESIS (NOVOZYMES A/S), EVOZYNE INC., PROTEIN EVOLUTION INC., ARZEDA CORP., CREATIVE ENZYMES, ALVEO TECHNOLOGIES, C-LECTA GMBH, ABSCI CORPORATION, BIOMILQ (CELL-FREE DE APPLICATIONS), INSCRIPTA INC., TELESIS BIO, DENOVIUM (ACQUIRED BY TWIST BIOSCIENCE), ENZYME BY DESIGN (EBD), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use Application (Pharmaceuticals & Biocatalysis, Industrial Biotechnology, Biofuels, Agriculture, Food & Beverage), By Technology Approach (Error-Prone PCR, DNA Shuffling, Saturation Mutagenesis, AI-Guided Evolution) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Pharmaceuticals & Biocatalysis, Industrial Biotechnology, Biofuels, Agriculture, Food & Beverage), By Technology Approach (Error-Prone PCR, DNA Shuffling, Saturation Mutagenesis, AI-Guided Evolution) Industry Trends & Forecast 2026–2034")

, By End-Use Application (Pharmaceuticals & Biocatalysis, Industrial Biotechnology, Biofuels, Agriculture, Food & Beverage), By Technology Approach (Error-Prone PCR, DNA Shuffling, Saturation Mutagenesis, AI-Guided Evolution) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Directed Evolution Platform Market?

Global Directed evolution platform market valued at USD 1.72B in 2024, reaching USD 5.82B by 2034, growing at a CAGR of 13.0% from 2026–2034.

Who are the major players in the Directed Evolution Platform Market?

CODEXIS INC., GINKGO BIOWORKS, TWIST BIOSCIENCE, NOVONESIS (NOVOZYMES A/S), EVOZYNE INC., PROTEIN EVOLUTION INC., ARZEDA CORP., CREATIVE ENZYMES, ALVEO TECHNOLOGIES, C-LECTA GMBH, ABSCI CORPORATION, BIOMILQ (CELL-FREE DE APPLICATIONS), INSCRIPTA INC., TELESIS BIO, DENOVIUM (ACQUIRED BY TWIST BIOSCIENCE), ENZYME BY DESIGN (EBD), OTHERS

Which segments covered the Directed Evolution Platform Market?

By Platform Type, (Software & Computational Tools, Wet-Lab Screening Infrastructure, Integrated Platform Solutions, Contract Directed Evolution Services), By End-Use Application, (Pharmaceuticals & Biocatalysis, Industrial Biotechnology & Specialty Chemicals, Biofuels & Renewable Energy, Agricultural Biotechnology, Food & Beverage, Research Tools & Others), By Technology Approach, (Error-Prone PCR & Random Mutagenesis, DNA Shuffling & Recombination, Saturation Mutagenesis, AI-Guided Semi-Rational Directed Evolution), By End-User, (Pharmaceutical & Biopharmaceutical Companies, Industrial Biotechnology Firms, Academic & Government Research Institutions, Contract Research Organizations, Agricultural Biotechnology Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Directed Evolution Platform Market

Published Date : 17 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date