- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Distributed Energy Virtual Power Plant Market Size | CAGR 17.2%

Global Distributed Energy Virtual Power Plant Market Size, Share, Growth & Industry Analysis By DER Type (Battery Energy Storage Systems, Solar PV Plus Storage, Demand Response Loads, EV Smart Charging & V2G, Distributed Generation), By Application (Ancillary Services, Energy Arbitrage, Capacity Markets, Demand Response, Renewable Integration), By Deployment Model (Utility, Aggregator, VPP-as-a-Service) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

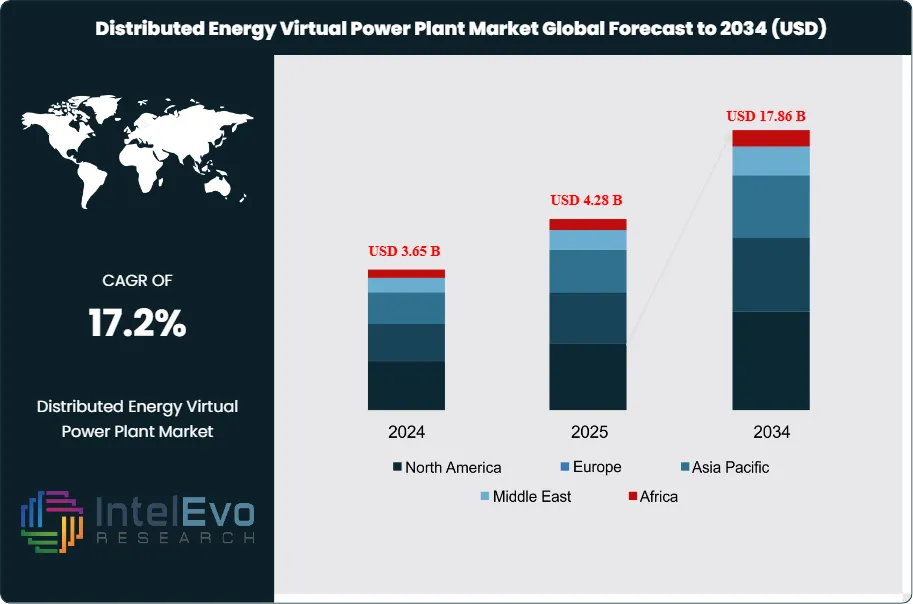

| USD 4.28 Billion | USD 17.86 Billion | 17.2% | North America, 38.4% |

The Distributed Energy Virtual Power Plant Market was valued at approximately USD 3.65 Billion in 2024 and reached USD 4.28 Billion in 2025. The market is projected to grow to USD 17.86 Billion by 2034, expanding at a CAGR of 17.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.58 Billion over the analysis period, driven by the accelerating deployment of distributed energy resources including residential solar, battery storage, electric vehicles, and smart thermostats, combined with regulatory mandates requiring grid operators to integrate these assets into dispatchable electricity supply capacity.

Get More Information about this report -

Request Free Sample ReportA distributed energy virtual power plant (DEVPP) aggregates geographically dispersed DERs including rooftop photovoltaic systems, behind-the-meter batteries, EV chargers, demand response-enrolled appliances, and distributed generators into a software-coordinated virtual generation unit capable of dispatching power and ancillary services into wholesale electricity markets on command. Unlike conventional power plants, DEVPPs carry no generation asset capital cost for their operators; the underlying DER assets are owned by residential and commercial customers, with DEVPP software platforms providing the control, dispatch, and market settlement infrastructure that converts these assets into dispatchable grid capacity. The distributed energy VPP market revenue encompasses software platform licenses, demand response program fees, grid services revenue sharing, VPP-as-a-service contracts, and hardware integration modules.

Several structural forces are accelerating distributed energy virtual power plant market expansion. The US Federal Energy Regulatory Commission's Order 2222, finalized in 2020 and progressively implemented by regional transmission organizations through 2025, mandates that DER aggregators access wholesale electricity markets alongside conventional generators, removing the regulatory barrier that previously excluded VPP operators from capacity market revenue. The EU's Electricity Market Design Reform, adopted in 2024, similarly requires member states to enable DER participation in balancing markets through aggregators by 2026, creating a European-wide regulatory framework that compels utilities to implement VPP programs. The IEA estimates that global DER capacity will surpass 2,000 GW by 2027, with residential battery storage alone growing from 45 GW in 2025 to over 300 GW by 2034, providing the asset base that distributed energy VPP platforms require to scale toward gigawatt aggregation capacity.

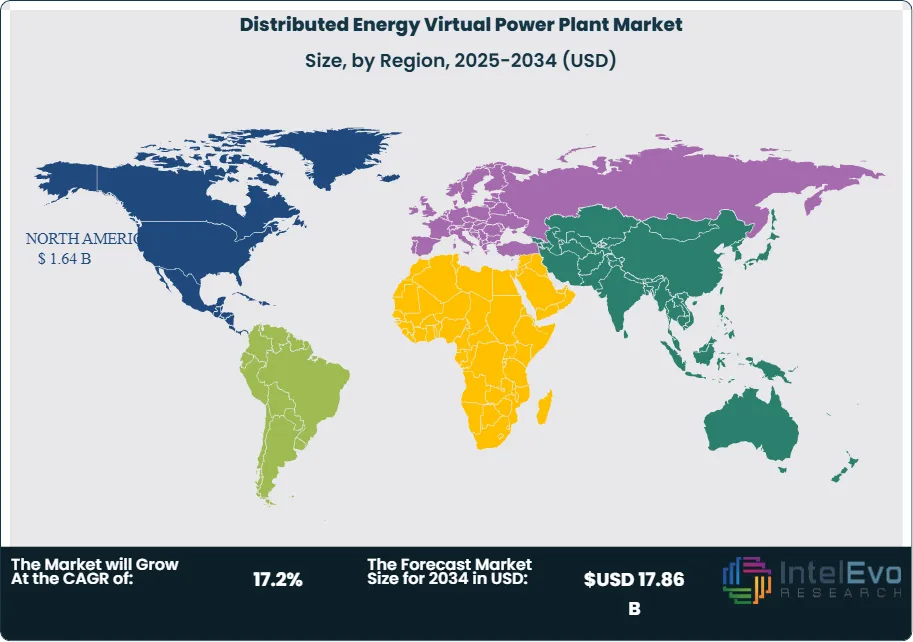

AI-driven dispatch optimization, which uses machine learning to predict renewable generation availability, load demand, and electricity price signals simultaneously at sub-minute resolution, is compressing DEVPP operating margins by 30-40% compared to rule-based dispatch systems and creating a technology performance gap that is defining competitive differentiation among VPP platform vendors. North America led the distributed energy virtual power plant market with a 38.4% share in 2025, equivalent to USD 1.64 Billion. Australia is the most commercially mature residential DEVPP market per capita globally, while Europe's regulatory-driven aggregator frameworks are advancing the continent toward the second-largest market position by 2027.

, By Application (Ancillary Services, Energy Arbitrage, Capacity Markets, Demand Response, Renewable Integration), By Deployment Model (Utility, Aggregator, VPP-as-a-Service) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global distributed energy virtual power plant market was valued at USD 4.28 Billion in 2025 and is forecast to reach USD 17.86 Billion by 2034, registering a CAGR of 17.2% during the 2026-2034 forecast period.

- Segment Dominance: By DER type, battery energy storage systems held the largest share at 36.8% of the distributed energy virtual power plant market in 2025, driven by the proliferation of residential Powerwall-class and commercial C&I battery installations providing the fastest-responding and most dispatchable asset class for VPP frequency regulation and ancillary service delivery.

- Segment Dominance: By end-use application, ancillary services and frequency regulation accounted for 34.2% of the distributed energy virtual power plant market in 2025, reflecting wholesale market operators' critical need for fast-responding DER aggregations to replace the inertia and frequency response services previously provided by retiring thermal power plants.

- Driver: FERC Order 2222 implementation by MISO, PJM, CAISO, and other RTOs has opened wholesale capacity markets to DER aggregators, with VPP capacity clearing capacity market auctions reaching an estimated 8.4 GW in PJM alone by 2025, directly generating revenue streams that improve VPP program economics for both operators and enrolled customers.

- Restraint: Grid interconnection and interoperability standards for DER aggregation remain fragmented across jurisdictions, with VPP operators facing up to 18-month integration timelines for new utility partnerships due to incompatible communication protocols between DER assets, distribution system operators, and wholesale market settlement systems.

- Opportunity: The global electric vehicle fleet is projected to exceed 350 Million vehicles by 2034, with vehicle-to-grid capable EV chargers representing an addressable VPP flexibility market estimated at USD 3.8 Billion annually by 2034 as automakers standardize bidirectional charging interfaces and VPP platforms extend aggregation to EV battery capacity.

- Trend: AI-native VPP platforms using reinforcement learning for real-time multi-asset dispatch across ancillary service, energy arbitrage, and capacity market programs simultaneously grew at approximately 34.8% annual adoption rate among utility-scale VPP operators in 2025, outperforming rule-based legacy platforms by an estimated 28% in revenue per enrolled kilowatt.

- Regional Analysis: North America led the distributed energy virtual power plant market with a 38.4% share, equivalent to USD 1.64 Billion in 2025, driven by FERC Order 2222 market access, DOE VPP loan guarantee programs, and a concentrated base of residential solar-plus-storage VPP programs in California, Texas, and New England.

Competitive Landscape Overview

The distributed energy virtual power plant market is moderately fragmented, with AutoGrid, Siemens Energy, Enbala (Statkraft), and Virtual Peaker collectively holding approximately 44% of global revenues in 2025. Competition centers on AI dispatch model performance, DER asset type breadth, utility partnership depth, and speed of wholesale market settlement system integration. M&A activity intensified in 2024-2025, with Schneider Electric acquiring AutoGrid to integrate VPP software into its energy management suite and Statkraft's Enbala generating significant European traction through utility partnerships across 3 GW of aggregated assets. Tesla Energy's Autobidder platform represents the most commercially deployed consumer VPP globally, with 85,000+ enrolled residential storage systems in Australia and California generating measurable ancillary service revenue.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| AutoGrid Systems | USA | Leader | AutoGrid Flex VPP Platform | North America & Europe | Signed 500 MW VPP aggregation deal with a US investor-owned utility; Q1 2025. |

| Siemens Energy | Germany | Leader | Spectrum Power VPP SCADA Platform | Europe & Global | Launched AI-enhanced Spectrum Power 8 with real-time DER dispatch optimization; March 2025. |

| Enbala (Statkraft) | Canada/Norway | Leader | Concerto VPP Management Software | North America & Europe | Expanded Concerto platform to 3 GW of aggregated DER capacity across North America; Q2 2025. |

| Virtual Peaker | USA | Leader | VPP-as-a-Service Platform for Utilities | North America | Raised USD 35M Series C to expand AI-driven demand response VPP deployments; 2025. |

| Enel X (Enel Group) | Italy | Challenger | JuiceX & DemandConnect VPP | Europe & North America | Expanded JuiceX EV smart charging VPP program to 200,000 vehicles in 8 countries; Q3 2025. |

| Tesla Energy | USA | Challenger | Autobidder Real-Time VPP Trading | North America & Australia | Expanded Autobidder Powerwall VPP to 85,000 households in Australia and California; 2025. |

| Fluence Energy | USA | Challenger | Mosaic Bidding & VPP Software | North America & Asia Pacific | Secured USD 120M contract for grid-scale BESS VPP integration in South Korea; 2025. |

| Landis+Gyr | Switzerland | Niche Player | Gridstream VPP & AMI Integration | Europe & North America | Partnered with a German DSO for smart meter-enabled VPP demand response; Q2 2025. |

| Enphase Energy | USA | Niche Player | IQ Microgrid & VPP Integration | North America | Launched Enphase VPP program covering 100,000 residential solar+storage systems; Q3 2025. |

| Generac Power Systems | USA | Niche Player | PWRfleet Home Energy VPP Platform | North America | Expanded PWRfleet VPP to 50,000 residential backup systems enrolled in grid services; Jan 2026. |

By DER Type

The distributed energy virtual power plant market by DER type spans battery energy storage systems, solar photovoltaic plus storage, demand response-enrolled loads, electric vehicle smart charging, and distributed generation including backup generators and fuel cells. Battery energy storage systems held the dominant DER type share at 36.8% of the distributed energy virtual power plant market in 2025, equivalent to approximately USD 1.57 Billion. BESS assets are preferred as VPP resources because of their bidirectional power flow capability, sub-second response time to dispatch signals, and ability to deliver both energy and ancillary services including frequency regulation, voltage support, and spinning reserve simultaneously. Behind-the-meter residential batteries including Tesla Powerwall, Enphase IQ, and Generac PWRcell provide 10-15 kWh per unit with 5-7.5 kW bidirectional power capability, enabling individual households to contribute 3-5 kW of net VPP capacity after local self-consumption requirements are met. Commercial and industrial battery systems of 100 kW to 10 MW scale provide larger individual contributions to utility VPP programs.

Solar PV plus storage combined DER assets represented 24.6% of the distributed energy virtual power plant market in 2025. The co-location of solar generation and battery storage on the same premises enables VPP platforms to optimize solar self-consumption during low-price periods, charge batteries from the grid during negative pricing events, and dispatch stored energy during peak demand windows, generating revenue from multiple market mechanisms simultaneously. Demand response-enrolled loads including smart thermostats, HVAC systems, water heaters, and commercial refrigeration held 18.4% of the market in 2025, representing the largest DER population by unit count though with lower per-asset revenue contribution than battery-based DERs. EV smart charging and vehicle-to-grid assets accounted for 12.6% of the market in 2025. Distributed generation including fuel cells, micro-turbines, and diesel backup generators in VPP programs represented the remaining 7.6%.

By Application

The distributed energy virtual power plant market by application covers ancillary services and frequency regulation, energy arbitrage and peak shaving, capacity market participation, demand response programs, and renewable energy integration and curtailment reduction. Ancillary services and frequency regulation held the dominant application share at 34.2% of the distributed energy virtual power plant market in 2025, equivalent to approximately USD 1.46 Billion. Grid frequency regulation is the highest-value ancillary service for VPP assets, with PJM's RegD signal requiring fast-ramping resources capable of 100% response within 4 seconds, a requirement that battery-based DEVPPs meet with sub-second response times versus conventional generators requiring 4-10 seconds. The economics of frequency regulation VPP programs are compelling: a 1 MW battery portfolio enrolled in PJM frequency regulation generates approximately USD 60,000-100,000 per year in market revenue at typical 2025 clearing prices, providing a revenue stream that materially improves the economics of customer battery investments.

Energy arbitrage and peak shaving represented 26.4% of the distributed energy virtual power plant market in 2025. VPP platforms optimize behind-the-meter battery charging and discharging schedules to minimize customer electricity bills through time-of-use rate arbitrage while simultaneously bidding available battery capacity into day-ahead energy markets. Capacity market participation, where aggregated DER capacity qualifies for capacity market auctions run by ISOs and RTOs, accounted for 18.6% of the market in 2025 and is growing rapidly as FERC Order 2222 implementation expands DER eligibility across US capacity market regions. Demand response programs held 14.2%, primarily serving utility programs that dispatch demand response events through the VPP platform to curtail load during grid stress events. Renewable energy integration and curtailment reduction represented the remaining 6.6%.

By Deployment Model

The distributed energy virtual power plant market by deployment model covers utility-operated VPP programs, third-party aggregator VPP platforms, technology vendor VPP-as-a-service, and government or grid operator-sponsored VPP programs. Utility-operated VPP programs held the largest deployment model share at 42.4% of the distributed energy virtual power plant market in 2025. Investor-owned utilities in California, New England, Australia, and Germany have each established utility-branded VPP programs that enroll residential and commercial customer DER assets, offering bill credits or revenue sharing to enrolled customers while operating the aggregated capacity as a grid management tool. Pacific Gas and Electric's Virtual Power Plant program, with over 150,000 enrolled residential assets by 2025, exemplifies the scale that utility-operated programs can achieve through customer bill channels and existing utility-customer relationships.

Third-party aggregator VPP platforms represented 32.6% of the distributed energy virtual power plant market in 2025, serving independent aggregators that enroll DER customer assets independently of utility programs and participate directly in wholesale market programs under FERC Order 2222 authorization. Technology vendor VPP-as-a-service models, where platform vendors operate VPP programs on behalf of utilities or aggregators through managed service contracts, held 18.4% of the market in 2025. Government and grid operator-sponsored VPP programs, including Australia's AEMO VPP Trial program and FERC-funded VPP demonstration projects, accounted for the remaining 6.6% of the distributed energy virtual power plant market by deployment model in 2025.

By End-User Type

The distributed energy virtual power plant market by end-user type covers residential DER owners, commercial and industrial customers, utilities and DSOs, and independent power producers and aggregators. Residential DER owners held the largest end-user share at 44.8% of the distributed energy virtual power plant market in 2025, reflecting the explosive growth of residential solar, battery storage, and EV ownership that provides the DER asset base enrolled in VPP programs. The average US residential VPP participant with solar and battery storage generates approximately USD 400-800 per year in bill savings and revenue sharing from VPP program enrollment, representing a meaningful ongoing return on the household's energy investment. Commercial and industrial customers represented 28.4% of the market in 2025, where larger individual DER assets per enrollment site generate higher VPP revenue contributions. Utilities and DSOs held 18.6% of the market, purchasing VPP platform software to operate programs. Independent power producers and aggregators represented the remaining 8.2%.

Regional Analysis

North America

North America distributed energy virtual power plant market held a 38.4% share in 2025, generating approximately USD 1.64 Billion in revenue. The United States is the dominant national market, where FERC Order 2222's wholesale market access mandate has created the regulatory foundation for commercial VPP operations at scale in every major ISO and RTO territory. California's Self-Generation Incentive Program, which has subsidized over 1,000 MW of behind-the-meter battery installations, and the California Public Utilities Commission's virtual net metering and DER aggregation tariffs create the densest residential VPP asset base of any US state, with CAISO's managed charging and demand response programs aggregating over 2 GW of enrolled DER capacity by 2025. New England ISO's Forward Capacity Market has cleared DER aggregations exceeding 500 MW in its most recent capacity auctions, validating VPP commercial viability in multi-asset capacity market participation. Texas ERCOT's market structure, which generates some of the most volatile spot electricity prices globally, creates exceptional energy arbitrage revenue for battery-based VPP programs, with commercial battery portfolios earning USD 150-300 per MWh during peak demand events. Canada contributes through Ontario's demand response programs and British Columbia's demand-side management VPP initiatives. Mexico is an emerging VPP market as its Federal Electricity Commission modernizes grid infrastructure and regulatory frameworks to accommodate DER participation.

Europe

Europe held approximately 28.6% of the global distributed energy virtual power plant market in 2025, generating approximately USD 1.22 Billion. Germany is the largest European national VPP market, where the Renewable Energy Sources Act's DER proliferation, the Federal Network Agency's balancing market access framework for aggregators, and major utility programs from E.ON, EnBW, and Vattenfall have created a sophisticated commercial VPP market. Germany's household battery storage fleet exceeded 1.5 Million units by 2025, providing the largest residential BESS VPP asset base in Europe. The EU Electricity Market Design Reform, adopted in 2024 and requiring member state implementation by 2026, mandates that national energy regulatory authorities enable DER aggregator access to all balancing and capacity markets, creating a binding regulatory market access commitment across 27 EU member states that will unlock EUR-denominated VPP revenue streams across continental Europe. The UK's Flexibility Markets and Contracts for Difference schemes have enabled significant VPP participation in frequency response and balancing markets, with National Grid ESO's Dynamic Containment and Dynamic Moderation services providing high-value ancillary service revenue for aggregated residential battery fleets. France, Netherlands, and the Nordic markets each represent growing VPP deployment environments where DSO flexibility procurement programs and retail TOU tariffs create VPP revenue opportunities.

Asia Pacific

Asia Pacific held approximately 22.4% of the global distributed energy virtual power plant market in 2025, generating approximately USD 959 Million. Australia is the most commercially advanced residential VPP market globally on a per-capita basis, where AEMO's DER Integration Program, the South Australian VPP demonstration involving Tesla Powerwalls, and state government battery subsidy programs have created a residential BESS VPP fleet exceeding 250,000 enrolled households by 2025. The National Electricity Market's Five Minute Settlement reform, implemented in 2021, created direct revenue incentives for fast-responding DER assets that VPP platforms can capture on behalf of enrolled customers. Japan is the second-largest Asia Pacific VPP market, where METI's Demand Response and Virtual Power Plant demonstration programs under the Green Innovation Fund are advancing commercial VPP deployment, and major utilities including TEPCO and Kansai Electric are testing residential battery aggregation for frequency regulation. South Korea's RE100 corporate renewable commitments and grid modernization programs are driving enterprise VPP adoption. China's large-scale DER deployment, including over 100 GW of distributed solar by 2025, creates enormous potential VPP capacity, with National Energy Administration pilot programs in multiple provinces testing DER aggregation frameworks that could unlock the world's largest VPP market by the early 2030s.

Latin America

Latin America held approximately 6.8% of the global distributed energy virtual power plant market in 2025, generating approximately USD 291 Million. Brazil is the dominant regional market, where ANEEL's distributed generation regulations and the country's prosumer framework allow behind-the-meter solar and storage owners to participate in demand response programs. Brazil's National System Operator ONS has been developing DER aggregation frameworks that could enable commercial VPP operations in the country's Interconnected System, and several state distribution utilities are piloting residential demand response programs with smart thermostat and water heater aggregation. Chile's competitive electricity market structure and growing commercial solar deployment create favorable conditions for third-party VPP aggregators, particularly in the competitive retail segment where time-of-use tariffs provide energy arbitrage incentives. Mexico's electricity reform landscape creates regulatory uncertainty for VPP development, though private sector DER investment continues to grow the behind-the-meter asset base that future VPP programs will aggregate. Colombia and Argentina represent secondary markets where deregulated electricity market structures are beginning to accommodate DER participation in ancillary service markets.

Middle East & Africa

The Middle East and Africa region held approximately 3.8% of the global distributed energy virtual power plant market in 2025, generating approximately USD 163 Million. The UAE is the most commercially active regional VPP market, where DEWA's Smart Grid strategy and Abu Dhabi's clean energy transition programs are developing regulatory frameworks for DER participation in grid balancing. Several commercial and industrial customers in Dubai are participating in early-stage demand response VPP programs that aggregate rooftop solar, battery storage, and HVAC systems for DSO flexibility services. Saudi Arabia's Vision 2030 energy transformation includes residential solar and storage deployment targets that will build the DER asset base for future VPP programs, with NEOM's fully renewable smart city infrastructure specifically designed for VPP operations from inception. South Africa leads the African VPP market, where load-shedding-driven residential and commercial battery storage adoption has created a large installed base of potential VPP assets, and Eskom's demand response programs are beginning to aggregate commercial DER capacity for grid balancing during generation shortfalls. Israel's advanced energy technology sector contributes VPP platform technology development that serves both domestic programs and international export markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By DER Type

- Battery Energy Storage Systems (BESS)

- Solar PV Plus Storage

- Demand Response-Enrolled Loads

- Electric Vehicle Smart Charging & V2G

- Distributed Generation (Fuel Cells, Generators)

By Application

- Ancillary Services & Frequency Regulation

- Energy Arbitrage & Peak Shaving

- Capacity Market Participation

- Demand Response Programs

- Renewable Energy Integration & Curtailment Reduction

By Deployment Model

- Utility-Operated VPP Programs

- Third-Party Aggregator VPP Platforms

- Technology Vendor VPP-as-a-Service

- Government & Grid Operator-Sponsored VPP Programs

By End-User Type

- Residential DER Owners

- Commercial & Industrial Customers

- Utilities & DSOs

- Independent Power Producers & Aggregators

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.28 B |

| Forecast Revenue (2034) | USD 17.86 B |

| CAGR (2025-2034) | 17.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By DER Type, (Battery Energy Storage Systems (BESS), Solar PV Plus Storage, Demand Response-Enrolled Loads, Electric Vehicle Smart Charging & V2G, Distributed Generation (Fuel Cells, Generators)), By Application, (Ancillary Services & Frequency Regulation, Energy Arbitrage & Peak Shaving, Capacity Market Participation, Demand Response Programs, Renewable Energy Integration & Curtailment Reduction), By Deployment Model, (Utility-Operated VPP Programs, Third-Party Aggregator VPP Platforms, Technology Vendor VPP-as-a-Service, Government & Grid Operator-Sponsored VPP Programs), By End-User Type, (Residential DER Owners, Commercial & Industrial Customers, Utilities & DSOs, Independent Power Producers & Aggregators) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | AUTOGRID SYSTEMS (SCHNEIDER ELECTRIC), SIEMENS ENERGY, ENBALA (STATKRAFT), VIRTUAL PEAKER, ENEL X (ENEL GROUP), TESLA ENERGY, FLUENCE ENERGY, LANDIS+GYR, ENPHASE ENERGY, GENERAC POWER SYSTEMS, SUNRUN, ITRON, OLIVINE INC., ORMAT TECHNOLOGIES, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Ancillary Services, Energy Arbitrage, Capacity Markets, Demand Response, Renewable Integration), By Deployment Model (Utility, Aggregator, VPP-as-a-Service) Industry Trends & Forecast 2026–2034")

, By Application (Ancillary Services, Energy Arbitrage, Capacity Markets, Demand Response, Renewable Integration), By Deployment Model (Utility, Aggregator, VPP-as-a-Service) Industry Trends & Forecast 2026–2034")

, By Application (Ancillary Services, Energy Arbitrage, Capacity Markets, Demand Response, Renewable Integration), By Deployment Model (Utility, Aggregator, VPP-as-a-Service) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Distributed Energy Virtual Power Plant Market?

Global Distributed Energy Virtual power plant market valued at USD 3.65B in 2024, reaching USD 17.86B by 2034, growing at a CAGR of 17.2% from 2026–2034.

Who are the major players in the Distributed Energy Virtual Power Plant Market?

AUTOGRID SYSTEMS (SCHNEIDER ELECTRIC), SIEMENS ENERGY, ENBALA (STATKRAFT), VIRTUAL PEAKER, ENEL X (ENEL GROUP), TESLA ENERGY, FLUENCE ENERGY, LANDIS+GYR, ENPHASE ENERGY, GENERAC POWER SYSTEMS, SUNRUN, ITRON, OLIVINE INC., ORMAT TECHNOLOGIES, OTHERS

Which segments covered the Distributed Energy Virtual Power Plant Market?

By DER Type, (Battery Energy Storage Systems (BESS), Solar PV Plus Storage, Demand Response-Enrolled Loads, Electric Vehicle Smart Charging & V2G, Distributed Generation (Fuel Cells, Generators)), By Application, (Ancillary Services & Frequency Regulation, Energy Arbitrage & Peak Shaving, Capacity Market Participation, Demand Response Programs, Renewable Energy Integration & Curtailment Reduction), By Deployment Model, (Utility-Operated VPP Programs, Third-Party Aggregator VPP Platforms, Technology Vendor VPP-as-a-Service, Government & Grid Operator-Sponsored VPP Programs), By End-User Type, (Residential DER Owners, Commercial & Industrial Customers, Utilities & DSOs, Independent Power Producers & Aggregators)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Distributed Energy Virtual Power Plant Market

Published Date : 24 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date