- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Electric Aircraft Propulsion Market Size, Share | CAGR 16.1%

Global Electric Aircraft Propulsion Market Size, Share, Analysis By Platform Type (eVTOL Urban Air Mobility, UAVs, Regional Commuter Aircraft, General Aviation, Commercial Airliners), By Propulsion Component (Electric Motors, Batteries, Power Electronics, Turbogenerators, Hydrogen Fuel Cells), By Application (Passenger, Cargo Delivery, Military, Agriculture), By End-User (Airlines, Logistics, Defense, Flight Schools) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 5.85 Billion | USD 22.45 Billion | 16.1% | North America, 41.2% |

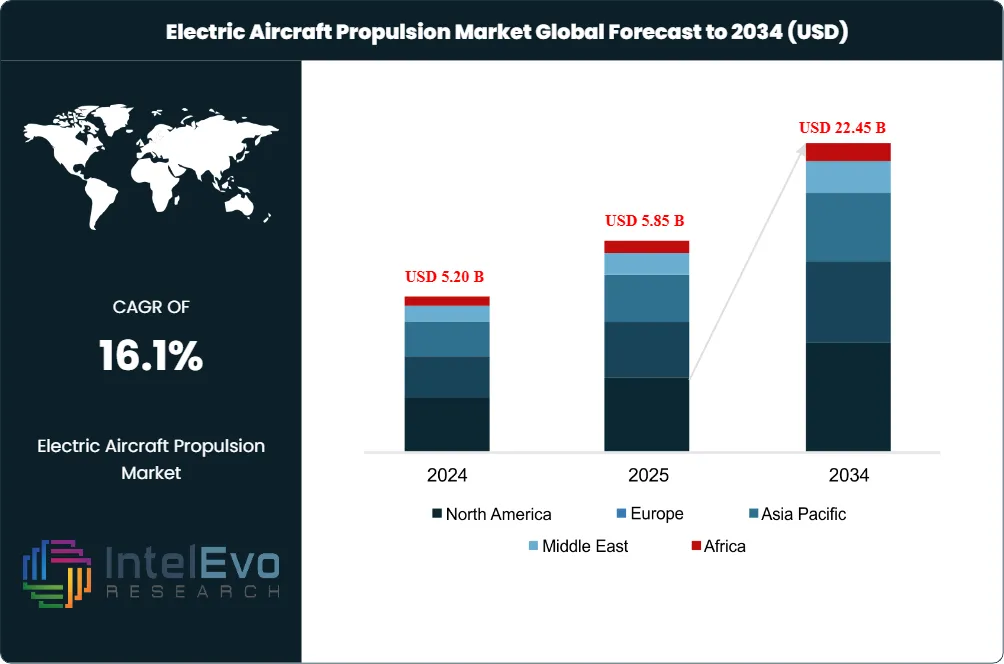

The Electric Aircraft Propulsion Market was valued at USD 5.20 Billion in 2024 and USD 5.85 Billion in 2025. The market is projected to reach USD 22.45 Billion by 2034, expanding at a CAGR of 16.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 16.60 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe electric aircraft propulsion market spans electric motors, generators, power electronics (inverters, converters, distribution), high-voltage architectures (540 to 800 V), wide bandgap silicon carbide and gallium nitride power stages, aviation-grade lithium-ion and solid-state battery systems, and integrated propulsion units across electric vertical takeoff and landing (eVTOL) aircraft, electric conventional takeoff and landing (eCTOL) aircraft, hybrid-electric regional aircraft, and More Electric Aircraft (MEA) commercial platforms. Aviation-grade battery packs reached 250 to 300 Wh/kg at system level in flight-test configurations, with motor specific power in prototypes reaching 10 to 15 kW/kg, enabling megawatt-class propulsion for regional and eVTOL programs. Next-generation SiC and GaN power stages deliver greater than 98% inverter efficiency.

Regulatory anchors are concentrated under the U.S. Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA). Joby Aviation and Archer Aviation lead Western FAA Type Certification progress, with Joby disclosing an 18-percentage-point quarterly advance in FAA Stage 4 progress on February 25, 2026 and Archer receiving FAA acceptance of the Midnight certification basis in November 2025. The White House eVTOL Integration Pilot Program (eIPP), directed by Presidential Executive Order, enables mature eVTOL aircraft to begin operations in select markets ahead of full FAA certification; on April 27, 2026 Joby executed its first NYC point-to-point demonstration sorties bridging JFK International Airport with Downtown Skyport plus the East 34th and West 30th Street heliports. NASA's Electrified Powertrain Flight Demonstration (EPFD) project advances hybrid-electric flight testing on a De Havilland Dash 7 with magniX magni650 propulsion units in 2026, although FY2026 federal budget cuts reduced EPFD funding.

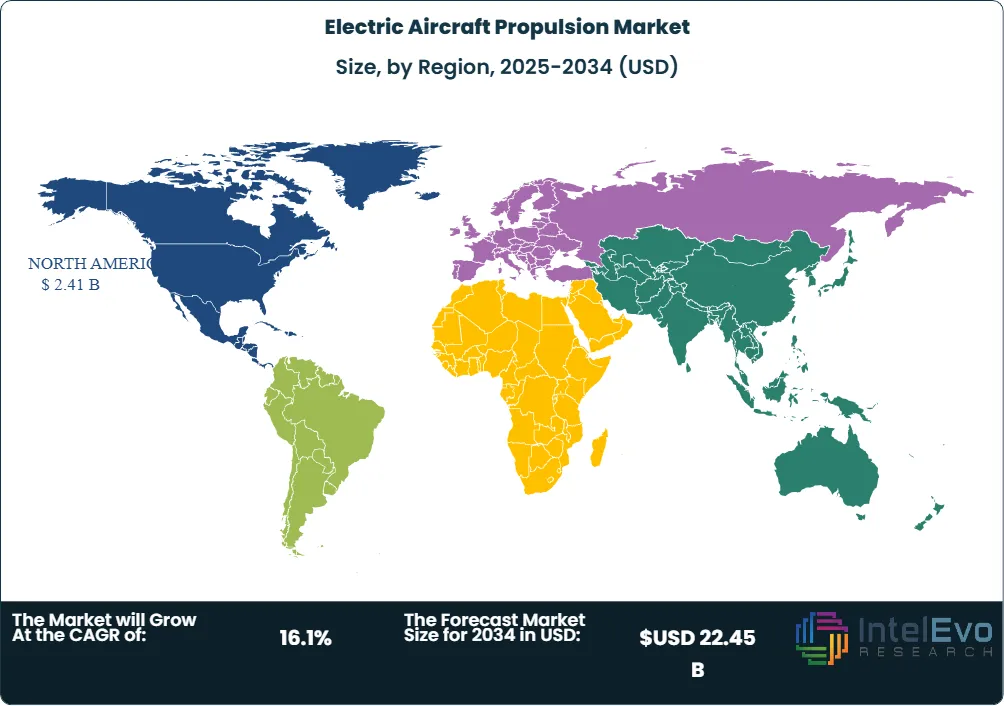

Defense and commercial demand has accelerated parallel investment streams. Vertical Aerospace expanded its Honeywell partnership in May 2025 to USD 1 Billion contract value covering at least 150 VX4 units by 2030. Archer Aviation maintains a USD 6 Billion backlog with United Airlines (USD 1.5 Billion conditional order), Future Flight Global, Soracle, Ethiopian Airlines, Abu Dhabi Aviation, and the U.S. Air Force. Beta Technologies completed its IPO on the New York Stock Exchange in November 2025 with USD 971 Million projected 2026 net cash and ALIA-250 customers including UPS, United Therapeutics, and Air New Zealand. Regionally, North America held 41.2% revenue share in 2025, equating to approximately USD 2.41 Billion, anchored by FAA leadership, NASA EPFD, and U.S. eVTOL OEM concentration.

Market Definition and Scope

The electric aircraft propulsion market is defined as the segment of aerospace and advanced materials covering propulsion subsystems for fully electric, hybrid-electric, and More Electric Aircraft platforms. The market encompasses electric motors and generators (high-specific-power above 5 kW/kg), power electronics (inverters, DC-DC converters, high-voltage distribution), aviation-grade lithium-ion and emerging solid-state batteries, hybrid-electric controllers, and supporting thermal management. Vehicle categories include eVTOL aircraft (multirotor, lift-plus-cruise, vectored thrust, tilt-rotor), eCTOL aircraft, hybrid-electric regional aircraft, light and ultralight electric aircraft, and More Electric Aircraft commercial platforms.

This analysis covers OEM platforms, propulsion subsystem suppliers, battery and power electronics suppliers, and supporting infrastructure. Major participants include Joby Aviation, Archer Aviation, Beta Technologies, Vertical Aerospace, Lilium, Volocopter, EHang, Eve Air Mobility, magniX, Honeywell International, Safran SA, GE Aerospace, RTX Corporation (Pratt and Whitney, Collins Aerospace), and Rolls-Royce Electrical. Excluded from this scope are conventional jet engines without electrification, hydrogen fuel cell powertrains classified under hydrogen-electric aviation as a separate category, and ground-based eVTOL infrastructure such as vertiports. The parent global aircraft electrification market reached approximately USD 14.29 Billion in 2025; electric propulsion subsystems represented approximately 41% of that parent market value.

, By Propulsion Component (Electric Motors, Batteries, Power Electronics, Turbogenerators, Hydrogen Fuel Cells), By Application (Passenger, Cargo Delivery, Military, Agriculture), By End-User (Airlines, Logistics, Defense, Flight Schools) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

Key Takeaways

- Market Growth: The electric aircraft propulsion market expanded from USD 5.85 Billion in 2025 toward a projected USD 22.45 Billion by 2034, registering a CAGR of 16.1% during the forecast period.

- Segment Dominance by Platform: eVTOL platforms captured approximately 60.22% revenue share of the broader electric aircraft market in 2025, while More Electric Aircraft fixed-wing programs anchor 27.4% of propulsion subsystem revenue.

- Segment Dominance by Component: Batteries and energy storage represented approximately 36% of propulsion-attributed component value in 2025, while electric motors and generators captured 22% with the segment growing fastest at 18.4% CAGR.

- Driver: The White House eVTOL Integration Pilot Program (eIPP) directed by Presidential Executive Order enables Joby Aviation, Archer Aviation, and competitors to begin commercial operations in 2026 ahead of full FAA Type Certification across 10 selected states including New York, New Jersey, Arizona, Florida, Idaho, North Carolina, Oklahoma, Oregon, Texas, and Utah.

- Restraint: Aviation-grade battery energy density at 250 to 300 Wh/kg system-level constrains range and payload, limiting fully electric eVTOL to short-sea regional and urban routes; solid-state batteries above 500 Wh/kg are required for regional missions exceeding 200 nautical miles.

- Opportunity: Joby Aviation reported sector-leading certification progress with an 18-point increase in FAA Stage 4 advancement on February 25, 2026, supporting potential aircraft and services sales exceeding USD 1 Billion as production scales to 24 aircraft per year across Marina, California (435,000 square feet) and Dayton, Ohio.

- Trend: Megawatt-class hybrid-electric propulsion advances with the magniX magni650 demonstrating 700 kW continuous power output at 30,000 feet simulated altitude during NASA NEAT facility tests, supported by 60% of active demonstrators using high-voltage 540 to 800 V architectures.

- Regional: North America held the largest regional share at 41.2%, equating to approximately USD 2.41 Billion in 2025, anchored by FAA leadership, NASA EPFD, and the concentration of leading eVTOL OEMs in California, Vermont, and Washington.

Key Insights Summary

- On April 27, 2026 Joby Aviation executed inaugural point-to-point eVTOL demonstration sorties across New York City using its JAS4-1 aircraft (tail number N545JX), bridging JFK International Airport with Downtown Skyport and the East 34th and West 30th Street heliports in under 10 minutes; over 2025 the company logged more than 40,000 flight test miles across nearly 600 sorties.

- In a Form 8-K filed February 25, 2026 Joby disclosed an industry-best 18-percentage-point quarterly advance in FAA Stage 4 Type Certification status, with every airframe needed for Type Inspection Authorization (TIA) now on the production line and FAA test-pilot sorties expected to follow shortly.

- During May 2025 Vertical Aerospace and Honeywell International widened their VX4 partnership, with the expanded scope projected at USD 1 Billion of contract value across a minimum of 150 aircraft by 2030 and anchored by Honeywell propulsion electronics integration.

- Beta Technologies executed an NYSE listing in November 2025 (ticker BETA), with sell-side consensus modeling roughly USD 971 Million of net cash by the close of 2026 and no equity raise required until operating cash flow turns positive in 2030 across customer relationships spanning UPS, United Therapeutics, Air New Zealand, and Eve Air Mobility.

- Archer Aviation secured FAA acceptance of the Midnight eVTOL certification basis in November 2025, reportedly representing 90% FAA compliance and underwriting a USD 6 Billion conditional order book that includes USD 1.5 Billion from United Airlines, plus commitments from Future Flight Global, Soracle, Ethiopian Airlines, Abu Dhabi Aviation, and the U.S. Air Force.

- In December 2024 the magniX magni650 propulsion unit completed testing at the NASA NEAT facility, registering 700 kilowatts of continuous output at simulated 30,000-foot altitude under the NASA Electrified Powertrain Flight Demonstration (EPFD) program; in-flight tests on the De Havilland Dash 7 testbed are slated for 2026.

Competitive Landscape Overview

The electric aircraft propulsion market is moderately consolidated at the established aerospace tier and highly competitive at the venture-backed eVTOL OEM tier. Established Tier 1 propulsion suppliers, including Honeywell International Inc., Safran SA, GE Aerospace, RTX Corporation (Pratt and Whitney, Collins Aerospace), and Rolls-Royce Electrical, anchor component supply across multiple OEMs. Vertically integrated eVTOL platform leaders include Joby Aviation, Archer Aviation, Beta Technologies, Vertical Aerospace, Lilium, and EHang. Industry analysis indicates over 500 eVTOL companies active worldwide, with approximately 183 eVTOLs delivered in 2024 and trade association projections of over 15% CAGR reaching 10,000+ cumulative deliveries by 2040. Competition is technology-led across three architectures: vertically integrated TaaS providers (Joby with Toyota, Uber, and Delta partnerships), OEM platforms relying on Tier 1 suppliers (Archer with Stellantis, Vertical with Honeywell), and pure-play propulsion specialists (magniX, Hybrid Air Vehicles). New entrants include Skyfly (Axe SN001 received FAA Experimental Permit October 2025), Eviation, Wright Electric, Heart Aerospace, Pipistrel, Bye Aerospace, and ZeroAvia hydrogen-electric. Boeing Wisk and Embraer Eve anchor incumbent OEM responses.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

| Honeywell International Inc. | Charlotte, USA | Leader | Electric propulsion, power generation, flight control electronics | North America, Europe, Global | Vertical Aerospace partnership expanded May 2025 to 150 VX4 units by 2030 |

| Joby Aviation, Inc. | Santa Cruz, USA | Leader | JAS4-1 eVTOL aircraft; vertically integrated propulsion | North America, UAE | First NYC point-to-point demonstration flights completed April 27, 2026 |

| Archer Aviation Inc. | San Jose, USA | Leader | Midnight eVTOL; tilt-rotor electric propulsion | North America, UAE | FAA acceptance of Midnight certification basis announced November 2025 |

| magniX | Everett, Washington, USA | Leader | magni650 EPU; Samson 450-kWh battery packs | North America | magni650 NASA EPFD flight tests on Dash 7 commencing 2026 |

| Safran SA | Paris, France | Challenger | ENGINeUS electric motor; ECOPulse hybrid-electric propulsion | Europe, Global | EU Clean Aviation participation in EcoPulse hybrid-electric flight tests |

| GE Aerospace | Cincinnati, Ohio, USA | Challenger | Megawatt-class hybrid-electric powertrain (CT7-9B testbed) | North America, Europe | NASA EPFD funding constrained under FY2026 budget reductions |

| RTX Corporation (Pratt & Whitney, Collins Aerospace) | Arlington, Virginia, USA | Challenger | PT6A hybrid-electric program; STEP-Tech demonstrator | North America, Europe, Global | JetZero blended-wing demonstrator power units integration March 2025 |

| Beta Technologies | Burlington, Vermont, USA | Challenger | ALIA-250 eCTOL and eVTOL; UPS, Air New Zealand customers | North America | IPO completed November 2025 with USD 971 Million projected 2026 net cash |

| Vertical Aerospace Ltd. | Bristol, United Kingdom | Niche Player | VX4 eVTOL with Honeywell propulsion electronics | Europe | Honeywell partnership expanded May 2025 to USD 1 Billion contract value |

| EHang Holdings Ltd. | Guangzhou, China | Niche Player | EH216-S autonomous passenger eVTOL | China, Asia Pacific | First commercial passenger eVTOL operations launched in China |

By Platform Type

The electric aircraft propulsion market by platform type is led by eVTOL aircraft, which captured approximately 60.22% revenue share of broader electric aircraft platform value in 2025 driven by urban air mobility (UAM), regional air mobility (RAM), and air taxi commercialization. Multirotor, lift-plus-cruise, tilt-rotor, and vectored thrust eVTOL configurations anchor segment volumes. Vectored thrust held 64% share of eVTOL platform value in 2024 due to operational range and payload flexibility, with lift-plus-cruise projected to grow fastest as energy efficiency optimization advances. eCTOL aircraft, including Beta Technologies' ALIA-250, captured 14.6% share, with cargo and logistics anchoring near-term commercial revenue.

Hybrid-electric regional aircraft represented 12.4% share, projected to grow at 18.6% CAGR through 2034 supported by NASA EPFD demonstrations and Pratt and Whitney Canada hybrid-electric programs. Light and ultralight electric aircraft captured 8.3% share led by Pipistrel Velis Electro and Bye Aerospace eFlyer training applications. More Electric Aircraft commercial platform retrofits including Boeing 787 bleed-less architecture contributed 4.5% share. Comparison: vertically integrated TaaS eVTOL platforms (Joby) commanded a 2.8x higher revenue per aircraft economic value than OEM-only sales (Archer, Vertical) due to operating service margins, although both models compete in the certification race.

By Propulsion Component

The electric aircraft propulsion market by component is led by batteries and energy storage at approximately 36% revenue share in 2025. Lithium-ion batteries captured 67% share within the battery segment in 2025, with solid-state batteries projected to grow at the fastest CAGR driven by higher energy density above 500 Wh/kg, improved safety, and longer lifecycle. Electric motors and generators held 22% share of propulsion components, growing at the fastest 18.4% CAGR with magniX, Safran ENGINeUS, MagniX, MGM COMPRO, and EMRAX anchoring high-specific-power offerings (10 to 15 kW/kg in prototypes).

Power electronics, including inverters, DC-DC converters, and high-voltage distribution units, captured 26% share. Wide bandgap SiC and GaN power stages deliver greater than 98% inverter efficiency, with high-voltage 540 to 800 V architectures featured in 60% of active demonstrators. Thermal management systems, MRO, certification services, and ground charging infrastructure made up the residual 16% share. Procurement leads at eVTOL OEMs and aerospace primes should evaluate propulsion subsystem selection against three criteria: FAA Part 33 or Part 35 certification basis (or eVTOL-specific G-1 certification blueprint), specific power rating in kW/kg at certified altitude, and supplier production qualification under AS9100 quality management systems.

By Application

The electric aircraft propulsion market by application is led by passenger air taxi and urban air mobility at approximately 38% share in 2025, anchored by Joby Aviation, Archer Aviation, Lilium, Volocopter, and EHang programs. Cargo and logistics applications captured 21% share with UPS contracting Beta Technologies' ALIA-250, and Wing, Zipline, and Matternet operating smaller-scale electric drone delivery. Military and defense applications represented approximately 47% of the broader electric aircraft market in 2025 per industry analysis, anchored by U.S. Department of Defense Defense Innovation Unit (DIU) procurement and AUKUS naval autonomous trials. Commercial regional aviation captured 8% share with Heart Aerospace, Surf Air Mobility, and Eviation Alice anchoring development.

Pilot training and flight school applications held 6% share, anchored by Pipistrel Velis Electro (the first FAA Type Certified electric airplane), H55 Bristell Energic, and Bye Aerospace eFlyer. Emergency medical services and HEMS captured 3.4% share, with eVTOL air ambulance trials advancing in the United Arab Emirates. ROI calculation for eVTOL platform deployment must account for FAA Type Certification timeline (typically 5 to 8 years from G-1 to TIA completion), aircraft unit cost (USD 1.3 to 4 Million), production scale economics (24 aircraft per year at Joby Marina California; 4 per month projected by 2027), and TaaS revenue per flight hour.

By End-User

The electric aircraft propulsion market by end-user is led by commercial airlines and air taxi operators at approximately 42% share in 2025. United Airlines (Archer USD 1.5 Billion order), Delta Air Lines (Joby partnership), Japan Airlines, All Nippon Airways, Ethiopian Airlines, and Abu Dhabi Aviation anchor commercial demand. Cargo and logistics operators including UPS, FedEx, and Air New Zealand contributed 18% share, primarily through Beta Technologies and Wisk Aero engagements. Military and defense procurement, anchored by U.S. Air Force Agility Prime, U.S. Navy MASC parallel procurement, and NATO partner programs, captured 28% share. Aerospace OEMs including Boeing (via Wisk subsidiary investment), Airbus, Embraer (via Eve), and Hyundai Motor Group (Supernal subsidiary) drove 9% share through joint development. Research institutes including NASA Glenn, NASA Armstrong, and the European Clean Aviation Joint Undertaking drove the residual 3% share through demonstration program funding.

Regional Analysis

The electric aircraft propulsion market by region is led by North America at 41.2% revenue share in 2025, equating to approximately USD 2.41 Billion. The United States dominates with FAA leadership, NASA EPFD funding, and concentrated venture activity in California (Joby Aviation Santa Cruz, Archer Aviation San Jose), Vermont (Beta Technologies Burlington), Washington (magniX Everett), and Ohio (Joby Dayton manufacturing). The White House eVTOL Integration Pilot Program (eIPP) selected New York, New Jersey, Arizona, Florida, Idaho, North Carolina, Oklahoma, Oregon, Texas, and Utah for early commercial operations. Canada anchors regional supply through Pratt and Whitney Canada (Longueuil) hybrid-electric turboprop programs and ATI Inc. testbed integration.

Europe held 28.6% share in 2025, equivalent to approximately USD 1.67 Billion. The European Union Aviation Safety Agency (EASA) administers Type Certification under SC-VTOL framework. Clean Aviation grants and the EU Green Deal channel public funds into liquid-hydrogen handling, superconducting cables, and hybrid-electric flight tests through projects including GOLIAT and EcoPulse. France hosts Safran SA (Paris) with the ENGINeUS electric motor and ECOPulse partnership. Germany hosts Lilium and Volocopter eVTOL programs alongside MTU Aero Engines hybrid-electric R&D. The United Kingdom anchors classification innovation through Vertical Aerospace (Bristol) and the UK Civil Aviation Authority (CAA). Switzerland hosts H55 (Sion) on training applications, while the Nordics host Heart Aerospace (Sweden) for regional 30-passenger ES-30.

Asia Pacific captured 22.4% share in 2025, valued at approximately USD 1.31 Billion, projected at the fastest regional CAGR of 24.77% through 2035. China leads regional development through EHang Holdings (Guangzhou) with the EH216-S autonomous passenger eVTOL achieving NMPA-equivalent commercial operations launch, AutoFlight, Xpeng AeroHT, and CATL battery supply integration. Japan hosts Suzuki, Honda Aircraft Company, and SkyDrive eVTOL development supported by METI funding and the World Expo 2025 Osaka Joby flight tests. South Korea anchors through Hyundai Motor Group's Supernal subsidiary developing the SA-2 eVTOL. Australia contributes through magniX heritage operations and AMSL Aero Vertiia.

Middle East and Africa held 5.6% share in 2025, approximately USD 328 Million, projected at the fastest regional CAGR through 2030. The United Arab Emirates serves as launch market for Joby Aviation Dubai (Uber partnership) and Archer Aviation Abu Dhabi commercial operations targeted for 2026. Saudi Arabia advances under Vision 2030 with NEOM eVTOL pilots.

Latin America contributed 2.2% share, valued at approximately USD 129 Million in 2025. Brazil leads through Embraer-backed Eve Air Mobility (NYSE: EVEX) with Beta Technologies propulsion supply, plus Thales and BAE Systems partnerships.

Country Analysis

United States

The electric aircraft propulsion market in the United States was valued at approximately USD 2.18 Billion in 2025 and is projected to grow at a CAGR of 17.4% during 2025-2034, the fastest among major country markets. The FAA leads global certification standards with Joby Aviation in late Stage 4 Type Certification (an industry-best 18-percentage-point quarterly advance disclosed February 25, 2026) and Archer Aviation receiving certification basis acceptance November 2025. The White House eIPP enables 10-state commercial operations ahead of full certification. NASA EPFD funds magniX magni650 hybrid-electric Dash 7 flight tests through 2026, although FY2026 federal budget cuts reduced program funding. The Department of Defense Defense Innovation Unit and U.S. Air Force Agility Prime program support military eVTOL procurement. State-level activity concentrates in California, Vermont, Washington, and Ohio.

United Kingdom

The United Kingdom's electric aircraft propulsion market reached approximately USD 320 Million in 2025 with a country CAGR of 13.8% during 2025-2034. Vertical Aerospace Ltd. (Bristol, NYSE: EVTL) anchors domestic activity with the VX4 eVTOL targeting UK Civil Aviation Authority (CAA) and EASA certification in 2028 followed by FAA validation. The May 2025 Honeywell partnership extension to USD 1 Billion contract value supports VX4 production scaling. The CAA Future Flight Challenge funds UK eVTOL R&D, while Rolls-Royce Electrical (Derby) advances superconducting motor research alongside ZeroAvia (Cotswold) hydrogen-electric programs. Aerospace innovation clusters in Bristol, Derby, and Cranfield support translational development.

China

China's electric aircraft propulsion market reached approximately USD 745 Million in 2025 with a country CAGR of 18.6% during 2025-2034, anchored by domestic production and government-backed urban air mobility initiatives. EHang Holdings Limited (Guangzhou, NASDAQ: EH) launched commercial passenger eVTOL operations in China and obtained type certification for the EH216-S autonomous platform. AutoFlight, Xpeng AeroHT, and Volant Aerotech compete on lift-plus-cruise and tilt-rotor configurations. CATL and BYD anchor battery supply at scale, while the Civil Aviation Administration of China (CAAC) administers airworthiness certification. The Made in China 2025 initiative emphasizes domestic eVTOL leadership with significant public investment in Shenzhen, Guangzhou, and Suzhou test corridors.

France

France's electric aircraft propulsion market reached approximately USD 285 Million in 2025 with a country CAGR of 13.2% during 2025-2034. Safran SA (Paris) anchors domestic production through the ENGINeUS electric motor and ECOPulse hybrid-electric flight test program with Daher and Airbus partners. Airbus Group leads pan-European integration, while Thales contributes navigation and avionics. The French Civil Aviation Authority (DGAC) coordinates with EASA on Type Certification basis development. Public funding through the France 2030 program and Bpifrance supports eVTOL and hybrid-electric R&D. Aerospace clusters in Toulouse, Paris-Le Bourget, and Bordeaux concentrate manufacturing and test infrastructure.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Platform Type

- Fixed-Wing Aircraft

- Rotary-Wing Aircraft

- Electric Vertical Take-Off and Landing (eVTOL) Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Advanced Air Mobility (AAM) Aircraft

- Others

By Propulsion Component

- Electric Motors

- Batteries and Energy Storage Systems

- Power Electronics

- Propellers

- Power Distribution Systems

- Thermal Management Systems

- Battery Management Systems (BMS)

- Aircraft Propulsion Control Systems

- Others

By Application

- Commercial Aviation

- Urban Air Mobility (UAM)

- Military and Defense Aviation

- Cargo and Logistics

- General Aviation

- Air Taxi Services

- Pilot Training Aircraft

- Surveillance and Reconnaissance

- Others

By End-User

- Aircraft Manufacturers (OEMs)

- Airlines and Air Operators

- Military and Defense Organizations

- Urban Air Mobility Operators

- Cargo and Logistics Companies

- Research and Academic Institutions

- Government Aviation Agencies

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.85 B |

| Forecast Revenue (2034) | USD 22.45 B |

| CAGR (2025-2034) | 16.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Platform Type, (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Electric Vertical Take-Off and Landing (eVTOL) Aircraft, Unmanned Aerial Vehicles (UAVs), Advanced Air Mobility (AAM) Aircraft, Others), By Propulsion Component, (Electric Motors, Batteries and Energy Storage Systems, Power Electronics, Propellers, Power Distribution Systems, Thermal Management Systems, Battery Management Systems (BMS), Aircraft Propulsion Control Systems, Others), By Application, (Commercial Aviation, Urban Air Mobility (UAM), Military and Defense Aviation, Cargo and Logistics, General Aviation, Air Taxi Services, Pilot Training Aircraft, Surveillance and Reconnaissance, Others), By End-User, (Aircraft Manufacturers (OEMs), Airlines and Air Operators, Military and Defense Organizations, Urban Air Mobility Operators, Cargo and Logistics Companies, Research and Academic Institutions, Government Aviation Agencies, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HONEYWELL INTERNATIONAL INC., JOBY AVIATION, INC., ARCHER AVIATION INC., MAGNIX, SAFRAN SA, GE AEROSPACE, RTX CORPORATION (PRATT & WHITNEY, COLLINS AEROSPACE), BETA TECHNOLOGIES, VERTICAL AEROSPACE LTD., EHANG HOLDINGS LIMITED, LILIUM GMBH, VOLOCOPTER GMBH, WISK AERO (BOEING), EVE AIR MOBILITY (EMBRAER), AIRBUS SE, ROLLS-ROYCE ELECTRICAL, HYUNDAI MOTOR GROUP (SUPERNAL), AUTOFLIGHT, XPENG AEROHT, PIPISTREL GROUP, EVIATION AIRCRAFT, WRIGHT ELECTRIC, HEART AEROSPACE, BYE AEROSPACE, H55, ZEROAVIA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Propulsion Component (Electric Motors, Batteries, Power Electronics, Turbogenerators, Hydrogen Fuel Cells), By Application (Passenger, Cargo Delivery, Military, Agriculture), By End-User (Airlines, Logistics, Defense, Flight Schools) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

, By Propulsion Component (Electric Motors, Batteries, Power Electronics, Turbogenerators, Hydrogen Fuel Cells), By Application (Passenger, Cargo Delivery, Military, Agriculture), By End-User (Airlines, Logistics, Defense, Flight Schools) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

, By Propulsion Component (Electric Motors, Batteries, Power Electronics, Turbogenerators, Hydrogen Fuel Cells), By Application (Passenger, Cargo Delivery, Military, Agriculture), By End-User (Airlines, Logistics, Defense, Flight Schools) Region & Key Players-Segment Overview, Dynamics, Trends & Forecast 2026-2035")

Frequently Asked Questions

How big is the Electric Aircraft Propulsion Market?

The Global Electric Aircraft Propulsion Market was valued at USD 5.20 Billion in 2024 and USD 5.85 Billion in 2025, and is projected to reach USD 22.45 Billion by 2034, growing at a CAGR of 16.1% from 2026 to 2034. Market growth is driven by electric propulsion systems, eVTOL aircraft, sustainable aviation, and advanced air mobility.

Who are the major players in the Electric Aircraft Propulsion Market?

HONEYWELL INTERNATIONAL INC., JOBY AVIATION, INC., ARCHER AVIATION INC., MAGNIX, SAFRAN SA, GE AEROSPACE, RTX CORPORATION (PRATT & WHITNEY, COLLINS AEROSPACE), BETA TECHNOLOGIES, VERTICAL AEROSPACE LTD., EHANG HOLDINGS LIMITED, LILIUM GMBH, VOLOCOPTER GMBH, WISK AERO (BOEING), EVE AIR MOBILITY (EMBRAER), AIRBUS SE, ROLLS-ROYCE ELECTRICAL, HYUNDAI MOTOR GROUP (SUPERNAL), AUTOFLIGHT, XPENG AEROHT, PIPISTREL GROUP, EVIATION AIRCRAFT, WRIGHT ELECTRIC, HEART AEROSPACE, BYE AEROSPACE, H55, ZEROAVIA, Others

Which segments covered the Electric Aircraft Propulsion Market?

By Platform Type, (Fixed-Wing Aircraft, Rotary-Wing Aircraft, Electric Vertical Take-Off and Landing (eVTOL) Aircraft, Unmanned Aerial Vehicles (UAVs), Advanced Air Mobility (AAM) Aircraft, Others), By Propulsion Component, (Electric Motors, Batteries and Energy Storage Systems, Power Electronics, Propellers, Power Distribution Systems, Thermal Management Systems, Battery Management Systems (BMS), Aircraft Propulsion Control Systems, Others), By Application, (Commercial Aviation, Urban Air Mobility (UAM), Military and Defense Aviation, Cargo and Logistics, General Aviation, Air Taxi Services, Pilot Training Aircraft, Surveillance and Reconnaissance, Others), By End-User, (Aircraft Manufacturers (OEMs), Airlines and Air Operators, Military and Defense Organizations, Urban Air Mobility Operators, Cargo and Logistics Companies, Research and Academic Institutions, Government Aviation Agencies, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Electric Aircraft Propulsion Market

Published Date : 30 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date