- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Edge AI Processor Market Forecast 2034 | CAGR 15.4%

Global Edge AI Processor Market Size, Share, Growth & Industry Analysis By Processor Type (NPU & ASIC Accelerators, GPU, CPU, FPGA, MCU & Others), By Application (Computer Vision, Generative AI & Human-Machine Interface, Predictive Maintenance, Autonomous Systems & Robotics, Speech & Audio Analytics), By End-Use Industry (Consumer Electronics, Automotive, Industrial, Healthcare, Retail & Smart Cities) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

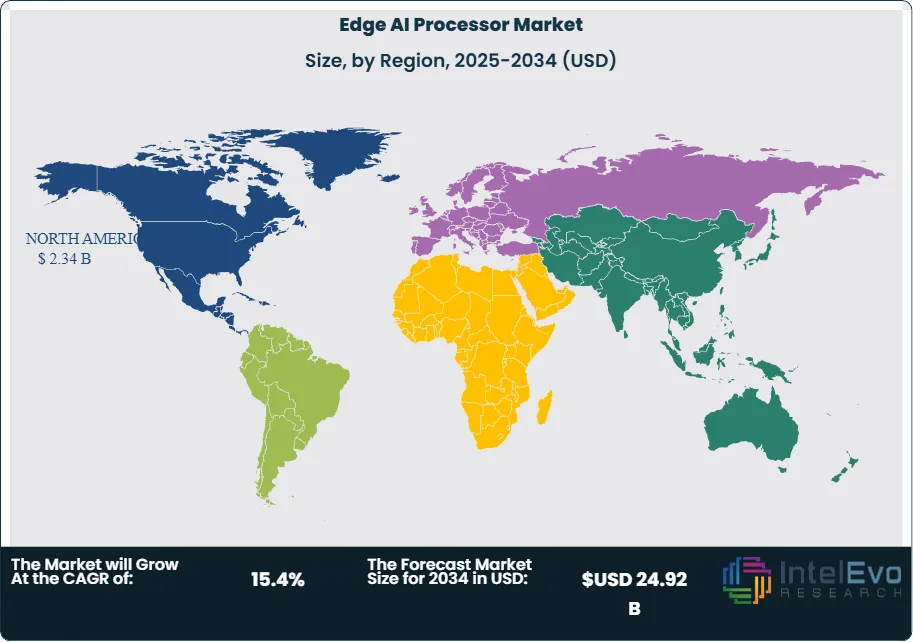

| USD 6.84 Billion | USD 24.92 Billion | 15.4% | North America, 34.2% |

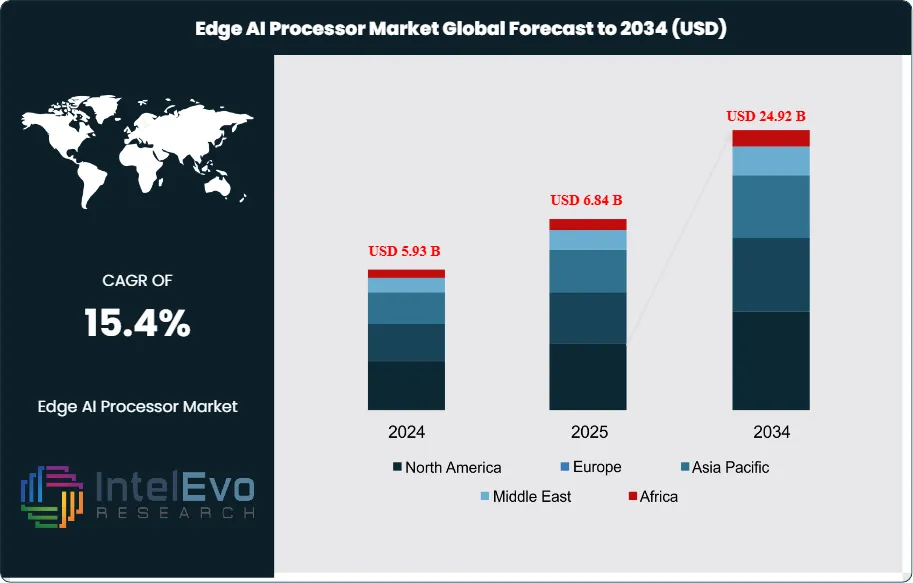

The Edge AI Processor Market was valued at approximately USD 5.93 Billion in 2024 and reached USD 6.84 Billion in 2025. The market is projected to grow to USD 24.92 Billion by 2034, expanding at a CAGR of 15.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 18.08 Billion over the analysis period. The Edge AI Processor Market moved from an early embedded-compute category into a strategic semiconductor class during 2025 as OEMs pushed inference closer to sensors, cameras, HMIs, gateways, robots, and vehicle domain controllers. Demand shifted from pure vision inference to mixed workloads that combine computer vision, speech, time-series analytics, and compact generative models on the same device.

Get More Information about this report -

Request Free Sample ReportThe Edge AI Processor Market gained momentum because power, latency, privacy, and bandwidth constraints increasingly favor local inference over cloud-only execution. Qualcomm expanded its Dragonwing portfolio for industrial and embedded use cases in 2025 and 2026. Intel rolled out AI Edge Systems, Edge AI Suites, and Open Edge Platform initiatives in March 2025 to speed deployment across retail, manufacturing, smart cities, and media workloads. NVIDIA moved Jetson Thor into general availability in August 2025 with claims of 7.5x more AI compute and 3.5x greater energy efficiency than Jetson Orin, aimed directly at robotics and physical AI deployments.

Supply conditions also improved the category’s economics. Global semiconductor sales reached USD 791.7 Billion in 2025, up 25.6% year over year, which gave processor vendors greater room to fund edge-specific product lines, packaging, and software stacks. At the same time, policy support remained strong. The European Chips Act continues to target stronger design, manufacturing, and packaging capacity in Europe and aims to lift the region’s semiconductor position by 2030. In the United States, industry bodies continued to frame AI hardware as a strategic priority, while NIST’s 2025 standards work reinforced the role of the AI Risk Management Framework and ISO-based governance for commercial AI deployments.

Current market assessment shows three forces shaping the 2025 base year. First, smart cameras, industrial PCs, robotics controllers, and automotive cockpits moved from proof-of-concept to production. Second, processor buying criteria shifted from raw TOPS alone to TOPS-per-watt, memory bandwidth, software portability, and model orchestration. Third, edge generative AI widened the addressable market. Hailo launched the Hailo-10H in July 2025 with native support for generative workloads at typical 2.5W power draw, while Ambarella introduced the N1-655 for on-premise multi-channel VLM and neural-network processing under 20W.

Regional investment remained concentrated in North America, East Asia, and selected European industrial clusters. IndiaAI’s public push to expand AI computing access and South Korea’s stepped-up AI chip funding added new demand nodes in 2025–2026. China also continued to build mature-node capacity used in automotive, smartphones, and electronics, reinforcing Asia’s manufacturing weight in edge-oriented semiconductors.

, By Application (Computer Vision, Generative AI & Human-Machine Interface, Predictive Maintenance, Autonomous Systems & Robotics, Speech & Audio Analytics), By End-Use Industry (Consumer Electronics, Automotive, Industrial, Healthcare, Retail & Smart Cities) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Edge AI Processor Market stood at USD 6.84 Billion in 2025 and is projected to reach USD 24.92 Billion by 2034. That implies a verified CAGR of 15.4% across 2026–2034.

- Segment Dominance: By processor type, NPUs and ASIC accelerators led the Edge AI Processor Market with 44.0% share in 2025, equal to about USD 3.01 Billion. Their lead came from superior TOPS-per-watt and tighter fit for vision, sensor fusion, and compact LLM inference.

- Segment Dominance: By end use, consumer electronics held the largest 2025 share at 29.0%, or USD 1.98 Billion. Smartphones, PCs, smart displays, home gateways, and wearables drove this position as on-device AI became a standard feature set.

- Driver: The main growth driver is the move toward local inference for low-latency and privacy-sensitive workloads. Hailo reported sub-1 second first-token latency and more than 10 tokens per second on 2B models at typical 2.5W, showing why on-device inference is now commercially viable.

- Restraint: The main restraint is cost and supply-chain complexity at advanced packaging, memory, and software-porting layers. Even with stronger semiconductor sales in 2025, export controls, packaging bottlenecks, and ecosystem fragmentation held back broader adoption in price-sensitive devices.

- Opportunity: The largest opportunity sits in industrial and automotive edge systems, where the addressable revenue pool is expected to add more than USD 7.0 Billion between 2025 and 2034. Qualcomm, NXP, AMD, and NVIDIA all expanded product or software offerings for these workloads in 2025–2026.

- Trend: The dominant trend is edge generative AI. Qualcomm launched an on-prem AI appliance and inference suite in January 2025, Ambarella launched a sub-20W GenAI SoC in January 2025, and NXP added agentic AI orchestration at the edge in January 2026.

- Regional Analysis: North America led the Edge AI Processor Market in 2025 with 34.2% share and USD 2.34 Billion in revenue. The region benefits from semiconductor design depth, robotics demand, AI software tooling, and large OEM spending.

Competitive Landscape Overview

The Edge AI Processor Market is moderately consolidated. The top four players accounted for an estimated 48.5% of 2025 revenue, with competition centered on power efficiency, software stack maturity, and design wins in robotics, industrial IoT, automotive, and smart vision systems. Competitive intensity increased through 2025 as vendors moved beyond single-chip positioning toward full toolchains, reference platforms, and vertical partnerships. Qualcomm’s Edge Impulse acquisition, Intel’s open edge software push, and NVIDIA’s Jetson Thor rollout show that software control now matters almost as much as silicon performance.

Competitive Landscape Matrix

| Company Name | Headquarters (Country) | Market Position | Key Product/Solution in this market | Geographic Strength | Recent Strategic Move |

| NVIDIA Corporation | United States | Leader | Jetson AGX Thor | North America | Jetson Thor reached general availability in Aug 2025 with 7.5x more AI compute than Jetson Orin. |

| Qualcomm Technologies | United States | Leader | Dragonwing IQ Series | North America, Asia Pacific | Qualcomm launched the Dragonwing brand in Feb 2025 and agreed to acquire Edge Impulse in Mar 2025. |

| Intel Corporation | United States | Leader | Intel AI Edge Systems and Core Ultra for edge | North America, Europe | Intel launched AI Edge Systems, Edge AI Suites, and Open Edge Platform initiatives in Mar 2025. |

| NXP Semiconductors | Netherlands | Leader | i.MX 9 and eIQ Agentic AI Framework | Europe, automotive global | NXP introduced the eIQ Agentic AI Framework in Jan 2026 for secure autonomous edge workflows. |

| Advanced Micro Devices | United States | Challenger | Ryzen AI Embedded P100/X100 | North America | AMD launched Ryzen AI Embedded processors in Jan 2026 with up to 50 AI TOPS. |

| MediaTek | Taiwan | Challenger | Genio 720 and 520 | Asia Pacific | MediaTek introduced Genio 720 and 520 edge-AI IoT platforms for generative AI in Mar 2025. |

| Ambarella | United States | Niche Player | N1-655 Edge GenAI SoC | North America, smart vision global | Ambarella launched the N1-655 in Jan 2025 for multimodal VLM and CNN processing under 20W. |

| Hailo | Israel | Niche Player | Hailo-10H | Europe, enterprise edge | Hailo commercialized the Hailo-10H in Jul 2025 and HP selected it in May 2025 for an AI accelerator card. |

| Arm | United Kingdom | Niche Player | Armv9 Edge AI Platform with Cortex-A320 | Europe, Asia Pacific | Arm launched its Armv9 edge AI platform in Feb 2025 with 10x ML uplift over Cortex-A35. |

| Renesas Electronics | Japan | Niche Player | RZ/V and edge MCU/MPU portfolio | Asia Pacific | Renesas expanded its MCU/MPU portfolio for edge AI needs in Aug 2025. |

Segmentation Analysis

The Edge AI Processor Market generated USD 6.84 Billion in 2025, and segmentation shows where value capture is tightening around performance-per-watt, software portability, and vertical specialization.

By Processor Type.

NPUs and ASIC accelerators held the largest 2025 share at 44.0%, or USD 3.01 Billion. This segment won the largest volume because OEMs increasingly prefer fixed-function or semi-programmable architectures for camera analytics, industrial vision, smart access control, and compact multimodal assistants. Their economic case improved as edge models became lighter and more deployment-ready. Hailo’s 2.5W generative inference positioning and Ambarella’s under-20W multimodal video pipeline both illustrate why dedicated acceleration now commands the premium tier in edge deployments. GPUs accounted for 21.0%, or USD 1.44 Billion, and stayed strong in robotics, vehicle cockpit compute, and complex multimodal workloads where flexibility matters more than lowest power. CPUs represented 19.0%, or USD 1.30 Billion, mainly in industrial PCs, gateways, and mixed control-and-inference systems. FPGAs held 10.0%, or USD 0.68 Billion, where determinism, safety, and reconfigurability remain essential. MCUs and other low-power controllers represented 6.0%, or USD 0.41 Billion, but they remain relevant for always-on sensing and basic inference at the far edge.

By Application.

Computer vision remained the largest application in 2025 with 38.0% share and USD 2.60 Billion in revenue. Security cameras, machine vision, occupancy analytics, retail traffic mapping, and in-cabin monitoring kept vision as the anchor workload for processor buyers. Generative AI and human-machine interface workloads reached 21.0%, or USD 1.44 Billion, as vendors moved compact LLMs and VLMs onto devices for local assistance, multimodal search, and natural-language control. Predictive maintenance and industrial analytics captured 17.0%, or USD 1.16 Billion, supported by vibration analysis, anomaly detection, and edge time-series inference in factories and utilities. Autonomous systems and robotics represented 15.0%, or USD 1.03 Billion, but this segment showed the fastest spending acceleration because robotics now needs real-time perception, planning, and local reasoning. Speech and audio analytics contributed 9.0%, or USD 0.62 Billion, with traction in smart speakers, vehicle voice assistants, and industrial hands-free control. The application mix shows a clear shift. Vision still anchors revenue, but multimodal inference is now the highest-value expansion vector.

By End-Use Industry.

Consumer electronics led with 29.0% of 2025 revenue, or USD 1.98 Billion, because on-device AI moved into mainstream phones, PCs, home gateways, wearables, and smart displays. Automotive ranked second at 25.0%, or USD 1.71 Billion, driven by digital cockpits, driver monitoring, occupancy sensing, and software-defined vehicle compute. NXP, AMD, and MediaTek all pushed automotive-relevant edge AI platforms during 2025–2026. Industrial accounted for 22.0%, or USD 1.50 Billion, supported by robotics, PLC-connected machine vision, warehouse automation, and local control loops that cannot wait for cloud round trips. Retail, smart city, and security represented 14.0%, or USD 0.96 Billion, where vision, loss prevention, and premise analytics remain high-volume processor buyers. Healthcare contributed 10.0%, or USD 0.68 Billion, with growth in patient monitoring, imaging support, and edge inference in regulated clinical settings. From 2025 to 2034, industrial and automotive will expand faster than consumer electronics because they carry higher average selling prices, longer software lifecycles, and stronger demand for deterministic performance.

Regional Analysis

North America

The Edge AI Processor Market in North America held 34.2% share in 2025, equal to USD 2.34 Billion, making it the largest regional market. The United States represented the clear majority of regional demand because it combines semiconductor design leadership, hyperscaler-driven AI software ecosystems, robotics investment, and large enterprise IT budgets. Intel launched AI Edge Systems and Open Edge Platform in 2025 from this base, while NVIDIA advanced Jetson Thor adoption across manufacturing, logistics, healthcare, and retail. Canada remained smaller in revenue but strong in robotics research and AI software talent. Mexico gained importance as electronics and automotive assembly increasingly demanded more local intelligence in cameras, cockpit systems, and industrial gateways. North America also benefits from CHIPS-era investment momentum and the fact that the U.S. semiconductor industry still holds about half of global market share.

Europe

The Edge AI Processor Market in Europe held 22.1% share in 2025, or USD 1.51 Billion. Germany led the region due to factory automation, machine vision, automotive electronics, and industrial PC demand. France followed with strength in aerospace, defense electronics, and smart infrastructure. The UK remained important in processor IP, embedded AI software, and startup activity, supported by Arm’s edge AI platform launch in 2025. The Netherlands mattered because of NXP’s scale in automotive and secure connected edge processors. Europe’s policy setting is unusually relevant in this market. The European Chips Act entered into force in 2023 and continues to push local semiconductor resilience, while the EU AI Act implementation phase is shaping how edge AI systems are documented, governed, and brought into regulated sectors. Those rules raise compliance costs in the short term, but they also favor vendors with secure software stacks, lifecycle support, and auditable inference pipelines. Europe will remain a strong market for industrial, automotive, and safety-aware edge AI processors rather than low-cost volume consumer chips.

Asia Pacific

The Edge AI Processor Market in Asia Pacific accounted for 31.0% of 2025 revenue, or USD 2.12 Billion. China, Japan, India, and South Korea defined the regional picture. China led regional unit demand through smart devices, electronics manufacturing, surveillance systems, and automotive electronics, while continued buildout in mature-node fabrication supports processors used in cars, phones, and connected devices. Japan remained strong in automotive electronics, industrial automation, and edge-adjacent semiconductor investment. India is still earlier in processor manufacturing but moved faster on AI deployment infrastructure through the IndiaAI Mission, which announced an outlay of INR 10,372 crore to build the domestic AI ecosystem. South Korea strengthened its AI chip push further in 2026 through new support for local AI semiconductor champions. Taiwan also remains a critical design and manufacturing node through MediaTek and the broader foundry chain. Asia Pacific will post the fastest revenue expansion over the forecast period because the region combines device volume, automotive demand, and strong local manufacturing depth.

Latin America

The Edge AI Processor Market in Latin America held 5.4% share in 2025, or USD 0.37 Billion. Brazil led the region through retail analytics, industrial monitoring, agritech sensing, and smart surveillance demand. Mexico also ranked high because of automotive and electronics assembly links to North American supply chains. Chile contributed through mining automation and remote monitoring use cases, while the rest of Latin America remained smaller but active in security, logistics, and edge-connected telecom equipment. Regional adoption still faces pressure from imported hardware costs, currency volatility, and fewer local design ecosystems. Even so, edge AI processors are gaining traction because cloud connectivity is not always stable or economical across remote industrial, utility, and transport environments. This makes local inference more attractive than cloud-only models. Growth in this region will center on practical deployments with fast payback, especially video analytics, fleet monitoring, industrial safety, and energy asset diagnostics.

Middle East & Africa

The Edge AI Processor Market in the Middle East & Africa represented 7.3% of 2025 revenue, or USD 0.50 Billion. The UAE led regional spending through smart city deployments, transport monitoring, and AI-backed public service digitization. Saudi Arabia followed, with demand linked to industrial diversification, digital infrastructure, and large-scale automation projects. South Africa remained the largest sub-Saharan market due to security, retail, and industrial monitoring applications. The rest of MEA is earlier in the adoption curve, but the case for edge AI processors is strong in this region because local inference reduces dependence on external bandwidth, supports privacy-sensitive public deployments, and improves response times in utilities, energy, ports, and logistics hubs. Processor demand here skews toward ruggedized smart vision systems, gateways, and industrial control devices rather than premium robotics platforms. MEA will remain a smaller market in absolute terms, but its adoption curve is steep in public infrastructure, transport corridors, and energy-linked use cases.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Processor Type

- NPU and ASIC Accelerators

- GPU

- CPU

- FPGA

- MCU and Others

By Application

- Computer Vision

- Generative AI and Human-Machine Interface

- Predictive Maintenance and Industrial Analytics

- Autonomous Systems and Robotics

- Speech and Audio Analytics

By End-Use Industry

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Retail, Smart City and Security

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.84 B |

| Forecast Revenue (2034) | USD 24.92 B |

| CAGR (2025-2034) | 15.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Processor Type, (NPU and ASIC Accelerators, GPU, CPU, FPGA, MCU and Others), By Application, (Computer Vision, Generative AI and Human-Machine Interface, Predictive Maintenance and Industrial Analytics, Autonomous Systems and Robotics, Speech and Audio Analytics), By End-Use Industry, (Consumer Electronics, Automotive, Industrial, Healthcare, Retail, Smart City and Security), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NVIDIA CORPORATION, QUALCOMM TECHNOLOGIES, INTEL CORPORATION, NXP SEMICONDUCTORS, ADVANCED MICRO DEVICES, MEDIATEK, AMBARELLA, HAILO, RENESAS ELECTRONICS, ARM, STMICROELECTRONICS, TEXAS INSTRUMENTS, SYNAPTICS, GOOGLE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Computer Vision, Generative AI & Human-Machine Interface, Predictive Maintenance, Autonomous Systems & Robotics, Speech & Audio Analytics), By End-Use Industry (Consumer Electronics, Automotive, Industrial, Healthcare, Retail & Smart Cities) Industry Trends & Forecast 2026–2034")

, By Application (Computer Vision, Generative AI & Human-Machine Interface, Predictive Maintenance, Autonomous Systems & Robotics, Speech & Audio Analytics), By End-Use Industry (Consumer Electronics, Automotive, Industrial, Healthcare, Retail & Smart Cities) Industry Trends & Forecast 2026–2034")

, By Application (Computer Vision, Generative AI & Human-Machine Interface, Predictive Maintenance, Autonomous Systems & Robotics, Speech & Audio Analytics), By End-Use Industry (Consumer Electronics, Automotive, Industrial, Healthcare, Retail & Smart Cities) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Edge AI Processor Market?

Global Edge AI processor market valued at USD 5.93B in 2024, reaching USD 24.92B by 2034, growing at a CAGR of 15.4% from 2026–2034.

Who are the major players in the Edge AI Processor Market?

NVIDIA CORPORATION, QUALCOMM TECHNOLOGIES, INTEL CORPORATION, NXP SEMICONDUCTORS, ADVANCED MICRO DEVICES, MEDIATEK, AMBARELLA, HAILO, RENESAS ELECTRONICS, ARM, STMICROELECTRONICS, TEXAS INSTRUMENTS, SYNAPTICS, GOOGLE, Others

Which segments covered the Edge AI Processor Market?

By Processor Type, (NPU and ASIC Accelerators, GPU, CPU, FPGA, MCU and Others), By Application, (Computer Vision, Generative AI and Human-Machine Interface, Predictive Maintenance and Industrial Analytics, Autonomous Systems and Robotics, Speech and Audio Analytics), By End-Use Industry, (Consumer Electronics, Automotive, Industrial, Healthcare, Retail, Smart City and Security),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date