- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Disposables Packaging Market Size, Growth Trends | CAGR of 7.6%

Global Disposables Packaging Market Size, Share & Materials Analysis By Product Type (Plastics, Paper, Biodegradable), By End Use (Foodservice, Healthcare, E-commerce), Sustainability Regulations, Smart Packaging Trends & Forecast 2025–2034

Report Overview

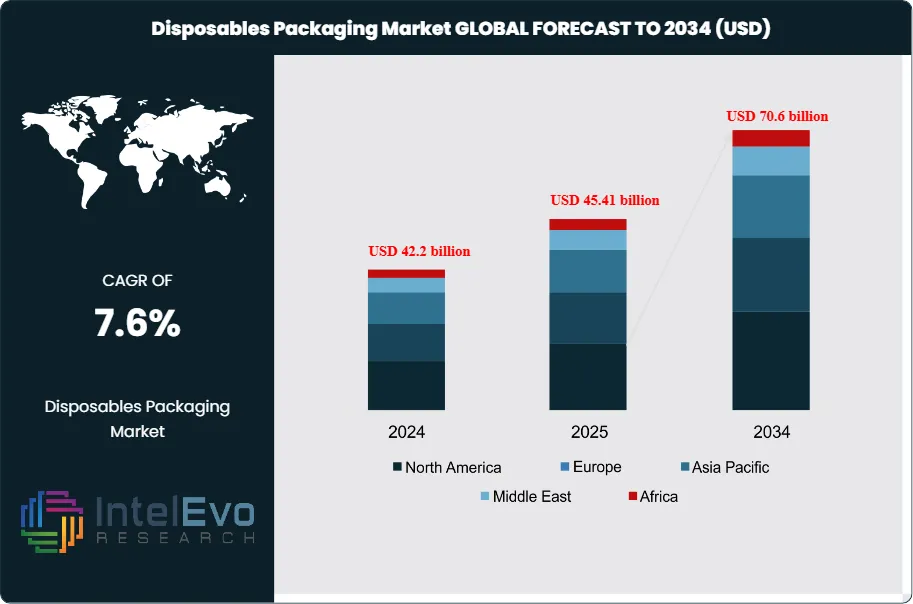

The Disposables Packaging Market is estimated at USD 42.2 billion in 2024 and is on track to reach roughly USD 70.6 billion by 2034, implying a compound annual growth rate of 7.6% over 2025–2034. This growth is driven by the rapid expansion of food delivery, e-commerce, and healthcare services, where hygiene, convenience, and safety are non-negotiable requirements. Increasing adoption of sustainable, biodegradable, and recyclable packaging materials is further accelerating market momentum. In parallel, smart packaging features such as QR codes and tamper-evident designs are enhancing consumer trust and regulatory compliance, positioning disposable packaging as a critical enabler of modern consumption patterns.

Get More Information about this report -

Request Free Sample ReportThis steady expansion reflects the growing role of single-use packaging across food, healthcare, retail, and e-commerce supply chains. Historically, the market has expanded in line with urbanization and rising hygiene standards. Over the past decade, the surge in online retail has accelerated demand, with global e-commerce sales reaching USD 5.9 trillion in 2023 and projected to surpass USD 8 trillion by 2027. This structural shift has made protective, lightweight, and disposable packaging a critical enabler of logistics efficiency.

Demand-side growth is driven by consumer preference for convenience, safety, and hygiene. Food delivery platforms and healthcare providers rely heavily on disposable formats to ensure compliance and reduce contamination risks. On the supply side, manufacturers face rising costs of raw materials and increasing competition, which has intensified price pressures. Market saturation is evident, with many suppliers offering similar solutions. To differentiate, companies are investing in recyclable paper, compostable bioplastics, and lightweight aluminum formats that balance durability with sustainability.

Regulatory frameworks are reshaping the industry. In the United States, Extended Producer Responsibility laws are gaining momentum, with Minnesota mandating packaging waste management by 2031. Similar policies in Europe and parts of Asia are accelerating the transition toward recyclable and biodegradable materials. Compliance is no longer optional; it is becoming a prerequisite for market access. For investors, this regulatory shift signals both risk and opportunity. Firms that adapt early by redesigning packaging systems will capture share, while laggards may face penalties and reputational setbacks.

Technological progress is also influencing adoption. Automation in packaging lines, AI-driven material optimization, and digital tracking of supply chains are improving efficiency and reducing waste. For example, industry best practices recommend three inches of internal packaging for fragile shipments, a standard increasingly supported by automated design tools. These advances not only reduce product returns—estimated at 20% to 30% of shipments during peak seasons—but also strengthen brand reliability.

Regionally, North America and Western Europe remain mature markets with strong regulatory oversight and high consumer expectations. Asia-Pacific is emerging as the fastest-growing region, supported by rapid e-commerce penetration in China, India, and Southeast Asia. For investors, the most attractive opportunities lie in markets where sustainability mandates intersect with rising consumer demand, creating a clear pathway for growth.

, By End Use (Foodservice, Healthcare, E-commerce), Sustainability Regulations, Smart Packaging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global disposables packaging market was valued at USD 40.2 billion in 2024 and is projected to reach USD 70.6 billion by 2034, expanding at a CAGR of 7.6%. Growth is supported by rising e-commerce volumes, food delivery expansion, and heightened hygiene standards in healthcare and retail.

- Material: Plastic accounted for 41.8% of the market in 2024, driven by its low cost, versatility, and widespread use across foodservice and medical applications. Despite regulatory pressure, its dominance persists due to established supply chains and performance advantages.

- Packaging Type: Flexible packaging led with 52.7% share in 2024, supported by its lightweight properties, reduced logistics costs, and suitability for high-volume food and beverage shipments. Its adoption is expected to remain strong as companies seek cost-efficient formats.

- Product Type: Containers represented 38.9% of the market in 2024, reflecting their critical role in food and beverage packaging. Their durability and ability to preserve freshness make them the preferred choice for quick-service restaurants and delivery platforms.

- End Use: The food and beverage sector held 60.1% share in 2024, underpinned by rising demand for packaged meals, ready-to-eat products, and online food delivery. This segment will remain the largest consumer of disposables packaging through 2034.

- Driver: Global e-commerce sales reached USD 5.9 trillion in 2023 and are forecast to exceed USD 8 trillion by 2027. This surge directly fuels demand for protective disposable packaging to reduce product damage and returns.

- Restraint: Market saturation and price competition are intensifying, with multiple suppliers offering similar solutions. This has compressed margins and limited differentiation, particularly in mature markets.

- Opportunity: Asia-Pacific is expected to record the fastest CAGR through 2034, supported by rapid e-commerce penetration in China, India, and Southeast Asia. Rising consumer demand for sustainable packaging creates a high-growth investment window.

- Trend: Sustainability regulations are reshaping product design. Extended Producer Responsibility laws in the U.S. and Europe are accelerating the shift toward recyclable and compostable materials, with early adopters gaining competitive advantage.

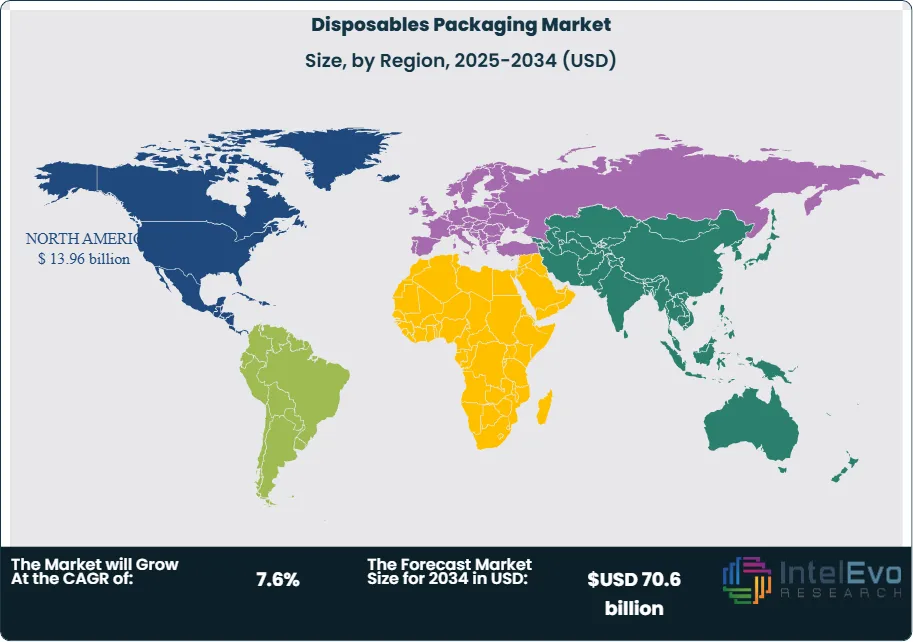

- Regional Analysis: North America led with 35.6% share and USD 13.96 billion in 2024, supported by strong foodservice and healthcare demand. Asia-Pacific is emerging as the key growth hub, while Europe remains a regulatory leader driving sustainable packaging adoption.

Material Type Analysis

Plastic continues to dominate the disposables packaging market, accounting for 41.8% of global share in 2024 and maintaining its lead into 2025. Its low cost, durability, and adaptability across multiple industries make it the preferred choice for food containers, trays, wraps, and medical packaging. Quick-service restaurants and delivery platforms rely heavily on plastic cups, lids, and utensils, while the expansion of online food delivery and convenience retail further sustains demand. Despite regulatory pressure, plastic remains entrenched due to its cost efficiency and ability to preserve freshness and prevent leakage.

Paper and paperboard are gaining traction as sustainability concerns reshape consumer and regulatory priorities. Their recyclability and alignment with corporate sustainability goals have positioned them as the fastest-growing material segment, with adoption rising in retail and foodservice packaging. Aluminum retains a strong presence in beverage cans and foil trays, particularly where extended shelf life is critical. Glass, while niche, is favored in premium and reusable packaging formats. Emerging biodegradable polymers and compostable materials are also entering the market, supported by regulatory incentives and consumer demand for eco-friendly alternatives.

Packaging Type Analysis

Flexible packaging accounted for 52.7% of the market in 2024 and is projected to expand further through 2030. Its lightweight structure, lower material use, and reduced logistics costs make it the preferred choice for snacks, condiments, frozen foods, and single-use consumer products. Flexible formats such as pouches, sachets, and films also extend shelf life by protecting against moisture and oxygen, making them attractive to both manufacturers and retailers. Rising demand for resealable and portable packaging continues to reinforce this segment’s growth trajectory.

Rigid packaging, which includes bottles, containers, and trays, remains essential for products requiring structural integrity and protection. It is widely used in beverages, fragile goods, and heavy items where stacking and durability are critical. While rigid formats face competition from flexible alternatives, their role in foodservice, healthcare, and industrial applications ensures steady demand. Companies are increasingly adopting recyclable rigid materials to align with sustainability regulations, particularly in North America and Europe.

By Product Type

Containers held the largest share at 38.9% in 2024, reflecting their widespread use in foodservice, takeout, and delivery platforms. Their ability to maintain temperature, prevent contamination, and offer portion control makes them indispensable across quick-service restaurants and meal delivery services. The rise of home-delivered meals and ready-to-eat products has further accelerated demand for leak-proof and stackable container formats.

Trays are widely used for bakery items and ready meals, while cups and lids remain essential in cafes and beverage outlets. Bottles continue to dominate in beverages, sauces, and personal care packaging. Pouches and sachets are gaining share due to their convenience in condiments, wipes, and sample packaging. Wraps and films are heavily used in supermarkets for fresh produce and meat. Other formats, including clamshells and hybrid packaging, are expanding as companies experiment with sustainable and compostable designs.

End-Use Industry Analysis

The food and beverage sector accounted for 60.1% of the market in 2024 and remains the largest consumer of disposable packaging in 2025. Rising urbanization, changing dietary habits, and the growth of online food delivery platforms such as Uber Eats and DoorDash continue to drive demand. Disposable packaging ensures hygiene, portability, and convenience, making it indispensable for quick-service restaurants, cafes, and supermarkets.

Healthcare is another critical end-use sector, with disposable packaging used extensively for medicines, diagnostic kits, and sterile instruments. Personal care and cosmetics rely on sachets, bottles, and wipes for portability and consumer convenience. Industrial applications include protective packaging for components, chemicals, and spare parts. Other sectors such as hospitality, education, and events also contribute to demand, particularly for single-use items that support hygiene and efficiency.

Regional Analysis

North America led the global market with a 35.6% share in 2024, valued at USD 13.96 billion, and continues to hold a strong position in 2025. The region’s dominance is supported by high consumption of packaged food, widespread adoption of food delivery services, and strong healthcare demand. Quick-service restaurants and supermarkets remain major contributors, while regulatory pressure is accelerating the shift toward recyclable and biodegradable packaging.

Europe follows closely, driven by stringent sustainability regulations and consumer preference for eco-friendly packaging. The European Union’s circular economy policies are pushing companies to redesign packaging systems and adopt recyclable materials. Asia Pacific is the fastest-growing region, supported by rapid e-commerce expansion in China, India, and Southeast Asia. Latin America and the Middle East & Africa are emerging markets, where rising urban populations and expanding retail networks are creating new opportunities for disposable packaging adoption.

This segmentation highlights a market in transition, where cost efficiency and convenience continue to drive demand, but sustainability and regulatory compliance are increasingly shaping investment priorities.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Material Type

- Plastic

- Paper & Paperboard

- Aluminum

- Glass

- Others

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By Product Type

- Trays

- Containers

- Cups & Lids

- Bottles

- Pouches & Sachets

- Wraps & Films

- Others

By End-Use Industry

- Food & Beverage

- Healthcare

- Personal Care & Cosmetics

- Industrial

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 42.2 B |

| Forecast Revenue (2034) | USD 70.6 B |

| CAGR (2024-2034) | 7.6% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type (Plastic, Paper & Paperboard, Aluminum, Glass, Others), By Packaging Type (Rigid Packaging, Flexible Packaging), By Product Type (Trays, Containers, Cups & Lids, Bottles, Pouches & Sachets, Wraps & Films, Others), By End-Use Industry (Food & Beverage, Healthcare, Personal Care & Cosmetics, Industrial, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Constantia Flexibles Group GmbH, WestRock Company, Novolex Holdings, Inc., Amcor plc, Huhtamaki Oyj, Sealed Air Corporation, Printpack, Inc., Reynolds Group Holdings Limited, Tetra Pak International S.A., Berry Global Inc., Sonoco Products Company, Mondi Group, Bemis Company, Inc. (now part of Amcor) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End Use (Foodservice, Healthcare, E-commerce), Sustainability Regulations, Smart Packaging Trends & Forecast 2025–2034")

, By End Use (Foodservice, Healthcare, E-commerce), Sustainability Regulations, Smart Packaging Trends & Forecast 2025–2034")

, By End Use (Foodservice, Healthcare, E-commerce), Sustainability Regulations, Smart Packaging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Disposables Packaging Market?

The disposables packaging market was valued at USD 42.2 billion in 2024 and is projected to reach USD 70.6 billion by 2034, growing at a CAGR of 7.6% during 2025–2034. Growth is driven by rising food delivery, e-commerce, and healthcare demand, alongside increasing adoption of sustainable, biodegradable, and smart packaging solutions worldwide.

Who are the major players in the Disposables Packaging Market?

Constantia Flexibles Group GmbH, WestRock Company, Novolex Holdings, Inc., Amcor plc, Huhtamaki Oyj, Sealed Air Corporation, Printpack, Inc., Reynolds Group Holdings Limited, Tetra Pak International S.A., Berry Global Inc., Sonoco Products Company, Mondi Group, Bemis Company, Inc. (now part of Amcor)

Which segments covered the Disposables Packaging Market?

By Material Type (Plastic, Paper & Paperboard, Aluminum, Glass, Others), By Packaging Type (Rigid Packaging, Flexible Packaging), By Product Type (Trays, Containers, Cups & Lids, Bottles, Pouches & Sachets, Wraps & Films, Others), By End-Use Industry (Food & Beverage, Healthcare, Personal Care & Cosmetics, Industrial, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Disposables Packaging Market

Published Date : 02 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date