- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Downhole Tools Market Size, Share & Growth Analysis | CAGR 4.9%

Global Downhole Tools Market Size, Share, Analysis By Tool Type (Downhole Control Tools, Drilling Tools, Flow and Pressure Control Tools, Handling Tools and Others), By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Landscape, Technology Innovations, Strategic Developments, Investment Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 5.18 Billion, 2025 | USD 7.97 Billion, 2034 | 4.9%, 2026–2034 | North America, 34.9%, 2025 |

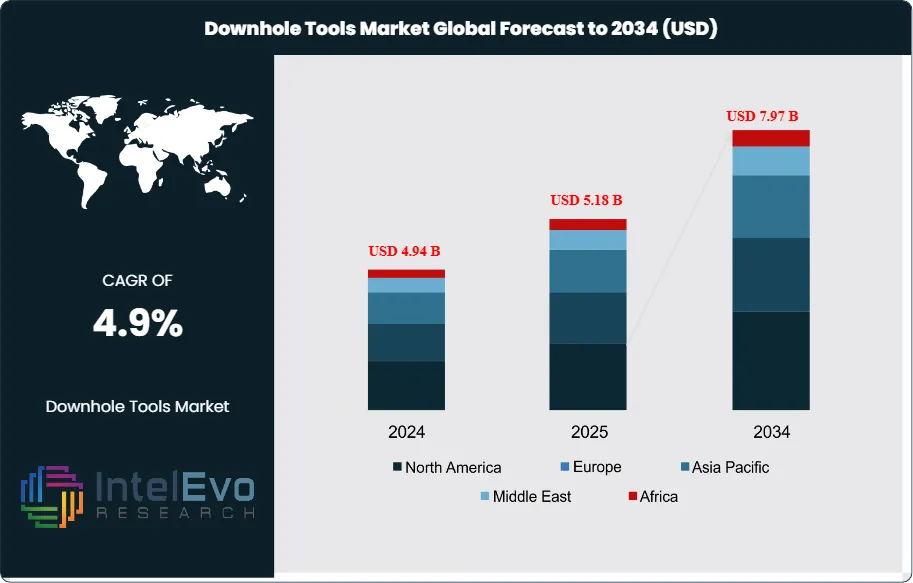

The Downhole Tools Market was valued at approximately USD 4.94 Billion in 2024 and increased to USD 5.18 Billion in 2025. The market is projected to reach nearly USD 7.97 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 4.9% during the forecast period from 2026 to 2034. The Downhole Tools Market is expanding because operators need higher drilling accuracy, tighter wellbore control, lower non-productive time, and better recovery from mature and complex reservoirs. Grand View Research places the market at USD 5.18 Billion in 2025, identifies North America as the largest region with 34.9% share in 2025, and shows downhole control tools as the largest tool category. It also identifies drilling as the leading application in 2025.

Get More Information about this report -

Request Free Sample ReportThe Downhole Tools Market is being shaped by two field realities. First, drilling programs remain technically demanding across shale, offshore, and deeper conventional wells. Second, mature fields still need completion, intervention, and production-support tools to hold output and improve well economics. Grand View notes that rising exploration and production activity, stronger demand for efficient drilling and completion, and the need to maximize recovery from complex and mature reservoirs are the main growth drivers. The same source also points to stronger use of MWD/LWD systems, rotary steerable systems, drilling motors, reamers, and flow and pressure control tools to improve real-time decisions and reduce operational risk.

Technology is moving the Downhole Tools Market toward smarter, data-linked tools rather than purely mechanical hardware. SLB launched the Retina at-bit imaging tool in May 2025 and the OnWave autonomous logging platform in 2025, both aimed at faster and higher-quality downhole data acquisition. Halliburton launched the SmartWell Turing electro-hydraulic control system in September 2025 and the StreamStar wired drill pipe interface system in October 2025 to improve reservoir flow control and real-time downhole power and data transfer. These launches show that digitalization, automation, and better downhole sensing are now central to product differentiation.

Regional demand remains uneven. North America leads because of shale intensity, service density, and sustained drilling and completion activity. Asia Pacific is the fastest-growing region in Grand View’s outlook, supported by rising exploration activity and stronger demand from China, India, Japan, and South Korea. Fortune Business Insights also points to strong Asia Pacific momentum, with China at USD 0.57 Billion in 2025 and Asia Pacific reaching USD 1.15 Billion in 2025 in its regional view. Risks remain real. The IEA expects upstream oil investment to fall 6% in 2025, and Reuters reported weaker 2025 drilling demand in North America and parts of the Middle East for Halliburton. That combination limits discretionary tool spending, especially in price-sensitive land markets, even though long-cycle offshore and production-support work remains more resilient.

, By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Landscape, Technology Innovations, Strategic Developments, Investment Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Downhole Tools Market stood at USD 5.18 Billion in 2025 and is projected to reach USD 7.97 Billion by 2034 at a 4.9% CAGR over 2026–2034.

- Segment Dominance: Downhole control tools led the market with a 30.2% share in 2025, equal to about USD 1.56 Billion, 2025.

- Segment Dominance: Drilling applications led with a 33.1% share in 2025, equal to about USD 1.71 Billion, 2025.

- Driver: The main driver is the need to improve drilling efficiency and well performance in complex reservoirs, supported by stronger use of MWD/LWD, rotary steerable systems, and drilling motors.

- Restraint: The main restraint is lower upstream spending and softer drilling demand in some markets. The IEA expects upstream oil investment to fall 6.0% in 2025, while Halliburton’s North America revenue fell 9.0% year over year in Q2 2025.

- Opportunity: The strongest opportunity sits in offshore and intelligent completion workflows. The offshore segment is the fastest-growing deployment area, while new intelligent control systems are increasing value per well.

- Trend: The dominant trend is smarter, sensor-rich downhole tools. SLB says the OnWave platform takes less than half the time to deploy compared with conventional wireline platforms, while Halliburton’s StreamStar adds continuous downhole power and high-speed data transmission.

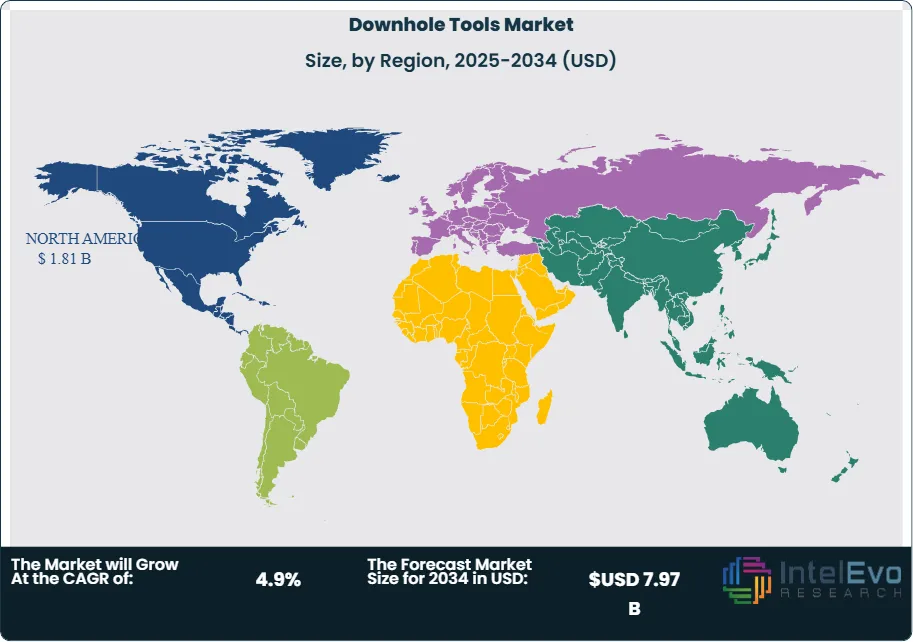

- Regional Analysis: North America led the Downhole Tools Market with a 34.9% share in 2025, equal to about USD 1.81 Billion, 2025.

Competitive Summary

The Downhole Tools Market is moderately consolidated. The top four companies, SLB, Halliburton, Baker Hughes, and Weatherford, accounted for an estimated 48.0% of 2025 market revenue. Competition is mainly technology-driven and geographic. Leaders win where drilling performance, intelligent completions, real-time downhole data, and global field support matter most. Competitive intensity increased in 2025–2026 through SLB’s Retina and OnWave launches, Halliburton’s Turing and StreamStar releases, Weatherford’s multi-year completions and wireline awards, and NOV’s integrated bottomhole assembly push.

Competitive Landscape Matrix

| Company | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| SLB | US | Leader | Retina at-bit imaging / OnWave autonomous logging | North America, Middle East, Latin America | Launched Retina in May 2025 and OnWave in 2025, expanding advanced downhole imaging and autonomous logging capabilities. |

| Halliburton | US | Leader | SmartWell Turing / StreamStar wired drill pipe | North America, Middle East, Europe | Launched SmartWell Turing in Sep 2025 and StreamStar in Oct 2025 to improve reservoir flow control and real-time downhole data transfer. |

| Baker Hughes | US | Leader | DirectKNCT PDC drill bit technology | North America, Middle East, Asia Pacific | Continued rollout of DirectKNCT in 2025 and highlighted major integrated well construction awards with drill bits, wireline, and completions scope. |

| Weatherford | US | Leader | Integrated Completions Solutions / autonomous inflow control device screens | Middle East, Asia Pacific, Latin America | Reported multiple 2025 awards, including a 3-year Turkmenistan completions contract and Jadestone Malaysia lower completions scope. |

| NOV | US | Challenger | ReedHycalog drill bits and integrated BHA | North America, Middle East | Reported in Q1 2025 that integrated BHAs using drill bits, motors, and MWD were being supplied to customers, supporting market share gains. |

| Oil States International | US | Challenger | Downhole perforation systems and completion tools | North America, Offshore International | Continued expanding downhole technologies and offshore deployments through 2025, with advanced offshore technology adoption noted in company disclosures. |

| TechnipFMC | UK | Challenger | IWOCS and well access systems | Europe, Latin America, Middle East | Continued 2025 rollout of hybrid flexible and subsea access technologies tied to intervention and completion work. |

| Hunting PLC | UK | Niche Player | TCP hardware, setting tools, MWD/LWD components | Europe, Middle East | Reported $17.5 million acquisition of Organic Oil Recovery Technology in Mar 2025 and later exited Rival Downhole in 2026 restructuring commentary. |

| Rubicon Oilfield International | US | Niche Player | Completion and intervention downhole tools | North America | Continued North America tool exposure through 2025 and remained a recognized market participant. |

| United Drilling Tools | India | Niche Player | Downhole drilling and handling tools | Asia Pacific, Middle East | Continued participation as a recognized global supplier in 2025 market listings and regional tool demand growth. |

By Tool Type

Downhole control tools held the largest share of the Downhole Tools Market at 30.2% in 2025, equal to about USD 1.56 Billion, 2025. The segment is gaining from rising demand for wellbore stability, pressure regulation, zonal control, and higher operational control during drilling and completion. This is where intelligent completions, inflow control devices, safety valves, and reservoir flow management systems sit. Halliburton’s SmartWell Turing launch in September 2025 directly supports this trend, as it targets remote control and monitoring of reservoir zones. Weatherford’s integrated completion solutions and 2025 completions contracts in Turkmenistan and Malaysia also point to stronger commercial demand for these tools. Competitive intensity is highest among Halliburton, Weatherford, Baker Hughes, and SLB because customers value field reliability, control precision, and compatibility with broader completion architectures. This segment should remain the largest through 2034 because it benefits from both new well completions and mature-field production optimization.

Drilling tools accounted for an estimated 27.0% share in 2025, equal to about USD 1.40 Billion, 2025. This segment includes drill bits, motors, reamers, stabilizers, jars, and related BHA components. It remains central to market demand because drilling intensity still drives the largest application share globally. Drilling accounted for 33.1% of total application revenue in 2025, which supports sustained demand for drilling-focused downhole tools. SLB’s Retina launch, NOV’s integrated BHA supply commentary, and Baker Hughes’ DirectKNCT PDC bit technology all show that tool suppliers are competing on rate of penetration, formation evaluation quality, and lower non-productive time. The segment is highly technology-driven, especially in shale, offshore, and extended-reach wells where tool failure or slow penetration quickly raises total well cost. Drilling tools will remain a major revenue pool through 2034, but growth will track rig activity and upstream spending more closely than completion and control categories.

Flow and pressure control tools represented an estimated 23.0% share in 2025, or about USD 1.19 Billion, 2025. This segment covers valves, pressure control devices, circulation tools, and flow management equipment used during drilling, completion, production, and intervention. Demand is strongest where operators need tighter control over pressure windows, fluid movement, and well integrity in difficult formations. The segment benefits from both offshore growth and higher completion complexity. Halliburton’s StreamStar wired drill pipe interface system, which adds continuous downhole power and high-speed data, supports better pressure and drilling control in automated workflows. TechnipFMC’s well access and intervention control systems also sit close to this space in subsea environments. The segment is smaller than downhole control tools, but it is becoming more important as operators push deeper, hotter, and higher-pressure wells. Growth should remain solid through 2034, particularly in offshore and high-spec completions work.

Handling tools and other tool categories held the remaining estimated 19.8% share in 2025, or about USD 1.03 Billion, 2025. This segment includes running tools, fishing tools, retrieval hardware, and auxiliary downhole equipment used across drilling, completion, and intervention. Revenue is more fragmented here because many specialized manufacturers compete basin by basin or job by job. Even so, these tools remain essential because they support the safe execution of larger downhole operations and help reduce rig time when failures or retrieval needs arise. Hunting, Oil States, United Drilling Tools, and multiple regional suppliers remain active in this segment. The growth outlook is moderate rather than exceptional, but the segment stays relevant because every increase in drilling and completion complexity raises the importance of tool handling, reliability, and recovery support.

By Application

Drilling was the largest application segment with 33.1% share in 2025, equal to about USD 1.71 Billion, 2025. This segment leads because drilling operations require the broadest mix of bits, motors, reamers, sensors, steering tools, and BHA components. It also benefits most directly from digitalization, because the commercial value of real-time downhole data is highest while drilling is active. SLB’s Retina at-bit imaging, Halliburton’s StreamStar, and NOV’s integrated BHA activity all support this segment. North America remains the main demand center because shale and unconventional drilling rely heavily on tool performance, while offshore markets create higher value per tool run. The segment should keep its leadership through 2034, although growth may moderate if rig activity softens in lower-price environments.

Completion accounted for an estimated 24.0% share in 2025, or about USD 1.24 Billion, 2025. This segment includes intelligent completions, sand control tools, packers, safety valves, inflow control devices, and related completion hardware. It is gaining strategic importance because operators increasingly want higher recovery, zonal management, and better long-term control over water, gas, and pressure movement. Halliburton’s SmartWell Turing launch and Weatherford’s multiple completions-related contracts show that the commercial focus is moving toward more connected and controllable completion systems. Completion demand is especially strong in offshore assets, long laterals, and mature wells where production management matters more than simple initial installation. Competitive intensity is high because customers demand reliability, lower intervention needs, and compatibility with broader field architectures. The segment should outpace some drilling-linked categories in value-added terms through 2034.

Intervention and production together represented an estimated 29.0% share in 2025, equal to about USD 1.50 Billion, 2025. These applications rely on downhole tools for workovers, monitoring, flow control, completion repair, and production optimization. Demand is strongest in mature reservoirs, brownfield offshore assets, and high-value wells where restoring or stabilizing flow justifies tool-intensive work. Weatherford’s wireline, completions, and mechanized systems awards in 2025 show how active this space remains. Oil States and TechnipFMC also participate where offshore intervention and completion control systems overlap. This segment benefits from longer field life and the industry’s need to extract more value from installed infrastructure. Growth should remain steady through 2034, supported by mature-field economics and late-life asset management.

Formation evaluation held an estimated 13.9% share in 2025, or about USD 0.72 Billion, 2025. The segment is smaller in revenue than drilling or completion, but it is highly technology-rich and strategically important. It includes logging and evaluation tools that help operators understand formation properties, reduce uncertainty, and improve placement and completion design. SLB’s Retina and OnWave launches both reinforce the commercial relevance of evaluation tools. The segment benefits from deeper wells, harsher environments, and stronger demand for real-time, cable-free, and autonomous measurement systems. It will remain smaller in absolute revenue than drilling, but it should record healthy growth through 2034 because better evaluation improves the economics of every later well decision.

By Location of Deployment

Onshore dominated the Downhole Tools Market with an estimated 72.0% share in 2025, equal to about USD 3.73 Billion, 2025. This structure is consistent with the broad concentration of global drilling and completion activity on land, especially in North America, the Middle East, China, India, and Latin America. Onshore demand is driven by shale, tight reservoirs, mature conventional wells, and the large number of wells drilled and serviced each year. It is also the most competitive part of the market because many regional and global suppliers can participate. Drilling tools, control tools, and completion tools all see high turnover in this segment. North America’s 34.9% global market share in 2025 is heavily tied to land activity. The onshore segment will remain dominant through 2034, although pricing and margins will remain more sensitive to drilling cycles than in offshore work.

Offshore held an estimated 28.0% share in 2025, or about USD 1.45 Billion, 2025. The offshore segment is expected to grow at the fastest pace, supported by rising efforts to locate reserves offshore and the need for robust tools in harsh and remote environments. Offshore jobs are fewer in count than onshore jobs, but revenue per tool run is higher because failure risk, logistics, and tool complexity are greater. TechnipFMC’s well access systems, Halliburton’s completion control systems, and Weatherford’s offshore completions awards show why offshore remains a premium segment. Brazil, the Gulf of Mexico, the North Sea, the Middle East, and parts of Asia Pacific anchor this demand. Offshore should gain share gradually through 2034 because deeper reservoirs, subsea systems, and brownfield intervention all require higher-spec downhole equipment.

Regional Analysis

North America Downhole Tools Market

North America held 34.9% of the Downhole Tools Market in 2025, equal to about USD 1.81 Billion, 2025. The region leads because it combines the largest shale and unconventional drilling base with dense oilfield service infrastructure and fast adoption of advanced tools. The United States is the core market. It benefits from shale drilling, long laterals, hydraulic fracturing support, and higher use of MWD/LWD, drill bits, reamers, and completion control systems. Canada remains important through oil sands, deep land basins, and cold-weather drilling and workover requirements. Mexico adds strategic offshore value through Gulf activity and field redevelopment. North America also hosts most of the leading global suppliers, including SLB, Halliburton, Baker Hughes, NOV, Oil States, and Weatherford. The main risk is cyclical drilling weakness. Halliburton’s North America revenue fell 9% year over year in Q2 2025 as drilling softened. Even so, North America should remain the largest regional market through 2034 because tool intensity per well remains high and customers here adopt new tool technologies faster than most other regions.

Europe Downhole Tools Market

Europe accounted for an estimated 16.5% share in 2025, equal to about USD 0.85 Billion, 2025. The region is smaller than North America in total well count, but it remains a high-value market because of offshore complexity, mature field redevelopment, and strict operating standards. The UK and Norway dominate demand through North Sea drilling, completions, intervention, and well access systems. Germany is smaller and more engineering-oriented, while France has limited upstream scale but remains part of regional technology and service networks. Europe benefits from strong demand for offshore and subsea downhole tools, especially in completion, flow control, and intervention-related categories. TechnipFMC, Halliburton, SLB, and Hunting are especially relevant here. Europe’s regulatory environment raises compliance demands, but it also supports higher-spec equipment and better reliability standards. The region is less about volume and more about tool value per deployment. Growth will remain moderate through 2034, supported by brownfield optimization, subsea operations, and later-life field management.

Asia Pacific Downhole Tools Market

Asia Pacific held an estimated 26.0% share in 2025, equal to about USD 1.35 Billion, 2025. The region is rising because governments and operators are investing in both conventional and unconventional reserves to improve energy security. China is the largest country market, supported by large domestic drilling activity and growing use of advanced downhole equipment. India is expanding through exploration and production spending and a stronger focus on well efficiency. Japan is smaller in hydrocarbon activity, but it remains regionally relevant in technology and service networks. Australia is strategically relevant for offshore and unconventional demand in practical market terms. Asia Pacific benefits from both onshore and offshore activity, with stronger demand for drilling tools, control tools, and completion systems. The region should gain share through 2034 because it combines expanding energy demand with a still-rising adoption curve for higher-spec downhole technology.

Latin America Downhole Tools Market

Latin America represented an estimated 9.0% share in 2025, equal to about USD 0.47 Billion, 2025. The region is smaller in total revenue, but it remains strategically important because of offshore Brazil, shale activity in Argentina, and production optimization in Mexico and other mature basins. Brazil is the dominant market by a wide margin because pre-salt and offshore development require high-spec drilling, completion, and control tools. Mexico adds offshore and redevelopment demand, while Argentina contributes through unconventional drilling and completion activity. Tool value per well is often high in Latin America because geology and offshore conditions make equipment quality critical. Baker Hughes, SLB, Weatherford, and TechnipFMC all have strong relevance here. The main challenge is spending volatility tied to policy and operator budgets. Even so, Latin America should grow steadily through 2034 because high-complexity reservoirs and offshore development support premium downhole tool demand.

Middle East & Africa Downhole Tools Market

Middle East & Africa held an estimated 13.6% share in 2025, equal to about USD 0.70 Billion, 2025. This region remains smaller than North America and Asia Pacific in current revenue, but it has one of the strongest long-term growth profiles because giant fields, offshore redevelopment, and gas expansion all require advanced downhole tools. Saudi Arabia and the UAE are the main regional anchors. South Africa remains smaller today, but long-term offshore relevance keeps it on the map. Operators in the Middle East and Africa value reliability, high-temperature performance, and integrated support because well complexity and production stakes are high. Weatherford’s Turkmenistan contract and deepwater Gulf awards, along with Halliburton’s and SLB’s digital drilling tools, show how the regional market is leaning toward smarter, higher-control equipment. The region should gain share through 2034 as offshore and giant-field development keep requiring premium downhole technology.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Tool Type

- Downhole Control Tools

- Drilling Tools

- Flow and Pressure Control Tools

- Handling Tools and Others

By Application

- Drilling

- Completion

- Intervention and Production

- Formation Evaluation

By Location of Deployment

- Onshore

- Offshore

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.18 B |

| Forecast Revenue (2034) | USD 7.97 B |

| CAGR (2025-2034) | 4.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Tool Type (Downhole Control Tools, Drilling Tools, Flow and Pressure Control Tools, Handling Tools and Others), By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, OIL STATES INTERNATIONAL, TECHNIPFMC, HUNTING PLC, RUBICON OILFIELD INTERNATIONAL, UNITED DRILLING TOOLS, WENZEL DOWNHOLE TOOLS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Landscape, Technology Innovations, Strategic Developments, Investment Trends & Forecast 2026–2034")

, By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Landscape, Technology Innovations, Strategic Developments, Investment Trends & Forecast 2026–2034")

, By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Landscape, Technology Innovations, Strategic Developments, Investment Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Downhole Tools Market?

The Global Digital Oilfield Solutions Market was valued at USD 25.7 Billion in 2024 and USD 28.6 Billion in 2025, projected to reach USD 76.4 Billion by 2034 at a CAGR of 11.4% from 2026–2034. Growth is driven by AI-powered analytics, digital twins, cloud-based reservoir modeling, predictive maintenance, and increasing adoption of integrated digital oilfield platforms.

Who are the major players in the Downhole Tools Market?

SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, OIL STATES INTERNATIONAL, TECHNIPFMC, HUNTING PLC, RUBICON OILFIELD INTERNATIONAL, UNITED DRILLING TOOLS, WENZEL DOWNHOLE TOOLS, Others

Which segments covered the Downhole Tools Market?

By Tool Type (Downhole Control Tools, Drilling Tools, Flow and Pressure Control Tools, Handling Tools and Others), By Application (Drilling, Completion, Intervention and Production, Formation Evaluation), By Location of Deployment (Onshore, Offshore)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date