- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Drill Bit Market Size, Share, Growth Analysis & Forecast | CAGR 5.7%

Global Drill Bit Market Size, Share & Industry Analysis By Type (PDC and Fixed Cutter Bits, Roller Cone Bits, Hammer and Percussion Bits, Specialty and Coring Bits), By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic and Other Specialty Materials), By Application (Oil & Gas Drilling, Mining Operations, Construction & Infrastructure Development, Manufacturing & Metalworking), By Sales Channel (OEM & Direct Sales, Aftermarket & Distributor Sales) Regional Insights, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

| USD 7.8 Billion | USD 12.9 Billion | 5.7% | North America, 32.5% |

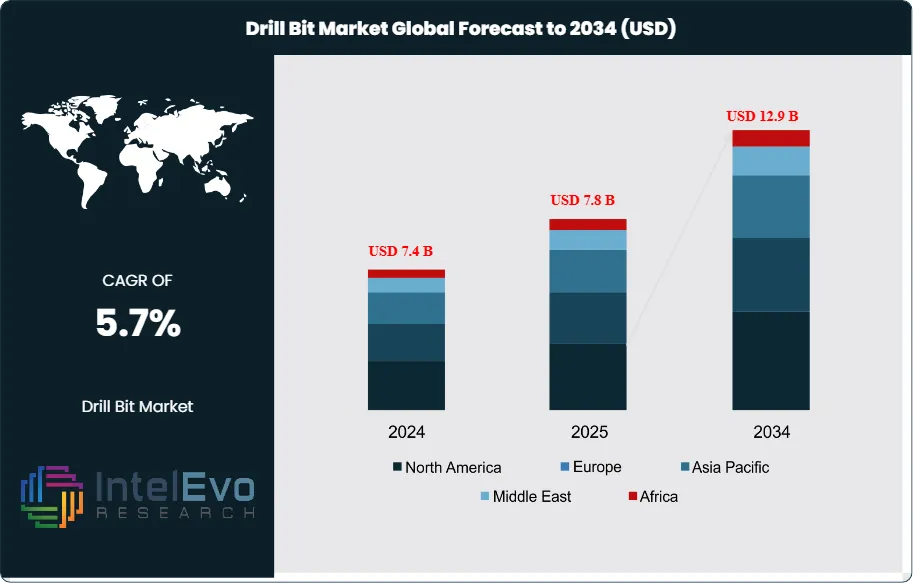

The Drill Bit Market was valued at approximately USD 7.4 Billion in 2024 and increased to USD 7.8 Billion in 2025. The market is projected to reach nearly USD 12.9 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2026 to 2034. The market growth is largely driven by increasing oil and gas exploration activities, rising demand for advanced drilling technologies, and expanding mining operations worldwide. Furthermore, technological advancements in polycrystalline diamond compact (PDC) and roller cone drill bits, along with growing investments in offshore and unconventional resource extraction, are expected to further support market expansion in the coming years.

Get More Information about this report -

Request Free Sample ReportThe Drill Bit Market in 2025 sits at the intersection of oil and gas drilling intensity, mining output growth, infrastructure build-outs, and steady replacement demand from metalworking and industrial boring operations. Demand remains strongest in high-cycle environments where bit wear directly affects cost per meter drilled. Premium polycrystalline diamond compact, or PDC, products continue to gain share because operators want longer runs, fewer trips, and tighter wellpath control. This shift is especially visible in oilfield applications, where horizontal drilling now dominates U.S. shale production and where faster decline rates require a larger flow of new wells to sustain output.

From a market structure standpoint, the Drill Bit Market remains moderately consolidated in premium oilfield bits and more fragmented in mining, construction, and industrial drilling tools. Fixed cutter and hybrid platforms command pricing strength because they deliver measurable gains in penetration rate and total bit life. Halliburton continues to push in-bit sensing deeper into bit design. Baker Hughes promotes hybrid stability and directional control. SLB keeps expanding the Smith Bits portfolio across oil, gas, and geothermal use cases. NOV is also moving upmarket with its ReedHycalog Evolve line aimed at harder, more abrasive formations. These product moves support the market’s pricing base and keep premium tiers ahead of standard commodity bits.

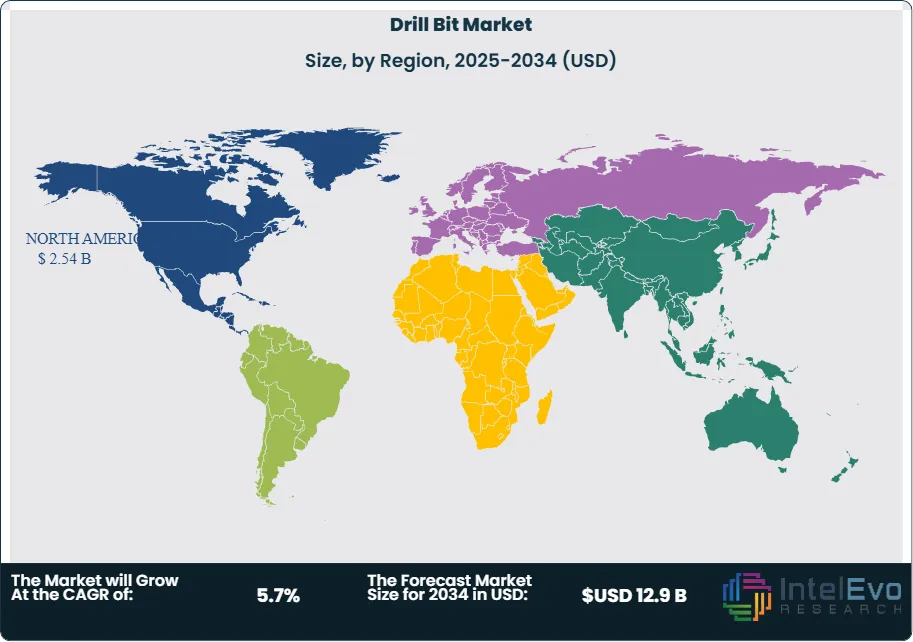

The 2025 market mix shows PDC and fixed cutter products leading with 41.0% share, followed by roller cone bits at 29.0%, hammer and percussion formats at 18.0%, and specialty and coring products at 12.0%. By application, oil and gas accounts for 38.0% of Drill Bit Market revenue in 2025, mining for 31.0%, construction and infrastructure for 19.0%, and manufacturing and metalworking for 12.0%. North America leads with 32.5% share, or USD 2.54 Billion in 2025, supported by shale drilling, offshore replacement work, and a large installed base. Asia Pacific follows with 28.5%, driven by mining, tunneling, and industrial production.

Supply conditions remain manageable but not loose. Tungsten carbide, diamond table quality, machining precision, and specialized cutter placement still shape lead times and gross margins. New investment hotspots include the Middle East for deep drilling programs, Latin America for offshore and hard-rock demand, and geothermal drilling in North America and Europe. Key risks include steel and carbide cost swings, weaker oil prices, slower Chinese industrial output, and drilling deferrals in smaller basins. Still, digital design, sensor-enabled bits, and hybrid cutter geometries should keep the Drill Bit Market on a steady upward path through 2034.

, By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic and Other Specialty Materials), By Application (Oil & Gas Drilling, Mining Operations, Construction & Infrastructure Development, Manufacturing & Metalworking), By Sales Channel (OEM & Direct Sales, Aftermarket & Distributor Sales) Regional Insights, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Drill Bit Market stands at USD 7.8 Billion in 2025 and is projected to reach USD 12.9 Billion by 2034. This implies a 5.7% CAGR across 2026-2034.

- Segment Dominance: PDC and fixed cutter bits lead the market by type with a 41.0% share in 2025, equal to about USD 3.20 Billion.

- Segment Dominance: Oil and gas is the top application segment with 38.0% of market revenue in 2025, or USD 2.96 Billion.

- Driver: The main demand driver is high replacement drilling intensity in shale and mature fields, which keeps premium bit consumption high across long lateral and directional drilling programs.

- Restraint: The main restraint is upstream spending pressure and input-cost inflation. Lower-margin drilling programs remain sensitive to steel, carbide, and procurement cost swings.

- Opportunity: Geothermal, deep hard-rock mining, and abrasive-formation drilling create the clearest growth pocket and are expected to add about USD 1.6 Billion in incremental revenue between 2025 and 2034.

- Trend: Sensor-enabled and application-specific premium bits are the strongest product trend. By 2025, digitally designed and premium monitored bits account for an estimated 28.0% of oilfield market revenue.

- Regional Analysis: North America is the leading regional market with 32.5% share and USD 2.54 Billion in revenue in 2025.

Competitive Landscape

The Drill Bit Market is moderately consolidated in premium oilfield products and more fragmented across mining, construction, and industrial formats. The top four companies account for an estimated 38.0% of 2025 global revenue. Competition is technology-led in oilfield and hard-rock drilling, but price pressure remains high in standard industrial products. Competitive intensity increased through 2025 and early 2026 as suppliers launched new hybrid, PCD, and sensor-enabled platforms while widening channel reach across mining and infrastructure.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | Smith Bits Spyder hybrid drill bit | North America, Middle East | Launched Spyder hybrid drill bit in Jun 2025 for lower torque and better bit dynamics. |

| HALLIBURTON | US | Leader | HyperSteer MX directional drill bit | North America, Latin America | Launched HyperSteer MX shankless matrix-body directional drill bit in Jan 2026. |

| BAKER HUGHES | US | Leader | Kymera hybrid drill bits | North America, Middle East | Expanded hybrid and geothermal bit positioning through Kymera and Vulcanix platforms in 2025. |

| NOV | US | Leader | ReedHycalog Evolve performance line | North America, Middle East | Introduced ReedHycalog Evolve premium drill bit line in Mar 2025. |

| EPIROC | Sweden | Challenger | PCD drill bits / Hero 8 core bit | Europe, Asia Pacific, Latin America | Launched Hero 8 diamond core bit in Mar 2025 and new PCD drill bits in Nov 2025. |

| SANDVIK | Sweden | Challenger | Top hammer drilling tools | Europe, Australia, North America | Signed acquisition of OSA Demolition Equipment in Apr 2025. |

| KENNAMETAL | US | Niche Player | Mining roof bits and carbide drills | North America | Expanded 2025 drilling product pipeline in industrial and mining tooling categories. |

| ATLAS COPCO | Sweden | Niche Player | Drilling rods and bits for rock drills | Europe, Middle East, Asia Pacific | Continued expansion of rods and bits offering for pneumatic rock drills in 2025. |

| BOART LONGYEAR | US | Niche Player | Diamond core bits | North America, Latin America, Australia | Maintained focus on exploration drilling consumables and coring systems through 2025. |

| VAREL ENERGY SOLUTIONS | US | Niche Player | Fixed cutter and roller cone bits | North America, Middle East | Kept regional expansion focus in premium oilfield drilling consumables during 2025. |

By Type

By type, the Drill Bit Market is led by PDC and fixed cutter bits with a 41.0% share in 2025, equal to USD 3.20 Billion. These products lead because they deliver faster penetration, lower vibration, and fewer trips in shale, directional drilling, and abrasive rock settings. Roller cone bits hold 29.0% share, or USD 2.26 Billion, and remain important in conventional drilling, geothermal intervals, softer formations, and cost-sensitive markets where proven run reliability matters more than premium speed. Hammer and percussion bits represent 18.0%, or USD 1.40 Billion, driven by mining, quarrying, and infrastructure drilling where hole consistency and bit life shape contractor economics. Specialty coring, diamond exploration, and niche bits account for the remaining 12.0%, or USD 0.94 Billion. This segment is smaller but posts above-market growth because mineral exploration, geothermal development, and difficult formations require highly tuned designs rather than standard catalog products.

By Material

By material, carbide-based drill bits account for 34.0% of 2025 market revenue, or USD 2.65 Billion. Carbide still holds the broadest installed base because it serves mining, construction, percussion drilling, and standard industrial applications where hardness, wear resistance, and predictable cost matter most. PDC and other diamond-based bits follow closely with 31.0%, or USD 2.42 Billion, reflecting strong demand in oilfield drilling, hard-rock exploration, and premium rock-tool applications. High-speed steel, or HSS, holds 21.0%, or USD 1.64 Billion, largely in general industrial, metalworking, and lower-value drilling use cases where price remains the first filter. The remaining 14.0%, or USD 1.09 Billion, sits in cobalt alloy, ceramic, and mixed-material specialty products used in heat-heavy, precision, or high-abrasion environments.

By Application

By application, oil and gas remains the largest revenue block with 38.0% share in 2025, or USD 2.96 Billion. This segment stays ahead because bit performance has a direct effect on total well cost, especially in long laterals, deep offshore sections, and high-temperature formations. Mining ranks second with 31.0%, or USD 2.42 Billion, supported by blast-hole drilling, underground development, surface production drilling, and mineral exploration. Construction and infrastructure holds 19.0%, or USD 1.48 Billion, tied to tunneling, foundation works, road projects, and quarry operations. Manufacturing and metalworking account for 12.0%, or USD 0.94 Billion, where demand is steadier but pricing is lower and competition is broader. The market by application clearly shows two economic models. Oil and gas and hard-rock mining favor engineered, premium, application-specific bits with tighter service support. Construction and industrial channels carry larger SKU counts, shorter replacement cycles, and sharper price competition.

By Sales Channel

By sales channel, OEM and direct solution sales account for 57.0% of market revenue in 2025, or USD 4.45 Billion. This share is highest in oilfield drilling, major mining accounts, and technically demanding rock-tool applications where bit choice depends on formation modeling, drilling parameters, and field engineering support. Aftermarket and distributor-led sales account for 43.0%, or USD 3.35 Billion, and dominate contractor fleets, construction drilling, local mining operations, and industrial machining environments where inventory availability and price win more deals than engineering support. The market is slowly tilting toward direct and data-linked selling because premium bits increasingly rely on application input, digital modeling, and run-performance feedback.

By Regional Analysis

North America Drill Bit Market

North America holds 32.5% of the Drill Bit Market in 2025, equal to USD 2.54 Billion. The region leads because the United States remains the world’s largest market for premium oilfield drill bits, hybrid bits, and sensor-enabled drilling tools. The United States accounts for about USD 2.09 Billion of regional revenue in 2025. Canada contributes roughly USD 0.29 Billion, supported by oil sands, shale, mining, and geothermal drilling demand. Mexico adds about USD 0.16 Billion, with offshore and directional oilfield demand supporting premium offerings. The region will retain leadership through 2034, though growth moderates as the market shifts from explosive rig growth to efficiency-led replacement demand.

Europe Drill Bit Market

Europe accounts for 19.0% of the Drill Bit Market in 2025, or USD 1.48 Billion. Germany leads regional demand with about USD 0.31 Billion, followed by the UK at USD 0.24 Billion, France at USD 0.21 Billion, and Sweden at USD 0.18 Billion. Europe’s market mix favors precision, tool life, and lower emissions per meter drilled rather than pure drilling speed. Mining tools, tunneling, industrial drilling, and geothermal applications play a larger role here than shale oilfield drilling. Europe is not the fastest-growth region, but it is one of the most technically demanding and margin-supportive parts of the market.

Asia Pacific Drill Bit Market

Asia Pacific holds 28.5% of the Drill Bit Market in 2025, equal to USD 2.22 Billion. China leads with about USD 0.86 Billion in 2025, supported by large-scale construction, metals processing, and domestic mining. Australia follows with USD 0.43 Billion due to iron ore, gold, and hard-rock drilling intensity. India contributes around USD 0.32 Billion through infrastructure, quarrying, water-well drilling, and manufacturing demand. Japan adds roughly USD 0.18 Billion, backed by industrial precision drilling and specialty tools. Asia Pacific is the fastest-growing regional market through 2034 because governments and private capital continue funding roads, tunnels, rail links, industrial parks, and resource extraction.

Latin America Drill Bit Market

Latin America represents 8.0% of the Drill Bit Market in 2025, or USD 0.62 Billion. Brazil leads with about USD 0.24 Billion, driven by offshore oil and gas, mining, and infrastructure. Mexico follows at USD 0.16 Billion, with activity tied to directional drilling, offshore work, and replacement demand in mature energy assets. Chile contributes around USD 0.11 Billion due to copper mining and related exploration drilling. The region offers solid growth but uneven purchasing cycles because currency swings, public procurement delays, and project financing gaps can slow standard bit demand.

Middle East & Africa Drill Bit Market

Middle East & Africa accounts for 12.0% of the Drill Bit Market in 2025, equal to USD 0.94 Billion. Saudi Arabia contributes about USD 0.24 Billion of regional demand in 2025, the UAE about USD 0.14 Billion, and South Africa around USD 0.11 Billion. The rest is spread across Oman, Kuwait, Qatar, Egypt, and selected mining markets in Southern and West Africa. The key regional draw is the willingness to pay for reliability in harsh formations and remote operations. That keeps Middle East & Africa one of the better-margin regions in the global market.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- PDC and Fixed Cutter Bits

- Roller Cone Bits

- Hammer and Percussion Bits

- Specialty and Coring Bits

By Material

- Carbide Bits

- PDC and Diamond Bits

- High-Speed Steel Bits

- Cobalt Alloy, Ceramic, and Other Specialty Bits

By Application

- Oil and Gas

- Mining

- Construction and Infrastructure

- Manufacturing and Metalworking

By Sales Channel

- OEM and Direct Sales

- Aftermarket and Distributor Sales

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.8 B |

| Forecast Revenue (2034) | USD 12.9 B |

| CAGR (2025-2034) | 5.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (PDC and Fixed Cutter Bits, Roller Cone Bits, Hammer and Percussion Bits, Specialty and Coring Bits), By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic, and Other Specialty Bits), By Application (Oil and Gas, Mining, Construction and Infrastructure, Manufacturing and Metalworking), By Sales Channel (OEM and Direct Sales, Aftermarket and Distributor Sales) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, NOV, EPIROC, SANDVIK, KENNAMETAL, ATLAS COPCO, BOART LONGYEAR, VAREL ENERGY SOLUTIONS, SANDVIK COROMANT, MITSUBISHI MATERIALS, SUMITOMO ELECTRIC HARDMETAL, GUHRING, WALTER TOOLS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic and Other Specialty Materials), By Application (Oil & Gas Drilling, Mining Operations, Construction & Infrastructure Development, Manufacturing & Metalworking), By Sales Channel (OEM & Direct Sales, Aftermarket & Distributor Sales) Regional Insights, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

, By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic and Other Specialty Materials), By Application (Oil & Gas Drilling, Mining Operations, Construction & Infrastructure Development, Manufacturing & Metalworking), By Sales Channel (OEM & Direct Sales, Aftermarket & Distributor Sales) Regional Insights, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

, By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic and Other Specialty Materials), By Application (Oil & Gas Drilling, Mining Operations, Construction & Infrastructure Development, Manufacturing & Metalworking), By Sales Channel (OEM & Direct Sales, Aftermarket & Distributor Sales) Regional Insights, Competitive Landscape, Key Players, Market Dynamics, Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Drill Bit Market?

The Global Drill Bit Market was valued at USD 7.4 Billion in 2024 and reached USD 7.8 Billion in 2025, projected to grow to USD 12.9 Billion by 2034 at a CAGR of 5.7% from 2026–2034. Market growth is driven by rising oil & gas exploration, increasing mining activities, and technological advancements in PDC and roller cone drill bits worldwide.

Who are the major players in the Drill Bit Market?

SLB, HALLIBURTON, BAKER HUGHES, NOV, EPIROC, SANDVIK, KENNAMETAL, ATLAS COPCO, BOART LONGYEAR, VAREL ENERGY SOLUTIONS, SANDVIK COROMANT, MITSUBISHI MATERIALS, SUMITOMO ELECTRIC HARDMETAL, GUHRING, WALTER TOOLS, Others

Which segments covered the Drill Bit Market?

By Type (PDC and Fixed Cutter Bits, Roller Cone Bits, Hammer and Percussion Bits, Specialty and Coring Bits), By Material (Carbide Bits, PDC and Diamond Bits, High-Speed Steel Bits, Cobalt Alloy, Ceramic, and Other Specialty Bits), By Application (Oil and Gas, Mining, Construction and Infrastructure, Manufacturing and Metalworking), By Sales Channel (OEM and Direct Sales, Aftermarket and Distributor Sales)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date