- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Drug Safety Database Market Size, Share & Forecast | CAGR 11.1%

Global Drug Safety Database Market Size, Share, Growth Analysis By Deployment Mode (Cloud-Based/SaaS, On-Premise, Hybrid), By Application (Adverse Event Management, Signal Detection & Risk Management, Aggregate Reporting, Literature Monitoring & Case Processing), By Software Type, By End-User (Pharmaceutical Companies, CROs, Medical Device Manufacturers, Regulatory Bodies), Industry Trends, Competitive Landscape & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

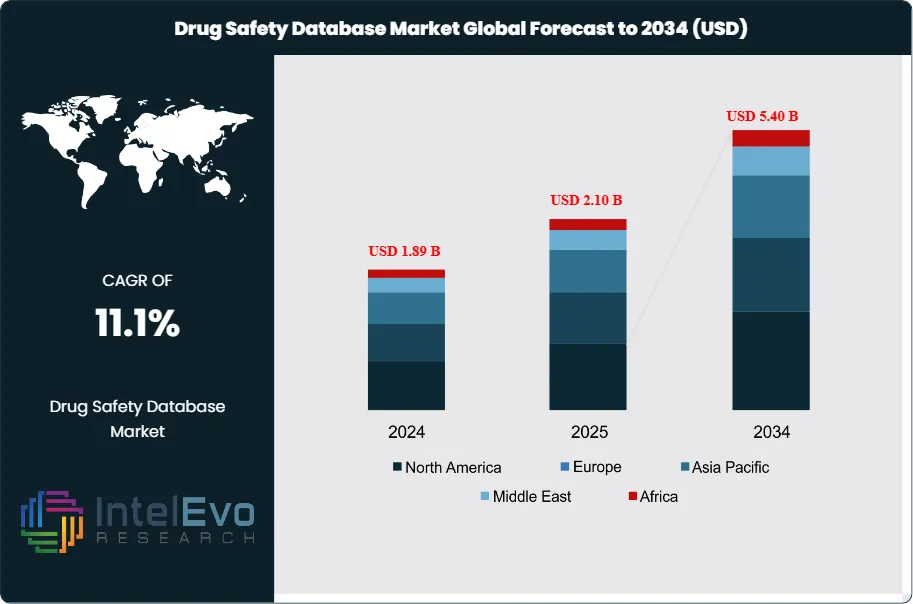

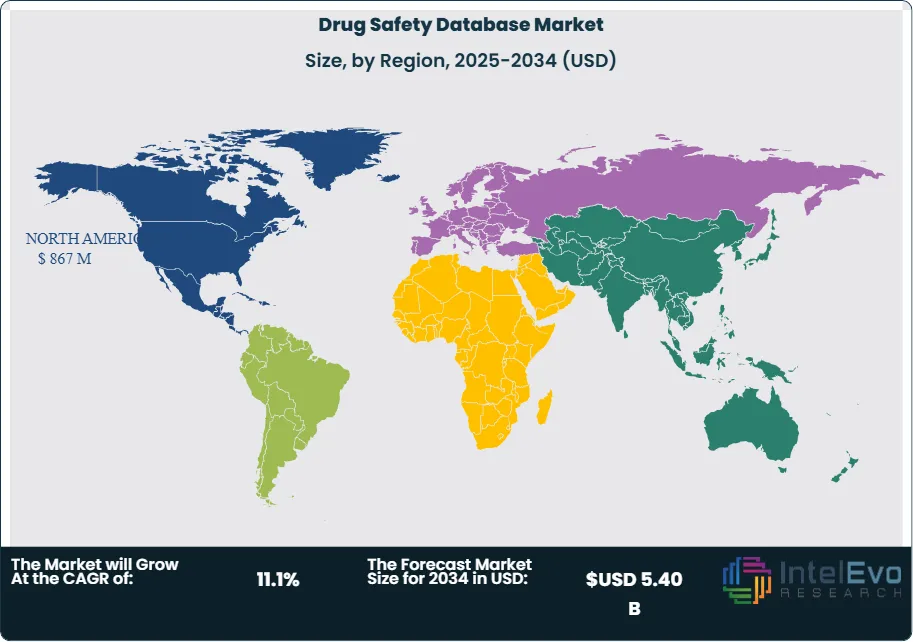

| USD 2.10 Billion | USD 5.40 Billion | 11.1% | North America, 41.3% |

The Drug Safety Database Market was valued at approximately USD 1.89 Billion in 2024 and reached USD 2.10 Billion in 2025. The market is projected to grow to USD 5.40 Billion by 2034, expanding at a CAGR of 11.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.30 Billion over the analysis period, driven by the intensifying global regulatory mandate for pharmacovigilance and the accelerating shift from on-premise legacy systems to cloud-native safety platforms.

Get More Information about this report -

Request Free Sample ReportDrug safety databases serve as the backbone of pharmacovigilance operations across the pharmaceutical, biotechnology, and medical device industries. These systems capture, process, evaluate, and report adverse events from clinical trials, post-marketing surveillance programs, and spontaneous reporting networks. Demand has expanded materially since the FDA's Safety Reporting Requirements for INDs and BA/BE studies (21 CFR Parts 312 and 320) were updated, and since the European Medicines Agency mandated ICH E2B(R3) electronic data exchange standards for all Individual Case Safety Reports submitted to EudraVigilance. Trade data and regulatory filings suggest that the volume of Individual Case Safety Reports processed globally exceeded 22 million in 2024, a 31% increase from 2019 levels, creating a direct structural pull on database processing capacity and vendor software development investment.

The drug safety database market is experiencing a technology inflection driven by artificial intelligence and natural language processing. AI-powered case triage, automated MedDRA coding, and generative narrative generation are compressing adverse event processing times from an industry average of 4.2 hours per case to under 50 minutes at leading adopter sites. Cloud-based deployment, which holds 44.8% of 2025 market share, is the fastest-growing delivery model as pharmaceutical sponsors seek scalable pharmacovigilance infrastructure without the capital expenditure associated with on-premise installations.

North America accounts for 41.3% of 2025 global market revenue, supported by the concentration of large pharmaceutical manufacturers, the FDA's escalating pharmacovigilance enforcement activity, and the highest base of contract research organization capacity globally. Europe follows with 27.8% share, driven by EMA compliance obligations and active PSUR submission requirements under the EU pharmacovigilance legislation enacted in 2012 and subsequently reinforced through Good Pharmacovigilance Practices (GVP) modules. Asia Pacific is the fastest-growing regional market, with India's contract research organization sector and China's NMPA pharmacovigilance reform agenda serving as primary growth catalysts. The drug safety database market remains moderately consolidated, with Oracle, IQVIA, Veeva, and ArisGlobal (Cognizant) together commanding approximately 58% of 2025 global revenue.

, By Application (Adverse Event Management, Signal Detection & Risk Management, Aggregate Reporting, Literature Monitoring & Case Processing), By Software Type, By End-User (Pharmaceutical Companies, CROs, Medical Device Manufacturers, Regulatory Bodies), Industry Trends, Competitive Landscape & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global drug safety database market was valued at USD 2.10 Billion in 2025 and is projected to reach USD 5.40 Billion by 2034, at a CAGR of 11.1% for 2026–2034.

- Segment Dominance: Cloud-based deployment holds the largest share at 44.8% of 2025 market revenue, as pharmaceutical and biotech sponsors migrate from legacy on-premise systems to subscription-based SaaS pharmacovigilance platforms.

- Segment Dominance: Adverse event and case management is the leading application segment at 38.4% of 2025 market revenue, anchored by global regulatory requirements mandating structured capture and expedited reporting of serious adverse drug reactions.

- Driver: Escalating global pharmacovigilance regulations, including ICH E2B(R3) mandates and EMA GVP module requirements, are forcing pharmaceutical manufacturers to upgrade database infrastructure; the volume of Individual Case Safety Reports processed globally exceeded 22 million in 2024, a 31% increase over 2019.

- Restraint: High implementation and validation costs for drug safety database systems — typically USD 500,000 to USD 2.5 Million for enterprise-grade on-premise deployments — restrict adoption among small and mid-size pharmaceutical companies and emerging biotech organizations.

- Opportunity: The integration of real-world evidence and electronic health record data into pharmacovigilance workflows represents an estimated USD 680 Million incremental opportunity by 2030, as regulators including the FDA and EMA formally recognize real-world safety data in risk-benefit assessments.

- Trend: AI-powered case processing automation is the dominant trend; early adopter pharmaceutical organizations report a 62% to 78% reduction in median triage time per case compared to manual processing workflows, driving accelerating enterprise contract conversions across the sector.

- Regional Analysis: North America leads the drug safety database market with 41.3% of 2025 global revenue, equivalent to approximately USD 867 Million, underpinned by FDA pharmacovigilance enforcement activity and dense pharmaceutical R&D and post-marketing infrastructure.

Competitive Landscape Overview

The drug safety database market is moderately consolidated, with the top four vendors — Oracle Health Sciences, IQVIA Holdings, Veeva Systems, and Cognizant (ArisGlobal) — collectively commanding approximately 58% of global 2025 revenue. Competition is platform-driven, with vendors differentiating on regulatory rule library breadth, AI-enabled automation, cloud-native architecture, and global submission coverage. M&A activity intensified between 2023 and 2025, including Cognizant's integration of ArisGlobal's LifeSphere platform and Dassault Systèmes' deeper embedding of Medidata Safety into its life sciences suite. AI-native functionality has become the primary basis for enterprise contract conversions, with vendors investing heavily in automated MedDRA coding, narrative generation, and signal detection capabilities.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Oracle Health Sciences | USA | Leader | Argus Safety | North America | Released Argus Safety Cloud 9.2 with AI-driven signal detection and real-time EMA eXEVMPD integration (Feb 2025) |

| IQVIA Holdings | USA | Leader | IQVIA ARISg / Insight | Global | Expanded ARISg cloud platform with automated aggregate reporting for ICH E2B(R3); added 14 new country-specific regulatory rule libraries (Jan 2025) |

| Veeva Systems | USA | Challenger | Veeva Vault Safety | North America | Launched Vault Safety 25R1 with generative AI case processing and automated MedDRA coding engine (Apr 2025) |

| Cognizant (ArisGlobal) | USA | Challenger | LifeSphere Safety | Global | Integrated AI-powered narrative generation into LifeSphere Safety; signed 8 new Tier-1 pharma enterprise agreements (Mar 2025) |

| Ennov | France | Niche Player | Ennov Clinical Safety | Europe | Launched Ennov Safety 10.0 with native EudraVigilance gateway and automated SUSAR submission workflows (Jun 2025) |

| Samarind (Tata Consultancy Services) | UK | Niche Player | Samarind Pharmacovigilance Suite | Europe | Expanded UK and EU deployment capacity following post-Brexit regulatory divergence; added EMA MDR module (Sep 2025) |

| EXTEDO | Germany | Niche Player | EURS / PharmaReady | Europe | Released EURS 6.5 with HL7 FHIR-compliant safety data exchange for hospital pharmacovigilance networks (Jan 2026) |

| Relsys International | India | Niche Player | PVWorks | Asia Pacific | Secured multi-year contract with three Indian CDMO clients for cloud PV database deployment; launched PVWorks 4.0 (Oct 2025) |

| Max Neelsen (bioclinica legacy) | USA | Niche Player | SafetyComplete | North America | Launched AI triage module for expedited case classification; integrated real-world evidence feed from EHR networks (May 2025) |

| Medidata (Dassault Systèmes) | USA | Niche Player | Medidata Safety | North America | Integrated Medidata Safety with Rave EDC for direct clinical trial adverse event capture; 22 new sponsor sites onboarded (Feb 2025) |

By Deployment Mode

Cloud-based and SaaS deployment is the dominant modality in the drug safety database market, holding 44.8% of 2025 global revenue. The structural shift toward cloud delivery accelerated between 2020 and 2025 as pharmaceutical manufacturers sought to reduce the validation burden associated with on-premise system upgrades under 21 CFR Part 11 and EU Annex 11 GxP requirements. Cloud platforms remove the need for internal hardware management and allow continuous regulatory rule library updates without formal change control validation cycles for each update. Current market assessment shows that cloud-based pharmacovigilance deployments reduce average total cost of ownership by 32% to 44% over a five-year horizon compared to equivalent on-premise installations. Major vendors including Veeva, IQVIA, and ArisGlobal have rebuilt their primary commercial offerings as cloud-native products, signaling a structural rather than cyclical shift in delivery preference. Remaining on-premise deployments, which hold 33.2% of 2025 market share, are concentrated among the largest global pharmaceutical companies with proprietary compliance frameworks, legacy data migration constraints, and data sovereignty requirements in specific markets. Hybrid deployment models account for 22.0% of 2025 revenue and are growing fastest among mid-size specialty pharmaceutical companies that retain on-premise archives for historical safety data while processing new cases on cloud infrastructure.

By Application

Adverse event and case management is the largest application segment in the drug safety database market, commanding 38.4% of 2025 global revenue. This category encompasses the full individual case safety report lifecycle, from intake and medical review through MedDRA coding, narrative writing, regulatory causality assessment, and submission to national competent authorities and the FDA's MedWatch system. The regulatory obligation for expedited reporting of serious unexpected adverse drug reactions — within 7 days for fatal or life-threatening events and 15 days for other serious events under ICH E2D — creates non-discretionary demand for this application tier. Signal detection and risk management accounts for 26.7% of 2025 market share and encompasses quantitative signal detection algorithms, disproportionality analysis, and benefit-risk evaluation platforms. This segment is growing faster than case management as regulators including the EMA and FDA place greater emphasis on proactive signal management and Risk Management Plan execution. Aggregate reporting, covering periodic safety update reports, periodic benefit-risk evaluation reports, and development safety update reports, holds 18.9% of 2025 revenue. Literature monitoring and case processing — encompassing systematic literature search automation, duplicate detection, and global case intake from partner networks — represents the remaining 12.6% of 2025 market share and is the fastest-growing application sub-segment by percentage, driven by ICH M9 and EMA literature monitoring guideline requirements.

By Software Type

Standalone drug safety software products hold the largest share within the software type dimension at 52.3% of 2025 global market revenue. These purpose-built pharmacovigilance platforms, including Oracle Argus Safety, IQVIA ARISg, and ArisGlobal LifeSphere, are designed specifically for adverse event processing, regulatory submission, and global case management workflows. Their depth of regulatory rule library coverage, validated submission gateway connectivity, and established audit history in FDA inspections make them the default choice for pharmaceutical companies managing large product portfolios across multiple jurisdictions. Integrated safety and electronic data capture suites account for 30.4% of 2025 market share and are gaining ground as pharmaceutical sponsors seek to eliminate manual transcription of clinical trial adverse events between EDC systems and safety databases. Veeva's integration of Vault Safety with Vault CDMS and Medidata's Safety-Rave EDC link represent the primary commercial implementations of this architecture. Pharmacovigilance services platforms — software-as-a-service offerings that bundle database access with outsourced case processing and regulatory submission services — hold the remaining 17.3% of 2025 market share and are particularly relevant for emerging biotech companies without internal pharmacovigilance operations.

By End-User

Pharmaceutical and biotech companies represent the dominant end-user cohort in the drug safety database market, generating 47.2% of 2025 global revenue. This group spans innovator pharmaceutical manufacturers with large post-marketing safety obligations, specialty pharma companies managing complex biologics portfolios, and clinical-stage biotech organizations with IND-phase safety reporting requirements. The post-approval pharmacovigilance obligations associated with a standard New Drug Application — including MedWatch reporting, Periodic Adverse Drug Experience Reports, and Risk Evaluation and Mitigation Strategy submissions — sustain recurring annual software expenditure that is independent of R&D pipeline performance. Contract research organizations account for 24.6% of 2025 market share and represent the fastest-growing end-user segment by absolute revenue, driven by the outsourcing of pharmacovigilance operations from both large pharmaceutical companies and emerging biotechs to specialized CROs. Medical device and diagnostics manufacturers hold 18.3% of 2025 revenue, propelled by expanding post-market surveillance obligations under the EU Medical Device Regulation and the FDA's updated postmarket safety reporting requirements under 21 CFR Part 803. Regulatory and government agencies, including national pharmacovigilance centers and the WHO Uppsala Monitoring Centre, account for the remaining 9.9% of 2025 market revenue.

Regional Analysis

North America

North America leads the global drug safety database market with 41.3% of 2025 revenue, equivalent to approximately USD 867 Million. The United States is the dominant national market, driven by the world's largest pharmaceutical industry base, the FDA's active pharmacovigilance enforcement program, and the concentration of global CRO capacity in Research Triangle, Philadelphia, and the San Francisco Bay Area. The FDA's 2024 pharmacovigilance strategic plan, which accelerated timelines for MedWatch integration and expanded real-world evidence use in post-market safety reviews, has directly stimulated investment in upgraded database infrastructure at large pharmaceutical companies. FDA warning letters citing inadequate adverse event reporting procedures more than doubled between 2020 and 2024, creating compliance urgency that has accelerated drug safety database contract renewals and system upgrades. Canada contributes a meaningful share through pharmaceutical manufacturer subsidiaries and a well-developed CRO sector, while Health Canada's alignment with ICH pharmacovigilance guidelines ensures demand for the same class of platforms used in the United States. Mexico's growing pharmaceutical manufacturing base, particularly in Jalisco and Mexico City, is beginning to generate demand for cloud-based pharmacovigilance infrastructure as COFEPRIS strengthens post-marketing surveillance requirements.

Europe

Europe holds 27.8% of 2025 global drug safety database market revenue, approximately USD 584 Million. The region operates under one of the world's most demanding pharmacovigilance regulatory frameworks, anchored by the EU Pharmacovigilance Legislation of 2012 (Directive 2010/84/EU and Regulation EU 1235/2010) and the EMA's Good Pharmacovigilance Practices modules covering signal management, PSUR submission, and benefit-risk evaluation. Germany is the continent's largest single national market, driven by the domestic pharmaceutical industry cluster including Bayer, Boehringer Ingelheim, and Merck KGaA, each maintaining substantial internal pharmacovigilance operations. France follows as the second-largest European market through ANSM pharmacovigilance obligations and a significant CRO industry base. The United Kingdom, operating under MHRA-specific pharmacovigilance requirements since Brexit, represents a distinct compliance market that has created demand for dual-submission capability within drug safety databases — handling both UK and EU reporting simultaneously. Switzerland contributes through Swissmedic obligations and the global pharmacovigilance headquarters of Roche, Novartis, and several specialty pharma companies. The EMA's ongoing digitalization of pharmacovigilance, including its DARWIN EU real-world evidence program and updated EudraVigilance data-quality assurance framework, continues to drive software investment across European pharmaceutical companies.

Asia Pacific

Asia Pacific accounts for 20.4% of 2025 global drug safety database market revenue, approximately USD 428 Million, and is the fastest-growing major region with an estimated regional CAGR exceeding 14% through 2034. Japan is the most technically mature national market in the region, with the Pharmaceuticals and Medical Devices Agency maintaining strict pharmacovigilance submission standards and a well-established adverse event reporting culture among domestic pharmaceutical manufacturers. China is the highest-growth single market, driven by the NMPA's 2019 pharmacovigilance regulations that brought Chinese post-marketing safety requirements into alignment with ICH E2 guidelines, creating mandatory adverse event database infrastructure obligations for all domestic and multinational marketing authorization holders operating in China. India is the most significant long-term growth driver, where the expansion of domestic CRO capacity — particularly for global clinical trial management and pharmacovigilance outsourcing — is generating demand for enterprise-grade safety database platforms at organizations such as Parexel India, Syneos Health India, and Lambda Therapeutic Research. South Korea's pharmaceutical and medical device sector, including Samsung Biologics and Celltrion, is investing in pharmacovigilance database infrastructure to support MFDS post-market surveillance obligations and global regulatory submissions.

Latin America

Latin America represents 6.2% of 2025 global drug safety database market revenue, approximately USD 130 Million. Brazil is the dominant national market in the region, supported by ANVISA's pharmacovigilance system — one of the most structured in Latin America — which mandates regular adverse event reporting for all marketed pharmaceutical products and requires formal pharmacovigilance system master files for new product registrations. The Brazilian pharmaceutical generic manufacturing sector, which accounts for more than 60% of domestic pharmaceutical volume by units, is a source of incremental demand for cloud-based pharmacovigilance platforms as mid-size manufacturers seek compliance solutions without enterprise-scale infrastructure. Mexico contributes meaningfully through COFEPRIS obligations and the operations of multinational pharmaceutical subsidiaries. Argentina's pharmacovigilance authority, ANMAT, has been progressively strengthening post-marketing surveillance requirements, creating demand among domestic manufacturers and distributor subsidiaries. The region's overall drug safety database market growth is moderated by healthcare budget constraints and variable regulatory enforcement intensity across national competent authorities, though growing harmonization through the Pan American Network for Drug Regulatory Harmonization is gradually elevating baseline compliance standards.

Middle East & Africa

The Middle East and Africa region accounts for 4.3% of 2025 global drug safety database market revenue, approximately USD 90 Million. The UAE is the most active market in the region, driven by the Dubai Health Authority and MOHAP pharmacovigilance requirements and the presence of international pharmaceutical regional headquarters in Dubai and Abu Dhabi. Saudi Arabia is the largest absolute pharmaceutical market in the region, and the Saudi Food and Drug Authority's pharmacovigilance guidelines — which align closely with ICH E2 standards — have created mandatory adverse event database obligations for marketing authorization holders. South Africa is the most technically developed African market, with the South African Health Products Regulatory Authority maintaining structured spontaneous reporting requirements and pharmacovigilance system expectations for registered products. The broader African continent represents a nascent but growing demand segment, driven by the African Medicines Regulatory Harmonisation initiative and World Health Organization technical assistance programs that are gradually building national pharmacovigilance infrastructure across WHO member states. Gulf Cooperation Council regulatory harmonization efforts, particularly GCC harmonized pharmacovigilance requirements, are expanding the addressable market for standardized drug safety database platforms across the region.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment Mode

- Cloud-Based / SaaS

- On-Premise

- Hybrid

By Application

- Adverse Event / Case Management

- Signal Detection & Risk Management

- Aggregate Reporting (PSUR/PBRER/DSUR)

- Literature Monitoring & Case Processing

By Software Type

- Standalone Drug Safety Software

- Integrated Safety-EDC Suite

- Pharmacovigilance Services Platform

By End-User

- Pharmaceutical & Biotech Companies

- Contract Research Organizations (CROs)

- Medical Device & Diagnostics Manufacturers

- Regulatory & Government Bodies

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.10 B |

| Forecast Revenue (2034) | USD 5.40 B |

| CAGR (2025-2034) | 11.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment Mode, (Cloud-Based / SaaS, On-Premise, Hybrid), By Application, (Adverse Event / Case Management, Signal Detection & Risk Management, Aggregate Reporting (PSUR/PBRER/DSUR), Literature Monitoring & Case Processing), By Software Type, (Standalone Drug Safety Software, Integrated Safety-EDC Suite, Pharmacovigilance Services Platform), By End-User, (Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs), Medical Device & Diagnostics Manufacturers, Regulatory & Government Bodies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ORACLE HEALTH SCIENCES, IQVIA HOLDINGS, VEEVA SYSTEMS, COGNIZANT (ARISGLOBAL), ENNOV, SAMARIND (TATA CONSULTANCY SERVICES), EXTEDO GMBH, RELSYS INTERNATIONAL, MEDIDATA SOLUTIONS (DASSAULT SYSTÈMES), MAX NEELSEN / SAFETYCOMPLETE, SYMSOFT AB, COMPREHEND SYSTEMS, PHARMALEX GMBH, OMNIXUS (CLINTEC), UL SOLUTIONS (PHARMACOVIGILANCE DIVISION), AB SCIENCE SA (INTERNAL SAFETY), SCINAI IMMUNOTHERAPEUTICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Adverse Event Management, Signal Detection & Risk Management, Aggregate Reporting, Literature Monitoring & Case Processing), By Software Type, By End-User (Pharmaceutical Companies, CROs, Medical Device Manufacturers, Regulatory Bodies), Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Application (Adverse Event Management, Signal Detection & Risk Management, Aggregate Reporting, Literature Monitoring & Case Processing), By Software Type, By End-User (Pharmaceutical Companies, CROs, Medical Device Manufacturers, Regulatory Bodies), Industry Trends, Competitive Landscape & Forecast 2026-2034")

, By Application (Adverse Event Management, Signal Detection & Risk Management, Aggregate Reporting, Literature Monitoring & Case Processing), By Software Type, By End-User (Pharmaceutical Companies, CROs, Medical Device Manufacturers, Regulatory Bodies), Industry Trends, Competitive Landscape & Forecast 2026-2034")

Frequently Asked Questions

How big is the Drug Safety Database Market?

The Global Drug Safety Database Market was valued at USD 1.89 Billion in 2024 and is projected to reach USD 5.40 Billion by 2034, growing at a CAGR of 11.1% from 2026 to 2034, driven by rising pharmacovigilance requirements, increasing adverse event reporting, and growing adoption of AI-powered drug safety management solutions.

Who are the major players in the Drug Safety Database Market?

ORACLE HEALTH SCIENCES, IQVIA HOLDINGS, VEEVA SYSTEMS, COGNIZANT (ARISGLOBAL), ENNOV, SAMARIND (TATA CONSULTANCY SERVICES), EXTEDO GMBH, RELSYS INTERNATIONAL, MEDIDATA SOLUTIONS (DASSAULT SYSTÈMES), MAX NEELSEN / SAFETYCOMPLETE, SYMSOFT AB, COMPREHEND SYSTEMS, PHARMALEX GMBH, OMNIXUS (CLINTEC), UL SOLUTIONS (PHARMACOVIGILANCE DIVISION), AB SCIENCE SA (INTERNAL SAFETY), SCINAI IMMUNOTHERAPEUTICS, Others

Which segments covered the Drug Safety Database Market?

By Deployment Mode, (Cloud-Based / SaaS, On-Premise, Hybrid), By Application, (Adverse Event / Case Management, Signal Detection & Risk Management, Aggregate Reporting (PSUR/PBRER/DSUR), Literature Monitoring & Case Processing), By Software Type, (Standalone Drug Safety Software, Integrated Safety-EDC Suite, Pharmacovigilance Services Platform), By End-User, (Pharmaceutical & Biotech Companies, Contract Research Organizations (CROs), Medical Device & Diagnostics Manufacturers, Regulatory & Government Bodies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date