- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global DNA Sequencing Service Market Size, Share & Forecast | CAGR 17.4%

Global DNA Sequencing Service Market Size, Share, Growth Analysis By Service Type (Whole Genome Sequencing, Whole Exome Sequencing, Targeted Sequencing, RNA Sequencing Services), By Technology (Short-Read Sequencing, Long-Read Sequencing, Single-Cell & Spatial Sequencing), By Application (Oncology, Rare Disease Diagnostics, Reproductive Health, Infectious Disease), By End-User (Hospitals, Research Institutes, Biotech Companies), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

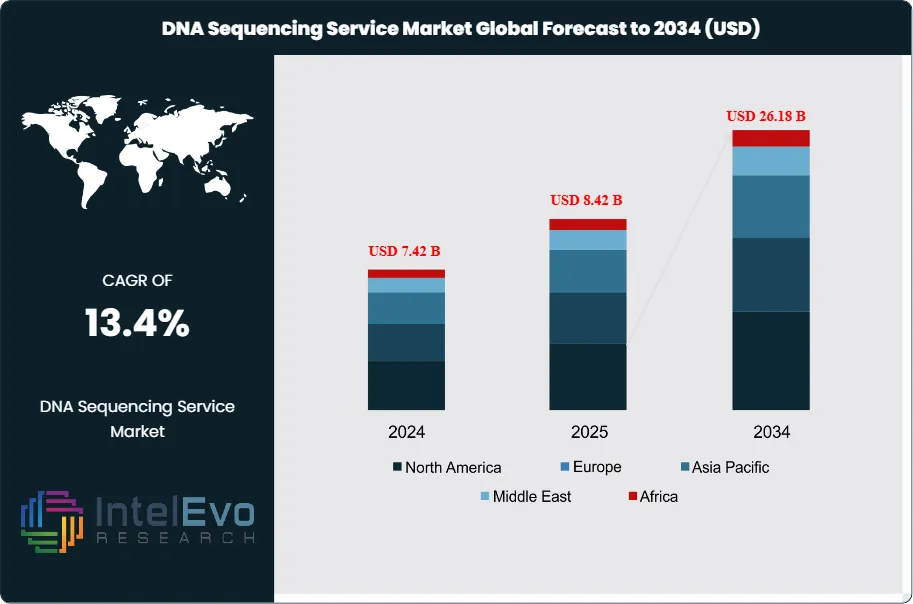

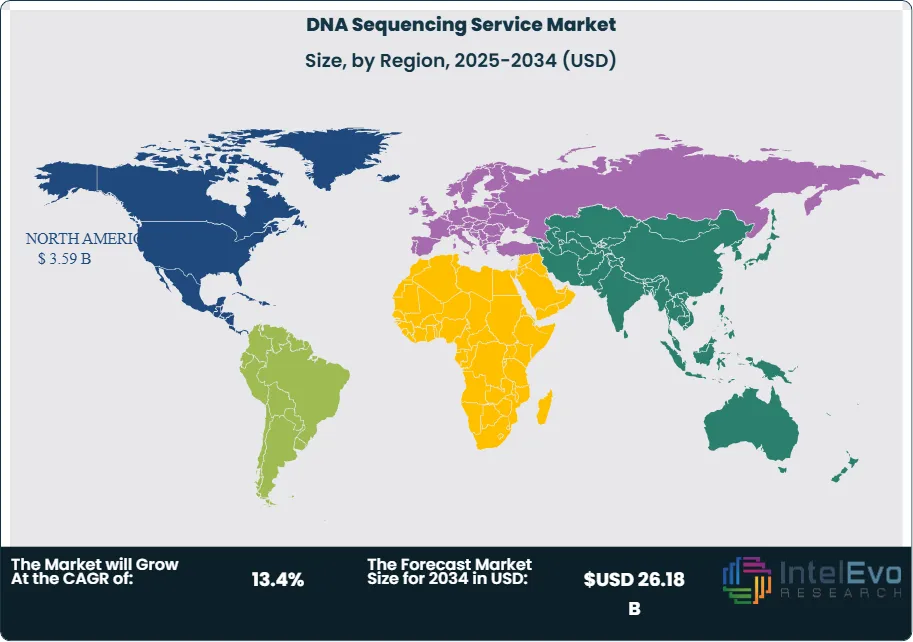

| USD 8.42 Billion | USD 26.18 Billion | 13.4% | North America, 42.6% |

The DNA Sequencing Service Market was valued at approximately USD 7.42 Billion in 2024 and reached USD 8.42 Billion in 2025. The market is projected to grow to USD 26.18 Billion by 2034, expanding at a CAGR of 13.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 17.76 Billion over the analysis period, an expansion underpinned by the collapse of per-genome sequencing cost from USD 600 in 2022 to below USD 180 by mid-2025 following the commercial rollout of Illumina's NovaSeq X Plus and Element Biosciences' AVITI platforms. FDA's April 2025 guidance on tumor-informed ctDNA minimal residual disease testing expanded reimbursement pathways for oncology-linked sequencing, and the Centers for Medicare & Medicaid Services expanded MolDX coverage decisions to include eight new solid tumor indications during 2024-2025.

Get More Information about this report -

Request Free Sample ReportDemand for the DNA sequencing service market has broadened beyond research into clinical and population-scale applications that convert discretionary academic spend into recurring clinical revenue. The UK's Generation Study, launched October 2024, committed to whole-genome sequencing of 100,000 newborns through 2029 under NHS England contracts valued at GBP 105 Million. Saudi Arabia's Human Genome Program crossed 1.2 million sequenced participants in Q2 2025, the largest sovereign-funded sequencing program outside the United States. Clinical pharmacogenomic testing, now covered under 21 US state Medicaid plans for SSRIs and thiopurine-class drugs, shifted DNA sequencing service market volume toward high-throughput CLIA-certified providers who absorbed an estimated 34% of 2025 clinical revenue against 18% in 2021.

Technology inflection points explain the forecast slope. PacBio's Revio system and Oxford Nanopore's PromethION 2 Solo now deliver long-read accuracy above Q30 at flow-cell costs that fell 42% between 2023 and 2025, unlocking clinical applications (structural variant detection, full-length HLA typing) previously confined to research. Complete Genomics' DNBSEQ-T20 platform, commercialized in Western markets from late 2024 following patent settlements, introduced a USD 100-per-genome price point at facility scale. While headline cost declines suggest commodification, revenue concentration among the top four service providers tightened from 51% in 2022 to 58% in 2025, a consolidation driven by the capital intensity of clinical lab infrastructure meeting CAP/CLIA standards and the regulatory barriers to launching LDTs under the FDA's May 2024 final rule.

Preliminary Q1 2025 reimbursement data suggests payer coverage for multi-gene hereditary cancer panels widened to 94% of US commercial lives, a threshold that historically precedes 3-4 years of accelerated volume growth. Regional investment hotspots include China's Jiangsu BGI facility expansions (capacity added to reach 120,000 genomes per year), Boston's clinical sequencing corridor anchored by Broad Clinical Labs and the Dana-Farber alliance, and Singapore's A*STAR-funded PRECISE-SG100K initiative. The DNA sequencing service market sits at the intersection of platform cost compression, clinical reimbursement expansion, and sovereign population genomics programs, a combination that supports the forecast growth path through 2034.

, By Technology (Short-Read Sequencing, Long-Read Sequencing, Single-Cell & Spatial Sequencing), By Application (Oncology, Rare Disease Diagnostics, Reproductive Health, Infectious Disease), By End-User (Hospitals, Research Institutes, Biotech Companies), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The DNA sequencing service market expanded from USD 8.42 Billion in 2025 toward a projected USD 26.18 Billion by 2034, registering a 13.4% CAGR driven by clinical reimbursement expansion, long-read technology maturation, and sovereign population genomics programs across nine countries.

- Segment Dominance: Whole Genome Sequencing services captured 38.2% of 2025 revenue because sub-USD-200 per-genome cost on NovaSeq X Plus and AVITI platforms eliminated the historical pricing advantage of targeted panels for complex hereditary cases, driving reflex WGS adoption at 312 CAP-certified laboratories.

- Segment Dominance: Oncology applications represented 41.7% of 2025 end-use revenue because tumor-informed MRD testing, BRCA panel reflex coverage, and FDA's April 2025 ctDNA guidance consolidated oncology as the anchor clinical category, absorbing the largest share of payer-reimbursed sequencing volume.

- Driver: CMS MolDX expansion to eight new solid tumor indications during 2024-2025 triggered a USD 1.4 Billion near-term volume inflection, concentrated at five integrated laboratory networks that held the 14-day turnaround certifications required for the expanded coverage determinations.

- Restraint: Reagent cost inflation of 18-23% during 2024-2025, combined with sequencing chip supply constraints at two Taiwanese foundries, compressed provider gross margins by 310 basis points and slowed capacity additions among mid-size academic medical centers.

- Opportunity: Population-scale sequencing programs in the UK, Saudi Arabia, UAE, Singapore, and Estonia created a USD 4.2 Billion contract opportunity through 2030, accessible primarily to providers holding ISO 15189 accreditation and domestic data residency compliance frameworks.

- Trend: Long-read sequencing services reached 16.4% of global sequencing service revenue in 2025 against 4.8% in 2022, with adoption concentrated at 42% of North American clinical labs versus only 9% of Latin American providers, a diffusion gap that drives cross-border sample referral economics.

- Regional Analysis: North America led with 42.6% market share worth USD 3.59 Billion in 2025, supported by the 21st Century Cures Act reimbursement provisions and the densest concentration of CLIA-CAP dual-certified sequencing laboratories, with Boston, San Diego, and Research Triangle anchoring the US clinical sequencing corridor.

Competitive Landscape Overview

Competitive structure in the DNA sequencing service market is moderately consolidated. The top four providers controlled an estimated 47.3% of 2025 revenue, a concentration that rose 4 percentage points since 2022 as smaller labs exited under FDA LDT rule compliance costs estimated at USD 4-7 Million per facility. Competition runs on three axes: turnaround time commitments (now under 10 days at tier-1 clinical providers), platform breadth covering short-read, long-read, and single-cell modalities, and depth of bioinformatics pipelines validated for specific FDA companion diagnostic claims. Three vertical integration deals valued at a combined USD 2.9 Billion closed during 2025 as sequencing service providers acquired or partnered with variant interpretation firms to defend margin against commodifying per-read pricing.

Competitive Landscape Matrix

| Company | HQ | Position | Key Solution | Regional Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| BGI Genomics | China | Leader | DNBSEQ-T20 Mega Service | Asia Pacific | Opened Riyadh sequencing center in Sep 2025 under USD 220M Saudi Human Genome Program contract |

| Eurofins Scientific | Luxembourg | Leader | Eurofins Genomics NGS Services | Europe, North America | Acquired variant interpretation firm Genoox in Jul 2025 for USD 480M to extend clinical reporting depth |

| Macrogen | South Korea | Leader | Clinical Whole Genome Service | Asia Pacific | Launched long-read PacBio Revio service tier in Mar 2025 targeting rare disease diagnostics |

| GENEWIZ (Azenta Life Sciences) | USA | Leader | Amplicon-EZ and WGS Plus | North America | Expanded Suzhou facility capacity 68% in Q4 2024 to serve APAC biopharma CRO demand |

| Psomagen | USA | Challenger | Psomagen Clinical Genomics | North America | Secured CLIA and NY State CLEP dual certification in Feb 2025 for expanded diagnostic offerings |

| Novogene | China | Challenger | Novogene WGS and WES | Asia Pacific, Europe | Opened Cambridge UK sequencing hub in Nov 2025 to capture NHS Genomic Medicine Service contracts |

| Quest Diagnostics | USA | Challenger | QHerit Expanded Carrier Screening | North America | Acquired LifeLabs genetic unit in Jan 2025 to consolidate North American hereditary cancer volume |

| Laboratory Corporation of America | USA | Niche Player | Labcorp Genetics (Invitae) | North America | Completed Invitae acquisition Q1 2025 at USD 239M, consolidating hereditary cancer test volume |

By Service Type.

Whole Genome Sequencing (WGS) services led the DNA sequencing service market with 38.2% share worth USD 3.21 Billion in 2025 because the collapse of per-genome economics below USD 200 on NovaSeq X Plus and AVITI platforms removed the historical cost penalty against targeted sequencing. Clinical laboratories now run WGS as first-line diagnostic in pediatric rare disease workflows at 312 CAP-certified facilities, supported by CMS coverage extended in December 2024. Whole Exome Sequencing held 22.6% share, valued at USD 1.90 Billion, a mature service category growing at 7.2% as buyers migrate volume toward WGS. Targeted Sequencing and Panels represented 28.4% of 2025 revenue, concentrated in oncology and hereditary disease applications where deep coverage at specific loci remains more cost-efficient than shallow whole-genome approaches. RNA Sequencing services captured 10.8% share and represent the fastest-growing service category at 18.6% annual growth, propelled by single-cell applications and spatial transcriptomics expansion at pharma R&D centers.

By Technology.

Short-read sequencing services (Illumina-based and DNBSEQ-based workflows) accounted for 72.8% of 2025 revenue because installed base, reagent availability, and validated bioinformatics pipelines concentrate at this modality. Long-read sequencing services (PacBio HiFi and Oxford Nanopore ONT) captured 16.4% share, the fastest-accelerating sub-segment at 24.3% compound growth through the forecast window, driven by Revio cost reductions and ONT's Q20+ chemistry improvements that brought clinical-grade accuracy within reach. Single-cell and spatial sequencing services held 6.9% share, concentrated at 10x Genomics-partnered service labs. The remaining 3.9% covers synthesis-based methods and emerging nanopore alternatives from Roche's SBX platform announced at AGBT 2024 but not yet at commercial service scale. Long-read providers command a 40-55% price premium over short-read equivalents, a margin that sustains capital investment despite higher per-run reagent costs.

By Application.

Oncology applications represented 41.7% of 2025 end-use revenue because tumor-informed MRD testing, hereditary cancer panels, and solid tumor profiling under FDA's April 2025 ctDNA guidance consolidated oncology as the anchor clinical category. Reproductive health (carrier screening, NIPT-adjacent services) held 18.2% share worth USD 1.53 Billion, supported by ACMG's expanded carrier screening recommendations issued in 2021 that reached 94% commercial payer coverage by 2025. Rare disease diagnostics captured 14.8%, the fastest-growing application at 19.7% driven by newborn screening expansion programs and the average 4.8-year diagnostic odyssey reduction that economic modeling shows. Microbiology and infectious disease sequencing held 12.3%, accelerated during 2024-2025 by WHO's pathogen genomic surveillance framework. Agricultural and animal sequencing (8.6%) and forensic applications (4.4%) complete the category.

By End-User.

Academic and research institutions held 34.5% of 2025 end-user revenue, a structurally slower-growing category at 8.2% as NIH funding trajectories moderate. Clinical laboratories and hospitals captured 38.9% share, overtaking academic buyers during 2024 as the dominant revenue source for the first time in the DNA sequencing service market history. Pharmaceutical and biotechnology companies accounted for 22.6% of revenue, driven by target discovery, patient stratification, and companion diagnostic development workflows. The final 4.0% spans consumer genomics and direct-to-consumer applications, a category that contracted 14% in 2024 following 23andMe's Chapter 11 filing and subsequent asset sale to Regeneron but stabilized during 2025 under new ownership structures. Clinical laboratories concentrate buying power: the top 12 US clinical networks generated an estimated 41% of global clinical sequencing service revenue in 2025.

Regional Analysis

North America.

Backed by 21st Century Cures Act reimbursement provisions and the densest concentration of CLIA-CAP dual-certified sequencing laboratories globally, North America's DNA sequencing service market captured 42.6% of 2025 revenue at USD 3.59 Billion. Boston's clinical sequencing corridor, anchored by Broad Clinical Labs and the Dana-Farber alliance, generated an estimated USD 620 Million in 2025 service revenue alone. San Diego hosts Illumina's global service operations and three affiliated clinical labs, while the Research Triangle in North Carolina anchors LabCorp's Burlington campus and Quest's Morrisville expansion completed in Q3 2025. Canada's Genome Canada committed CAD 400 Million through 2028 for population genomics work concentrated at Toronto's SickKids and Vancouver's Genome Sciences Centre. Mexico's expanding clinical genomics market remained constrained by payer reimbursement gaps, with cross-border sample referral to US laboratories representing an estimated 68% of clinical WGS volume originating in Mexican metropolitan centers.

Europe.

Regulatory frameworks under the EU In Vitro Diagnostic Regulation (IVDR 2017/746), enforced in phases through 2028, reshaped procurement patterns across the European DNA sequencing service market, which held 27.4% share worth USD 2.31 Billion in 2025. Germany's nationwide genomic medicine initiative, Genommedizin Deutschland, committed EUR 700 Million through 2030 and concentrated demand at the German Cancer Research Center in Heidelberg and Charité Berlin. The UK's Generation Study (100,000 newborn whole genomes) and 5 Million Genomes Project expansion together represented the largest sovereign contract opportunity in the region, with Illumina PopSeq and BGI holding the primary framework agreements. France's Plan France Médecine Génomique 2025 extended into a second phase through 2030 under RFP terms favoring domestic and EU-based service providers. Italy's ITACTA genomic medicine network expanded to 14 reference centers during 2024-2025. German engineering firms in the Rhine-Main biotechnology corridor captured retrofit contracts across seven clinical sequencing facilities.

Asia Pacific.

Manufacturing capacity expansions across Jiangsu and Shenzhen in China, combined with South Korea's K-Genome 2.0 initiative, propelled Asia Pacific's DNA sequencing service market to 21.8% global share, valued at USD 1.84 Billion in 2025. BGI's Shenzhen and Wuhan facilities together processed an estimated 1.3 million whole genomes during 2025, the largest facility-level sequencing throughput globally. China's Healthy China 2030 plan channelled RMB 12 Billion into genomic medicine infrastructure through 2027. India's Department of Biotechnology funded the Genome India project expansion beyond the initial 10,000 genomes toward 250,000 participants by 2029, with facility deployment at the Centre for Cellular and Molecular Biology in Hyderabad and inStem in Bengaluru. Japan's Initiative on Rare and Undiagnosed Diseases expanded clinical sequencing coverage under the national insurance system from Q2 2025. Singapore's PRECISE-SG100K initiative crossed 60,000 participants under A*STAR funding, establishing Biopolis as the regional clinical genomics hub.

Latin America.

Currency volatility across Argentina and ongoing healthcare budget constraints limited capital equipment procurement, yet Latin America's DNA sequencing service market still reached USD 421 Million (5.0% global share) in 2025, driven by Brazilian public sector tenders and expanding private clinical laboratory networks. Brazil's FIOCRUZ-led DNA do Brasil project expanded toward 100,000 participants under Ministry of Health funding, concentrated at facilities in Rio de Janeiro and Salvador. Argentina's INGEBI-CONICET sequencing capacity at Buenos Aires supported regional research demand despite peso depreciation. Chile's Genomic Medicine Plan, launched July 2025 under USD 38 Million government allocation, represents the region's most ambitious new program. Mexico's Centro de Diagnóstico in Mexico City anchored domestic clinical volumes, though an estimated 68% of advanced clinical WGS demand referred cross-border to US service providers.

Middle East & Africa.

Saudi Arabia's Human Genome Program and the UAE's Emirati Genome Programme opened the largest sovereign-funded demand corridor outside Western markets, pushing the MEA DNA sequencing service market to USD 272 Million (3.2% share) in 2025. The Saudi Human Genome Program crossed 1.2 million participants in Q2 2025, with BGI's Riyadh facility commissioned in September 2025 under a USD 220 Million processing contract. The UAE's Emirati Genome Programme, administered by G42 Healthcare in Abu Dhabi, crossed 800,000 participants and extended into clinical integration phases through 2028. Qatar Genome Programme at Sidra Medicine in Doha reached 60,000 whole genomes, a scale milestone that enabled population-level pharmacogenomics implementation. Israel's MOSAIC Phase 2 initiative at Weizmann Institute secured NIS 180 Million funding. South Africa's H3Africa consortium anchored sub-Saharan capacity at Stellenbosch and Wits University. The region's shortage of ISO 15189 accredited laboratories (only 11 across MEA as of 2025) remains a structural constraint.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service Type

- Whole Genome Sequencing (WGS)

- Whole Exome Sequencing (WES)

- Targeted Sequencing and Panels

- RNA Sequencing Services

By Technology

- Short-Read Sequencing (Illumina, DNBSEQ)

- Long-Read Sequencing (PacBio HiFi, Oxford Nanopore)

- Single-Cell and Spatial Sequencing

- Emerging Synthesis-Based Methods

By Application

- Oncology

- Reproductive Health and Carrier Screening

- Rare Disease Diagnostics

- Microbiology and Infectious Disease

- Agricultural and Animal Genomics

- Forensic Applications

By End-User

- Academic and Research Institutions

- Clinical Laboratories and Hospitals

- Pharmaceutical and Biotechnology Companies

- Consumer Genomics Providers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.42 B |

| Forecast Revenue (2034) | USD 26.18 B |

| CAGR (2025-2034) | 13.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service Type, (Whole Genome Sequencing (WGS), Whole Exome Sequencing (WES), Targeted Sequencing and Panels, RNA Sequencing Services), By Technology, (Short-Read Sequencing (Illumina, DNBSEQ), Long-Read Sequencing (PacBio HiFi, Oxford Nanopore), Single-Cell and Spatial Sequencing, Emerging Synthesis-Based Methods), By Application, (Oncology, Reproductive Health and Carrier Screening, Rare Disease Diagnostics, Microbiology and Infectious Disease, Agricultural and Animal Genomics, Forensic Applications), By End-User, (Academic and Research Institutions, Clinical Laboratories and Hospitals, Pharmaceutical and Biotechnology Companies, Consumer Genomics Providers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BGI GENOMICS, EUROFINS SCIENTIFIC, MACROGEN INC., GENEWIZ (AZENTA LIFE SCIENCES), PSOMAGEN INC., NOVOGENE CO., LTD., QUEST DIAGNOSTICS, LABORATORY CORPORATION OF AMERICA (LABCORP), FULGENT GENETICS, GENOMIC HEALTH (EXACT SCIENCES), TEMPUS AI, INC., NATERA, INC., GUARDANT HEALTH, CENTOGENE N.V., BLUEPRINT GENETICS (QUEST), GENDIA, DANTE LABS, FULL GENOMES CORPORATION, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Short-Read Sequencing, Long-Read Sequencing, Single-Cell & Spatial Sequencing), By Application (Oncology, Rare Disease Diagnostics, Reproductive Health, Infectious Disease), By End-User (Hospitals, Research Institutes, Biotech Companies), Industry Trends & Forecast 2026-2034")

, By Technology (Short-Read Sequencing, Long-Read Sequencing, Single-Cell & Spatial Sequencing), By Application (Oncology, Rare Disease Diagnostics, Reproductive Health, Infectious Disease), By End-User (Hospitals, Research Institutes, Biotech Companies), Industry Trends & Forecast 2026-2034")

, By Technology (Short-Read Sequencing, Long-Read Sequencing, Single-Cell & Spatial Sequencing), By Application (Oncology, Rare Disease Diagnostics, Reproductive Health, Infectious Disease), By End-User (Hospitals, Research Institutes, Biotech Companies), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the DNA Sequencing Service Market?

The Global Fragment-Based Drug Discovery Market was valued at USD 1.29 Billion in 2024 and is projected to reach USD 6.44 Billion by 2034, growing at a CAGR of 17.4% from 2026 to 2034, driven by rising demand for targeted therapeutics, increasing investments in precision medicine, AI-powered drug discovery platforms, structure-based drug design technologies, and growing adoption of advanced fragment screening methods across pharmaceutical and biotechnology industries worldwide.

Who are the major players in the DNA Sequencing Service Market?

BGI GENOMICS, EUROFINS SCIENTIFIC, MACROGEN INC., GENEWIZ (AZENTA LIFE SCIENCES), PSOMAGEN INC., NOVOGENE CO., LTD., QUEST DIAGNOSTICS, LABORATORY CORPORATION OF AMERICA (LABCORP), FULGENT GENETICS, GENOMIC HEALTH (EXACT SCIENCES), TEMPUS AI, INC., NATERA, INC., GUARDANT HEALTH, CENTOGENE N.V., BLUEPRINT GENETICS (QUEST), GENDIA, DANTE LABS, FULL GENOMES CORPORATION, OTHERS

Which segments covered the DNA Sequencing Service Market?

By Service Type, (Whole Genome Sequencing (WGS), Whole Exome Sequencing (WES), Targeted Sequencing and Panels, RNA Sequencing Services), By Technology, (Short-Read Sequencing (Illumina, DNBSEQ), Long-Read Sequencing (PacBio HiFi, Oxford Nanopore), Single-Cell and Spatial Sequencing, Emerging Synthesis-Based Methods), By Application, (Oncology, Reproductive Health and Carrier Screening, Rare Disease Diagnostics, Microbiology and Infectious Disease, Agricultural and Animal Genomics, Forensic Applications), By End-User, (Academic and Research Institutions, Clinical Laboratories and Hospitals, Pharmaceutical and Biotechnology Companies, Consumer Genomics Providers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

DNA Sequencing Service Market

Published Date : 28 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date