- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Drone-Assisted Smart Agriculture Market to Hit $20.2B by 2034 | CAGR 14.5%

Global Drone-Assisted Smart Agriculture Market Size, Share, Analysis Report By Type (Fixed-wing Drones, Rotary-wing Drones, Hybrid Drones), Application (Crop Monitoring, Precision Spraying, Soil Analysis, Livestock Monitoring, Crop Health Assessment), Component (Hardware, Software, Services), Farm Size (Small-scale Farms, Medium-scale Farms, Large-scale Farms), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview

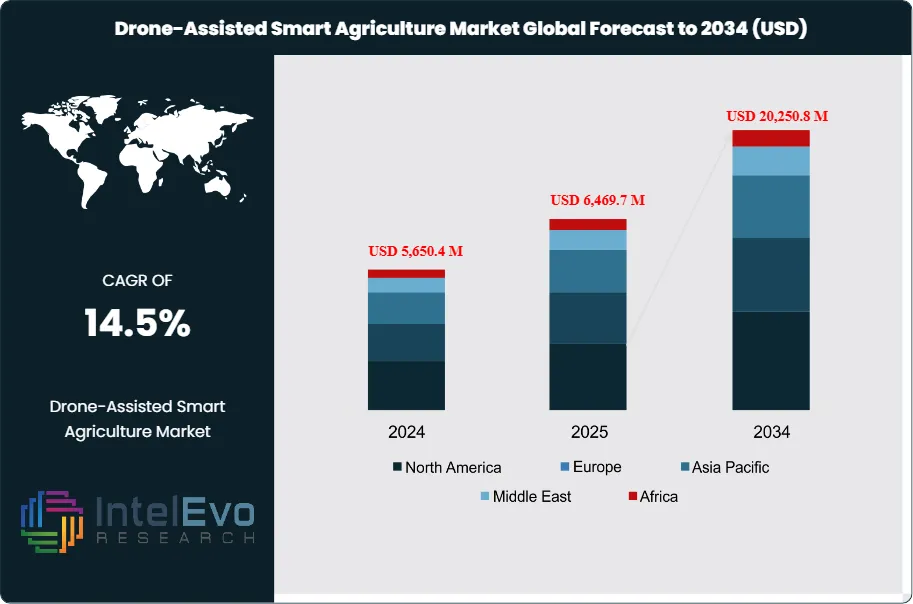

The Global Drone-Assisted Smart Agriculture Market size is expected to be worth around USD 20,250.8 million by 2034, from USD 5,650.4 million in 2024, growing at a CAGR of 14.5% during the forecast period from 2024 to 2034. The rising adoption of precision farming, AI-driven crop monitoring, and government support for agri-tech innovations are fueling this growth. Drones are transforming agriculture by enhancing efficiency, reducing operational costs, and enabling real-time data-driven decision-making, making them a game-changer for sustainable farming worldwide.

Get More Information about this report -

Request Free Sample ReportThe Global Market for Smart Agriculture using Drones includes a variety of unmanned aerial vehicles used in farming to improve productivity, efficiency, and sustainability. Farmers use drones for tasks like monitoring crops, spraying pesticides accurately, and analyzing soil to help them make decisions based on data. The present market is marked by fast technological progress, like enhanced sensors and AI integration, making drone operations more efficient and attainable. With the rise of technology in agriculture, the need for drone-assisted solutions has increased, highlighting the benefits they bring in enhancing resource efficiency and boosting crop production.

The market's expansion is driven by various important factors, such as the rising use of precision farming methods to optimize agricultural production and reduce resource inefficiency. The demand for drone technology is driven by factors like the requirement for better crop health monitoring, pest control, and effective irrigation practices. Furthermore, the increasing attention on sustainable farming, driven by environmental issues and government benefits, has also boosted market expansion. Expectations point to increased market potential in the future due to investments in drone research and development, as well as the growth of service providers offering drone-related agricultural services. Moreover, the lower cost of drones and the accessibility of specialized software are set to draw in a wider variety of users.

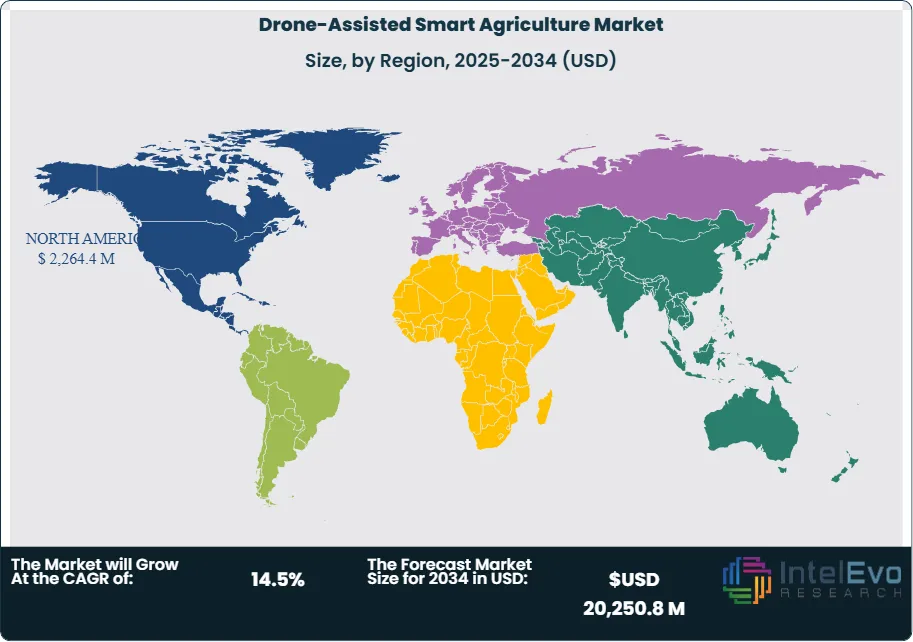

North America is the top in the drone-supported smart farming sector due to high-tech agricultural methods and substantial tech funding. The United States has seen widespread use of drones by farmers because of favorable regulations and a focus on innovation, in particular. Europe, including nations such as Germany and France, actively supports precision agriculture programs. At the same time, the Asia-Pacific area is expected to see rapid growth because of rising agricultural needs, especially in nations like China and India, where the use of technology in farming is increasing. This diversification in the region provides chances for market participants to enter developing markets.

The drone-assisted smart agriculture market has been significantly affected by the various aspects of the COVID-19 pandemic. Supply chain interruptions initially caused a lack of drones and related technologies, but the pandemic highlighted the need for effective agricultural practices to guarantee food security. Farmers are more and more using technology like drones to remotely monitor crops and reduce their reliance on labor. Furthermore, the pandemic expedited the acceptance of digital solutions in agriculture, leading to a continued transition towards automation and data-based farming methods. Therefore, the market is ready for strong recovery and expansion as stakeholders adopt new technologies in the post-pandemic environment.

, Application (Crop Monitoring, Precision Spraying, Soil Analysis, Livestock Monitoring, Crop Health Assessment), Component (Hardware, Software, Services), Farm Size (Small-scale Farms, Medium-scale Farms, Large-scale Farms), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways

- Market Growth: The drone-assisted smart agriculture market is projected to reach USD 19,545.5 million by 2034, growing at a robust CAGR of 14.0%, indicating strong market expansion driven by technological advancements and increasing adoption among farmers.

- Type Segment Analysis: Fixed-wing drones dominate the market due to their longer flight time and ability to cover larger areas efficiently. They are particularly useful for crop monitoring and mapping applications, enhancing operational efficiency in agriculture.

- Application Segment Analysis: Crop monitoring holds the largest share within the application segment. Drones enable real-time monitoring of crop health, allowing farmers to make data-driven decisions and optimize resource allocation, significantly improving yield.

- Driver: The increasing need for precision agriculture is a key driver for market growth, as farmers seek efficient solutions to enhance productivity and reduce resource waste, responding to rising food demand and environmental sustainability pressures.

- Restraint: High initial investment costs and regulatory challenges in drone operations may hinder market growth. Farmers may be deterred by the financial barrier associated with adopting drone technology, especially in developing regions.

- Opportunity: The rising trend of digital agriculture in emerging markets presents significant growth opportunities. As farmers adopt technology for improved crop management, the demand for drone services and solutions is expected to increase substantially.

- Trend: Integration of AI and machine learning in drone technology is becoming prevalent, enhancing data analytics capabilities for better decision-making in agricultural practices.

- Regional Analysis: North America is currently the leading region, driven by advanced agricultural practices and supportive regulations. However, Asia-Pacific is anticipated to witness the fastest growth, fueled by increasing agricultural demands and technology adoption in countries like China and India.

Type:

The smart agriculture market aided by drones is mainly divided into fixed-wing, rotary-wing, and hybrid drones. Fixed-wing drones are recognized for their extended flight durations and capability to efficiently cover vast areas, making them well-suited for activities like crop mapping and surveillance. They are usually utilized in bigger farms that require wide-ranging coverage. Quadcopters, also known as rotary-wing drones, provide increased agility and are ideal for tasks that demand accuracy, like precise crop spraying and targeted crop inspections. Hybrid drones mix attributes from both kinds, offering flexibility for different farming duties. The various requirements of the agricultural industry fuel the need for these distinct types of drones, each created to fulfill specific operational needs.

Application:

Drone technology in agriculture can be used for monitoring crops, spraying with precision, analyzing soil, monitoring livestock, and assessing crop health. Crop monitoring is a major use case, enabling farmers to collect up-to-date information on crop status, enabling prompt actions. Precision spraying improves the effectiveness of applying pesticides and fertilizers, decreasing both wastage and environmental harm. Examining soil with drones can assist in comprehending soil makeup and condition, leading to improved land management techniques. Livestock surveillance offers understanding of animal well-being and actions, allowing for improved herd overseeing. Every application highlights the usefulness of drones in enhancing operational efficiency and decision-making, ultimately boosting agricultural productivity.

Component:

The market is divided into segments based on elements such as hardware, software, and services. Hardware includes the drones themselves, along with a variety of sensors and imaging technologies that are necessary for agricultural activities. The software component consists of tools for analyzing and managing data gathered by drones, enabling farmers to make informed decisions through analytics. Services such as training, maintenance, and support are provided to help users effectively deploy and manage drone technologies in their agricultural practices. This part is important because it shows the comprehensive approach required to incorporate drones into current agricultural practices, highlighting the significance of both technology and service elements in order to achieve successful adoption.

Farm Size:

Farm size classification comprises of small-scale, medium-scale, and large-scale farms. Small farms with few resources are more and more using drones to improve efficiency and increase productivity. Medium-sized farms take advantage of drones to enhance crop management and monitoring efficiency. Big farms use drone technology extensively for thorough monitoring and management over wide areas, allowing accurate application of resources. With the changing landscape of agriculture, the use of drones differs depending on the size of the farm, aligning with the unique demands and capabilities of different farming activities. Drone solutions are versatile and can be used on farms of all sizes, leading to their widespread use in agriculture.

Region Analysis:

North America Leads With Significant Market Share in Drone-Assisted Smart Agriculture: North America holds the largest share of the drone-assisted smart agriculture market, accounting for approximately 35% of the total market. This dominance can be attributed to several factors, including advanced technological infrastructure, significant investments in agricultural R&D, and a strong emphasis on precision agriculture. The United States, in particular, is at the forefront of adopting drone technology for farming, leveraging its vast agricultural landscape and innovative farming techniques. The presence of major drone manufacturers and service providers further enhances the market landscape, driving competition and technological advancements. Additionally, supportive government regulations and initiatives aimed at promoting sustainable farming practices contribute to the region's market leadership, making it a key player in the global drone-assisted smart agriculture landscape.

Asia-Pacific is rapidly becoming the fastest-growing region in the drone-assisted smart agriculture market, with a projected growth rate exceeding 16% CAGR during the forecast period. This growth is fueled by increasing agricultural demands driven by population growth, the need for enhanced productivity, and the adoption of modern farming practices in countries like China and India. The region's diverse agricultural landscape offers significant opportunities for drone applications, ranging from crop monitoring to precision spraying. Moreover, the rise of digital agriculture initiatives and government support for technology adoption are key drivers behind this growth. In contrast, Europe and Latin America are witnessing steady growth, focusing on sustainable agriculture practices, while the Middle East and Africa are gradually adopting drone technology to address unique agricultural challenges and enhance food security in their respective regions.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Drone Type:

- Fixed-Wing Drones

- Rotary Blade Drones

- Hybrid Drones

By Component:

- Hardware

- Software

- Services

By Technology:

- AI & Machine Learning Integration

- IoT-Enabled Drones

- GPS & Remote Sensing

- Cloud-Based Analytics

By Farm Size:

- Small Farms

- Medium Farms

- Large Farms

By End-User:

- Farmers & Growers

- Agribusiness Companies

- Research Institutes

- Government & NGOs

By Application:

- Crop Monitoring & Precision Agriculture

- Livestock Monitoring

- Irrigation Management

- Soil & Field Analysis

- Planting & Seeding

- Pesticide & Fertilizer Spraying

- Others

By Region:

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6,469.7 M |

| Forecast Revenue (2034) | USD 20,250.8 M |

| CAGR (2025-2034) | 14.5% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Drone Type: (Fixed-Wing Drones, Rotary Blade Drones, Hybrid Drones), By Component: (Hardware, Software, Services), By Technology: (AI & Machine Learning Integration, IoT-Enabled Drones, GPS & Remote Sensing, Cloud-Based Analytics), By Farm Size: (Small Farms, Medium Farms, Large Farms), By End-User: (Farmers & Growers, Agribusiness Companies, Research Institutes, Government & NGOs), By Application: (Crop Monitoring & Precision Agriculture, Livestock Monitoring, Irrigation Management, Soil & Field Analysis, Planting & Seeding, Pesticide & Fertilizer Spraying, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Deere & Company, Trimble Inc., Raven Industries, Topcon Positioning Systems, Autonomous Solutions Inc., DeLaval Inc., Farmers Edge Inc., BouMatic Robotic B.V., AgJunction Inc., AGCO Corporation, DroneDeploy, PrecisionHawk, Yamaha Motor Corporation, senseFly (Parrot Drones), AeroVironment, Skycatch, Terra Drone Corporation, Pictometry International Corp., Groupe ADP, DNV GL |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Application (Crop Monitoring, Precision Spraying, Soil Analysis, Livestock Monitoring, Crop Health Assessment), Component (Hardware, Software, Services), Farm Size (Small-scale Farms, Medium-scale Farms, Large-scale Farms), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Application (Crop Monitoring, Precision Spraying, Soil Analysis, Livestock Monitoring, Crop Health Assessment), Component (Hardware, Software, Services), Farm Size (Small-scale Farms, Medium-scale Farms, Large-scale Farms), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Application (Crop Monitoring, Precision Spraying, Soil Analysis, Livestock Monitoring, Crop Health Assessment), Component (Hardware, Software, Services), Farm Size (Small-scale Farms, Medium-scale Farms, Large-scale Farms), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Drone-Assisted Smart Agriculture Market?

The Global Drone-Assisted Smart Agriculture Market is projected to reach USD 20.2 billion by 2034, growing at a CAGR of 14.5%. Rising adoption of precision farming, AI-driven crop monitoring, and sustainable farming solutions is driving rapid market expansion.

Who are the major players in the Drone-Assisted Smart Agriculture Market?

Deere & Company, Trimble Inc., Raven Industries, Topcon Positioning Systems, Autonomous Solutions Inc., DeLaval Inc., Farmers Edge Inc., BouMatic Robotic B.V., AgJunction Inc., AGCO Corporation, DroneDeploy, PrecisionHawk, Yamaha Motor Corporation, senseFly (Parrot Drones), AeroVironment, Skycatch, Terra Drone Corporation, Pictometry International Corp., Groupe ADP, DNV GL

Which segments covered the Drone-Assisted Smart Agriculture Market?

By Drone Type: (Fixed-Wing Drones, Rotary Blade Drones, Hybrid Drones), By Component: (Hardware, Software, Services), By Technology: (AI & Machine Learning Integration, IoT-Enabled Drones, GPS & Remote Sensing, Cloud-Based Analytics), By Farm Size: (Small Farms, Medium Farms, Large Farms), By End-User: (Farmers & Growers, Agribusiness Companies, Research Institutes, Government & NGOs), By Application: (Crop Monitoring & Precision Agriculture, Livestock Monitoring, Irrigation Management, Soil & Field Analysis, Planting & Seeding, Pesticide & Fertilizer Spraying, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Drone-Assisted Smart Agriculture Market

Published Date : 12 Dec 2024 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date