- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Drilling Waste Management Market Size, Share & Forecast 2034 | CAGR 4.7%

Global Drilling Waste Management Market Size, Share, Analysis By Service (Treatment and Disposal, Containment and Handling, Solids Control and Waste Minimization, Transportation and Ancillary Services), By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation and Stabilization) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Environmental Compliance Trends & Forecast 2026–2034

Report Overview

| Market Size, 2025 | Forecast Value, 2034 | CAGR, 2026-2034 | Leading Region, 2025 |

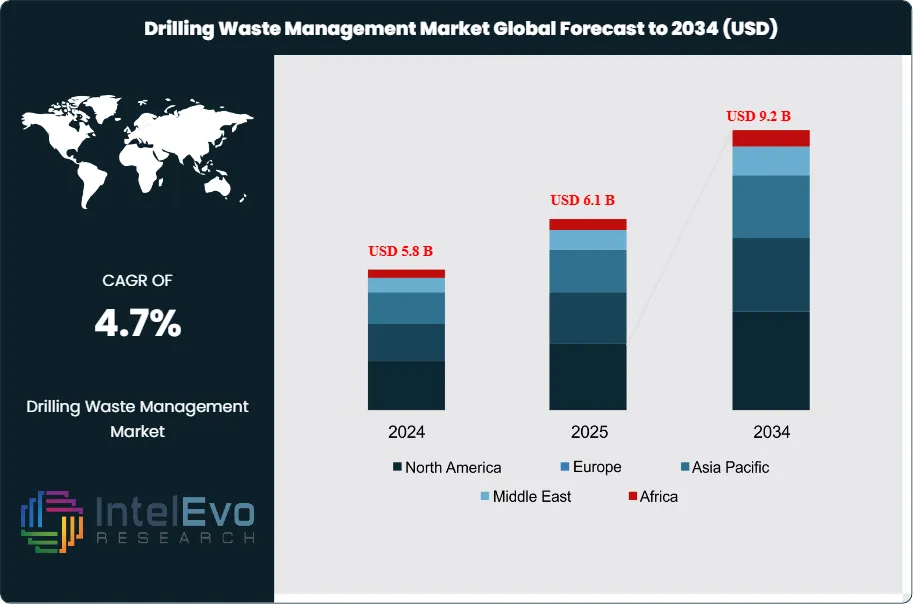

| USD 6.1 Billion | USD 9.2 Billion | 4.7% | North America, 31.0% |

The Drilling Waste Management Market was valued at USD 5.8 billion in 2024 and is projected to reach approximately USD 6.1 billion in 2025. The market is further expected to expand to nearly USD 9.2 billion by 2034, registering a compound annual growth rate (CAGR) of about 4.7% during the forecast period from 2026 to 2034. The Drilling Waste Management Market is expanding because drilling programs are still active across offshore, shale, and gas-led basins, while environmental controls on cuttings, fluids, and contaminated water remain firm. Public market references already show a broad but consistent growth direction for the drilling waste management market, with most forecasts pointing to mid-single-digit or better long-term expansion. This report places the market near the center of that current range and aligns growth with actual spending, regulation, and service capacity trends visible in 2025.

Get More Information about this report -

Request Free Sample ReportThe Drilling Waste Management Market sits at the intersection of upstream drilling intensity and environmental compliance. Demand is strongest in regions where operators drill large onshore pad programs, offshore wells with strict discharge rules, or mature reservoirs that generate higher fluid-treatment and solids-handling needs. North America remains the largest revenue pool because of sustained land drilling, waste transport networks, and broad commercial disposal infrastructure. Europe and the North Sea support high-value offshore waste management because OSPAR restrictions on oil-contaminated cuttings keep treatment quality standards tight. In the United States, EPA effluent rules continue to shape how operators manage drilling fluids, cuttings, and related discharges across onshore, coastal, and offshore activity.

Supply conditions favor large integrated providers and specialist waste handlers with installed treatment assets, logistics networks, and solids-control equipment. Halliburton, Baker Hughes, SLB, SECURE, TWMA, and NOV all hold visible positions, but the market remains fragmented because local disposal capacity, transport permits, and basin-specific regulations still matter. Competition is not based on price alone. It is shaped by waste recovery rates, thermal treatment throughput, drilling-fluid reuse, zero-discharge capability, and the ability to cut transport volumes. Halliburton documented a 2025 UAE project where Baroid waste management personnel treated more than 8,100 m³ of oil-based cuttings and recovered 1,110 m³ of base oil, generating more than USD 1.39 million in net profit for the operator. That example shows why drilling waste management is now tied directly to drilling economics rather than only compliance spend.

Technology is changing the Drilling Waste Management Market in clear ways. Thermal desorption, solids-control automation, waste-volume reduction, cuttings drying, and digital tracking now shape tender outcomes. SLB introduced its Cuttings Management and Recycling System in 2025 to reduce waste volume and improve water efficiency. NOV reported a 2025 contract for a customized solids-control solution in Iceland, showing that specialized separation systems continue to gain share beyond conventional oil and gas drilling. At the same time, risk remains material. The IEA expects upstream oil and gas cost inflation of about 3% in 2025, and project timing remains vulnerable to commodity-price swings and regional politics. Still, the Drilling Waste Management Market should post steady growth because environmental limits are not easing and drilling waste remains an unavoidable output of well construction.

Regional investment hotspots support that view. The Middle East is set to invest about USD 130 Billion in oil and gas supply in 2025. U.S. Gulf of America crude output is expected to average 1.80 million barrels per day in 2025. Latin America remains important through offshore Brazil, while Asia Pacific keeps adding demand from offshore gas and deepwater programs. These investment flows keep the need for containment, treatment, disposal, and fluid-recovery services intact across the forecast period to 2034.

, By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation and Stabilization) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Environmental Compliance Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Drilling Waste Management Market was valued at USD 6.1 Billion, 2025 and is projected to reach USD 9.2 Billion, 2034, at a 4.7% CAGR during 2025–2034. This scenario sits between recent public market references that range from USD 5.88 Billion, 2025 to stronger growth cases built from broader service definitions.

- Segment Dominance: By service, treatment and disposal led the Drilling Waste Management Market with 34.0% share, 2025, equal to USD 2.1 Billion, 2025. Operators continue to spend most on final treatment, thermal recovery, cuttings processing, and compliant disposal because those steps carry the highest regulatory burden.

- Segment Dominance: By application, onshore drilling waste management accounted for 63.0% share, 2025, equal to USD 3.8 Billion, 2025. Large land-drilling programs in North America and the Middle East keep onshore waste volumes ahead of offshore volumes.

- Driver: The main driver is stricter environmental control on cuttings and fluids across offshore and onshore drilling. EPA rules cover wastewater from exploration, drilling, production, well treatment, and completion activities, while OSPAR continues to restrict discharge of organic-phase drilling fluids and contaminated cuttings.

- Restraint: The main restraint is cost pressure. The IEA expects upstream oil and gas cost inflation of about 3.0%, 2025, which raises handling, transport, and disposal costs and slows adoption in lower-margin wells.

- Opportunity: The largest opportunity is waste recovery and recycling. Halliburton’s UAE case recovered 1,110 m³ of base oil from 8,100 m³ of oil-based drill cuttings and generated more than USD 1.39 million in operator profit, showing the direct value of reuse-led waste management.

- Trend: The defining trend is automation-led solids control and recycling. SLB launched a 2025 cuttings management and recycling system focused on lower waste volumes and improved water efficiency, while NOV reported a new solids-control contract in April 2025 for geothermal drilling.

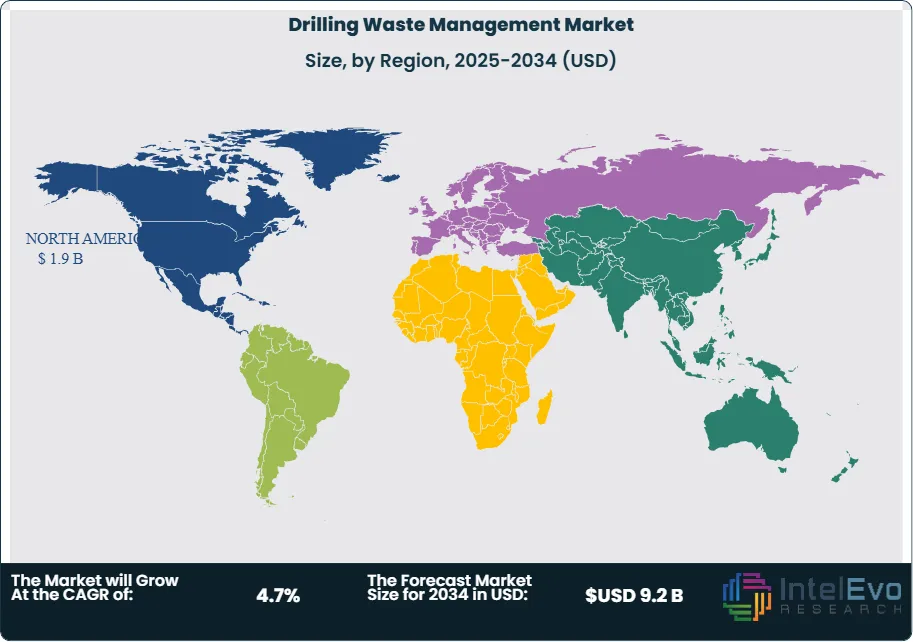

- Regional Analysis: North America led the Drilling Waste Management Market with 31.0% share, 2025, equal to USD 1.9 Billion, 2025. The region benefits from large onshore waste volumes, developed disposal infrastructure, and continued Gulf of America drilling activity.

Competitive Landscape

The Drilling Waste Management Market is fragmented to moderately consolidated. The top four players, HALLIBURTON, BAKER HUGHES, SLB, and SECURE WASTE INFRASTRUCTURE, held an estimated 33.0% of global revenue in 2025. Competition is shaped by technology, disposal access, basin coverage, and recovery economics rather than price alone. Competitive intensity increased in 2025 as SLB launched a new recycling system, TWMA added major North Sea contracts, and SECURE expanded financing and infrastructure capacity to support waste and water volumes.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| HALLIBURTON | US | Leader | Baroid® waste management services | North America, Middle East | Expanded Baroid deployment in UAE in 2025; treated over 8,100 m³ of cuttings and recovered 1,110 m³ of base oil. |

| BAKER HUGHES | US | Leader | Fluids Environmental Services | Middle East, Africa, Latin America | Advanced a drilling and completion fluids laboratory footprint in Muscat in 2025, strengthening regional fluids and waste support. |

| SLB | US | Leader | Cuttings Management and Recycling System | Middle East, Latin America, Offshore global | Introduced its CMRS recycling system on 30 June 2025 to cut waste volume and improve water efficiency. |

| SECURE WASTE INFRASTRUCTURE | Canada | Leader | Industrial Waste Processing and Disposal network | Canada, North America | Increased revolving credit capacity in May 2025 and continued facility expansion in 2025. |

| TWMA | UK | Challenger | RotoMill® drilling waste processing | North Sea, Middle East | Won a three-year TotalEnergies UK drilling waste contract in April 2025 and a bp North Sea contract in May 2025. |

| NOV | US | Challenger | Solids Control customized systems | North America, Europe | Reported a customized solids-control contract for a geothermal drilling campaign in Iceland in April 2025. |

| GN SOLIDS CONTROL | China | Challenger | GN cuttings dryers and solids-control systems | Asia Pacific, Middle East | Reported delivery of more than 10 solids-control system sets in February 2026 across Asia, Europe, and domestic fields. |

| DERRICK EQUIPMENT COMPANY | US | Niche Player | HyperPool® shale shakers | North America | Continued push of high-capacity solids-control systems through its 2024–2025 drilling brochure and basin deployments. |

| SOLI-BOND | US | Niche Player | Solidification and waste stabilization systems | North America, Middle East | Maintained active market presence in drilling waste stabilization applications through 2025. |

| SOILTECH | Norway | Niche Player | TCC and offshore waste treatment solutions | Europe, Middle East | Continued offshore waste processing focus in zero-discharge and recovery-oriented markets through 2025. |

By Service

Treatment and disposal held the largest share of the Drilling Waste Management Market at 34.0%, 2025, equivalent to USD 2.1 Billion, 2025. This segment leads because final treatment and compliant disposal sit at the core of every waste-management workflow, especially for oil-based cuttings, contaminated mud, and residual slurries. Thermal desorption, stabilization, landfill routing, and licensed disposal remain high-value activities because they carry both environmental liability and specialist equipment needs. Containment and handling accounted for 24.0%, 2025, or USD 1.5 Billion, 2025. This segment includes skips, tanks, transfer equipment, and wellsite waste control. It grows with rig count but carries lower pricing power than treatment. Solids control and waste minimization represented 27.0%, 2025, equal to USD 1.6 Billion, 2025, and continues to gain because fluid recovery directly reduces disposal cost. Transportation and ancillary services made up the remaining 15.0%, 2025, or USD 0.9 Billion, 2025. While smaller in value, this segment remains essential in shale basins and remote offshore logistics. Competitive positioning is strongest where providers combine solids control with downstream disposal access, which is why Halliburton, Baker Hughes, SLB, SECURE, and TWMA retain an edge over local single-step vendors.

By Application

Onshore drilling accounted for 63.0% share, 2025, equal to USD 3.8 Billion, 2025, making it the largest application block in the Drilling Waste Management Market. Onshore dominance is rooted in volume. Shale and land-rig programs generate continuous flows of cuttings, spent fluids, contaminated water, and tank bottoms, and they require a dense chain of collection, transport, treatment, and disposal services. North America is the main demand center, but the Middle East also supports large onshore waste volumes through conventional drilling programs. Offshore drilling represented 37.0%, 2025, or USD 2.3 Billion, 2025. Offshore waste commands higher revenue per well because regulatory control is tighter, logistics are harder, and zero-discharge or near-zero-discharge requirements often raise technology intensity. OSPAR restrictions in the North Sea and EPA permit controls in U.S. offshore waters keep offshore service specifications high. Offshore also benefits more from waste-volume reduction, because every ton avoided lowers marine transport and disposal cost. This is why TWMA, SLB, and Halliburton remain more visible in offshore tenders, while SECURE and regional handlers retain more weight in large land markets.

By Waste Type

Drill cuttings formed the largest waste-type segment with 39.0% share, 2025, equal to USD 2.4 Billion, 2025. Cuttings dominate because every drilled interval generates solids, and oil-based or synthetic-based mud residues make treatment more complex and more expensive. Drilling fluids represented 28.0%, 2025, or USD 1.7 Billion, 2025. This segment includes spent mud, fluid losses, recovered base oil, and mud treatment streams. Its share is large because fluid chemistry has both economic value and compliance risk. Contaminated water and wash water accounted for 19.0%, 2025, equal to USD 1.2 Billion, 2025, with demand rising in basins that push reuse and water stewardship. The remaining 14.0%, 2025, or USD 0.9 Billion, 2025, came from other wastes such as tank bottoms, sludges, oily debris, and mixed industrial drilling residues. The competitive pattern is clear. Vendors with strong cuttings drying, thermal treatment, and fluid-recovery capacity capture the highest-value portions of the market. Halliburton’s 2025 UAE case shows how oil recovery from cuttings can shift customer economics materially, while SLB’s 2025 recycling system confirms that drill-cuttings reduction remains a technology priority.

By Treatment Technology

Thermal treatment and recovery led the Drilling Waste Management Market by treatment technology with 31.0% share, 2025, equal to USD 1.9 Billion, 2025. It leads because thermal desorption remains one of the most effective routes for separating hydrocarbons from oil-based cuttings and enabling resource recovery. Solids control systems held 29.0%, 2025, or USD 1.8 Billion, 2025. This segment includes shale shakers, centrifuges, cuttings dryers, and fluid-recovery packages. It is growing because operators want to reduce waste before final disposal. Reinjection and secure subsurface disposal represented 18.0%, 2025, equal to USD 1.1 Billion, 2025, with greatest relevance in offshore or remote areas where surface disposal is limited. Bioremediation, stabilization, and other chemical or biological treatments made up 22.0%, 2025, or USD 1.3 Billion, 2025. These remain important in land markets where lower-cost treatment paths fit local rules. Technology competition is shifting toward systems that lower waste volumes and improve recovery economics, which helps SLB, NOV, GN Solids Control, and TWMA. It also creates room for local disposal specialists where regulation favors stabilized landfill disposal over advanced recovery.

Regional Analysis

North America Drilling Waste Management Market

North America held 31.0% share, 2025, equal to USD 1.9 Billion, 2025, making it the largest regional block in the Drilling Waste Management Market. The United States dominates regional demand, followed by Canada and Mexico. The region leads because it combines high land-drilling intensity, mature industrial-waste infrastructure, and large commercial networks for collection, treatment, and disposal. The United States remains the anchor market. EPA effluent rules continue to frame waste handling across exploration, drilling, production, well treatment, and completion activities, while Gulf of America crude output is expected to average 1.80 million barrels per day, 2025. That combination supports both onshore and offshore service demand. Canada contributes strongly through basin-centered waste processing, disposal wells, and produced-water handling, especially through companies such as SECURE. Mexico remains smaller but relevant in offshore and cross-border service demand.

The competitive structure in North America favors integrated operators with disposal assets and local logistics. SECURE has a clear regional edge because of its industrial waste processing network, produced-water assets, and active 2025 infrastructure expansion. Halliburton, Baker Hughes, SLB, NOV, and Derrick are also important because they connect solids control and fluid systems to broader wellsite operations. Regulatory enforcement remains a tailwind. Waste manifests, storage, transport, and treatment quality are tightly managed in many producing jurisdictions, which protects pricing in compliant service categories. The main constraint is drilling cyclicality. When rig activity softens, handling volumes fall quickly. Even so, North America should remain the largest regional market through 2034 because of scale, service density, and persistent environmental control on waste streams.

Europe Drilling Waste Management Market

Europe accounted for 22.0% share, 2025, equal to USD 1.3 Billion, 2025. The UK, Norway, Germany, and the Netherlands are the most relevant countries, though the true commercial center is the North Sea. Europe remains a high-value market because offshore drilling waste management is governed by strict discharge standards, strong environmental oversight, and high offshore logistics costs. OSPAR rules remain central. The use and discharge of organic-phase drilling fluids and contaminated cuttings are tightly controlled, which supports demand for treatment, transport, and recovery systems rather than simple discharge pathways. The UK and Norway dominate service demand because of offshore field activity and legacy infrastructure that requires careful waste handling. Denmark is also gaining relevance through ongoing operator activity and contractor demand in the broader North Sea supply chain.

Europe favors specialist offshore providers more than most regions. TWMA is especially visible because its RotoMill processing model fits wellsite waste reduction and lower transport demand. The company won a three-year TotalEnergies UK contract in April 2025 and a bp North Sea contract in May 2025, both of which confirm that operators still value specialist waste handlers with offshore execution depth. Soiltech and other niche recovery-focused companies also remain relevant in the regional mix. The main growth limit is basin maturity. Europe does not have the volume potential of North America or the Middle East. Still, Europe should keep a high revenue-per-well profile because waste management standards remain strict and offshore handling costs remain elevated.

Asia Pacific Drilling Waste Management Market

Asia Pacific captured 18.0% share, 2025, equivalent to USD 1.1 Billion, 2025. China, Australia, India, and Indonesia lead the regional profile. The region mixes offshore gas, offshore oil, and land-drilling activity, which creates varied waste streams and different treatment needs across countries. Australia and offshore Southeast Asia drive premium offshore waste-management demand because marine transport, environmental compliance, and waste-volume reduction matter more in remote operations. China contributes through both onshore and offshore drilling, while India adds steady growth from offshore redevelopment and rising compliance needs. Indonesia remains a practical growth market because deepwater and offshore activity support higher-value handling and treatment requirements.

The supplier base in Asia Pacific is split between global integrated vendors and regional equipment specialists. Baker Hughes maintains a strong position in fluids and waste services, while GN Solids Control has grown through equipment delivery and solids-control systems. In February 2026, GN reported delivery of more than 10 system sets across multiple markets, reinforcing the role of regional manufacturers in basin-level competition. Asia Pacific growth is supported by a combination of offshore gas investment, rising local environmental oversight, and stronger operator focus on recycling and fluid recovery. The main challenge is uneven policy enforcement across countries. Some markets maintain high control standards; others remain price driven. Even so, Asia Pacific should post steady growth through 2034 because offshore development and drilling complexity continue to support demand for specialized waste services and solids-control equipment.

Latin America Drilling Waste Management Market

Latin America held 13.0% share, 2025, equal to USD 0.8 Billion, 2025. Brazil is the main market, followed by Mexico and Argentina. Brazil leads because offshore drilling and subsea-linked well construction keep waste-control requirements high, while large offshore projects sustain demand for fluid systems, solids control, and compliant disposal pathways. Mexico remains an important secondary market through offshore operations, while Argentina contributes through land drilling and unconventional development that create steady cuttings and fluid-handling demand. The region also benefits from larger energy-sector capital flows. The IEA expects Latin America’s overall energy investment to reach about USD 160 Billion, 2025, although that figure spans more than oil and gas alone.

Competitive positioning in Latin America favors Baker Hughes, Halliburton, and SLB because these firms bring fluids systems, solids-control equipment, and waste handling inside broader well-construction contracts. Baker Hughes’ Namibian mud-plant project from 2024 also shows how service providers are investing in regional logistics and fluid support close to offshore growth areas, a model that can extend into Atlantic-margin opportunities tied to Latin America and Africa. The regional challenge is contract timing and policy shifts. Waste-management demand can move in waves with offshore drilling campaigns and national budget cycles. Even so, Latin America should remain one of the more attractive mid-term markets for offshore drilling waste management because well complexity is rising and discharge scrutiny remains firm.

Middle East & Africa Drilling Waste Management Market

Middle East & Africa represented 16.0% share, 2025, equal to USD 1.0 Billion, 2025. Saudi Arabia, the UAE, Oman, and South Africa are the most relevant named markets, though activity is concentrated most heavily in the Gulf states. The region remains important because the IEA expects the Middle East to invest about USD 130 Billion in oil and gas supply, 2025, with Saudi upstream investment around USD 40 Billion, 2025. That level of upstream activity directly supports drilling waste management demand across land rigs, offshore programs, and large integrated well campaigns. Saudi Arabia and the UAE lead on scale. Oman remains relevant for drilling-fluid support and regional service laboratories, while South Africa matters more as a strategic coverage market than as the current regional revenue anchor.

The region supports both global service majors and specialists. Halliburton has visible proof of value in UAE waste recovery. TWMA expanded Middle East operations after a contract win worth about USD 70 Million in October 2024, showing that offshore and large-field operators still award meaningful waste-management scopes to focused providers. Baker Hughes also strengthened its regional drilling and completion fluids footprint in Muscat in 2025. The main risks in the region are geopolitics, procurement delays, and uneven waste-service depth outside major oil-producing corridors. Even so, Middle East & Africa remains a solid growth market through 2034 because upstream activity is high and operators increasingly seek lower waste volumes, better fluid recovery, and tighter environmental control.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service

- Treatment and Disposal

- Containment and Handling

- Solids Control and Waste Minimization

- Transportation and Ancillary Services

By Application

- Onshore Drilling

- Offshore Drilling

By Waste Type

- Drill Cuttings

- Drilling Fluids

- Contaminated Water and Wash Water

- Others

By Treatment Technology

- Thermal Treatment and Recovery

- Solids Control Systems

- Reinjection and Secure Subsurface Disposal

- Bioremediation, Stabilization, and Other Treatments

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.1 B |

| Forecast Revenue (2034) | USD 9.2 B |

| CAGR (2025-2034) | 4.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service (Treatment and Disposal, Containment and Handling, Solids Control and Waste Minimization, Transportation and Ancillary Services), By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation, Stabilization, and Other Treatments) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HALLIBURTON, BAKER HUGHES, SLB, SECURE WASTE INFRASTRUCTURE, TWMA, NOV, GN SOLIDS CONTROL, DERRICK EQUIPMENT COMPANY, SOLI-BOND, SOILTECH, WEATHERFORD, SPECIALTY DRILLING FLUIDS, RIDGELINE CANADA, IMDEX, SCOMI GROUP, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation and Stabilization) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Environmental Compliance Trends & Forecast 2026–2034")

, By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation and Stabilization) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Environmental Compliance Trends & Forecast 2026–2034")

, By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation and Stabilization) Industry Region & Key Players–Industry Segment Overview, Market Dynamics, Competitive Strategies, Environmental Compliance Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Drilling Waste Management Market?

Global Drilling Waste Management Market was valued at USD 5.8 billion in 2024 and is projected to reach USD 9.2 billion by 2034, expanding at a CAGR of 4.7%. Explore key trends, environmental regulations, offshore drilling growth, and waste treatment technologies shaping the industry.

Who are the major players in the Drilling Waste Management Market?

HALLIBURTON, BAKER HUGHES, SLB, SECURE WASTE INFRASTRUCTURE, TWMA, NOV, GN SOLIDS CONTROL, DERRICK EQUIPMENT COMPANY, SOLI-BOND, SOILTECH, WEATHERFORD, SPECIALTY DRILLING FLUIDS, RIDGELINE CANADA, IMDEX, SCOMI GROUP, Others

Which segments covered the Drilling Waste Management Market?

By Service (Treatment and Disposal, Containment and Handling, Solids Control and Waste Minimization, Transportation and Ancillary Services), By Application (Onshore Drilling, Offshore Drilling), By Waste Type (Drill Cuttings, Drilling Fluids, Contaminated Water and Wash Water, Others), By Treatment Technology (Thermal Treatment and Recovery, Solids Control Systems, Reinjection and Secure Subsurface Disposal, Bioremediation, Stabilization, and Other Treatments)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Drilling Waste Management Market

Published Date : 11 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date