- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Electric Vehicle Charging Management Software Market Size | CAGR 16.2%

Global Electric Vehicle Charging Management Software Market Size, Share, Growth Analysis By Deployment (Cloud-Based, On-Premise), By Application (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level (DC Fast Charging, AC Level 2, AC Level 1), By End-User (Commercial, Public Charging Networks, Residential, Fleet & Transportation), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

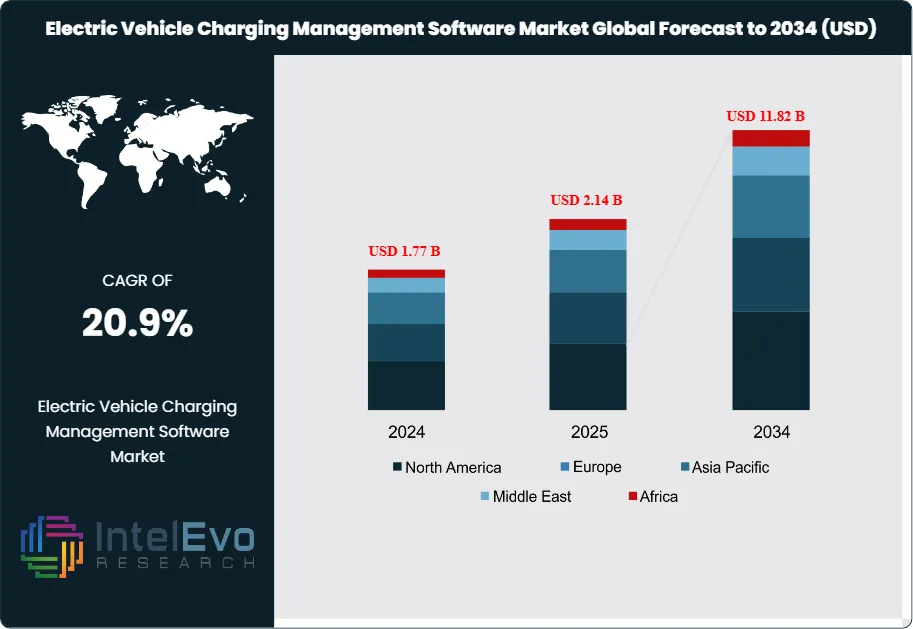

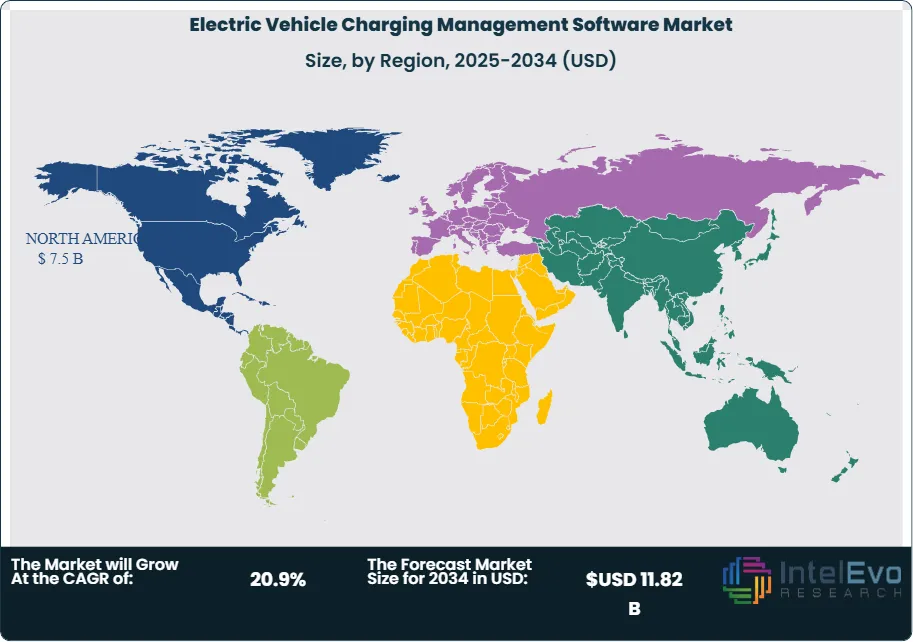

| USD 2.14 Billion | USD 11.82 Billion | 20.9% | North America, 36.8% |

The Electric Vehicle Charging Management Software Market was valued at approximately USD 1.77 Billion in 2024 and reached USD 2.14 Billion in 2025. The market is projected to grow to USD 11.82 Billion by 2034, expanding at a CAGR of 20.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 9.68 Billion over the analysis period — a trajectory sustained by the compounding intersection of accelerating EV fleet penetration creating raw demand for charging infrastructure management, grid integration requirements converting simple on-off charging control into a complex real-time energy optimization function, and regulatory frameworks across three major EV markets mandating interoperability standards that functionally require software management layers between hardware and grid operators.

Get More Information about this report -

Request Free Sample ReportThe first specific causal trigger behind the market's current growth rate is the scale inflection in deployed public charging infrastructure that crossed operational complexity thresholds in 2024 and 2025. The International Energy Agency's 2025 Global EV Outlook reported 12.4 million publicly accessible charging points globally at end-2024, up from 5.8 million at end-2022 — a 114% expansion in two years that transformed the operational challenge from deploying hardware to managing distributed energy assets at utility scale. A network operator managing 500 charging points can rely on manual monitoring and reactive maintenance; an operator managing 50,000 points across multiple geographies, tariff regimes, and grid connection types requires software that automates fault detection, demand forecasting, price signal ingestion, and settlement reconciliation. ChargePoint's 330,000-port network processes approximately 2.4 million charging sessions monthly — a transaction volume comparable to a mid-size payment processor — generating real-time data flows that only purpose-built software platforms can manage without prohibitive manual overhead.

A second structural trigger is the transition of EV charging from a passive load on distribution grids to an active grid resource under regulatory frameworks explicitly designed to monetize EV battery capacity. The European Union's Alternative Fuels Infrastructure Regulation (AFIR), fully applicable from April 2025, mandates that all publicly accessible charging stations above 50 kW display real-time dynamic pricing aligned with wholesale electricity market signals — a requirement that fundamentally transforms charging station software from a billing tool into a real-time electricity market participant. Simultaneously, the U.S. Federal Highway Administration's National Electric Vehicle Infrastructure program conditions USD 7.5 billion in state grants on charger compliance with OCPP 2.0.1 open protocol standards that enable third-party software management — effectively mandating software platform adoption for any operator accepting federal funding. These twin regulatory requirements, one pricing-oriented and one interoperability-oriented, have expanded the addressable market beyond charge point operators to include distribution utilities, energy retailers, and fleet managers who had previously treated charging as an infrastructure procurement decision rather than a software-intensive energy management challenge.

Technology maturation provides the third enabling condition. Open Charge Point Protocol version 2.0.1, finalized in 2020 and achieving broad hardware support by 2024, enables ISO 15118 Plug & Charge vehicle authentication, bidirectional Vehicle-to-Grid communication, and secure remote firmware updates — capabilities that require sophisticated software orchestration layers and create clear commercial separation between hardware commoditization and software differentiation. As Level 2 and DC fast charger hardware margins compress under Chinese manufacturer competition — CATL-affiliated hardware vendors entered European markets with AC Level 2 hardware priced 35–45% below Western incumbents in 2024 — charging management software becomes the primary margin-retention mechanism for network operators. This hardware commoditization dynamic, which mirrors the trajectory of Wi-Fi access point hardware in the 2010s where Cisco and Aruba transitioned from hardware-led to software-led business models, explains why software management revenue is growing at 20.9% CAGR while hardware installation revenue grows at approximately 12–14% annually.

A contrarian observation is warranted before projecting smooth adoption. The electric vehicle charging management software market currently operates across four incompatible open protocol versions simultaneously — OCPP 1.6, OCPP 2.0, OCPP 2.0.1, and proprietary variants — with an estimated 38% of deployed charging hardware in the United States and 29% in Europe remaining on OCPP 1.6 as of mid-2025. Hardware operators facing a USD 2,000–8,000 per-port firmware upgrade cost to achieve OCPP 2.0.1 compliance for NEVI program eligibility are making hardware replacement decisions rather than software upgrades, creating a retrofit investment barrier that moderates the near-term adoption curve for advanced management software features in markets with older installed base concentrations. This installed base fragmentation is the most significant near-term constraint on realized software feature penetration despite nominally strong headline growth.

, By Application (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level (DC Fast Charging, AC Level 2, AC Level 1), By End-User (Commercial, Public Charging Networks, Residential, Fleet & Transportation), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global electric vehicle charging management software market reached USD 2.14 Billion in 2025 and is forecast to reach USD 11.82 Billion by 2034 at a CAGR of 20.9% during the 2026–2034 period, driven by the scale inflection of deployed public charging infrastructure past operational complexity thresholds and regulatory mandates for open-protocol software interoperability.

- Segment Dominance (By Deployment): Cloud-based deployment captured 67.4% of deployment-segmented revenue at USD 1.44 Billion in 2025 because managing distributed charging infrastructure across multiple geographies, grid tariff zones, and operator partnerships requires centralized real-time data aggregation that on-premise systems architecturally cannot provide without prohibitive multi-site infrastructure replication costs.

- Segment Dominance (By Application): Network management and monitoring held 31.2% of application revenue at USD 0.668 Billion in 2025, its leading position anchored by the operational necessity of real-time fault detection and remote diagnostics across large charging networks — a function that directly determines charging uptime rates, the primary metric network operators report to enterprise clients and municipal partners in service level agreements.

- Driver: The EU Alternative Fuels Infrastructure Regulation's April 2025 full applicability mandate for real-time dynamic pricing at all publicly accessible chargers above 50 kW, combined with the U.S. NEVI program's OCPP 2.0.1 compliance condition on USD 7.5 billion in infrastructure grants, created dual procurement mandates that converted charging management software from optional operational tooling to legally required infrastructure.

- Restraint: Protocol version fragmentation across OCPP 1.6, OCPP 2.0, and OCPP 2.0.1 — with an estimated 38% of U.S. installed charging hardware remaining on OCPP 1.6 as of mid-2025 — creates per-port firmware upgrade costs of USD 2,000–8,000 that operators evaluate against hardware replacement, moderating the near-term penetration rate of advanced management software features in markets with concentrated pre-2022 hardware installations.

- Opportunity: Vehicle-to-Grid software orchestration represents an addressable market expansion of USD 1.8–2.9 Billion by 2030, as bidirectional charging-capable EVs reach an estimated 18% share of new vehicle sales by 2027 and Transmission System Operator ancillary service markets in Europe and California open formal V2G aggregator participation pathways — a revenue stream that transforms EV charging management software from a cost-center tool into a grid revenue-generating platform.

- Trend: AI-driven smart charging and demand response optimization reached 42% software feature adoption among North American Tier-1 charging network operators in 2025 versus 19% in Asia Pacific, with documented energy cost reductions of 18–27% per site through time-of-use tariff optimization, creating a measurable ROI differential that is accelerating feature upgrade cycles at mid-market operators who previously deferred smart charging investment.

- Regional Analysis: North America held 36.8% of global electric vehicle charging management software revenue at USD 0.788 Billion in 2025, anchored by NEVI program spending requirements, the concentration of ChargePoint's 330,000-port managed network, and California Public Utilities Commission mandates requiring demand response participation for commercial charging stations above 10 kW connected to investor-owned utility grids.

Competitive Landscape Overview

The electric vehicle charging management software market is moderately fragmented, with the top four vendors — ChargePoint Holdings, Siemens eMobility, ABB, and Driivz — collectively accounting for an estimated 44.2% of total market revenue in 2025. The competitive landscape bifurcates between vertically integrated hardware-software platform vendors (ChargePoint, Siemens, ABB, Schneider Electric) that bundle management software with proprietary charging hardware, and pure-play software specialists (Driivz, AMPECO, EV Connect) that operate hardware-agnostic platforms across multiple charger manufacturer ecosystems. Hardware-software bundled vendors command higher initial contract values — USD 3–15 million for Tier-1 network deployments — but face margin compression as hardware commoditizes. Pure-play software vendors achieve faster cross-hardware deployment and compete primarily on platform configurability, protocol breadth, and white-label packaging flexibility. In 2025, competitive dynamics shifted markedly as OCPP 2.0.1 standardization reduced hardware lock-in advantages for bundled vendors, enabling software-only specialists to onboard previously proprietary hardware estates and compressing the differentiation value of hardware-software integration. Concurrently, four major European utilities — including subsidiaries of E.ON, Iberdrola, and Engie — launched internally developed charging management software platforms for their own network operations, entering as self-supply competitors that reduce the addressable commercial software market within utility-owned charging infrastructure.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (2024–2026) |

| ChargePoint Holdings | USA | Leader | ChargePoint Cloud Management Platform | North America / Europe | Launched ChargePoint Assure predictive maintenance module in Feb 2025, using IoT sensor telemetry to forecast hardware failures 72 hours in advance, reducing charger downtime by 31% across its 330,000+ port network. |

| Siemens AG (eMobility) | Germany | Leader | Siemens eMobility Management Suite | Europe / North America | Integrated Siemens SICHARGE management software with Gridscale X demand response API in Q1 2025, enabling real-time load-shifting across 14 European Distribution System Operator grids under ENTSO-E balancing market rules. |

| ABB Ltd. | Switzerland | Leader | ABB Ability e-mobility Platform | Europe / Asia Pacific | Deployed ABB Ability fleet charging optimization across 23 European urban bus depots in Sep 2025, managing 1,200 MW of overnight depot charging capacity through predictive scheduling integrated with day-ahead electricity markets. |

| Driivz | Israel / USA | Leader | Driivz EV Charging Management Platform | Europe / North America | Secured a 10-year white-label platform agreement with a top-5 European utility in Nov 2025, covering software management for 85,000 public and destination charging ports across six countries. |

| Schneider Electric | France | Challenger | EcoStruxure EV Charging Expert | Europe / North America | Released EcoStruxure EV Charging Expert v4.0 in Mar 2025 with ISO 15118 Plug & Charge protocol support, enabling automatic vehicle authentication and billing for 40+ EV models at Schneider-managed sites. |

| AMPECO | Bulgaria / UK | Challenger | AMPECO EV Charging Platform | Europe / North America | Raised USD 22 million Series B in Jun 2025 to expand white-label platform coverage to North America and Asia Pacific, adding OCPP 2.0.1 and OCPI 2.3 protocol support for 180+ hardware partner integrations. |

| EVBox Group | Netherlands | Challenger | EVBox Everon Management Software | Europe / North America | Launched Everon Fleet module in Jan 2026 targeting commercial vehicle depot operators, providing driver ID-based charging authorization, cost allocation by vehicle, and EV-specific energy procurement analytics. |

| Enel X Way | Italy | Challenger | JuiceNet Enterprise Platform | Europe / North America / LATAM | Extended JuiceNet V2G (Vehicle-to-Grid) beta deployment to 4,200 Nissan Leaf and Mitsubishi Outlander PHEV owners in Italy in Oct 2025 under an Terna grid balancing services agreement worth EUR 8 million annually. |

| Blink Charging | USA | Niche Player | Blink Network Management Platform | North America | Deployed 4,200 new Level 2 commercial chargers across U.S. retail and grocery locations in 2025, expanding Blink Network to 105,000+ ports; launched AI-driven revenue optimization module in Aug 2025. |

| Hubject GmbH | Germany | Niche Player | Intercharge Network / eRoaming Hub | Europe / Asia Pacific | Extended Intercharge eRoaming protocol to South Korea and Taiwan in Q2 2025, connecting 340,000+ charging points across 18 countries into a single cross-operator roaming settlement network. |

By Deployment

Cloud-based deployment dominated the electric vehicle charging management software market at 67.4% of revenue and USD 1.44 Billion in 2025, a share grounded in the operational architecture requirements of large-scale distributed charging networks rather than in generic cloud adoption trends. Managing 10,000+ charging ports across multiple cities, grid operators, and time zones requires centralized real-time visibility into session status, hardware health, energy consumption, and revenue settlement — a data aggregation function that scales economically only through cloud infrastructure capable of ingesting millions of telemetry data points per hour. ChargePoint's cloud platform processes approximately 2.4 million monthly sessions across 330,000 ports, generating real-time state-of-charge, fault code, and transaction data that feeds its predictive maintenance and dynamic pricing engines. The cloud model's secondary advantage is software update propagation: ChargePoint can deploy firmware updates to its entire hardware estate within hours rather than the weeks required for on-premise update cycles, enabling rapid compliance with evolving OCPP protocol versions as NEVI program requirements change. The fastest-growing cloud sub-segment is multi-tenant white-label platforms — software infrastructure that charge point operators brand as proprietary — growing at an estimated 27.4% annually as regional operators seek enterprise-grade management capabilities without the development cost of building proprietary platforms.

On-premise deployment retained 32.6% of the market at USD 0.698 Billion in 2025, sustained by automotive OEM-operated private fleet charging depots, military and government facilities with network isolation requirements, and European utilities with data sovereignty obligations that prohibit transmission of grid-connected asset telemetry to non-EU cloud infrastructure under GDPR Article 46 restrictions. Volkswagen Group's European depot charging management for its commercial vehicle subsidiary Traton operates on an air-gapped on-premise architecture across 34 manufacturing and logistics facilities, processing charging data locally to prevent real-time EV fleet position data from transiting non-Group-controlled networks. On-premise deployments are growing more slowly at an estimated 12.8% annually, but represent a structurally persistent segment as automotive OEMs and grid-critical infrastructure operators face cybersecurity and data sovereignty requirements that cloud architectures cannot address without jurisdiction-specific infrastructure investments.

By Application

Network management and monitoring held 31.2% of application-segmented electric vehicle charging management software revenue at USD 0.668 Billion in 2025. Its leading position reflects a commercial logic specific to the charging network operating model: charging uptime is the primary SLA metric in enterprise, municipal, and fleet charging contracts, and automated fault detection with remote resolution capability is the foundational requirement before any advanced feature — energy optimization, V2G, dynamic pricing — can be credibly offered. A network operator reporting 85% uptime without automated monitoring relies on end-user fault reports that average 4.7 hours of undetected downtime per incident, compared with 47 minutes for operators using telemetry-based fault detection. ChargePoint's February 2025 Assure predictive maintenance module operationalized this advantage, reducing unplanned downtime by 31% through 72-hour failure prediction using voltage ripple, thermal cycling, and connector insertion frequency patterns that precede hardware failure.

Energy management and grid integration captured 26.8% of application revenue at USD 0.574 Billion in 2025, growing at the highest rate within the application segmentation at an estimated 28.6% annually. The specific event accelerating this sub-application is the EU AFIR regulation's real-time dynamic pricing mandate, which requires software capable of ingesting wholesale electricity market price signals — specifically from EPEX SPOT, Nord Pool, and OMIE — and transmitting time-differentiated tariffs to charging stations within 15-minute intervals. Implementing this requirement without software that automates price signal ingestion, tariff calculation, and OCPP protocol transmission would require continuous manual data entry across thousands of charging sites simultaneously, making automation not merely efficient but operationally necessary. Billing and payment processing at 22.4% and reservations and user management at 19.6% complete the application distribution, with roaming settlement becoming a rapidly growing billing sub-category as cross-operator eRoaming networks expand and charging sessions increasingly span multiple network operators within a single journey.

By Charging Level

DC fast charging (Level 3) generated 44.6% of charging-level segmented revenue at USD 0.954 Billion in 2025, commanding the largest software revenue share despite representing a smaller share of total installed port count because the complexity and value density of fast charging management justifies premium software investment. A 150 kW DC fast charger connected directly to a medium-voltage distribution grid requires active power management, demand charge mitigation, grid protection relay coordination, and session-level energy metering auditable to ISO 15118 standards — software functions generating 3.8–5.2x the management revenue per port compared with Level 2 AC chargers. Highway corridor fast charging sites along U.S. Interstate networks, typically operating 8–16 chargers at 150–350 kW each with combined site demand exceeding 2.5 MW, require sophisticated software orchestration to prevent demand spikes that would trigger utility demand charge thresholds representing USD 40,000–120,000 per month in additional electricity cost at commercial rates.

AC Level 2 charging contributed 41.8% of level-segmented revenue at USD 0.895 Billion in 2025, the dominant segment by port count where the software management value proposition centers on workplace and multi-family residential cost allocation, demand response participation, and utilization analytics that building owners use to optimize charger placement and capacity planning. Level 2 smart charging at workplace deployments achieved documented energy cost reductions of 18–27% through time-of-use tariff optimization in multi-site corporate fleet studies across three U.S. technology sector employers, generating ROI timelines of 14–22 months that procurement teams present to capital expenditure approval committees as standalone financial justifications for software licensing above baseline hardware-only deployments. AC Level 1 at 13.6% serves primarily residential applications where software management adds overnight smart charging scheduling and utility demand response enrollment capabilities.

By End-User

Commercial end-users — retail, hospitality, and workplace charging operators — represented 38.4% of end-user demand at USD 0.822 Billion in 2025. Commercial site operators adopt charging management software primarily to solve two distinct financial problems: eliminating unauthorized charging at paid stations, which depresses revenue capture by an estimated 14–22% at unmanaged commercial sites; and managing peak demand charges, which represent 30–45% of total electricity costs at commercial locations with DC fast charging installations. Grocery retailers in particular have become significant charging management software buyers following the recognition that EV drivers spend 22% longer in-store during charging sessions than non-charging shoppers — a behavioral data point that has elevated charging management from a facilities expense to a customer engagement revenue driver at Kroger, Whole Foods, and Walmart's real estate strategy teams.

Public charging networks held 29.7% of end-user revenue at USD 0.635 Billion in 2025, growing at 24.1% annually as national charging network operators — Electrify America, Blink, EVgo, and their European counterparts — scale infrastructure deployments that require enterprise-grade platform management. Fleet and transportation operators at 15.1% represent the fastest-growing end-user segment at an estimated 31.2% annually, driven by the accelerating electrification of commercial vehicle fleets under EU Stage V and U.S. EPA heavy-duty emissions standards and the complex depot management software requirements of multi-shift electric bus and delivery vehicle operations. Residential and multi-family at 16.8% completes the distribution, with utility-managed residential smart charging programs growing fastest within this category as demand response enrollment incentives expand across U.S. investor-owned utility territories.

Regional Analysis

North America

Backed by USD 7.5 billion in NEVI formula funding conditioning federal infrastructure grants on OCPP 2.0.1 open-protocol compliance — a requirement that functionally mandates third-party software management capability for any operator accepting federal subsidy — and the California Public Utilities Commission's mandatory demand response participation rules for commercial charging installations above 10 kW on investor-owned utility grids, North America's electric vehicle charging management software market captured 36.8% of global revenue at USD 0.788 Billion in 2025. The United States accounts for approximately 84% of North American market revenue, concentrated in California — home to 42% of U.S. registered EVs and the destination of 31% of total U.S. Level 2 and DC fast charger deployments — Texas, Florida, and the Northeast corridor states with active EV adoption incentives. ChargePoint's San Jose, California operational headquarters coordinates management of its 330,000-port network across all 50 U.S. states and Canadian provinces, generating the largest single-country managed charging dataset globally and establishing data-driven predictive analytics as the U.S. market's competitive benchmark. Canada contributed the regional balance, with British Columbia's Zero Emission Vehicle Act mandates driving Vancouver and Victoria metro area commercial charging deployments that BC Hydro manages through a proprietary charging management platform developed in partnership with ChargePoint.

Europe

Regulatory requirements under the EU Alternative Fuels Infrastructure Regulation's April 2025 full applicability deadline — mandating real-time dynamic pricing display, contactless payment acceptance, and ad hoc charging without mandatory registration at all publicly accessible charging points above 50 kW — fundamentally reshaped the software procurement landscape across the European electric vehicle charging management software market, which held 31.4% share worth USD 0.672 Billion in 2025. Germany led European demand through Autobahn GmbH's motorway charging concession program, which awarded software management contracts for 1,000+ motorway fast charging sites to Siemens eMobility and ABB in 2024–2025, and through the concentration of automotive OEM depot charging management at BMW's Leipzig and Mercedes-Benz's Sindelfingen manufacturing campuses. The Netherlands, home to the highest EV penetration rate in Europe at 35.4% of new car sales in 2024 and the largest public charging network density per capita globally, represents the most mature testing ground for advanced energy management features — Amsterdam-based network operator Allego operates 35,000+ charging points managed through Driivz's platform with real-time Dutch TSO frequency regulation signals. France's ENEDIS distribution network integration program, which mandates smart charging coordination between EDF-managed public chargers and local distribution transformers in 15 pilot cities, created significant energy management software procurement in 2025.

Asia Pacific

Manufacturing scale advantages concentrated in Guangdong province's EV supply chain ecosystem, combined with China's Ministry of Industry and Information Technology's 2025 mandate requiring all new public charging stations to implement GB/T 27930-2023 smart charging protocol compatibility, propelled Asia Pacific's electric vehicle charging management software market to 22.6% global share at USD 0.484 Billion in 2025. China dominated the APAC sub-market through sheer infrastructure scale — the People's Republic contained an estimated 6.8 million publicly accessible charging points as of end-2024, representing 55% of global installed capacity — but the software management revenue per port is substantially lower than in Western markets due to state-owned charging network operators that develop internal management platforms rather than purchasing from commercial vendors. Japan contributed significant software management revenue through Toyota and Honda corporate fleet electrification programs, with Nagoya-area automotive supplier complexes deploying workplace depot charging management software covering 28,000 employee EV charge points across Aichi prefecture. South Korea's EV charging market, dominated by KEPCO's publicly owned charging infrastructure, generated private-sector software revenue through the 340 independent charge point operators operating under KEPCO's open access program — a Korean Electric Vehicle Charging Business Association-mediated framework that Hubject's Intercharge eRoaming protocol connected to international networks in Q2 2025.

Latin America

Currency volatility and import duty structures on EV charging hardware constrained infrastructure deployment timelines across Latin America, yet the electric vehicle charging management software market still reached USD 0.120 Billion (5.6% global share) in 2025 as government-mandated charging networks and mining sector fleet electrification created defined software procurement events. Brazil dominated regional demand through ANEEL's Resolution 1000/2021 framework requiring electricity distributors to fund EV charging infrastructure in urban centers, with Enel Brasil and Neoenergia deploying utility-managed charging networks in São Paulo and Rio de Janeiro metropolitan areas that require commercial management software for session billing, demand monitoring, and ANEEL regulatory reporting. Chile's BYD-supplied electric bus fleet — the largest urban electric bus fleet in Latin America with 2,000+ units operating in Santiago as of 2025 — requires depot charging management software capable of coordinating overnight charging for 500+ buses per depot while respecting Coordinador Eléctrico Nacional grid injection limits during peak renewable generation periods. Colombia's Ministry of Transport's 2025 EV charging infrastructure regulation, requiring charging station operators above 10 units to implement remote management and real-time session reporting, created a defined compliance procurement event affecting 48 registered charging operators as of mid-2025.

Middle East & Africa

Saudi Arabia's National Renewable Energy Program target of 30% renewable electricity generation by 2030 — creating a surplus renewable generation profile during daylight hours that makes smart charging alignment with solar generation economically significant for commercial operators — and the UAE's EV Green Charger initiative committing 70,000 public charging points across Abu Dhabi and Dubai by 2030, opened material demand corridors that pushed the MEA electric vehicle charging management software market to USD 0.077 Billion (3.6% share) in 2025. The UAE's Abu Dhabi Distribution Company and DEWA's green mobility program represent the two largest current software procurement sources in the region, with DEWA's 3,500-point Green Charger network managed through a platform procured from an ABB-affiliated software partner. Saudi Arabia's NEOM smart city project infrastructure plan specifies 100% EV transportation within the NEOM development zone and has issued software management platform tenders covering 12,000 planned charging points across THE LINE and Sindalah development phases. South Africa's Eskom-adjacent charging network, while constrained by load-shedding infrastructure reliability concerns, generated software demand from private commercial charging operators at Johannesburg and Cape Town retail parks whose operators require software capable of managing charging availability notifications during scheduled power outage windows — a functionality requirement unique to markets with systematic grid reliability challenges.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Deployment

- Cloud-Based

- On-Premise

By Application

- Network Management & Monitoring

- Energy Management & Grid Integration

- Billing & Payment Processing

- Reservations & User Management

By Charging Level

- DC Fast Charging (Level 3)

- AC Level 2

- AC Level 1

By End-User

- Commercial (Retail, Hospitality, Workplace)

- Public Charging Networks

- Residential & Multi-Family

- Fleet & Transportation

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.14 B |

| Forecast Revenue (2034) | USD 11.82 B |

| CAGR (2025-2034) | 20.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Deployment, (Cloud-Based, On-Premise), By Application, (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level, (DC Fast Charging (Level 3), AC Level 2, AC Level 1), By End-User, (Commercial (Retail, Hospitality, Workplace), Public Charging Networks, Residential & Multi-Family, Fleet & Transportation) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CHARGEPOINT HOLDINGS, SIEMENS AG (eMOBILITY), ABB LTD., DRIIVZ, SCHNEIDER ELECTRIC, AMPECO, EVBOX GROUP (ENGIE), ENEL X WAY, BLINK CHARGING, HUBJECT GMBH, EV CONNECT, SHELL RECHARGE SOLUTIONS (GREENLOTS), ELECTRIFY AMERICA, BP PULSE, VOLTERRA, MONTA, EV.ENERGY, ZAPTEC, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level (DC Fast Charging, AC Level 2, AC Level 1), By End-User (Commercial, Public Charging Networks, Residential, Fleet & Transportation), Industry Trends & Forecast 2026-2034")

, By Application (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level (DC Fast Charging, AC Level 2, AC Level 1), By End-User (Commercial, Public Charging Networks, Residential, Fleet & Transportation), Industry Trends & Forecast 2026-2034")

, By Application (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level (DC Fast Charging, AC Level 2, AC Level 1), By End-User (Commercial, Public Charging Networks, Residential, Fleet & Transportation), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Electric Vehicle Charging Management Software Market?

The Global Electric Vehicle Charging Management Software Market was valued at USD 1.77 Billion in 2024 and is projected to reach USD 11.82 Billion by 2034, growing at a CAGR of 20.9% from 2026 to 2034, driven by rising EV adoption, increasing deployment of smart charging infrastructure, AI-powered charging analytics, vehicle-to-grid (V2G) integration, dynamic load balancing technologies, and growing demand for cloud-based EV energy management platforms worldwide.

Who are the major players in the Electric Vehicle Charging Management Software Market?

CHARGEPOINT HOLDINGS, SIEMENS AG (eMOBILITY), ABB LTD., DRIIVZ, SCHNEIDER ELECTRIC, AMPECO, EVBOX GROUP (ENGIE), ENEL X WAY, BLINK CHARGING, HUBJECT GMBH, EV CONNECT, SHELL RECHARGE SOLUTIONS (GREENLOTS), ELECTRIFY AMERICA, BP PULSE, VOLTERRA, MONTA, EV.ENERGY, ZAPTEC, Others

Which segments covered the Electric Vehicle Charging Management Software Market?

By Deployment, (Cloud-Based, On-Premise), By Application, (Network Management & Monitoring, Energy Management & Grid Integration, Billing & Payment Processing, Reservations & User Management), By Charging Level, (DC Fast Charging (Level 3), AC Level 2, AC Level 1), By End-User, (Commercial (Retail, Hospitality, Workplace), Public Charging Networks, Residential & Multi-Family, Fleet & Transportation)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Electric Vehicle Charging Management Software Market

Published Date : 27 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date