- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

EdTech Regulatory Compliance Market Size & Forecast 2034 | 14.2% CAGR

Global EdTech Regulatory Compliance Market Size, Share & Strategic Growth Outlook – By Component (Solutions, Services), By Solution Type (LMS Compliance Tools, Data Privacy & Protection Software, Accessibility Management Platforms, Cybersecurity Compliance Systems), By Deployment Mode (Cloud-Based, On-Premises), By End User (K-12, Higher Education, Corporate Institutions), By Region, Industry Trends, Competitive Landscape & Forecast 2025–2034

Report Overview

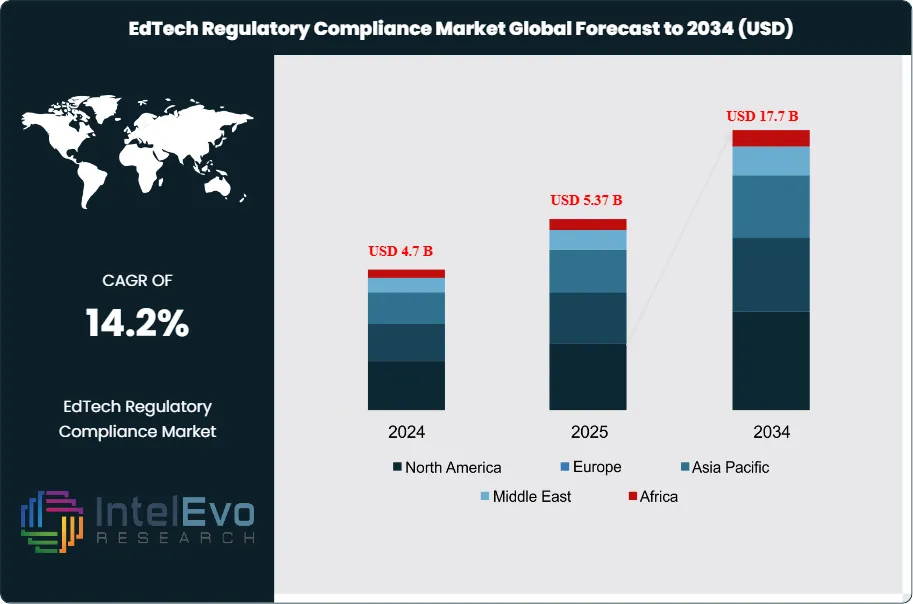

The Global EdTech Regulatory Compliance Market was valued at approximately USD 4.7 billion in 2024 and is projected to reach nearly USD 17.7 billion by 2034, driven by increasing data privacy mandates, cross-border education regulations, and the growing adoption of digital learning platforms. Based on the established growth trajectory, the market size for 2025 is estimated at approximately USD 5.37 billion. From 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 14.2% during 2026–2034, ultimately reaching around USD 17.7 billion by 2034.

Get More Information about this report -

Request Free Sample ReportRapid digitalization of learning environments, expanding data footprints, and tighter oversight of online education models drive sustained demand for compliance solutions and services across K–12, higher education, and lifelong learning segments.

EdTech regulatory compliance spans data protection, child privacy, content governance, accessibility, and consumer safeguards. Education providers and technology vendors increasingly depend on specialized consulting, audits, and software platforms to interpret complex rules, monitor adherence, and document controls in real time. As global EdTech spending is projected to rise from about USD 220.5 billion in 2023 to more than USD 810 billion by 2033, compliance budgets scale in parallel as institutions embed risk management into digital learning strategies.

Demand-side momentum strengthens as stakeholders react to misuse of student data and opaque subscription practices. A recent survey indicates that roughly two-thirds of respondents believe EdTech platforms require formal regulation, while over 90% endorse structured codes of conduct for pricing and service terms. These views translate into reputational and regulatory risk for non-compliant providers, pushing boards and investors to prioritize governance, transparency, and independent verification of compliance claims.

On the supply side, vendors integrate artificial intelligence, machine learning, and workflow automation into compliance suites. These tools classify sensitive data, flag jurisdiction-specific risks, and generate auditable reporting, which reduces manual effort and shortens response times to policy changes. However, reliance on AI also introduces model-governance and algorithmic-bias risks, prompting demand for explainable systems and strong oversight frameworks.

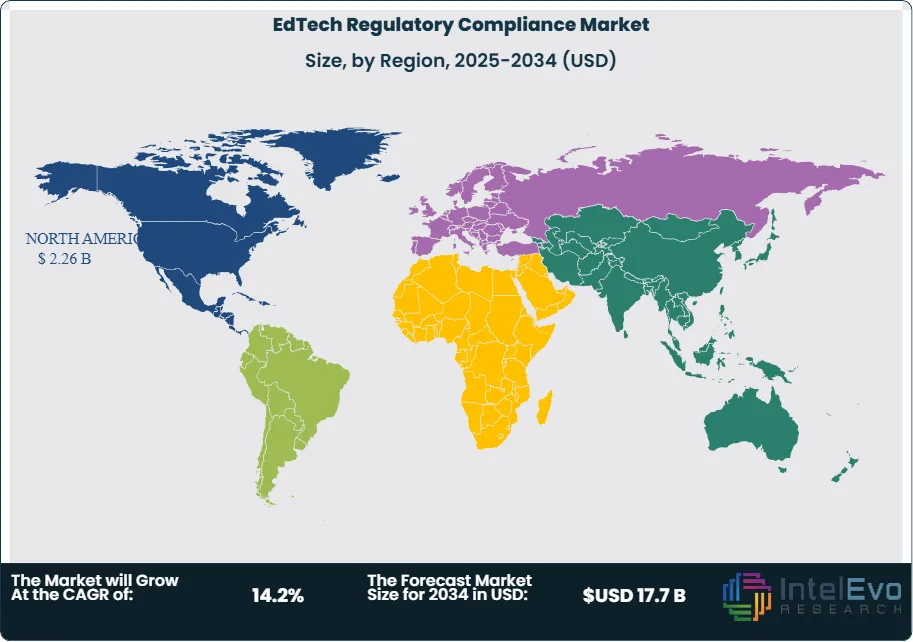

Regulation acts as both a growth catalyst and a constraint. Under the EU’s data protection regime, penalties can reach up to 4% of global revenue, while non-compliance with child privacy rules in the United States can trigger fines exceeding USD 40,000 per violation. Such exposure strengthens the business case for proactive compliance investment. North America currently represents around 42% of global EdTech regulatory compliance revenues, supported by mature digital infrastructure and stringent rules, while emerging opportunities build in Asia, where large student populations in markets such as India, combined with ambitious skilling agendas, accelerate adoption of compliant digital learning ecosystems.

, By Solution Type (LMS Compliance Tools, Data Privacy & Protection Software, Accessibility Management Platforms, Cybersecurity Compliance Systems), By Deployment Mode (Cloud-Based, On-Premises), By End User (K-12, Higher Education, Corporate Institutions), By Region, Industry Trends, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global EdTech regulatory compliance market stands at 4.7 billion USD, 2024 and is projected to reach 17.7 billion USD, 2034, implying a 14.2% CAGR, 2024-2034.

- Segment Dominance: The Solution segment leads the offering mix with 64.7% share, 2024 of total market revenues and anchors an estimated: 3.0 billion USD, 2024 in compliance-focused platforms and tools.

- Segment Dominance: Within functional categories, the Data Privacy and Protection segment accounts for 30.2% share, 2024, reflecting estimated: 1.4 billion USD, 2024 in spend on safeguarding learner data.

- Driver: Strong adoption in K-12 Education, which holds 46.0% share, 2024 of end-user demand, acts as a primary growth driver as school systems scale digital platforms toward 2034, creating an estimated: 9.0 billion USD, 2034 addressable market.

- Restraint: Dependence on legacy on-premises deployments, representing 58.4% share, 2024 of implementations, constrains agility and raises upgrade costs, with an estimated: 1.5 billion USD, 2024 in projects delayed by integration complexity.

- Opportunity: Vendors can capture upside by accelerating migration from on-premises models, 58.4% share, 2024, to more scalable cloud-native compliance solutions, targeting an estimated: 8.0 billion USD, 2034 revenue pool as hybrid deployment gains traction.

- Trend: Institutions increasingly favor automated compliance solutions, led by the Solution segment at 64.7% share, 2024, while AI-enabled monitoring and reporting tools are expected to grow at an estimated: 18.0% CAGR, 2024-2034.

- Regional Analysis: North America commands 42.0% share, 2024 of global EdTech regulatory compliance revenues at 1.9 billion USD, 2024, with the United States alone contributing 1.58 billion USD, 2024 and expanding at a 15.3% CAGR, 2024-2034.

By Component

The Solution segment continues to hold a central position in the EdTech regulatory compliance landscape in 2025. It accounted for more than 64.7 percent of global demand in 2024 and remains the primary category driving institutional investment. You see this strength reflected in rising adoption of LMS compliance tools, data privacy platforms, and audit automation software. Institutions depend on these systems to manage rising content volumes, validate curriculum alignment, and meet cross-border standards. Increased scrutiny around student data handling pushes your team to adopt applications capable of meeting frameworks such as GDPR, FERPA, and regional privacy codes in Asia and Latin America.

Learning environments now operate across multiple devices and platforms, which requires LMS tools that support SCORM and similar interoperability requirements. Administrators are adopting compliance dashboards that help you track policy updates, manage digital content, and maintain records for audits. Providers are expanding their product suites to include automated reporting, risk scoring, and secure data vaults. These tools are becoming standard as regulatory demands grow more complex.

Service providers also gain traction as institutions request strategy guidance, system configuration, and external audits to reduce compliance exposure. The combination of software and advisory services creates a more complete compliance ecosystem, which strengthens the position of the Solution segment as institutions expand their digital footprint.

By Deployment Mode

On-premises deployments held more than 58.4 percent of the market in 2024 and remain widely used in 2025. Institutions prefer this model when you require full control of data storage, access protocols, and internal security. Markets with strict data sovereignty expectations continue to favor on-premises systems because administrators maintain direct oversight of sensitive records. This model also supports high customization, which benefits institutions with legacy infrastructure or unique workflow needs.

Reliability plays an important role. On-premises installations operate independently of internet connectivity, reducing the risk of system downtime during instruction or assessments. Many schools and universities still rely on campus-based networks to maintain operational continuity.

While cloud-based compliance platforms grow at a faster rate through 2030, on-premises deployments maintain relevance where security and control remain top priorities. Most institutions pursue hybrid adoption strategies that allow you to preserve sensitive datasets locally while shifting non-critical workflows to the cloud.

By Compliance Type

Data Privacy and Protection represented more than 30.2 percent of the global market in 2024 and remains the leading compliance priority in 2025. Governments in Europe, North America, and Asia continue to tighten oversight of how institutions collect, store, and share learner information. Your teams now face mandatory reporting obligations, breach notification rules, and consent management requirements. This strengthens demand for encryption tools, access governance software, and automated monitoring applications.

Growth in AI-driven learning tools increases the need for more rigorous controls. AI models require large datasets, which intensifies risk around data exposure. Institutions now assess AI workflows for compliance alignment before permitting adoption. Vendors respond by incorporating privacy-preserving architectures, synthetic data tools, and real-time auditing features.

Content and curriculum requirements, accessibility standards, and cybersecurity regulations also expand. The shift toward digital material in assessments and instruction pushes institutions to ensure content accuracy, accessibility compliance, and secure delivery. This broadens the overall compliance scope and raises total spending on specialized regulatory systems.

By End User

K–12 education accounted for more than 46 percent of market demand in 2024 and remains the most active adopter in 2025. Districts continue to expand device programs, online learning modules, and student information systems. This growth requires strong compliance controls to protect minors’ data, ensure platform safety, and maintain instructional quality. You see rising adoption of privacy tools, monitoring systems, and parent consent management applications in this segment.

Higher education institutions expand compliance investments as they scale hybrid programs and cross-border partnerships. Universities store large volumes of academic records, research data, and learner analytics, which increases regulatory exposure. Business institutions, including training and professional development providers, adopt compliance systems to meet ISO, workforce development, and national data standards.

Across all end users, the shift toward digital credentialing, remote assessments, and AI-driven instruction heightens interest in consistent compliance governance. Institutions seek unified systems that help you monitor risk, maintain audit trails, and support long-term data integrity.

By Region

North America accounted for more than 42 percent of global revenue in 2024 and continues to lead the market in 2025 with strong demand in the United States and Canada. Institutions in this region operate under strict privacy laws, including state-level regulations that extend beyond federal requirements. Vendors headquartered in North America continue to expand their compliance portfolios to meet these expectations. Strong investment from public agencies and private equity firms further supports market growth.

Europe follows closely due to the enforcement strength of GDPR and ongoing updates to digital education directives. Institutions across Germany, France, the Nordics, and the UK invest in tools that support strict accountability and reporting standards. Asia Pacific represents the fastest-growing region as India, Japan, China, and Southeast Asian economies expand digital learning capacity. Large student populations and new data protection laws create strong demand for compliance frameworks tailored to local conditions.

Latin America and the Middle East & Africa expand at a steady rate as connectivity improves and governments introduce national digital education strategies. These regions represent rising opportunities for providers that can deliver compliance systems suited to emerging regulatory models and budget constraints.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Solution

- Learning Management System (LMS) compliance tools

- Data privacy and protection software

- Others

- Services

By Deployment Mode

- Cloud-Based

- On-Premises

By Compliance Type

- Data Privacy and Protection

- Accessibility Standards

- Content and Curriculum Compliance

- Cybersecurity Regulations

- Ethical Compliance

- Others

By End User

- K-12 Education

- Higher Education

- Business Institutions

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.37 B |

| Forecast Revenue (2034) | USD 17.7 B |

| CAGR (2025-2034) | 14.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Solution, Services), By Deployment Mode (Cloud-Based, On-Premises), By Compliance Type (Data Privacy and Protection, Accessibility Standards, Content and Curriculum Compliance, Cybersecurity Regulations, Ethical Compliance, Others), By End User (K-12 Education, Higher Education, Business Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Workday, Inc., Ellucian Company LLC, PowerSchool, Anthology Inc., Securly, Inc., Blackboard Inc., Microsoft Corporation, Instructure, Inc., Sai Global, OneTrust, LLC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Solution Type (LMS Compliance Tools, Data Privacy & Protection Software, Accessibility Management Platforms, Cybersecurity Compliance Systems), By Deployment Mode (Cloud-Based, On-Premises), By End User (K-12, Higher Education, Corporate Institutions), By Region, Industry Trends, Competitive Landscape & Forecast 2025–2034")

, By Solution Type (LMS Compliance Tools, Data Privacy & Protection Software, Accessibility Management Platforms, Cybersecurity Compliance Systems), By Deployment Mode (Cloud-Based, On-Premises), By End User (K-12, Higher Education, Corporate Institutions), By Region, Industry Trends, Competitive Landscape & Forecast 2025–2034")

, By Solution Type (LMS Compliance Tools, Data Privacy & Protection Software, Accessibility Management Platforms, Cybersecurity Compliance Systems), By Deployment Mode (Cloud-Based, On-Premises), By End User (K-12, Higher Education, Corporate Institutions), By Region, Industry Trends, Competitive Landscape & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

EdTech Regulatory Compliance Market

Published Date : 25 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date