- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Edge Computing in Autonomous Vehicles Market to Reach $5.3B by 2034 | CAGR 28.4%

Global Edge Computing in Autonomous Vehicles Market Size, Share, Analysis Report By Component (Hardware, Software, Services, ), Application (Vehicle-to-Everything Communication, Real-time Data Processing, Predictive Maintenance, Fleet Management), Technology (Edge Analytics, Edge AI, Fog Computing), Deployment Mode (On-premises, Cloud-based), End-user(Automotive Manufacturers, Technology Providers, Fleet Operators), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview

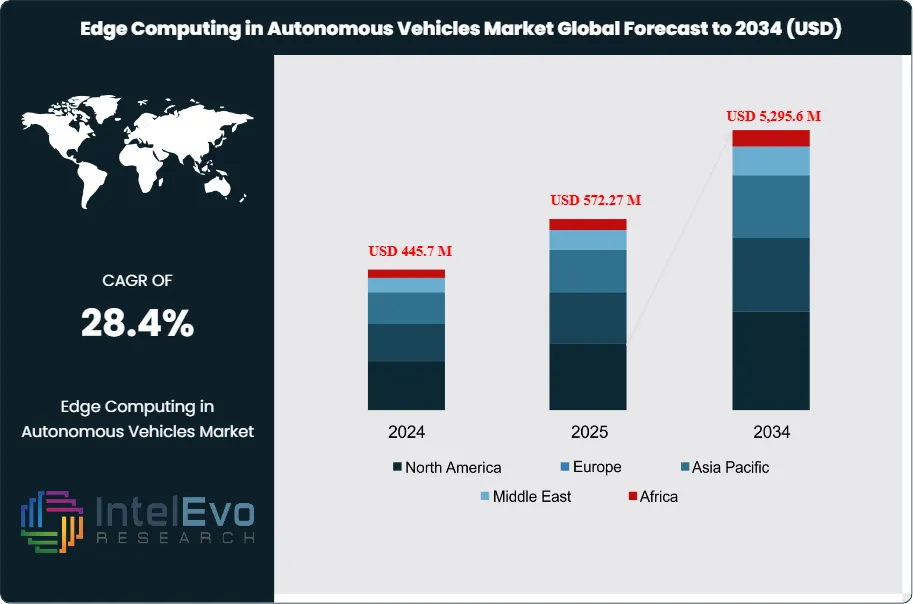

The Global Edge Computing in Autonomous Vehicles Market is projected to reach USD 5,295.6 Million by 2034, up from USD 445.7 Million in 2024, growing at a CAGR of 28.4% during the forecast period from 2024 to 2034. The growth is driven by the increasing adoption of autonomous vehicles, demand for real-time data processing, and low-latency AI analytics at the network edge. Edge computing enables faster decision-making, enhanced vehicle safety, and efficient traffic management, positioning it as a crucial technology for the future of smart mobility worldwide.

Get More Information about this report -

Request Free Sample ReportThe Edge Computing in Autonomous Vehicles Market comprises technologies that facilitate real-time data processing and analysis in autonomous vehicles. By analyzing data from onboard sensors and external sources, these solutions help to improve vehicle safety and operational efficiency, enabling quicker decision-making. By 2024, the market is expected to reach a value of around USD 432.94 million. The present environment is defined by fast technological progress, regulatory backing for self-driving projects, and an increasing incorporation of IoT gadgets, all contributing to market expansion.

There are various essential growth factors impacting the Market for Edge Computing in Autonomous Vehicles. The growing need for self-driving technology comes from urban growth, environmental worries, and a worldwide drive for more intelligent transportation networks. The growth is greatly attributed to the emergence of 5G technology, which enables quicker and more dependable communication between vehicles and edge servers, crucial for making real-time decisions. Moreover, by integrating artificial intelligence and machine learning into edge computing systems, automotive manufacturers can improve their data analysis abilities, giving them a competitive edge. Consequently, it is forecasted that the market will experience a compound annual growth rate (CAGR) of 28% between 2024 and 2034.

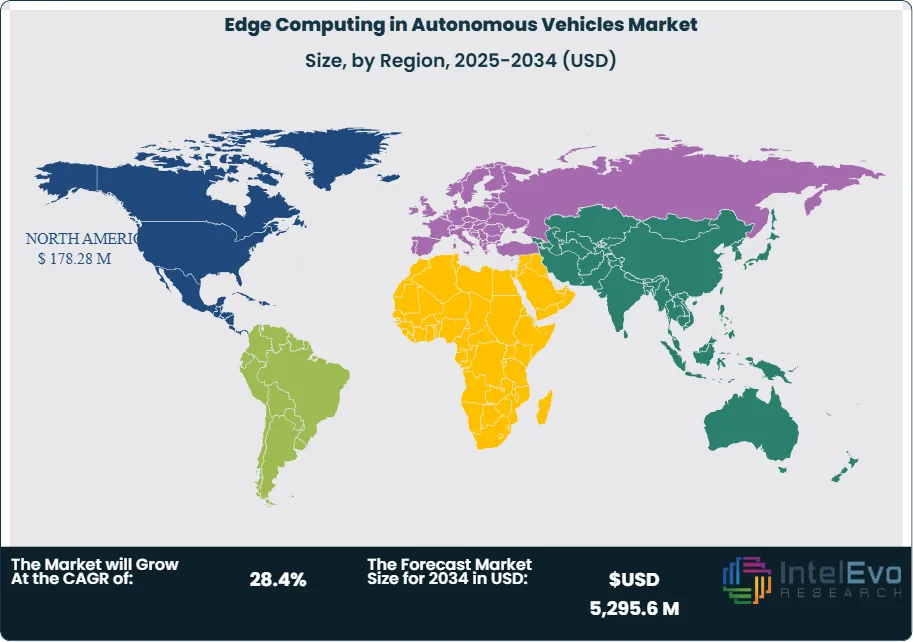

North America is expected to lead the Edge Computing in Autonomous Vehicles Market due to a strong automotive sector, significant investments in autonomous technologies, and the existence of major technology companies. The United States is especially dedicated to the advancement of vehicle-to-everything (V2X) communication systems, crucial for autonomous vehicle functionality. At the same time, the Asia-Pacific region is projected to experience the most rapid expansion, driven by fast urbanization, growing investments in smart city projects, and a thriving automotive industry, particularly in nations such as China and Japan.

The Edge Computing in Autonomous Vehicles Market has been greatly affected by the COVID-19 pandemic. At first, it caused interruptions in supply chains and postponed project schedules because of lockdown restrictions. Nevertheless, the pandemic sped up the integration of digital technologies such as edge computing, as businesses aimed to enhance operational efficiencies and adjust to new obstacles. The rise in remote work and telecommuting has led to a higher need for improved connectivity and data processing abilities, highlighting the significance of edge computing in the automotive sector.

, Application (Vehicle-to-Everything Communication, Real-time Data Processing, Predictive Maintenance, Fleet Management), Technology (Edge Analytics, Edge AI, Fog Computing), Deployment Mode (On-premises, Cloud-based), End-user(Automotive Manufacturers, Technology Providers, Fleet Operators), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways

- Market Growth: The Edge Computing in Autonomous Vehicles Market is expected to reach USD 5,295.6 million by 2034, growing at a robust CAGR of 28.4%, indicating strong market expansion driven by technological advancements and increasing demand for autonomous vehicles.

- Component Analysis: The hardware segment is anticipated to dominate the market due to the growing need for robust processing units and storage devices that facilitate real-time data handling and enhance overall vehicle performance.

- Application Analysis: Vehicle-to-Everything (V2X) communication is poised to be a key application area, enabling seamless interaction between vehicles and infrastructure, which is crucial for improving traffic management and ensuring safety in autonomous driving.

- Driver: The rising demand for smart transportation solutions and the proliferation of autonomous vehicle technologies are driving market growth. These advancements enhance operational efficiency and safety, making edge computing indispensable for real-time data processing.

- Restraint: The high costs associated with implementing edge computing infrastructure may limit market accessibility for smaller players. Additionally, concerns regarding data privacy and security can hinder adoption, especially in sensitive applications like autonomous driving.

- Opportunity: The integration of artificial intelligence and machine learning with edge computing presents significant growth opportunities. Companies can leverage these technologies to improve data analytics and operational efficiencies in autonomous vehicles.

- Trend: Increasing investments in smart city initiatives and advancements in 5G technology are driving trends in edge computing, enhancing connectivity and data processing capabilities for autonomous vehicles.

- Regional Analysis: North America is expected to hold the largest market share, driven by substantial investments in autonomous technologies and the presence of leading automotive and technology firms. The Asia-Pacific region is also emerging rapidly due to urbanization and increased automotive demand.

Component

The Edge Computing in Autonomous Vehicles Market is segmented into three primary components: hardware, software, and services. The hardware segment includes processing units, storage devices, and networking equipment, which are essential for real-time data handling and connectivity. As autonomous vehicles rely heavily on data for navigation and decision-making, high-performance hardware is crucial. The software segment encompasses the platforms and applications that facilitate data analysis, management, and communication between various vehicle systems. Finally, the services segment includes installation, maintenance, and consulting services, which support the integration of edge computing technologies into existing vehicle architectures. This multi-faceted approach ensures that all aspects of edge computing are addressed, driving market growth and innovation.

Application

Edge computing applications in autonomous vehicles include autonomous driving, ADAS (Advanced Driver Assistance Systems), fleet management, traffic monitoring, and infotainment systems. Autonomous driving uses on-board processing for instant decision-making and safe navigation. ADAS systems utilize edge-based AI for avoiding collisions, detecting lanes, and enabling emergency braking. Fleet management and traffic monitoring depend on off-board edge processing for real-time analytics and predictive insights, improving efficiency and reducing congestion. Infotainment systems combine hybrid edge computing to offer personalized, fast experiences for passengers. The rising demand for safety, efficiency, and data-driven vehicle operations is driving the broad use of edge computing applications throughout the autonomous vehicle ecosystem.

Edge Computing Type

The Edge Computing segment in autonomous vehicles is mainly divided into On-Board, Off-Board, and Hybrid Edge Computing. On-Board Edge Computing means processing data locally within the vehicle. This allows for real-time decision-making for important functions like collision avoidance, ADAS, and autonomous navigation. Off-Board Edge Computing uses external edge servers or cloud resources to manage extensive data analytics, monitor traffic, and handle fleet management tasks. The Hybrid Edge Computing model merges both on-board and off-board capabilities. This ensures low-latency processing while also taking advantage of scalable computing power for complex AI and machine learning algorithms. The growing use of connected vehicles and the need for better safety, efficiency, and real-time insights are fueling growth in all types of edge computing in autonomous mobility.

Vehicle Type

The autonomous vehicle market that uses edge computing is divided into passenger vehicles, commercial vehicles, and specialty vehicles. Passenger vehicles use edge computing to improve real-time safety systems, navigation, and infotainment, creating smooth autonomous driving experiences. Commercial vehicles, like trucks and buses, gain from edge-enabled fleet management, predictive maintenance, and route optimization, boosting operational efficiency and cutting downtime. Specialty vehicles, such as delivery robots and industrial machines, depend on edge computing for precise task execution, sensor integration, and awareness of their surroundings. The increasing use of autonomous mobility solutions across all vehicle types, along with the demand for quick decision-making and better AI-driven analytics, is driving market growth worldwide.

End-user

The end-user segment of the Edge Computing in Autonomous Vehicles Market includes automotive manufacturers, technology providers, and fleet operators. Automotive manufacturers are the primary drivers of market growth, as they seek to integrate edge computing technologies into their vehicles to enhance safety and performance. Technology providers develop the necessary hardware and software solutions that enable effective data processing and communication. Fleet operators utilize edge computing to optimize their operations, improve vehicle maintenance, and enhance route planning. By addressing the specific needs of these end users, the market can facilitate advancements in autonomous vehicle technologies, leading to safer and more efficient transportation solutions.

Region Analysis

North America Leads With 40% Market Share in Edge Computing in Autonomous Vehicles Market: North America is the leading region in the Edge Computing in Autonomous Vehicles Market, commanding approximately 40% of the global market share. Several factors contribute to this dominance, including the presence of major automotive manufacturers and technology firms that are actively investing in autonomous vehicle technologies. The region has a well-established infrastructure for testing and deploying advanced automotive solutions, bolstered by significant governmental support for research and development in smart transportation. Additionally, the rapid adoption of connected vehicles and IoT technologies enhances the need for edge computing, which facilitates real-time data processing and communication. This focus on innovation and safety, combined with a consumer base that is increasingly receptive to autonomous driving technologies, positions North America as a robust market leader.

Asia-Pacific is recognized as the fastest-growing region in the Edge Computing in Autonomous Vehicles Market, with a projected growth rate of over 30% during the forecast period. This growth is driven by rapid urbanization and increasing automotive production, particularly in countries like China, Japan, and India. The rising demand for smart city initiatives and advancements in 5G technology are also significant contributors, as they facilitate the deployment of connected vehicle technologies. Furthermore, government initiatives aimed at promoting electric and autonomous vehicles are creating a conducive environment for edge computing solutions. Meanwhile, Europe maintains a strong market presence due to stringent regulations on vehicle safety and emissions, supporting the growth of edge computing applications. Latin America and the Middle East & Africa are gradually catching up, focusing on enhancing transportation systems and infrastructure to accommodate the evolving demands of autonomous vehicles.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Vehicle Type

- Passenger Vehicles

- Commercial Vehicles

- Specialty Vehicles

By Edge Computing Type

- On-Board Edge Computing

- Off-Board Edge Computing

- Hybrid Edge Computing

By Component

- Hardware (Sensors, Processors, GPUs)

- Software (AI & Analytics Platforms, Middleware)

- Services (Deployment, Maintenance, Support)

By End-user

- Automotive Manufacturers

- Technology Providers

- Fleet Operators

By Application

- Autonomous Driving

- ADAS (Advanced Driver Assistance Systems)

- Fleet Management & Telematics

- Traffic & Road Safety Monitoring

- Infotainment Systems

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 572.27 M |

| Forecast Revenue (2034) | USD 5,295.6 M |

| CAGR (2025-2034) | 28.4% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Specialty Vehicles), By Edge Computing Type (On-Board Edge Computing, Off-Board Edge Computing, Hybrid Edge Computing), By Component (Hardware (Sensors, Processors, GPUs), Software (AI & Analytics Platforms, Middleware), Services (Deployment, Maintenance, Support)), By End-user (Automotive Manufacturers, Technology Providers, Fleet Operators), By Application (Autonomous Driving, ADAS (Advanced Driver Assistance Systems), Fleet Management & Telematics, Traffic & Road Safety Monitoring, Infotainment Systems) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NVIDIA, Waymo, Motional, Aurora Innovation, Embark Trucks, Cavnue, Nauto, WeRide, Toyota, Magna International, Intel, Tesla, Bosch, Qualcomm, IBM, Microsoft, Amazon Web Services (AWS), Pivotal, HPE (Hewlett Packard Enterprise), IBM Watson |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, Application (Vehicle-to-Everything Communication, Real-time Data Processing, Predictive Maintenance, Fleet Management), Technology (Edge Analytics, Edge AI, Fog Computing), Deployment Mode (On-premises, Cloud-based), End-user(Automotive Manufacturers, Technology Providers, Fleet Operators), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Application (Vehicle-to-Everything Communication, Real-time Data Processing, Predictive Maintenance, Fleet Management), Technology (Edge Analytics, Edge AI, Fog Computing), Deployment Mode (On-premises, Cloud-based), End-user(Automotive Manufacturers, Technology Providers, Fleet Operators), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Application (Vehicle-to-Everything Communication, Real-time Data Processing, Predictive Maintenance, Fleet Management), Technology (Edge Analytics, Edge AI, Fog Computing), Deployment Mode (On-premises, Cloud-based), End-user(Automotive Manufacturers, Technology Providers, Fleet Operators), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Frequently Asked Questions

How big is the Edge Computing in Autonomous Vehicles Market?

The Global Edge Computing in Autonomous Vehicles Market is projected to grow from USD 445.7M in 2024 to USD 5.3B by 2034 at a CAGR of 28.4%. Rising adoption of autonomous vehicles, real-time data processing, and low-latency AI analytics are driving rapid market expansion worldwide.

Who are the major players in the Edge Computing in Autonomous Vehicles Market?

NVIDIA, Waymo, Motional, Aurora Innovation, Embark Trucks, Cavnue, Nauto, WeRide, Toyota, Magna International, Intel, Tesla, Bosch, Qualcomm, IBM, Microsoft, Amazon Web Services (AWS), Pivotal, HPE (Hewlett Packard Enterprise), IBM Watson

Which segments covered the Edge Computing in Autonomous Vehicles Market?

By Vehicle Type (Passenger Vehicles, Commercial Vehicles, Specialty Vehicles), By Edge Computing Type (On-Board Edge Computing, Off-Board Edge Computing, Hybrid Edge Computing), By Component (Hardware (Sensors, Processors, GPUs), Software (AI & Analytics Platforms, Middleware), Services (Deployment, Maintenance, Support)), By End-user (Automotive Manufacturers, Technology Providers, Fleet Operators), By Application (Autonomous Driving, ADAS (Advanced Driver Assistance Systems), Fleet Management & Telematics, Traffic & Road Safety Monitoring, Infotainment Systems)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Edge Computing in Autonomous Vehicles Market

Published Date : 17 Dec 2024 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date