- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Edge AI ICs Market Size, Growth & Forecast 2034

Global Edge AI ICs Market Size, Share, and In-Depth Analysis By Chipset (CPU, GPU, ASIC, Others), By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices), By Application (Automotive, Industrial Automation, Consumer Electronics, Smart Cities, Healthcare, Retail), Industry Region & Key Players, Market Dynamics, Competitive Strategies, Technology Trends, Investment Landscape & Forecast 2025–2034

Report Overview

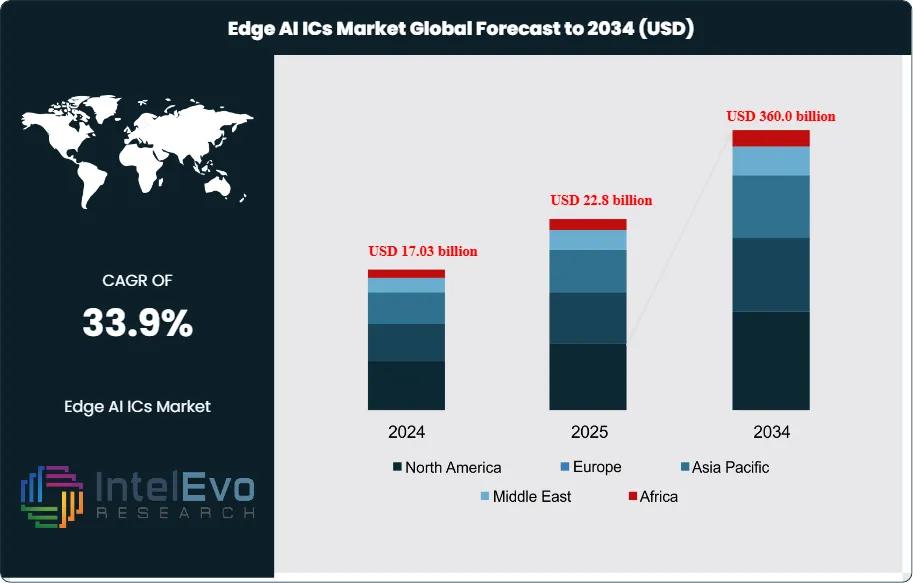

The Edge AI ICs Market is estimated to reach approximately USD 22.8 billion in 2025 and is projected to surge to around USD 360.0 billion by 2034. Based on an estimated USD 26.5 billion market size in 2026, the market is expected to register a robust compound annual growth rate (CAGR) of about 33.9% during the forecast period from 2026 to 2034. This strong expansion reflects the accelerating shift from cloud-centric architectures to distributed intelligence, as enterprises deploy AI processing closer to data sources to minimize latency, enhance data security, and reduce bandwidth and cloud dependency costs. Rising adoption of edge-enabled devices across automotive, industrial automation, consumer electronics, and smart infrastructure further reinforces market momentum and positions Edge AI ICs as a foundational technology for next-generation intelligent systems.

Get More Information about this report -

Request Free Sample ReportEdge AI integrated circuits are specialized processors that execute AI models directly on endpoints such as smartphones, cameras, vehicles, and industrial equipment. Demand accelerates as connected devices multiply and as sectors such as automotive, healthcare, manufacturing, retail, and consumer electronics embed local analytics into products and operations. Real-time perception, classification, and decision-making at the edge support use cases ranging from advanced driver assistance and autonomous navigation to clinical imaging, factory automation, and smart-home ecosystems.

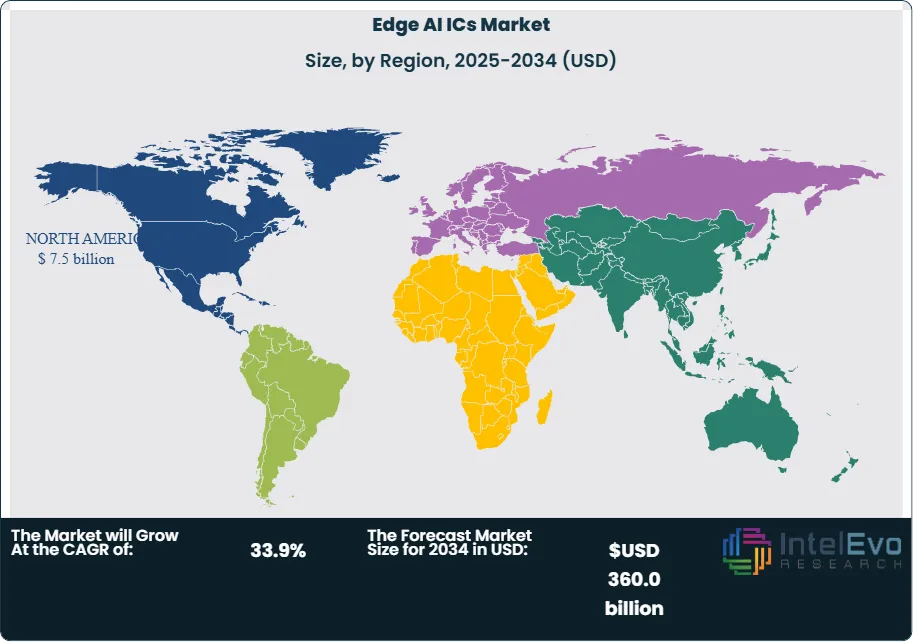

North America currently leads the market, accounting for about 37.4% of global revenue and roughly USD 7.5 billion in 2024, underpinned by strong adoption in the United States, which alone generates around USD 6.8 billion and is projected to grow at a CAGR of 33.2%. Asia-Pacific is emerging as the fastest-growing production and consumption hub, driven by electronics manufacturing in China, South Korea, Taiwan, and Southeast Asia, with regional revenues estimated at about USD 5.5 billion. Europe, with spending of approximately USD 3.2 billion, leverages strict data-protection rules and industrial digitalization programs to foster demand for secure, on-premise AI inference.

Technology advances in neural network architectures, low-power design, and embedded memory are reshaping the supply side. Leading semiconductor vendors, cloud providers, and IP licensors invest in custom accelerators and heterogeneous computing platforms, while foundry capacity and advanced packaging remain critical bottlenecks. Regulatory frameworks on AI accountability, safety, and data governance, together with standards in automotive functional safety and medical devices, shape design roadmaps and certification requirements.

Key risks include silicon supply-chain volatility, high capital intensity, rapid obsolescence of chip designs, and fragmentation across hardware, software, and model toolchains. Despite these challenges, investment continues to flow into specialized edge accelerators for autonomous systems, industrial Internet of Things, and secure embedded vision, positioning Edge AI ICs as a foundational enabler of the next decade of automation and digital transformation.

, By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices), By Application (Automotive, Industrial Automation, Consumer Electronics, Smart Cities, Healthcare, Retail), Industry Region & Key Players, Market Dynamics, Competitive Strategies, Technology Trends, Investment Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The Global Edge AI ICs Market stands at USD 22.8 billion in 2025 and is projected to reach USD 360.0 billion by 2034, implying a 33.9% CAGR, 2025-2034.

- Segment Dominance: The CPU segment leads the architecture mix with 64.0% share of global revenue, 2024, representing estimated: 11.1 billion USD, 2024 concentrated in general-purpose edge processing.

- Segment Dominance: Inference-centric use cases dominate workloads, with the Inference segment capturing 71.4% of functional spend, 2024, equating to estimate: 12.4 billion USD, 2024 in model execution at the edge.

- Driver: Consumer devices act as the primary demand catalyst, holding 84.7% of application revenue, 2024 and generating estimated: 14.7 billion USD, 2024 in edge AI IC spend across smartphones, wearables, and home electronics.

- Restraint: High design complexity, tooling, and verification add cost pressure, with leading vendors likely committing estimated: 2.0 billion USD, 2024 in combined R&D and compliance outlays that can delay commercialization timelines.

- Opportunity: Expanding deployments in automotive, industrial, and healthcare settings can lift non-consumer edge AI IC revenue from estimated: 2.6 billion USD, 2024 to estimated: 40.0 billion USD, 2034 as vendors address safety, reliability, and domain-specific accelerators.

- Trend: Vendors increasingly optimize for power-efficient inference-on-device, as reflected in the 34.7% CAGR, 2024-2034 and the 71.4% workload share, 2024 for Inference, which signal a sustained pivot away from cloud-only AI execution.

- Regional Analysis: North America leads with 37.4% global share and 7.5 billion USD, 2024 in revenue, while the U.S. alone posts 6.8 billion USD, 2024 and a 33.2% CAGR, 2024-2034, positioning the region as the core demand and innovation hub for Edge AI ICs.

Type

In 2024, CPUs accounted for about 64.0% of global Edge AI IC revenue, and they will remain the primary chipset class in 2025 as you continue to ship products that rely on mature software stacks and broad developer familiarity. General-purpose CPUs still handle a large share of low to mid-intensity inference workloads at the edge, especially in smartphones, gateways, and embedded controllers. At the same time, GPU and ASIC-based edge accelerators are gaining share in use cases that require higher throughput, such as computer vision in retail analytics, industrial inspection, and driver assistance.

From 2025 onward, you can expect a gradual shift toward heterogeneous designs that combine CPU, GPU, ASIC, and NPU cores on a single package. This shift reflects the need to balance power, thermal limits, and model complexity at the endpoint. ASIC and domain-specific accelerators will grow faster than the overall market, often at CAGRs above 35% through 2030, as OEMs seek better performance per watt for real-time vision, speech, and sensor fusion. The long installed base of CPU-centric systems will, however, keep CPUs at the center of system control and orchestration across most edge devices.

Application

Inference remains the core application for Edge AI ICs. In 2024, inference workloads represented about 71.4% of silicon demand, and this figure will stay above 70% through the medium term as most edge nodes run pre-trained models rather than train new ones. You see this in cameras that detect anomalies, wearables that classify activity, and industrial controllers that predict failure; all of them need fast, localized decisions more than they need frequent retraining.

Training at the edge is still a smaller share today, but it is beginning to expand as device makers explore on-device learning, personalization, and federated learning schemes. From 2025 to 2030, many forecasts point to training-related edge workloads growing at more than 30% annually, especially in applications that benefit from local adaptation such as personalized health, smart appliances, and industrial robotics. For your planning, this means prioritizing inference-first roadmaps while preparing for selective support of lightweight training and model updates at the edge.

End-Use

Consumer devices held around 84.7% of Edge AI IC shipments in 2024, reflecting the scale of smartphones, wearables, home assistants, and consumer cameras. In 2025, you continue to see strong pull from handset and wearable OEMs that embed on-device vision, audio, and language models to improve responsiveness and manage power. Growth in home automation, security systems, and gaming hardware adds further momentum, as households adopt more connected devices that run local AI to reduce latency and protect privacy.

Enterprise devices, however, represent the fastest-growing opportunity from 2025 onward. Industrial gateways, edge servers in factories, in-vehicle compute platforms, medical devices, and retail endpoints are deploying more capable Edge AI ICs to support predictive maintenance, quality inspection, workflow automation, and store analytics. While enterprise still represents a minority of total units, its revenue share is rising at a CAGR often in the mid-30% range, supported by higher average selling prices and more complex system designs. If you focus on B2B solutions, this segment offers stronger pricing power and deeper multi-year deployment cycles than the consumer market.

Region

North America accounted for about 37.4% of global Edge AI IC revenue in 2024, or roughly 7.5 billion USD, with the United States alone contributing around 6.8 billion USD. In 2025, this region continues to lead due to strong cloud and semiconductor ecosystems, active AI adoption in automotive, healthcare, and retail, and sustained investment from large technology companies and hyperscalers. For you, North America remains a priority market for early deployment of advanced edge architectures and software platforms.

Europe and Asia Pacific provide the next major pillars of demand, with distinct profiles that matter for your strategy. Europe moves steadily, driven by industrial automation, automotive safety systems, and strict data governance that favors local processing. Asia Pacific shows the fastest volume growth, underpinned by electronics manufacturing in China, South Korea, Taiwan, and rising demand from India’s digital and industrial programs. Latin America and the Middle East & Africa still represent smaller shares today, but they are building out telecom, smart city, and logistics infrastructure that relies on edge analytics. From 2025 onward, these emerging regions will post high CAGRs from a low base, giving you room to build long-term positions with localized partnerships and solutions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Chipset

- CPU

- GPU

- ASIC

- Others

By Function

- Training

- Inference

By Device

- Consumer Devices

- Enterprise Devices

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 22.8 billion |

| Forecast Revenue (2034) | USD 360.0 billion |

| CAGR (2025-2034) | 33.9% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Chipset (CPU, GPU, ASIC, Others), By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Huawei Technologies Co., Ltd., Qualcomm Technologies, Inc., Mythic, NVIDIA Corporation, Samsung, Alphabet Inc., Apple Inc., Other Major Players, Arm Limited, Advanced Micro Devices, Inc., Intel Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices), By Application (Automotive, Industrial Automation, Consumer Electronics, Smart Cities, Healthcare, Retail), Industry Region & Key Players, Market Dynamics, Competitive Strategies, Technology Trends, Investment Landscape & Forecast 2025–2034")

, By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices), By Application (Automotive, Industrial Automation, Consumer Electronics, Smart Cities, Healthcare, Retail), Industry Region & Key Players, Market Dynamics, Competitive Strategies, Technology Trends, Investment Landscape & Forecast 2025–2034")

, By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices), By Application (Automotive, Industrial Automation, Consumer Electronics, Smart Cities, Healthcare, Retail), Industry Region & Key Players, Market Dynamics, Competitive Strategies, Technology Trends, Investment Landscape & Forecast 2025–2034")

Frequently Asked Questions

How big is the Edge AI ICs Market?

Global edge AI ICs market to reach USD 360.0B by 2034, growing at 33.9% CAGR driven by distributed intelligence, low-latency AI, and edge computing adoption.

Who are the major players in the Edge AI ICs Market?

Huawei Technologies Co., Ltd., Qualcomm Technologies, Inc., Mythic, NVIDIA Corporation, Samsung, Alphabet Inc., Apple Inc., Other Major Players, Arm Limited, Advanced Micro Devices, Inc., Intel Corporation

Which segments covered the Edge AI ICs Market?

By Chipset (CPU, GPU, ASIC, Others), By Function (Training, Inference), By Device (Consumer Devices, Enterprise Devices)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date