- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Driver Drowsiness Detection System Market Size, Share & Forecast | 11.8% CAGR

Global Driver Drowsiness Detection System Market Size, Share, Growth Analysis By Product Type (Hardware Devices, Software Systems), By Vehicle Type (Passenger Cars, Commercial Vehicles), By System Type (Lane Departure Warning Systems, Driver Fatigue Monitoring Systems, Driver Distraction Monitoring Systems), By Technology (AI-Based Monitoring, Infrared Sensors, Camera-Based Systems) Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2025–2034

Report Overview

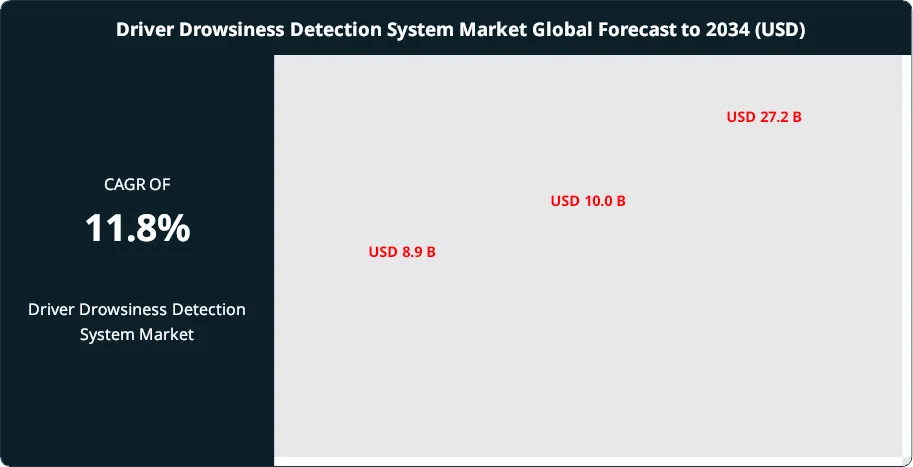

The Driver Drowsiness Detection System Market was valued at USD 8.9 Billion in 2024 and is estimated to reach approximately USD 10.0 Billion in 2025. With increasing adoption of advanced driver assistance systems (ADAS) and growing emphasis on road safety technologies, the market is projected to expand from about USD 11.1 Billion in 2026 to nearly USD 27.2 Billion by 2034, registering a compound annual growth rate (CAGR) of around 11.8% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportDriver drowsiness detection systems sit at the intersection of vehicle safety, onboard sensing, and applied AI. These solutions track fatigue and inattention signals in real time using in-cabin cameras, infrared illumination, steering and lane-keeping inputs, and software models that interpret eye movement, head pose, blink rate, and driving micro-corrections. As automakers expand advanced driver-assistance systems (ADAS) portfolios, drowsiness and attention monitoring increasingly functions as a core safety layer that supports higher levels of assisted driving and reduces exposure to fatigue-driven incidents.

Demand growth is anchored in two forces. First, regulators in Europe and North America continue to tighten active safety requirements, which raises baseline penetration in new vehicles and accelerates OEM-fit adoption. Second, accident and liability economics push fleets to adopt fatigue monitoring at scale. Drowsy driving remains a material safety and cost issue, with estimates pointing to roughly 100,000 crashes annually in the U.S. and 71,000 injuries tied primarily to fatigue-related incidents, alongside thousands of deaths each year. Behavioral data also indicates a persistent risk gap: while about 90% of adults avoid driving after a few drinks, only about 40% report seeking alternatives when sleep-deprived, reinforcing the case for in-vehicle safeguards.

On the supply side, the market continues to shift toward camera-led architectures and software-defined differentiation. Cameras and infrared modules are estimated to represent about 45–55% of system revenue, while AI models and embedded software account for roughly 30–40% as OEMs prioritize accuracy, lower false alerts, and continuous feature updates. OEM integrations are projected to hold about 65–75% of 2024 revenue, supported by platform-level ADAS roadmaps, while aftermarket demand remains stronger in commercial fleets where retrofits reduce incident rates and insurance costs.

Regionally, Europe is expected to remain a leading adoption center due to regulation-led fitment, while North America sustains growth through premium vehicle mix and fleet safety programs. High-growth investment hotspots include China and India, where falling sensor costs and rapid ADAS uptake expand the addressable base. Key risks include data privacy compliance, cybersecurity exposure in connected architectures, model bias across lighting and demographics, and semiconductor supply volatility. Over the forecast period, integration with telematics, cloud analytics, and predictive safety scoring should expand recurring software revenue and strengthen the strategic value of these systems within connected vehicle ecosystems.

, By Vehicle Type (Passenger Cars, Commercial Vehicles), By System Type (Lane Departure Warning Systems, Driver Fatigue Monitoring Systems, Driver Distraction Monitoring Systems), By Technology (AI-Based Monitoring, Infrared Sensors, Camera-Based Systems) Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market rises from 8.9 billion USD, 2024 to 27.2 billion USD, 2034 at 11.8% CAGR, 2024-2034. This trajectory reflects sustained safety-tech adoption across vehicle platforms, estimated: 1.1x penetration uplift, 2034.

- Segment Dominance : Hardware devices lead product-type revenue with 68.2%, 2024. This dominance reflects higher OEM bill-of-materials weight, estimated: 6.1 billion USD, 2024.

- Segment Dominance: Passenger cars hold the largest vehicle-type share at 58.0%, 2024. Volume-driven fitment keeps this segment central to scaling, estimated: 5.2 billion USD, 2024.

- Driver: Regulators and safety programs accelerate deployment, estimated: 2.0 major compliance mandates, 2024. Early ADAS uptake supports steady system integration, estimated: 14.0% annual platform rollout rate, 2024.

- Restraint: Cost and integration complexity slow broad deployment, estimated: 120.0 USD per vehicle, 2024. Data privacy and in-cabin monitoring concerns add compliance friction, estimated: 1.0 high-risk regulatory exposure, 2024.

- Opportunity: AI-enabled telematics and connected fleets expand recurring value, estimated: 3.5 billion USD serviceable software pool, 2034. Cloud analytics enables predictive fatigue scoring, estimated: 25.0% attach-rate, 2034.

- Trend: Lane departure warning systems dominate system-type share at 48.2%, 2024. OEMs increasingly pair camera-based attention monitoring with ADAS stacks, estimated: 60.0% camera-led architectures, 2034.

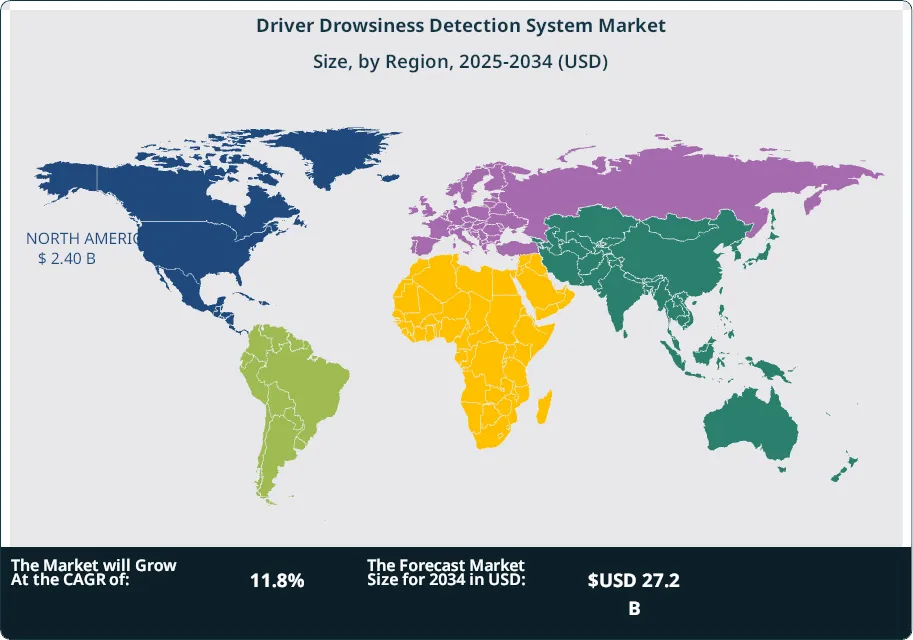

- Regional Analysis: North America leads with 27.6% share and 2.4 billion USD, 2024. Regulation intensity and early adoption sustain growth, estimated: 7.4 billion USD, 2034.

By Type

Hardware-based solutions continue to account for the majority of system deployments as the market moves into 2025. Camera modules, infrared sensors, steering input sensors, and seat-based pressure sensors collectively represented about 68 percent of global revenue in 2024 and remain central to real-time fatigue detection. OEMs prioritize these components due to their reliability in varied lighting and driving conditions, particularly in long-haul and night-time operations. Declining sensor costs and higher production volumes are supporting wider integration across mid-range vehicle platforms.

Software platforms represent the fastest-expanding component layer. Fatigue-detection algorithms, computer vision models, and embedded analytics engines are increasingly embedded into vehicle electronic architectures. Software adoption is strongest in premium and semi-autonomous vehicles, where real-time driver state assessment supports advanced assistance functions. By 2030, software is expected to approach 40 percent of total system value as automakers emphasize updateable, vehicle-wide safety intelligence.

By Application

Passenger-focused safety applications continue to drive volume demand. Driver drowsiness detection is increasingly offered as a standard or bundled feature within ADAS packages, particularly in urban and highway driving scenarios. Passenger vehicles accounted for roughly 58 percent of total installations in 2024, supported by rising safety awareness and regulatory encouragement across developed markets.

Commercial and fleet-based applications are expanding at a faster rate. Logistics operators and public transport providers adopt these systems to reduce accident exposure, insurance costs, and downtime. Integration with fleet telematics enables continuous monitoring and intervention. Adoption remains uneven across regions, but compliance-driven growth is expected to strengthen post-2025 as safety enforcement increases.

By End-Use

Original equipment manufacturers remain the primary end-users, representing more than two-thirds of system demand in 2024. OEM-led integration ensures compliance with safety standards and allows tighter coordination with braking, lane-keeping, and alert systems. Major automakers in North America, Europe, and East Asia continue to expand driver monitoring as part of standardized safety roadmaps.

Fleet operators and mobility service providers represent a growing end-use category. Commercial transport firms increasingly deploy fatigue monitoring to improve driver accountability and operational safety. Aftermarket adoption remains smaller but continues to gain traction in regulated fleet environments where retrofit solutions reduce capital risk.

By Region

North America remains the largest regional market, holding approximately 27.6 percent share and generating about USD 2.4 billion in revenue in 2024. Strong regulatory pressure, early ADAS adoption, and high vehicle ownership rates support continued growth beyond 2025. The United States leads regional demand through both consumer and commercial deployments.

Europe follows closely, supported by mandatory safety regulations and strong OEM compliance. Asia Pacific is projected to deliver the highest growth rate through 2034, driven by rising vehicle production, expanding middle-class ownership, and increasing road safety initiatives in China and India. Latin America and the Middle East and Africa show gradual expansion, constrained by cost sensitivity and uneven enforcement but supported by increasing imports of safety-equipped vehicles.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Hardware devices

- Software systems

By Vehicle Type

- Passenger cars

- Commercial vehicles

By System Type

- Lane Departure warning

- Driver fatigue monitoring

- Driver distraction monitoring

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 10.0 B |

| Forecast Revenue (2034) | USD 27.2 B |

| CAGR (2025-2034) | 11.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Hardware devices, Software systems), By Vehicle Type (Passenger cars, Commercial vehicles), By System Type (Lane Departure warning, Driver fatigue monitoring, Driver distraction monitoring) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Seeing Machines Ltd, Denso Corporation, Magna International Inc., Smart Eye AB, Continental, Aisin Seiki Co., Ltd., Robert Bosch, Hella GmbH & Co., Autoliv Inc., TRW Automotive, Delphi Automotive, Valco |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Vehicle Type (Passenger Cars, Commercial Vehicles), By System Type (Lane Departure Warning Systems, Driver Fatigue Monitoring Systems, Driver Distraction Monitoring Systems), By Technology (AI-Based Monitoring, Infrared Sensors, Camera-Based Systems) Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2025–2034")

, By Vehicle Type (Passenger Cars, Commercial Vehicles), By System Type (Lane Departure Warning Systems, Driver Fatigue Monitoring Systems, Driver Distraction Monitoring Systems), By Technology (AI-Based Monitoring, Infrared Sensors, Camera-Based Systems) Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2025–2034")

, By Vehicle Type (Passenger Cars, Commercial Vehicles), By System Type (Lane Departure Warning Systems, Driver Fatigue Monitoring Systems, Driver Distraction Monitoring Systems), By Technology (AI-Based Monitoring, Infrared Sensors, Camera-Based Systems) Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2025–2034")

Frequently Asked Questions

How big is the Driver Drowsiness Detection System Market?

The Global Driver Drowsiness Detection System Market was valued at USD 8.9 Billion in 2024 and is projected to reach USD 27.2 Billion by 2034, growing at a CAGR of 11.8% from 2026–2034. Explore key trends, ADAS integration, road safety innovations, market drivers, and future growth opportunities in automotive safety systems.

Who are the major players in the Driver Drowsiness Detection System Market?

Seeing Machines Ltd, Denso Corporation, Magna International Inc., Smart Eye AB, Continental, Aisin Seiki Co., Ltd., Robert Bosch, Hella GmbH & Co., Autoliv Inc., TRW Automotive, Delphi Automotive, Valco

Which segments covered the Driver Drowsiness Detection System Market?

By Product Type (Hardware devices, Software systems), By Vehicle Type (Passenger cars, Commercial vehicles), By System Type (Lane Departure warning, Driver fatigue monitoring, Driver distraction monitoring)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Driver Drowsiness Detection System Market

Published Date : 05 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date